|

市場調査レポート

商品コード

1693596

GRCクラッディング:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)GRC Cladding - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| GRCクラッディング:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

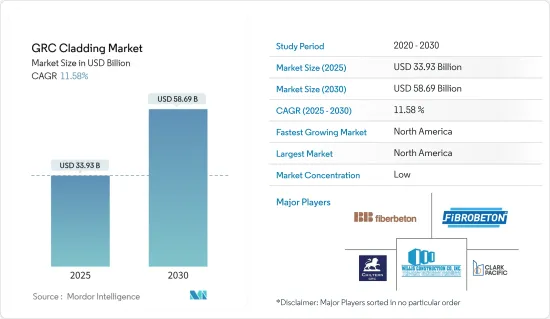

GRCクラッディングの市場規模は2025年に339億3,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは11.58%で、2030年には586億9,000万米ドルに達すると予測されます。

主なハイライト

- ガラスファイバー強化コンクリート(GRC)は、主に建築構造物の筋交いパネルとして使用される軽量クラッディングパネルです。繊維で補強されたコンクリートは、一般的なコンクリートと比較して環境改善につながるとしてよく紹介されます。

- GRCクラッディング市場は、グリーンビルディング(LEED評価)の重視の高まりによって牽引されており、優れた機械的特性が市場成長の原動力になると期待されています。米国では建築規制により、外壁材やクラッド材は延焼の媒体になってはならないと定められています。

- 米国と英国は、セメントの配合が燃焼の危険を冒すかどうかについて厳しいガイドラインを定めています。そのため、外壁材にはより耐火性の高い材料が求められるようになりました。

- GRCは、ポリマーと繊維の特殊配合により、不浸透性、耐候性、難燃性に優れているため、耐火性と不燃性に効果的です。

- GRCには、他の材料にはないさまざまな利点があります。GRCは、より軽く、より強く、より柔軟で、より耐久性があり、耐火性に優れた、本当に素晴らしい代替セメントです。

- GRCはその性質上、ロックウールを塗布することで遮熱、遮水、遮音効果を発揮します。この特性により、極端な気象条件の地域では需要が高まる可能性があります。

- クラッディングパネルのような大型のGRC製品は、スプレーを使って製造されます。吹き付けGRCは一般に、プレミックス振動鋳造GRCよりも強度が高いです。

- 急速に顕在化しつつある気候変動による緊急事態を受け、住宅建築物の耐震性を向上させるため、カナダ国家調査委員会は国家建築基準法(2025年)に極端な気象現象に耐える気候変動に強い建築物のガイドラインを導入しました。

GRCクラッディング市場の動向

商業空間の需要急増が市場を牽引

最近の調査によると、オフィススペースの需要は2024年末までに12~18%増加します。この成長は、今年度、オフィステナントの緩やかな復帰、マクロ経済環境の改善によって牽引されると予想されます。

最近の銀行危機は、商業用不動産に長い影を落としています。米国の地方銀行は、「システム上重要な」同業他社の規制を受けず、商業用不動産を担保に積極的な融資を行ってきました。このため、不動産の苦境と銀行の破綻が互いに補強し合うという「破滅のループ」シナリオが懸念されています。不動産市場の多くはアウトパフォームを続けているため、これは奇想天外に思えるかもしれないです。しかし、これはどちらも他方を崩壊させることはできないからです。オルタナティブ・レンダーやプライベート・エクイティが話題になっているが、銀行融資(商業用不動産融資全体の50%から60%を占め続けている)の引き下げは、今後数年間に返済が必要となる巨額の負債を考えると、得策ではないです。リファイナンスはすでに困難な状況にあり、与信基準の厳格化に伴い、さらに困難な状況になる可能性が高いです。

米国市場には景気循環や構造的な問題など多くの課題があるが、他地域のオフィス稼働率については楽観視できる理由が多いです。例えば、欧州では、オフィスの平均稼働率は2022年の43%から55%に回復し、週半ばの稼働率はCOVID-19以前の平均(70%)に近づいています。多くのアジア太平洋市場(ソウル、東京など)では、オフィス稼働率はパンデミック前の水準にほぼ戻っています。アジア太平洋では、質の高いビルの供給が限られているため、空室率は低く保たれ、賃料は上昇しています。

インドでは、2023年第1四半期の供給が前年同期比で23%減少したにもかかわらず、商業スペースの供給は回復し、2023年第3四半期には約4,700万~4,900万平方フィートに達すると予測されました。純吸収量に基づくと、2023年の供給量はパンデミック前の2017年から2019年の平均を上回ると予測されました。2024年の供給量は年率22%増の5,800万~6,000万平方フィートと予測されます。質への逃避が、機関投資家オーナーと既存デベロッパービルへの需要の二極化を促進します。

北米が市場を独占する見通し

倉庫・流通業は商業分野の中でも需要が高く、近年は米国の商業投資の半分以上を占めるまでに増加しています。

オフィス市場が引き続き活況を呈する中、今後のリーシング活動は、最も人気の高いサブマーケットやクラスAビルの小規模スペースに集中する可能性が高いです。大型店舗はスペースを集約し、eコマースやインフラへの投資を進めています。

ヘルスケアの建設支出は2023年まで高水準を維持し、大規模な病院拡張と外来患者および医療オフィスの需要回復がその原動力となりました。大規模プロジェクトは、最近の人口動態の変化、キャパシティ、メンテナンスニーズ、医療サービスに影響を与える新技術(ウェアラブルや遠隔医療など)に支えられました。

大規模な新設施設では、プロジェクトのスケジュールと予算を合理化するため、プレハブ化やモジュール化がますます進むと予想されます。これとは対照的に、専門医療施設や介護施設(SCH)は、依然として資源に大きな制約を受けており、建設活動が制限されています。

教会の閉鎖は開館を上回るペースで進んでおり、改築や再利用の新たな機会が生まれています。インフラと交通機関への投資は、最も競争の激しい市場のいくつかで、娯楽・レクリエーション施設の建設への支出を支えると思われます。

GRCクラッディング産業の概要

本レポートでは、GRCクラッディング市場で事業を展開する主要な国際企業を取り上げています。市場は非常に断片化されており、大企業が大きな市場シェアを占めています。主要企業は協業、技術革新、事業拡大、受賞・評価、その他の戦略に取り組み、提供サービスの向上と競争力の維持に努めています。

GRC被覆材市場の主要企業には、UltraTech Cement Ltd、Clark Pacific、BB Fiberbeton、Asahi Building-wall、Willis Construction Co. Inc.、Loveld、Fibrobeton、GB Architectural Cladding Products Ltd、Ibstock Telling、BCM GRC Limitedなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 市場概要

- 市場促進要因

- 市場を牽引する住宅セグメントの需要増加

- 都市化の進展が市場を牽引

- 市場抑制要因

- 市場成長の妨げとなる賃料の増加

- 市場機会

- 市場を牽引する建設業界の成長

- サプライチェーン/バリューチェーン分析への洞察

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 政府の規制と取り組み

- 技術動向

- COVID-19の市場への影響

第5章 市場セグメンテーション

- 用途別

- 商業建設

- 住宅建設

- インフラ建設

- 地域別

- アジア太平洋地域

- 北米

- 欧州

- 南米

- 中東・アフリカ

第6章 競合情勢

- 市場集中の概要

- 企業プロファイル

- UltraTech Cement Ltd

- Clark Pacific

- BB Fiberbeton

- ASAHI BUILDING-WALL CO. LTD

- Willis Construction Co. Inc.

- Loveld

- Fibrobeton

- GB Architectural Cladding Products Ltd

- Ibstock Telling

- BCM GRC Limited

- その他の企業

第7章 市場の将来

第8章 付録

The GRC Cladding Market size is estimated at USD 33.93 billion in 2025, and is expected to reach USD 58.69 billion by 2030, at a CAGR of 11.58% during the forecast period (2025-2030).

Key Highlights

- Glass-reinforced concrete cladding (GRC) is a lightweight cladding panel primarily used as fascia panels in building structures. Concrete, reinforced with fibers, is often presented as an environmental improvement compared to typical concrete.

- The GRC cladding market is driven by the increased emphasis on green buildings (LEED ratings), and superior mechanical characteristics are expected to drive the market's growth. In the United Kingdom, building regulations state that the materials used for external wall construction or wall cladding should not be a medium for spreading fire.

- The United States and the United Kingdom have stringent guidelines on whether cement formulations can run the risk of combustion. This increased the need for a more fire-resistant material for wall cladding.

- GRC is effective at fire resistance and incombustibility because the mix's special blend of polymers and fibers makes it impermeable, weather-resistant, and fire-retardant.

- GRC has many different advantages that come with its use over other materials. It is a genuinely amazing cement alternative that is lighter, stronger, more flexible, more durable, and fire-resistant.

- Due to its nature, GRC, water, and sound insulation provide thermal insulation by applying rock wool. This property may lead to increased demand in regions with extreme weather conditions.

- Larger GRC products, like cladding panels, are manufactured using a spray. Sprayed GRC is generally stronger than premix vibration-cast GRC.

- In the wake of the rapidly emerging climate change emergency and to help improve resiliency in residential buildings, the National Research Council, Canada, has introduced guidelines in the National Building Code (2025) for climate-resilient construction to withstand extreme weather events.

GRC Cladding Market Trends

The Surge in the Demand for Commercial Spaces is Driving the Market

According to a recent study, the demand for office space will increase by 12-18% by the end of 2024. The growth is expected to be driven by the current fiscal year, the gradual return of office tenants, and the improving macroeconomic environment.

The recent banking crisis has cast a long shadow on commercial real estate. Unburdened by the regulations of their larger 'systemically important' peers, US regional banks have been aggressively lending against commercial property. This raises the specter of a 'doom-loop' scenario, where real estate woes and banking failures reinforce each other. This may seem far-fetched, as much of the real estate market continues to outperform. However, this is because neither can bring the other down. For all the talk of alternative lenders and private equity, a pullback on bank lending (which continues to account for 50% to 60% of total commercial real estate lending) is ill-advised, given the massive amounts of debt that will need to be repaid over the next several years. Refinancing has already been challenging, and it is only likely to become more so as credit standards tighten.

While there are many challenges to the US market in terms of cyclicality and structural issues, there are many reasons to be optimistic about office occupancies in other regions. For example, in Europe, average office occupancies recovered to 55% compared to 43% in 2022, and midweek rates are now close to the pre-COVID-19 average (70%). In many Asia-Pacific markets (Seoul, Tokyo, etc.), office attendance is almost back to where it was before the pandemic. In Asia-Pacific, a limited supply of high-quality buildings keeps vacancy low and pushes up rents.

In India, despite a year-over-year decline of 23% in supply in Q1 2023, the supply of commercial spaces was projected to pick up and reach around 47-49 million square feet by Q3 2023. Based on net absorption, the 2023 supply was projected to be above the average of 2017-2019 before the pandemic. In 2024, supply is projected to grow by 22% yearly to 58-60 million square feet. A flight to quality drives demand polarization toward institutional owners and established developer buildings.

North America is Expected to Dominate the Market

Warehouse and distribution, a commercial segment, is in high demand and has increased in recent years to account for more than half of US commercial investment.

As the office market continues to boom, future leasing activity will likely focus on smaller spaces in the most sought-after submarkets and class-A buildings. Big-box stores are consolidating their space and investing in e-commerce offerings and infrastructure.

Healthcare construction spending remained high through 2023, driven by large-scale hospital expansions and outpatient and medical office demand recovery. Large-scale projects were supported by recent changes in demographics, capacity, maintenance needs, and new technologies that affect health services (such as wearables and telehealth).

Large-scale new facilities are expected to increasingly use prefabrication and modularization to streamline project schedules and budgets. In contrast, specialty care and nursing home (SCH) facilities remain heavily constrained by resources, limiting construction activity.

Churches are closing at a faster rate than they are opening, which is creating new opportunities for renovation or repurposing. Investments in infrastructure and transportation will support spending on the construction of amusement and recreational facilities in some of the most competitive markets.

GRC Cladding Industry Overview

The report covers major international players operating in the GRC cladding market. The market is highly fragmented, with large companies claiming significant market share. Key players engage in collaborations, innovations, business expansion, awards and recognition, and other strategies to improve their offerings and remain competitive.

Some of the key players in the GRC cladding market are UltraTech Cement Ltd, Clark Pacific, BB Fiberbeton, Asahi Building-wall Co. Ltd, Willis Construction Co. Inc., Loveld, Fibrobeton, GB Architectural Cladding Products Ltd, Ibstock Telling, BCM GRC Limited, etc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand in the Residential Segment Driving the Market

- 4.2.2 Increasing Urbanization Driving the Market

- 4.3 Market Restraints

- 4.3.1 Increasing Rents Hindering the Growth of the Market

- 4.4 Market Opportunities

- 4.4.1 Growing Construction Industry Driving the Market

- 4.5 Insights into Supply Chain/Value Chain Analysis

- 4.6 Industry Attractiveness - Porter's Five Force Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Government Regulations and Initiatives

- 4.8 Technological Trends

- 4.9 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Application

- 5.1.1 Commercial Construction

- 5.1.2 Residential Construction

- 5.1.3 Infrastructure Construction

- 5.2 By Geography

- 5.2.1 Asia-Pacific

- 5.2.2 North America

- 5.2.3 Europe

- 5.2.4 South America

- 5.2.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 UltraTech Cement Ltd

- 6.2.2 Clark Pacific

- 6.2.3 BB Fiberbeton

- 6.2.4 ASAHI BUILDING-WALL CO. LTD

- 6.2.5 Willis Construction Co. Inc.

- 6.2.6 Loveld

- 6.2.7 Fibrobeton

- 6.2.8 GB Architectural Cladding Products Ltd

- 6.2.9 Ibstock Telling

- 6.2.10 BCM GRC Limited*

- 6.3 Other Companies