|

市場調査レポート

商品コード

1693520

二次多量栄養素肥料:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Secondary Macronutrients Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 二次多量栄養素肥料:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 322 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

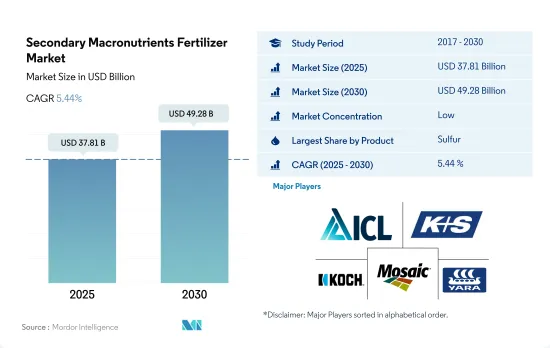

二次多量栄養素肥料の市場規模は2025年に378億1,000万米ドルと推定・予測され、2030年には492億8,000万米ドルに達し、予測期間(2025-2030年)のCAGRは5.44%で成長すると予測されます。

硫黄肥料の採用は他の二次多量栄養素よりも多い

- 2021年、硫黄は世界の二次多量栄養素肥料市場の42.6%を占めました。2021年、欧州の硫黄市場の金額は約11億9,000万米ドルでした。この市場において、特殊硫黄肥料の市場シェアは約49.4%、従来型硫黄肥料の市場シェアは約50.1%でした。特殊硫黄肥料の採用率は他の二次多量栄養素よりも高いです。特殊硫黄肥料市場は予測期間終了までに18億2,000万米ドルに達すると予想されます。

- マグネシウムは2021年に世界の二次多量栄養素肥料市場の48.9%を占めました。畑作物が88.8%と最大のシェアを占め、次いで芝生・観賞用作物が3.9%、園芸作物が7.3%のシェアを占めています。最も肥料を消費する作物は小麦とトウモロコシで、合計で土地面積の40.0%を占める。

- カルシウムは世界の二次多量栄養素肥料市場の総額の8.4%を占め、2021年には約5億3,870万米ドルを占める。アジア太平洋地域はカルシウム肥料市場を独占し、世界のカルシウム肥料市場の約41.1%を占め、2021年には2億2,160万米ドルを記録しました。カルシウム肥料市場におけるアジア太平洋地域の優位性は、主に土壌の酸性化によるもので、カルシウムやマグネシウムなどの塩基性陽イオンが失われ、鉄やアルミニウム錯体のような酸性元素に置き換わっています。

- 作物の栽培面積が減少しているため、より高い生産性が求められており、二次多量栄養素肥料の需要は予測期間中に伸びると予想されます。

気候の変化と土壌のpHレベルの変動が市場を牽引する可能性

- 二次多量栄養素肥料の施用は作物の収量にプラスの影響を与えます。カルシウム、マグネシウム、硫黄の需要は、近代的な高収量作物システムと連動して増加しており、植物の生産性において極めて重要な役割を担っていることが明らかになっています。

- アジア太平洋地域は世界の二次多量栄養素肥料市場を独占しており、2022年にはその39.2%を占める。同地域では、硫黄が63.5%と大半のシェアを占め、マグネシウムの30.0%がこれに続きます。アジア太平洋地域ではコメが主要な穀物作物であり、世界の生産と消費の90%を占めています。この地域の土壌は硫黄が不足しているため、重要な微量元素である硫黄は、植物の成長と収量を高めるために施肥によって補充されます。

- 2022年の世界の二次多量栄養素肥料市場では、欧州が26.9%のシェアで2位の座を確保しました。硫黄は市場金額の67.4%を占め、2022年の二次多量栄養素肥料のトップに躍り出た。ロシアは市場シェア19.2%で、欧州市場の支配的プレイヤーに浮上しました。

- 2022年、南米の二次多量栄養素肥料市場は世界市場の11.5%のシェアを占めました。最近の干ばつと熱波がこの地域の土壌における栄養分の利用可能性を妨げ、これらの欠乏に対抗するために二次多量栄養素肥料の採用を促進しました。

- 二次多量栄養素は、各栄養素が特定の代謝プロセスに影響を与えることで、植物の栄養バランスを維持する上で極めて重要な役割を果たしています。最適化された植物栄養の重要性がますます認識されるようになるにつれて、このダイナミックな動きが今後数年間の市場の成長を促進するものと思われます。

世界の二次多量栄養素肥料の市場動向

増大する食糧需要を満たすための農業部門への圧力の高まりは、畑作物の栽培面積を増加させると予想されます。

- 世界の農業部門は現在、多くの課題に直面しています。国連によると、世界人口は2050年までに90億人を超える可能性があります。この人口増加は、労働力不足と都市化の進展による農地の縮小により、すでに生産量の低下を経験している農業部門に過大な負担をかける可能性があります。国連食糧農業機関によると、2050年までに世界人口の70%が都市に住むようになると予想されています。世界的に耕地が減少しているため、農家は作物の収穫量を増やすために、より多くの肥料を利用する必要があります。

- アジア太平洋地域は世界最大の農産物生産地です。農業はこの地域の経済にとって不可欠であり、全労働人口の約20%を雇用しています。畑作がこの地域を支配しており、作物総面積の95%以上を占めています。米、小麦、トウモロコシがこの地域で生産される主要な畑作作物で、2022年の総栽培面積の約24.3%を占める。

- 北米は世界第2位の耕作可能地域です。その農場では、畑作物を中心に多様な作物が栽培されています。特に、トウモロコシ、綿花、米、大豆、小麦は、米国農務省が強調しているように、著名な畑作作物です。2022年、米国は北米の作物栽培面積の46.2%を占めていました。しかし、同国は2017年から2019年にかけて作付面積の大幅な減少を目の当たりにしたが、これは主にテキサスやヒューストンなどの地域で深刻な洪水に見舞われた悪環境が原因です。

硫黄は植物内で移動しないため、生育初期から収穫まで安定した供給が必要であり、供給が不足すると収量が制限される可能性があります。

- 2022年の畑作物における二次多量栄養素の世界平均施用量は33.73kg/haでした。同年のカルシウム施用量は約39.20kg/ヘクタール、マグネシウム施用量は約34.51kg/ヘクタール、硫黄施用量は27.47kg/ヘクタールでした。カルシウムは他の必須栄養素の吸収を助ける。マグネシウムは植物の成長と開花を促進する優れた酵素活性剤です。植物が必要とする二次多量栄養素は少量で、一次栄養素では代替できないです。

- 2022年の平均硫黄施用量は、トウモロコシ/メイズが34.33kg/haと最も多く、次いで綿花が29.72kg/ha、菜種/カノーラが27.57kg/haでした。硫黄は植物体内で移動しないため、生育初期から収穫まで安定した供給が必要です。生育のどの段階においても、硫黄が不足すると収量の低下につながります。N、P、Kの要求量はほぼ満たされたため、他の栄養素の不足が現れ始めました。硫黄はN、P、Kに次いで4番目に重要な養分だが、通常は少量しか必要とされないです。

- 南米、中東・アフリカ、アジア太平洋地域が二次多量栄養素の主な消費国で、平均施肥量が最も多く、2022年にはそれぞれ39.27kg/ha、32.79kg/ha、32.74kg/haを占めました。二次多量栄養素は植物にとって重要な栄養素であり、より強固な細胞壁を支え、打撲傷を減らし、畑作物の病気を予防するため、生産者は二次多量栄養素の重要性を認めています。二次多量栄養素は一次多量栄養素よりも収量を制限することは少ないが、作物は生産性を最適化するために、二次多量栄養素を必要とします。

二次多量栄養素肥料の業界概要

二次多量栄養素肥料市場は細分化されており、上位5社で10.61%を占めています。この市場の主要企業は以下の通りです。 ICL Group Ltd, K+S Aktiengesellschaft, Koch Industries Inc., The Mosaic Company and Yara International ASA(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 主要作物の作付面積

- 畑作物

- 園芸作物

- 平均養分施用率

- 二次多量栄養素

- 畑作物

- 園芸作物

- 二次多量栄養素

- 灌漑設備のある農地

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- タイプ

- ストレート

- 二次栄養素

- カルシウム

- マグネシウム

- 硫黄

- ストレート

- 施用モード

- 施肥

- 葉面散布

- 土壌

- 作物タイプ

- 畑作物

- 園芸作物

- 芝・観賞用

- 地域

- アジア太平洋地域

- オーストラリア

- バングラデシュ

- 中国

- インド

- インドネシア

- 日本

- パキスタン

- フィリピン

- タイ

- ベトナム

- その他アジア太平洋地域

- 欧州

- フランス

- ドイツ

- イタリア

- オランダ

- ロシア

- スペイン

- ウクライナ

- 英国

- その他欧州

- 中東・アフリカ

- ナイジェリア

- サウジアラビア

- 南アフリカ

- トルコ

- その他中東とアフリカ

- 北米

- カナダ

- メキシコ

- 米国

- その他北米地域

- 南米

- アルゼンチン

- ブラジル

- その他南米

- アジア太平洋地域

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Coromandel International Ltd.

- Deepak fertilizers & Petrochemicals Corporation Ltd

- Grupa Azoty S.A.(Compo Expert)

- Haifa Group

- ICL Group Ltd

- K+S Aktiengesellschaft

- Koch Industries Inc.

- The Mosaic Company

- Yara International ASA

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The Secondary Macronutrients Fertilizer Market size is estimated at 37.81 billion USD in 2025, and is expected to reach 49.28 billion USD by 2030, growing at a CAGR of 5.44% during the forecast period (2025-2030).

The adoption of sulfur fertilizer is more than other secondary macronutrients

- In 2021, sulfur accounted for 42.6% of the global secondary macronutrient fertilizer market. In 2021, the value of the European sulfur market was about USD 1.19 billion. In this market, specialty sulfur fertilizer accounted for a market share of approximately 49.4%, and conventional sulfur fertilizer accounted for about 50.1%. The adoption of specialty sulfur fertilizer is higher than that of other secondary macronutrients. The specialty sulfur fertilizer market is anticipated to reach USD 1.82 billion by the end of the forecast period.

- Magnesium accounted for 48.9% of the global secondary macronutrient fertilizer market in 2021. Field crops accounted for a maximum share of 88.8%, followed by turf and ornamental crops and horticulture crops, holding shares of 3.9% and 7.3%, respectively. The largest fertilizer-consuming crops are wheat and corn, accounting for a total of 40.0% of the land area.

- Calcium recorded 8.4% of the total value of the global secondary macronutrient fertilizer market, accounting for about USD 538.7 million in 2021. The Asia-Pacific region dominated the calcium fertilizer market and accounted for about 41.1% of the global calcium fertilizer market's value, registering USD 221.6 million in 2021. The dominance of the Asia-Pacific region in the calcium fertilizer market is mainly due to the acidification of soils, which means the loss of base cations, such as calcium and magnesium, and replacement with acidic elements, like iron and aluminum complexes.

- The demand for secondary macronutrient fertilizer is anticipated to grow during the forecast period, as the need for higher productivity is increasing due to the decline in the area under the cultivation of crops.

Climate changes and fluctuation in pH levels in soils may drive the market

- Applying secondary macronutrient fertilizers impacts crop yields positively. The demand for calcium, magnesium, and sulfur has risen in tandem with modern high-yield crop systems, underscoring their pivotal role in plant productivity.

- Asia-Pacific dominates the global secondary macronutrient fertilizer market, capturing 39.2% of its value in 2022. Within the region, sulfur claims the majority share at 63.5%, trailed by magnesium at 30.0%. Rice is the major grown cereal crop in Asia-Pacific, with the region accounting for 90% of global production and consumption. Given the region's sulfur-deficient soils, sulfur, a crucial trace element, is supplemented through fertilization to enhance plant growth and yield.

- Europe secured the second-largest share of the global secondary macronutrient fertilizer market in 2022, with a share of 26.9%. Sulfur, commanding a hefty 67.4% of the market's value, emerged as the leading secondary macronutrient fertilizer in 2022. Russia, with a 19.2% market share, emerged as the dominant player in Europe's market landscape.

- In 2022, the South American secondary macronutrient fertilizer market held an 11.5% share of the global market. Recent droughts and heat waves disrupted nutrient availability in the region's soils, driving up the adoption of secondary macronutrient fertilizers to counteract these deficiencies.

- Secondary macronutrients play a pivotal role in maintaining balanced plant nutrition, with each nutrient influencing specific metabolic processes. This dynamic is poised to fuel the growth of the market in the coming years as the importance of optimized plant nutrition becomes increasingly recognized.

Global Secondary Macronutrients Fertilizer Market Trends

The rising pressure on the agriculture sector to meet the growing demand for food is expected to increase the area under field crop cultivation

- The global agricultural sector is currently facing many challenges. According to the United Nations, the world population may exceed 9 billion by 2050. This population growth may overburden the agricultural sector, which is already experiencing an output loss due to a lack of laborers and the shrinkage of agricultural fields caused by rising urbanization. According to the Food and Agriculture Organization, 70% of the global population is expected to live in cities by 2050. Due to the global loss of arable land, farmers now need to utilize more fertilizers to increase crop yields.

- Asia-Pacific is the world's largest producer of agricultural products. Agriculture is critical to the region's economy, as it employs about 20% of the total available workforce. Field crop cultivation dominates the region, accounting for more than 95% of the total crop area. Rice, wheat, and corn are the major field crops produced in the region, together accounting for about 24.3% of the total crop area in 2022.

- North America ranks as the second-largest arable region across the world. Its farms cultivate a diverse range of crops, with a focus on field crops. Notably, corn, cotton, rice, soybean, and wheat are the prominent field crops, as highlighted by the USDA. In 2022, the United States commanded 46.2% of North America's crop cultivation area. However, the country witnessed a significant drop in crop acreage between 2017 and 2019, primarily due to adverse environmental conditions, leading to severe flooding in regions like Texas and Houston.

A steady supply of sulfur is required from early growth stages until harvest as it is immobile in plants, and any shortage in supply can limit the yield

- The global average application rate of secondary macronutrients in field crops was 33.73 kg/ha in 2022. In the same year, the calcium application rate was about 39.20 kg/hectare, magnesium was about 34.51 kg/hectare, and sulfur application rate was 27.47 kg/hectare. Calcium aids in the absorption of other essential nutrients. Magnesium is an excellent enzyme activator that promotes plant growth and flowering. Plants require only a small amount of secondary macronutrients that cannot be replaced by any primary nutrients.

- In 2022, corn/maize recorded the highest average sulfur application rate of 34.33 kg/ha, followed by cotton at 29.72 kg/ha and rapeseed/canola at 27.57 kg/ha. A steady supply of sulfur is required from early growth stages until harvest as it is immobile in plants. At any stage of growth, a shortage of sulfur can lead to lower yields. As N, P, and K requirements have mostly been met, deficits of other nutrients have started to appear. Sulfur is the fourth most crucial nutrient after N, P, and K but is usually only needed in low quantities.

- South America, the Middle East & Africa, and Asia-Pacific were the major consumers of secondary macronutrients, with the highest average nutrient application rates, accounting for 39.27 kg/ha, 32.79 kg/ha, and 32.74 kg/ha, respectively, in 2022. Growers acknowledged the importance of secondary macronutrients because they are crucial nutrients for plants, support stronger cell walls, lower bruising, and prevent disease in field crops. Although secondary macronutrients are less yield-limiting than primary macronutrients, crops need them at a rate that will optimize productivity.

Secondary Macronutrients Fertilizer Industry Overview

The Secondary Macronutrients Fertilizer Market is fragmented, with the top five companies occupying 10.61%. The major players in this market are ICL Group Ltd, K+S Aktiengesellschaft, Koch Industries Inc., The Mosaic Company and Yara International ASA (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Secondary Macronutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Secondary Macronutrients

- 4.3 Agricultural Land Equipped For Irrigation

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Type

- 5.1.1 Straight

- 5.1.1.1 Secondary Macronutrients

- 5.1.1.1.1 Calcium

- 5.1.1.1.2 Magnesium

- 5.1.1.1.3 Sulfur

- 5.1.1 Straight

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf & Ornamental

- 5.4 Region

- 5.4.1 Asia-Pacific

- 5.4.1.1 Australia

- 5.4.1.2 Bangladesh

- 5.4.1.3 China

- 5.4.1.4 India

- 5.4.1.5 Indonesia

- 5.4.1.6 Japan

- 5.4.1.7 Pakistan

- 5.4.1.8 Philippines

- 5.4.1.9 Thailand

- 5.4.1.10 Vietnam

- 5.4.1.11 Rest of Asia-Pacific

- 5.4.2 Europe

- 5.4.2.1 France

- 5.4.2.2 Germany

- 5.4.2.3 Italy

- 5.4.2.4 Netherlands

- 5.4.2.5 Russia

- 5.4.2.6 Spain

- 5.4.2.7 Ukraine

- 5.4.2.8 United Kingdom

- 5.4.2.9 Rest of Europe

- 5.4.3 Middle East & Africa

- 5.4.3.1 Nigeria

- 5.4.3.2 Saudi Arabia

- 5.4.3.3 South Africa

- 5.4.3.4 Turkey

- 5.4.3.5 Rest of Middle East & Africa

- 5.4.4 North America

- 5.4.4.1 Canada

- 5.4.4.2 Mexico

- 5.4.4.3 United States

- 5.4.4.4 Rest of North America

- 5.4.5 South America

- 5.4.5.1 Argentina

- 5.4.5.2 Brazil

- 5.4.5.3 Rest of South America

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Coromandel International Ltd.

- 6.4.2 Deepak fertilizers & Petrochemicals Corporation Ltd

- 6.4.3 Grupa Azoty S.A. (Compo Expert)

- 6.4.4 Haifa Group

- 6.4.5 ICL Group Ltd

- 6.4.6 K+S Aktiengesellschaft

- 6.4.7 Koch Industries Inc.

- 6.4.8 The Mosaic Company

- 6.4.9 Yara International ASA

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms