|

市場調査レポート

商品コード

1693557

中国の肥料:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)China Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国の肥料:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 299 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

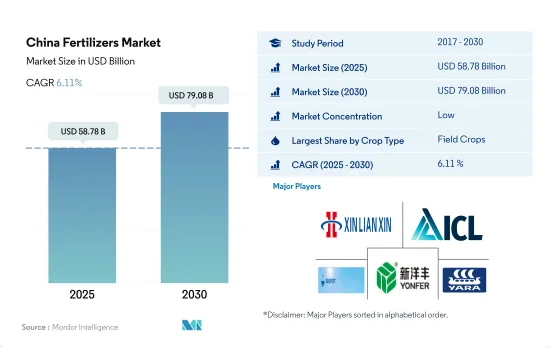

中国の肥料市場規模は2025年に587億8,000万米ドルと推定・予測され、2030年には790億8,000万米ドルに達し、予測期間中(2025~2030年)のCAGRは6.11%で成長すると予測されます。

肥料使用を必要とする集約栽培と単一栽培

- 輪作を伴わない長期にわたる継続的な耕作により、農地の肥沃度は枯渇し、不足が深刻化しており、特に中国南部では肥料の必要性が高まっています。環境汚染に対する懸念の高まりから、畑作物ではサステイナブル肥料に対する需要が高まっている

- 畑作物は多くの場合、最大の窒素肥料を利用します。広範な栽培により、穀物や穀類は土壌養分を枯渇させるため、それを補うために追加の肥料散布が必要となります。2022年の畑作物肥料市場全体のうち、プラクティス肥料が約73.3%、特殊肥料が約26.7%を占めています。

- 園芸作物は一年中栽培され、スプリンクラーや点滴灌漑のような優れた散水方法の恩恵を受け、水溶性肥料や液体肥料の使用を促すため、畑作物よりも特殊肥料を多く利用します。2021年には、園芸作物に使用される肥料の市場規模の約18.7%が特殊肥料で占められていました。

- 2022年には、国内の肥料市場全体のうち、芝生や観賞用の製品で構成される割合は1%以下となります。近年、政府は自給自足に重点を置き、温室での観賞用花の生産など、多くの方法を確立し、このセグメントの成長を支えることが期待されています。

- そのため、2023~2030年にかけては、畑作物の需要増と、観賞用花の輸入を減らすための自給率重視の高まりにより、部門による成長が押し上げられると予測されます。中国は肥料の主要生産国です。

中国の肥料市場動向

中国の栽培面積の拡大は、食糧需要の増加と主食の自給達成目標による。

- 中国では、畑作物の栽培面積は2017年の1億3,050万ヘクタールから2021年には1億2,780万ヘクタールに減少し、総栽培面積の71.4%を占めます。畑作物のシェアはトウモロコシが34.2%を占め、次いでコメが23.6%、小麦が18.3%となっています。この耕作面積の拡大が、同国の肥料需要を押し上げると予測されます。

- 中国は通常、畑作物の生産を夏/春(4月~9月)と冬の2シーズンに分けています。春作には早生トウモロコシ、早生コメ、早生小麦、綿花が含まれ、冬作は冬小麦と菜種が中心です。しかし、米とトウモロコシは中国の農業の中で優先され、中国の穀物生産量の3分の1を占めています。世界有数のコメ生産国として、中国は2022年に3,000万ヘクタールを稲作に割り当て、2億1,000万トンの収穫を見込んでいます。主要な米生産地域は黒龍江省、湖南省、江西省、湖北省、江蘇省、四川省、広西チワン族自治区、広東省、クラウド南省です。2022~23年の中国のトウモロコシ生産量は、主に収穫量の改善により、前年比460万トン増の2億7,720万トンに達すると予測されています。東北部の黒龍江省、吉林省、内モンゴル自治区は主要なトウモロコシ生産地域として際立っています。

- 春が主要な作期であることに変わりはないが、特に6月と7月の暑い時期には課題に直面します。中国の数百万人の主食である米は、特に影響を受けています。高温と降水量の少なさが重なると、土壌のミネラル不足が深刻化し、肥料の施用量を増やす必要があります。こうした乾燥した気象条件は、作物の収量にもリスクをもたらします。

世界の農地から排出される亜酸化窒素の約28%は、中国の農地から排出されています。

- 一次栄養素は、酵素活性などの生化学的プロセスを強化し、植物細胞の成長を促進します。これらの栄養素の欠乏は、植物の健康、発育、作物収量に大きな影響を与えます。2022年、畑作物における窒素、カリウム、リンを合わせた平均施用量は159.9kg/ヘクタールでした。具体的には、窒素がこの平均の65.23%、リンが28.07%、カリウムが6.68%を占めます。

- 窒素は、葉緑素やアミノ酸の構成成分として植物の代謝に重要な役割を果たし、一次栄養素の中でトップを占めています。2022年の平均施用量は279.65kg/ヘクタールでした。カリは105.3kg/ヘクタールでこれに続き、リンは94.9kg/ヘクタールでわずかに及ばなかりました。窒素とリンによる地表水と地下水の汚染は、農業従事者に対する施肥量の指導が不十分であったことに起因しています。注目すべきは、世界の農地からの亜酸化窒素排出量の約28%が中国に由来していることです。

- 2022年には、綿花、小麦、トウモロコシ、コメが、平均養分施用量が最も多い作物として浮上し、それぞれ255.41kg/ヘクタール、232.25kg/ヘクタール、198.44kg/ヘクタール、157.76kg/ヘクタールという数字でした。中国は綿花生産で世界をリードし、2022年には640万トンという驚異的な生産量を記録しました。また、綿花の最大の消費国であり輸入国でもあります。印象的なことに、中国は世界の綿花消費量の約20%を占め、その84%は新疆ウイグル自治区で生産されたものです。

- 増加する人口のニーズを満たすことが急務であることから、2023~2030年にかけて、畑作物への一次栄養素の施用が増加すると予想されています。

中国の肥料産業概要

中国の肥料市場は細分化されており、上位5社で12.84%を占めています。この市場の主要企業は、Henan XinlianXin Chemicals Group Company Limited、ICL Group Ltd、Sinofert Holdings Limited、Xinyangfeng Agricultural Technology、Yara International ASAなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 主要作物の作付面積

- 畑作物

- 園芸作物

- 平均養分施用率

- 微量栄養素

- 畑作物

- 園芸作物

- 一次栄養素

- 畑作物

- 園芸作物

- 二次多量栄養素

- 畑作物

- 園芸作物

- 微量栄養素

- 灌漑農地

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- タイプ

- 複合型

- ストレート

- 微量栄養素

- ホウ素

- 銅

- 鉄

- マンガン

- モリブデン

- 亜鉛

- その他

- 窒素

- 尿素

- その他

- リン酸

- DAP

- MAP

- SSP

- TSP

- その他

- ポタシス

- MoP

- SoP

- その他

- 二次栄養素

- カルシウム

- マグネシウム

- 硫黄

- 形態

- 従来型

- 特殊

- CRF

- 液体肥料

- SRF

- 水溶性

- 施肥モード

- 施肥

- 葉面散布

- 土壌

- 作物タイプ

- 畑作物

- 園芸作物

- 芝・観賞用

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Coromandel International Ltd.

- Grupa Azoty S.A.(Compo Expert)

- Hebei Monband Water Soluble Fertilizer Co. Ltd

- Hebei Sanyuanjiuqi Fertilizer Co., Ltd.

- Henan XinlianXin Chemicals Group Company Limited

- ICL Group Ltd

- Sinofert Holdings Limited

- Sociedad Quimica y Minera de Chile SA

- Xinyangfeng Agricultural Technology Co., Ltd.

- Yara International ASA

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

The China Fertilizers Market size is estimated at 58.78 billion USD in 2025, and is expected to reach 79.08 billion USD by 2030, growing at a CAGR of 6.11% during the forecast period (2025-2030).

Intensive cultivation and monoculture necessitating the fertilizers use

- Due to continuous long-term cultivation without crop rotation, farmland fertility has been depleted and has become more deficient, increasing the need for fertilizers, especially in South China. Due to growing concerns about environmental pollution, there is a rising demand for sustainable fertilizers in field crops.

- Field crops often utilize the greatest nitrogen fertilizers. Due to their extensive cultivation, grains and cereals deplete soil nutrients, requiring the application of additional fertilizers to make up for it. Conventional fertilizers accounted for about 73.3%, and specialty fertilizers accounted for about 26.7% of the total field crops fertilizer market value in 2022.

- Horticultural crops utilize more specialty fertilizers than field crops since they are grown all year long and benefit from superior watering methods like sprinkler and drip irrigation, which encourage the use of water-soluble and liquid fertilizers. About 18.7% of the market value of fertilizers used in horticultural crops was made up of specialty fertilizers in 2021.

- In 2022, less than 1% of the country's total fertilizer market was made up of turf and ornamental products. Over recent years, the government put greater emphasis on self-sufficiency and established a number of methods, such as the production of ornamental flowers in greenhouses, which are expected to support sectoral growth.

- Therefore, it is projected that the segmental growth will be boosted throughout 2023-2030 due to the rising demand from field crops and increased focus on self-sufficiency to reduce the import of ornamentals. The country is the leading producer of fertilizers.

China Fertilizers Market Trends

China's expanding cultivation area is driven by increased food demand and goal to achieve self-sufficiency in staple food

- In China, the cultivation area for field crops decreased from 130.5 million hectares in 2017 to 127.8 million hectares in 2021, representing 71.4% of the total cultivated area. Corn dominated the field crop landscape with a share of 34.2%, followed by rice and wheat at 23.6% and 18.3%, respectively. This expanding cultivation area is projected to drive up fertilizer demand in the country.

- China typically divides its field crop production into two seasons: summer/spring (April-September) and winter. Spring crops encompass early corn, early rice, early wheat, and cotton, while winter crops focus on winter wheat and rapeseed. Rice and corn, however, take precedence in China's agricultural landscape, accounting for a third of the nation's grain output. As the world's leading rice producer, China allocated 30 million hectares for rice farming in 2022, yielding a harvest of 210 million tonnes. Key rice-producing regions span Heilongjiang, Hunan, Jiangxi, Hubei, Jiangsu, Sichuan, Guangxi, Guangdong, and Yunan. China's corn production for 2022-23 is projected to hit 277.2 million tonnes, up by 4.6 million tonnes from the previous year, primarily due to improved harvests. The Northeast provinces of Heilongjiang, Jilin, and Inner Mongolia stand out as major corn-growing regions.

- While spring remains the primary cropping season, it faces some challenges, particularly during the hotter months of June and July. Rice, a staple for millions in China, is particularly affected. The combination of high temperatures and low precipitation exacerbates mineral depletion in the soil, necessitating higher fertilizer application. These dry weather conditions also pose a risk to crop yields.

About 28% of nitrous oxide emissions from cropland in the world are from China's agricultural lands

- Primary nutrients enhance biochemical processes, such as enzyme activity, and foster plant cell growth. Deficiencies in these nutrients can significantly impact plant health, development, and crop yields. In 2022, the average application rate for nitrogen, potassium, and phosphorus combined in field crops stood at 159.9 kg/hectare. Specifically, nitrogen accounted for 65.23%, phosphorus for 28.07%, and potassium for 6.68% of this average.

- Nitrogen takes the lead among primary nutrients, playing a vital role in plant metabolism as a constituent of chlorophyll and amino acids. Its average application rate in 2022 was 279.65 kg/hectare. Potash followed with 105.3 kg/hectare, and phosphorus trailed slightly at 94.9 kg/hectare. The contamination of surface and groundwater with nitrogen and phosphorus has been attributed to inadequate guidance on fertilizer application rates for farmers. Notably, around 28% of global nitrous oxide emissions from croplands originate from China.

- In 2022, cotton, wheat, corn, and rice emerged as the crops with the highest average nutrient application rates, with figures of 255.41 kg/hectare, 232.25 kg/hectare, 198.44 kg/hectare, and 157.76 kg/hectare, respectively. China led the world in cotton production, with a staggering 6.4 million metric tons in 2022. It also held the title of the largest consumer and importer of cotton. Impressively, China accounted for about 20% of global cotton consumption, with a significant 84% of its production hailing from Xinjiang.

- Given the imperative to meet the needs of a growing population, there is an anticipated increase in the application of primary nutrients in field crops between 2023 and 2030.

China Fertilizers Industry Overview

The China Fertilizers Market is fragmented, with the top five companies occupying 12.84%. The major players in this market are Henan XinlianXin Chemicals Group Company Limited, ICL Group Ltd, Sinofert Holdings Limited, Xinyangfeng Agricultural Technology Co., Ltd. and Yara International ASA (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Type

- 5.1.1 Complex

- 5.1.2 Straight

- 5.1.2.1 Micronutrients

- 5.1.2.1.1 Boron

- 5.1.2.1.2 Copper

- 5.1.2.1.3 Iron

- 5.1.2.1.4 Manganese

- 5.1.2.1.5 Molybdenum

- 5.1.2.1.6 Zinc

- 5.1.2.1.7 Others

- 5.1.2.2 Nitrogenous

- 5.1.2.2.1 Urea

- 5.1.2.2.2 Others

- 5.1.2.3 Phosphatic

- 5.1.2.3.1 DAP

- 5.1.2.3.2 MAP

- 5.1.2.3.3 SSP

- 5.1.2.3.4 TSP

- 5.1.2.3.5 Others

- 5.1.2.4 Potassic

- 5.1.2.4.1 MoP

- 5.1.2.4.2 SoP

- 5.1.2.4.3 Others

- 5.1.2.5 Secondary Macronutrients

- 5.1.2.5.1 Calcium

- 5.1.2.5.2 Magnesium

- 5.1.2.5.3 Sulfur

- 5.2 Form

- 5.2.1 Conventional

- 5.2.2 Speciality

- 5.2.2.1 CRF

- 5.2.2.2 Liquid Fertilizer

- 5.2.2.3 SRF

- 5.2.2.4 Water Soluble

- 5.3 Application Mode

- 5.3.1 Fertigation

- 5.3.2 Foliar

- 5.3.3 Soil

- 5.4 Crop Type

- 5.4.1 Field Crops

- 5.4.2 Horticultural Crops

- 5.4.3 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Coromandel International Ltd.

- 6.4.2 Grupa Azoty S.A. (Compo Expert)

- 6.4.3 Hebei Monband Water Soluble Fertilizer Co. Ltd

- 6.4.4 Hebei Sanyuanjiuqi Fertilizer Co., Ltd.

- 6.4.5 Henan XinlianXin Chemicals Group Company Limited

- 6.4.6 ICL Group Ltd

- 6.4.7 Sinofert Holdings Limited

- 6.4.8 Sociedad Quimica y Minera de Chile SA

- 6.4.9 Xinyangfeng Agricultural Technology Co., Ltd.

- 6.4.10 Yara International ASA

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms