|

市場調査レポート

商品コード

1693543

南米の肥料:市場シェア分析、産業動向、成長予測(2025年~2030年)South America Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 南米の肥料:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 315 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

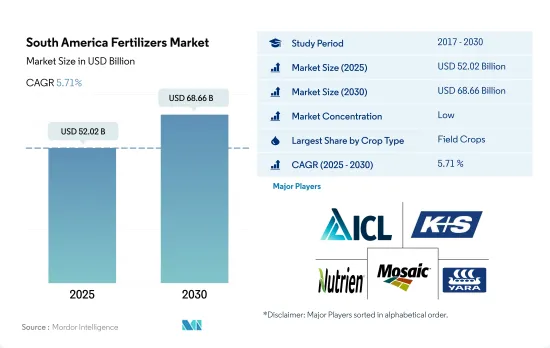

南米の肥料市場規模は2025年に520億2,000万米ドルと推定・予測され、2030年には686億6,000万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは5.71%で成長する見込みです。

気候パターンの変化と土壌養分不足の増加により、肥料市場は成長態勢にある

- 作物タイプによる肥料市場全体の金額は481億米ドルを占め、2023~2030年のCAGRは5.6%を記録すると推定されます。数量ベースでは、全体の消費量は6,400万トンを占め、2023~2030年のCAGRは3.3%を記録すると推定されます。

- 作物タイプ別では、畑作物が94.5%を占め、園芸作物が5.5%で続いています。園芸作物も畑作物も国の貿易と消費に欠かせない作物であり、国内外の需要の増加がこのセグメントの成長を後押ししています。

- 畑作物の栽培面積は、2023~2030年のCAGRで2.2%増加しています。同国では大豆、トウモロコシ、小麦などの重要な作物が栽培されており、国内需要を満たすために肥料を積極的に輸入しています。

- それに伴い、米国、チリ、ラテンアメリカ諸国間の自由貿易協定(FTA)が、過去数十年間における南米諸国の果物・野菜生産の増加の主要因となっています。NAFTA(USMCA)、CAFTA-DR、チリ、コロンビア、パナマ、ペルーなどの国々との二国間協定を含むこれらのFTAは、この地域の肥料需要をさらに押し上げると予想されます。

- 南米の肥料市場の成長は、増大する需要を満たし、作物の収量と品質を向上させ、生産量を増加させる必要性など、様々な要因によってもたらされています。その結果、市場規模は2023~2030年にかけてCAGR 3.3%を記録すると予想されます。

大豆のような主要作物の栽培面積が多いため、ブラジルの肥料消費量は高いシェアを占めています。

- 南米の国内肥料消費量の73.0%を占めるブラジルは、肥料使用量で同地域をリードしています。ブラジル市場を牽引しているのは主にプラクティス肥料で、2022年のシェアは95.2%と圧倒的でした。残りの4.8%は特殊肥料です。

- 小麦と大豆の世界的輸出国であるアルゼンチンは、農業がGDPに約5.9%寄与しています。2022年には、アルゼンチンは南米の肥料市場で14.6%のシェアを占めます。ブラジルと同様、プラクティス肥料が市場の96.1%を占め、特殊肥料は3.9%です。特殊肥料セグメントでは、液体肥料が44.7%でトップ、次いで水溶性肥料が52.6%でした。

- ブラジルとアルゼンチンを除くその他の南米は、2022年の肥料市場で14.8%のシェアを占めました。畑作物は数量ベースで83.1%の市場シェアを占め、2022年には815万トンに達しました。予測によると、この数量は2030年までに1,053万トンに増加し、大幅な成長軌道に乗る。

- 2022年の南米の肥料市場は、大豆、トウモロコシ、サトウキビを含む畑作作物が市場シェアの94.2%を占め、圧倒的な存在感を示しました。これらの作物は過去20年間に大幅な成長を遂げており、今後もさらなる成長が見込まれています。ブラジルのような国々が耕作面積を拡大し、より高い収量を目指していることから、この動向は今後も続くとみられます。

- 人口の増加とそれに伴う食糧穀物需要の急増に牽引され、南米では主要食糧作物の栽培面積が一貫して拡大しています。この動向は、2023~2030年にかけてこの地域の肥料市場が成長すると予測されることを示しています。

南米の肥料市場動向

自給自足を達成するための政府の取り組みが、畑作物の栽培面積の増加に大きく寄与しています。

- 南米における畑作物の栽培面積は顕著な増加を示し、2017年の1億1,160万haから2022年には1億2,610万haへと急増し、総面積の12.8%増を記録しました。このような栽培拡大は、同地域の肥料需要を押し上げると予測されます。畑作物が市場を独占し、96.8%の大きなシェアを占めています。2022年には、ブラジルが56.9%で最大シェアを占め、アルゼンチンが29.3%でこれに続きます。大豆生産と輸出の世界的リーダーとして知られるブラジルの大豆生産量は、2021年には約1億3,500万トンに達しました。そのうち82%を占める1億550万トンが輸出され、その82%は生大豆、16%は大豆ケーキ、2%は大豆油として輸出されます。

- 南米最大の栽培面積を誇る大豆は、主にブラジル(64.4%)とアルゼンチン(26.1%)で栽培されています。しかし、この地域は現在、長引く干ばつに悩まされており、主要河川の水位が危機的に低下しています。これは深刻な影響を及ぼし、収穫と重要な夏作物(特に大豆)の輸送の両方に支障をきたしています。その結果、このような状況は、南米における肥料施用量の増加需要を増幅させています。

- 旺盛な世界需要と良好な収益性に後押しされ、メルコスール地域の大豆栽培は急増しました。大豆価格の高騰は、他の原料とともに、生産者が新たな土地や設備に投資する動機付けとなり、事業の拡大や効率化を可能にしました。その結果、同地域の畑作物栽培面積は、国内と国際市場の成長に連動して拡大する態勢を整えています。

南米における畑作物の一次養分施用量の平均は約172.73kg/ヘクタールです。

- 過去20年間で、南米は畑作物生産の主要な担い手として台頭してきました。特に大豆、トウモロコシ、小麦、トウモロコシがそうです。この生産量の急増は、栽培面積の拡大と収量増加のための努力の強化の両方によるものです。特筆すべきは、ブラジルのような国々が耕作面積を積極的に拡大していることで、作物生産がさらに増加し、それに伴って肥料消費量も急増することを示しています。

- 栄養素は、植物の健康、作物の成長、作物の生産高にとって極めて重要です。一次栄養素、すなわち窒素、リン、カリウムは、植物の開発のための基本的なコンポーネントとしての役割を果たします。これらの栄養素が不足すると、作物の収量と品質の両方に大きな影響を与える可能性があり、畑作物にとっての重要性が浮き彫りになります。2022年、南米の畑作物への主要栄養素の平均施用量は172.7kg/ヘクタールでした。窒素が193.8kg/ヘクタールでトップ、カリウムが181.9kg/ヘクタールでこれに続きます。リンは142.4kg/ヘクタールとやや後塵を拝しました。

- 畑作物の中では、小麦、稲、トウモロコシ/メイズの平均養分施用量が最も多くなると予想されます。具体的には、小麦の平均養分施用量は231kg/ヘクタール、コメとトウモロコシの平均施用量はそれぞれ156kg/ヘクタールと149kg/ヘクタールになると予測されます。人口の増加とそれに伴う主要食糧作物への需要に牽引され、南米では収穫面積が拡大しています。この動向は、同地域における畑作物の一次養分使用量が今後数年間で大幅に増加することを示唆しています。

南米の肥料産業の概要

南米の肥料市場はセグメント化されており、上位5社で37.12%を占めています。この市場の主要企業は、ICL Group Ltd、K+S Aktiengesellschaft、Nutrien Ltd.、The Mosaic Company、Yara International ASAなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 主要作物の作付面積

- 畑作物

- 園芸作物

- 平均養分施用率

- 微量栄養素

- 畑作物

- 園芸作物

- 一次栄養素

- 畑作物

- 園芸作物

- 二次多量栄養素

- 畑作物

- 園芸作物

- 微量栄養素

- 灌漑農地

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- タイプ

- 複合型

- ストレート

- 微量栄養素

- ホウ素

- 銅

- 鉄

- マンガン

- モリブデン

- 亜鉛

- その他

- 窒素

- 硝酸アンモニウム

- 尿素

- その他

- リン酸

- DAP

- MAP

- SSP

- TSP

- その他

- ポタシス

- MoP

- SoP

- その他

- 二次栄養素

- カルシウム

- マグネシウム

- 硫黄

- 形態

- 従来型

- 特殊

- CRF

- 液体肥料

- SRF

- 水溶性

- 施肥モード

- 施肥

- 葉面散布

- 土壌

- 作物タイプ

- 畑作物

- 園芸作物

- 芝・観賞用

- 生産国

- アルゼンチン

- ブラジル

- その他の南米

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Fertgrow

- Grupa Azoty S.A.(Compo Expert)

- Haifa Group

- ICL Group Ltd

- K+S Aktiengesellschaft

- Nortox

- Nutrien Ltd.

- Sociedad Quimica y Minera de Chile SA

- The Mosaic Company

- Yara International ASA

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92608

The South America Fertilizers Market size is estimated at 52.02 billion USD in 2025, and is expected to reach 68.66 billion USD by 2030, growing at a CAGR of 5.71% during the forecast period (2025-2030).

The fertilizer market is poised for growth due to shifting climate patterns and rising soil nutrient deficiencies

- The overall fertilizer market value by crop type has accounted for USD 48.1 billion and is estimated to record a CAGR of 5.6% during 2023-2030. By volume, the overall consumption accounted for 64.0 million metric tons and is estimated to record a CAGR of 3.3% during 2023-2030.

- By crop type, field crops are dominating the market by 94.5%, followed by horticultural crops with 5.5% of fertilizer consumption value. Both horticultural and field crops are essential to the country's trade and consumption, and the increased domestic and international demand is bolstering the segment's growth.

- The area under field crop cultivation has increased by a CAGR of 2.2% during 2023-2030. With important crops being cultivated in the country, such as soybean, corn, and wheat, the country is actively importing fertilizers to meet the domestic demand, which is driving the growth of the segments.

- Accordingly, Free trade agreements (FTAs) between the United States, Chile, and several Latin American countries have been a major factor in the increase in fruit and vegetable production in South American countries over the last few decades. These FTAs, including NAFTA (USMCA), CAFTA-DR, and bilateral agreements with countries such as Chile, Colombia, Panama, and Peru, are expected to further boost fertilizer demand in the region.

- The growth of the South American fertilizers market is being driven by various factors, including the need to meet the growing demand, improve crop yield and quality, and increase production. As a result, the market volume is expected to register a CAGR of 3.3% from 2023 to 2030.

Due to higher cultivation areas under major crops like soybeans, fertilizer consumption in Brazil leads to a higher share

- Brazil, accounting for 73.0% of South America's domestic fertilizer consumption, leads the region in fertilizer usage. The Brazilian market is predominantly driven by conventional fertilizers, which held a commanding 95.2% share in 2022. Specialty fertilizers made up the remaining 4.8%.

- Argentina, a global exporter of wheat and soybeans, sees agriculture contributing around 5.9% to its GDP. In 2022, Argentina held a 14.6% share of the South American fertilizer market. Similar to Brazil, conventional fertilizers dominated, capturing 96.1% of the market, while specialty fertilizers accounted for 3.9%. Within the specialty segment, liquid fertilizers led at 44.7%, followed by water-soluble fertilizers at 52.6%.

- The Rest of South America, excluding Brazil and Argentina, held a 14.8% share of the regional fertilizer market in 2022. Field crops, commanding an 83.1% market share by volume, reached 8.15 million metric tons in 2022. Projections indicate this volume will climb to 10.53 million metric tons by 2030, representing a significant growth trajectory.

- Field crops, including soybeans, corn, and sugarcane, dominated the South American fertilizer market in 2022, capturing 94.2% of the market share. These crops have witnessed substantial growth over the past two decades, with further increases expected. Driven by countries like Brazil expanding their cultivated areas and aiming for higher yields, this trend is set to continue.

- Driven by a rising population and the subsequent surge in food grain demand, South America has witnessed a consistent expansion in the area dedicated to major food crops. This trend points to a projected growth in the region's fertilizer market during 2023-2030.

South America Fertilizers Market Trends

The government's initiatives to achieve self-sufficiency have significantly contributed to the increase in the area under field crop cultivation.

- The cultivation area for field crops in South America witnessed a notable rise, surging from 111.6 million ha in 2017 to 126.1 million ha in 2022, marking a 12.8% increase in the total area. This expansion in cultivation is projected to drive up the demand for fertilizers in the region. Field crops dominated the market, accounting for a significant 96.8% share. In 2022, Brazil held the maximum share of the market at 56.9%, with Argentina trailing at 29.3%. Brazil, renowned as the global leader in soy production and exports, saw its soy output reach nearly 135 million tonnes in 2021. Of this, a whopping 105.5 million tonnes, constituting 82%, were exported, with 82% in raw soybean form, 16% as soybean cake, and 2% as soybean oil.

- Soybean, commanding the largest cultivated area in South America, is primarily grown in Brazil (64.4%) and Argentina (26.1%). However, the region is currently grappling with an extended drought, leading to critically low water levels in major rivers. This has severe repercussions, hampering both harvests and the transportation of crucial summer crops, especially soybeans. Consequently, these conditions are amplifying the demand for increased fertilizer application in South America.

- Driven by robust global demand and favorable profitability, soybean cultivation in the Mercosur region witnessed a surge. The surge in soy prices, along with other raw materials, has incentivized producers to invest in new lands and equipment, enabling them to scale up operations and enhance efficiency. As a result, the field crop cultivation area in the region is poised to expand in tandem with the growing domestic and international markets.

The average rate of primary nutrient application for field crops in South America is about 172.73 kg/hectare

- Over the past two decades, South America has emerged as a key player in field crop production, notably for soybeans, corn, wheat, and maize. This surge in production can be attributed to both expanded cultivation and intensified efforts to boost yields. Notably, countries like Brazil are actively expanding their cultivated areas, indicating a further uptick in crop production and a subsequent surge in fertilizer consumption.

- Nutrients are pivotal for plant health, crop growth, and crop output. Primary nutrients, namely nitrogen, phosphorus, and potassium, serve as the fundamental building blocks for plant development. Any deficiency in these nutrients can significantly impact both crop yield and quality, underscoring their importance for field crops. In 2022, the average application rate of primary nutrients for field crops in South America stood at 172.7 kg/hectare. Nitrogen topped the list with an application rate of 193.8 kg/hectare, followed by potassium at 181.9 kg/hectare. Phosphorus trailed slightly behind, with an application rate of 142.4 kg/hectare.

- Among the field crops, wheat, rice, and corn/maize are expected to have the highest average nutrient application rate. Specifically, wheat is projected to have an average nutrient application rate of 231 kg/ha, while rice and corn/maize are estimated to have average rates of 156 kg/ha and 149 kg/ha, respectively. Driven by a growing population and subsequent demand for major food crops, South America has witnessed an expansion in harvested areas. This trend points to a significant uptick in primary nutrient usage for field crops in the region in the coming years.

South America Fertilizers Industry Overview

The South America Fertilizers Market is fragmented, with the top five companies occupying 37.12%. The major players in this market are ICL Group Ltd, K+S Aktiengesellschaft, Nutrien Ltd., The Mosaic Company and Yara International ASA (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Micronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.2 Primary Nutrients

- 4.2.2.1 Field Crops

- 4.2.2.2 Horticultural Crops

- 4.2.3 Secondary Macronutrients

- 4.2.3.1 Field Crops

- 4.2.3.2 Horticultural Crops

- 4.2.1 Micronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Type

- 5.1.1 Complex

- 5.1.2 Straight

- 5.1.2.1 Micronutrients

- 5.1.2.1.1 Boron

- 5.1.2.1.2 Copper

- 5.1.2.1.3 Iron

- 5.1.2.1.4 Manganese

- 5.1.2.1.5 Molybdenum

- 5.1.2.1.6 Zinc

- 5.1.2.1.7 Others

- 5.1.2.2 Nitrogenous

- 5.1.2.2.1 Ammonium Nitrate

- 5.1.2.2.2 Urea

- 5.1.2.2.3 Others

- 5.1.2.3 Phosphatic

- 5.1.2.3.1 DAP

- 5.1.2.3.2 MAP

- 5.1.2.3.3 SSP

- 5.1.2.3.4 TSP

- 5.1.2.3.5 Others

- 5.1.2.4 Potassic

- 5.1.2.4.1 MoP

- 5.1.2.4.2 SoP

- 5.1.2.4.3 Others

- 5.1.2.5 Secondary Macronutrients

- 5.1.2.5.1 Calcium

- 5.1.2.5.2 Magnesium

- 5.1.2.5.3 Sulfur

- 5.2 Form

- 5.2.1 Conventional

- 5.2.2 Speciality

- 5.2.2.1 CRF

- 5.2.2.2 Liquid Fertilizer

- 5.2.2.3 SRF

- 5.2.2.4 Water Soluble

- 5.3 Application Mode

- 5.3.1 Fertigation

- 5.3.2 Foliar

- 5.3.3 Soil

- 5.4 Crop Type

- 5.4.1 Field Crops

- 5.4.2 Horticultural Crops

- 5.4.3 Turf & Ornamental

- 5.5 Country

- 5.5.1 Argentina

- 5.5.2 Brazil

- 5.5.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Fertgrow

- 6.4.2 Grupa Azoty S.A. (Compo Expert)

- 6.4.3 Haifa Group

- 6.4.4 ICL Group Ltd

- 6.4.5 K+S Aktiengesellschaft

- 6.4.6 Nortox

- 6.4.7 Nutrien Ltd.

- 6.4.8 Sociedad Quimica y Minera de Chile SA

- 6.4.9 The Mosaic Company

- 6.4.10 Yara International ASA

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms