|

市場調査レポート

商品コード

1693544

アフリカの肥料:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Africa Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アフリカの肥料:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 296 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

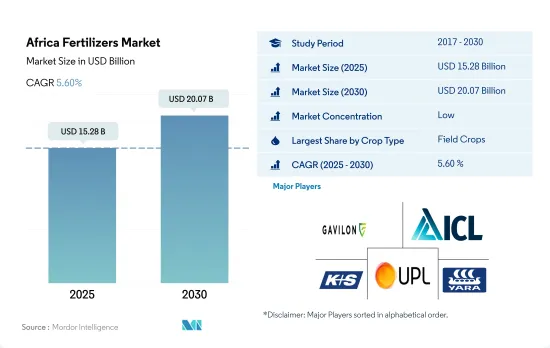

アフリカの肥料市場規模は2025年に152億8,000万米ドルと推定・予測され、2030年には200億7,000万米ドルに達し、予測期間中(2025~2030年)にCAGR 5.60%で成長すると予測されます。

それぞれの作物タイプにおける肥料の用途は、増加する人口を養うための食糧需要の増加により、2023~2030年にかけて拡大すると予測されます。

- 2022年、アフリカの肥料消費量は畑作物が圧倒的に多く、全体の71.1%を占めました。これは消費量1,550万トン、金額にして118億米ドルに相当します。

- 園芸作物がこれに続き、アフリカの肥料消費量の28.7%を占め、2022年には47億7,000万米ドルとなります。消費量は9,000トンと控えめであったが、園芸作物の栽培面積は2017年の3,650万ヘクタールから2022年には3,770万ヘクタールに拡大しました。この成長の原動力となったのは、隠れた飢餓や栄養不良が懸念されるなか、果物や野菜といった高価値作物への需要が高まったことです。このような栽培面積の急増は、生産性向上の必要性を強調し、園芸作物への肥料散布を増加させています。

- 主に国際市場におけるアフリカの花卉需要に牽引される芝・観賞用作物は、2021年のアフリカの肥料消費量の8.9%を占めました。これは市場規模7億7,060万米ドル、消費量150万トンに相当します。

- しかし2022年には、アフリカの肥料消費量に占める芝生・観賞用作物の割合はわずか0.02%に低下しました。このセグメントの市場規模は350万米ドルで、消費量は4,500トンです。従来型肥料が市場の57.0%を占め、特殊肥料が残りの43.0%を占めています。

- 作物タイプを問わず肥料の使用量は増加すると予想されます。この成長の原動力は、急増する人口の食糧需要を満たし、より高い収量を達成し、作物の生産性を向上させる必要性にあります。

南アフリカはアフリカ大陸の主要な農業生産国のひとつであり、輸入に依存しています。

- アフリカには窒素、リン酸、カリの膨大な鉱物資源が埋蔵されており、世界の肥料市場における主要企業となる可能性を秘めています。この地域の急速な人口増加は、進化する食料消費パターンと所得の上昇と相まって、農業生産の増加の必要性を促しています。その結果、肥料需要の増加が見込まれます。

- 2022年には、ナイジェリアがアフリカの肥料市場の36.7%を占め、アフリカの肥料市場を独占しました。ナイジェリアは世界有数のコメ消費量を誇り、年間生産量は700万トンです。同国の経済成長は主に農業部門に支えられており、今後数年間はCAGR 5.5%を維持すると予測されています。

- 主要国であるにもかかわらず、ナイジェリアの肥料使用量は比較的低く、1ヘクタール当たり20キログラム以下です。これは、肥料の施用量を増やす潜在的な可能性が大きく、市場のさらなる成長を促す可能性があることを示しています。これに対し、エジプトや南アフリカのような国々は、すでにナイジェリアの使用量を大幅に上回っており、ナイジェリアが追いつくには約500%の飛躍が必要であることを示唆しています。

- アフリカの主要農業国である南アフリカは、肥料の輸入に大きく依存しています。カリ肥料はすべて国内で消費されているが、窒素肥料は60%~70%が輸入されています。他の市場とは異なり、南アフリカの肥料セクタは規制緩和の中で運営されており、輸入関税や政府の制度は存在しないです。作物栽培の急増に伴い、南アフリカの肥料市場は大幅な成長を遂げ、2022年の17億7,000万米ドルから2030年には56億米ドルに拡大すると予測されています。

アフリカの肥料市場動向

この地域は農業生産を倍増させる可能性があり、消費需要の高まりにより畑作物の栽培面積が拡大すると予想されます。

- アフリカの農業生態学的ゾーンは、年2回の降雨がある密生した熱帯雨林から、降雨量の少ない乾燥した砂漠まで多岐にわたります。この地域の主要な畑作作物には、トウモロコシ、ソルガム、小麦、米が含まれます。2022年には、これらの作物の栽培面積は2億2,480万ヘクタールに達し、全農地の95%以上を占めました。

- 2018~19年シーズン、南アフリカのトウモロコシ農業従事者は、供給過剰による価格抑制に対応するため、作付面積を10%減らして210万ヘクタールとしました。その結果、国内のトウモロコシ生産量は1,300万トンから1,200万トンへと11%減少し、輸出量は250万トンから100万トンへと激減しました。このため、生産者はトウモロコシから油糧作物、なかでも大豆にシフトする可能性が高いです。このシフトにより、2018~2019年にかけてアフリカ全域でトウモロコシ栽培が全体的に減少すると予想されました。

- アフリカ最大のソルガム生産国はナイジェリアで、エチオピアが僅差でこれに続きます。ナイジェリアの穀物生産量の50%を占め、穀物栽培地の45%を占めるソルガムきびは、干ばつに強く、多様な土壌条件に適応する作物です。こうした特質から、ソルガムは特にアフリカの乾燥地帯で好まれる主食作物となっており、食糧と所得の安定を確保しています。

- ケニア、ソマリア、エチオピアの大部分は、深刻な食糧不足という差し迫った脅威に直面しています。過去10年間、アフリカの農業と耕作地は一貫して拡大しているにもかかわらず、食糧輸入への支出は3倍近くに増加しています。

窒素は、さまざまな畑作物に不可欠な重要な栄養素として際立っており、この地域では菜種が主要な栄養素消費国です。

- 菜種作物はカリウムとリンの施用率が最も高く、2022年にはそれぞれ162.4kg/ヘクタールと281.7kg/ヘクタールを占めます。一方、アフリカの畑作物の平均窒素施用量は、2022年には364.9kg/ヘクタールとなります。

- 2022年には、アフリカの畑作物は一次養分消費量全体の87.1%を占め、55万6,100トンに達しました。この優位性は、畑作物専用の広大な土地面積に起因しています。具体的には、これらの作物における窒素、リン、カリウムの平均養分施用量は、2022年にはそれぞれ223.2 kg/ha、125.3 kg/ha、155.3 kg/haでした。

- ナイジェリアのギニアサバンナは、トウモロコシ生産に適した環境条件を提供しています。しかし、このような可能性があるにもかかわらず、この地域の農業従事者は低い収量に苦しんでいます。その主要原因は、土地利用の激化による土壌の劣化と養分の枯渇(主に窒素)です。畑作物は、耕起、葉面積の拡大、穀粒の形成、充填、タンパク質合成の促進など、窒素には複数の利点があるため、窒素施用が優先されます。窒素はまた、穀物の収量と品質の向上にも重要な役割を果たしています。一次栄養素は作物の成長に不可欠であり、土壌の枯渇や窒素の溶出が懸念されることから、一次栄養素の施用率は今後数年間で大きく伸びると予想されます。

アフリカの肥料産業概要

アフリカの肥料市場はセグメント化されており、上位5社で7.43%を占めています。この市場の主要企業は、Gavilon South Africa(MacroSource、LLC)、ICL Group Ltd、K+S Aktiengesellschaft、UPL Limited、Yara International ASAなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 主要作物の作付面積

- 畑作物

- 園芸作物

- 平均養分施用率

- 微量栄養素

- 畑作物

- 園芸作物

- 一次栄養素

- 畑作物

- 園芸作物

- 二次多量栄養素

- 畑作物

- 園芸作物

- 微量栄養素

- 灌漑農地

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- タイプ

- 複合型

- ストレート

- 微量栄養素

- ホウ素

- 銅

- 鉄

- マンガン

- モリブデン

- 亜鉛

- その他

- 窒素

- 硝酸アンモニウム

- 尿素

- その他

- リン酸

- DAP

- MAP

- SSP

- TSP

- ポタシック

- MoP

- SoP

- 二次栄養素

- カルシウム

- マグネシウム

- 硫黄

- 形態

- 従来型

- 特殊

- CRF

- 液体肥料

- SRF

- 水溶性

- 施肥モード

- 施肥

- 葉面散布

- 土壌

- 作物タイプ

- 畑作物

- 園芸作物

- 芝・観賞用

- 生産国

- ナイジェリア

- 南アフリカ

- その他のアフリカ

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Foskor

- Gavilon South Africa(MacroSource, LLC)

- Haifa Group

- ICL Group Ltd

- K+S Aktiengesellschaft

- Kynoch Fertilizer

- UPL Limited

- Yara International ASA

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92609

The Africa Fertilizers Market size is estimated at 15.28 billion USD in 2025, and is expected to reach 20.07 billion USD by 2030, growing at a CAGR of 5.60% during the forecast period (2025-2030).

The application of fertilizers in the respective crop types is anticipated to grow during 2023-2030, owing to the increasing need for food to feed the growing populations

- In 2022, field crops dominated fertilizer consumption in Africa, representing 71.1% of the total. This translated to a volume consumption of 15.5 million metric tons, valued at USD 11.80 billion.

- Horticultural crops followed, accounting for 28.7% of Africa's fertilizer consumption, valued at USD 4.77 billion in 2022. Despite a modest volume consumption of 9.0 thousand metric tons, the cultivation area for horticultural crops expanded from 36.5 million hectares in 2017 to 37.7 million hectares in 2022. This growth was driven by rising demand for high-value crops, such as fruits and vegetables, amidst concerns of hidden hunger and malnutrition. This surge in cultivation areas underscores the need for enhanced productivity, driving up fertilizer application in horticultural crops.

- Turf & ornamental crops, primarily driven by the demand for African flowers in international markets, accounted for 8.9% of Africa's fertilizer consumption in 2021. This translated to a market value of USD 770.6 million and a volume consumption of 1.5 million metric tons.

- However, in 2022, the share of turf and ornamental crops in Africa's fertilizer consumption dropped to a mere 0.02%. The market value for this segment was USD 3.5 million, with a volume consumption of 4.5 thousand metric tons. Conventional fertilizers dominated the market, capturing a 57.0% share, while specialty fertilizers accounted for the remaining 43.0%.

- The application of fertilizers across crop types is expected to rise. This growth is driven by the need to meet the food demands of a burgeoning population, achieve higher yields, and enhance crop productivity.

South Africa is one of the major agriculture-producing countries in the continent and is import-dependent

- Africa's vast mineral reserves of nitrogen, phosphate, and potash position it as a potential major player in the global fertilizer market. The region's rapid population growth, coupled with evolving food consumption patterns and rising incomes, is driving a need for increased agricultural production. This, in turn, is expected to lead to an increase in fertilizer demand.

- In 2022, Nigeria dominated the African fertilizer market, accounting for 36.7% of the total. Nigeria boasts one of the world's highest rice consumption rates, with an annual production of 7 million metric tons. The country's economic growth, primarily propelled by the agricultural sector, is projected to sustain a CAGR of 5.5% in the coming years.

- Despite being a major player, Nigeria's fertilizer usage remains relatively low, at under 20kg/hectare. This indicates a significant untapped potential for increased fertilizer application, potentially driving further market growth. In comparison, countries like Egypt and South Africa have already surpassed Nigeria's usage by a significant margin, suggesting a potential leap of around 500% for Nigeria to catch up.

- South Africa, a key agricultural nation in Africa, heavily relies on fertilizer imports. While all potassic fertilizers are domestically consumed, a substantial 60%-70% of nitrogenous fertilizers are imported. Unlike some other markets, South Africa's fertilizer sector operates in a deregulated landscape, devoid of import tariffs or government schemes. With a surge in crop cultivation, the South African fertilizer market is projected to witness substantial growth, expanding from USD 1.77 billion in 2022 to USD 5.60 billion by 2030.

Africa Fertilizers Market Trends

The region has the potential to double its agricultural production, and the area under field crops is expected to expand due to the rising consumption demand

- The agroecological zones in Africa span from dense rainforests with bi-annual rainfall to arid deserts with minimal precipitation. Dominant field crops in the region include corn, sorghum, wheat, and rice. In 2022, the cultivation area for these crops reached 224.8 million hectares, accounting for over 95% of the total agricultural land.

- In the 2018-19 season, South African corn farmers reduced their planted area by 10% to 2.1 million hectares, responding to an oversupply that suppressed prices. Consequently, corn production in the country dipped by 11%, from 13 million to 12 million tonnes, and exports plummeted from 2.5 million to 1 million tonnes. In light of this, producers were likely to pivot from corn to oilseed crops, with soybeans being a favored choice. This shift was anticipated to lead to an overall decline in corn cultivation across Africa from 2018 to 2019.

- Nigeria takes the lead as the largest sorghum producer in Africa, closely followed by Ethiopia. Sorghum, accounting for 50% of Nigeria's cereal output and occupying 45% of its cereal cultivation land, is a drought-tolerant crop with adaptability to diverse soil conditions. These qualities make sorghum a preferred staple crop, particularly in Africa's drier regions, ensuring food and income security.

- Kenya, Somalia, and significant parts of Ethiopia face an imminent threat of severe food shortages. Over the past decade, Africa's spending on food imports nearly tripled despite a consistent expansion in its agricultural industry and cultivated land.

Nitrogen stands out as a crucial nutrient essential for various field crops, with rapeseed being the primary nutrient consumer in this region

- Rapeseed crops have the highest potassium and phosphorous application rates, accounting for 162.4 kg/hectare and 281.7 kg/hectare, respectively, in 2022. Meanwhile, the average nitrogen application rate for field crops in Africa stood at 364.9 kg/hectare in 2022.

- In 2022, field crops in Africa accounted for 87.1% of the total primary nutrient consumption, which amounted to 556.1 thousand metric tons. This dominance can be attributed to the extensive land area dedicated to field crops. Specifically, the average nutrient application rates for nitrogen, phosphorous, and potassium in these crops were 223.2 kg/ha, 125.3 kg/ha, and 155.3 kg/ha, respectively, in 2022.

- The Guinea savannas in Nigeria offer favorable environmental conditions for maize production. However, despite this potential, farmers in the region struggle with low yields. The primary culprits are soil degradation and nutrient depletion, primarily nitrogen, resulting from intensified land use. Field crops prioritize nitrogen application due to its multiple benefits, including promoting tillering, leaf area development, grain formation, filling, and protein synthesis. Nitrogen also plays a crucial role in enhancing both grain yield and quality. Given that primary nutrients are vital for crop growth and with concerns over soil depletion and nitrogen leaching, the application rates for primary nutrients are expected to witness significant growth in the coming years.

Africa Fertilizers Industry Overview

The Africa Fertilizers Market is fragmented, with the top five companies occupying 7.43%. The major players in this market are Gavilon South Africa (MacroSource, LLC), ICL Group Ltd, K+S Aktiengesellschaft, UPL Limited and Yara International ASA (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Type

- 5.1.1 Complex

- 5.1.2 Straight

- 5.1.2.1 Micronutrients

- 5.1.2.1.1 Boron

- 5.1.2.1.2 Copper

- 5.1.2.1.3 Iron

- 5.1.2.1.4 Manganese

- 5.1.2.1.5 Molybdenum

- 5.1.2.1.6 Zinc

- 5.1.2.1.7 Others

- 5.1.2.2 Nitrogenous

- 5.1.2.2.1 Ammonium Nitrate

- 5.1.2.2.2 Urea

- 5.1.2.2.3 Others

- 5.1.2.3 Phosphatic

- 5.1.2.3.1 DAP

- 5.1.2.3.2 MAP

- 5.1.2.3.3 SSP

- 5.1.2.3.4 TSP

- 5.1.2.4 Potassic

- 5.1.2.4.1 MoP

- 5.1.2.4.2 SoP

- 5.1.2.5 Secondary Macronutrients

- 5.1.2.5.1 Calcium

- 5.1.2.5.2 Magnesium

- 5.1.2.5.3 Sulfur

- 5.2 Form

- 5.2.1 Conventional

- 5.2.2 Speciality

- 5.2.2.1 CRF

- 5.2.2.2 Liquid Fertilizer

- 5.2.2.3 SRF

- 5.2.2.4 Water Soluble

- 5.3 Application Mode

- 5.3.1 Fertigation

- 5.3.2 Foliar

- 5.3.3 Soil

- 5.4 Crop Type

- 5.4.1 Field Crops

- 5.4.2 Horticultural Crops

- 5.4.3 Turf & Ornamental

- 5.5 Country

- 5.5.1 Nigeria

- 5.5.2 South Africa

- 5.5.3 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Foskor

- 6.4.2 Gavilon South Africa (MacroSource, LLC)

- 6.4.3 Haifa Group

- 6.4.4 ICL Group Ltd

- 6.4.5 K+S Aktiengesellschaft

- 6.4.6 Kynoch Fertilizer

- 6.4.7 UPL Limited

- 6.4.8 Yara International ASA

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms