|

市場調査レポート

商品コード

1693476

アフリカのソルガムきび種子:市場シェア分析、産業動向、成長予測(2025年~2030年)Africa Sorghum Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アフリカのソルガムきび種子:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 175 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

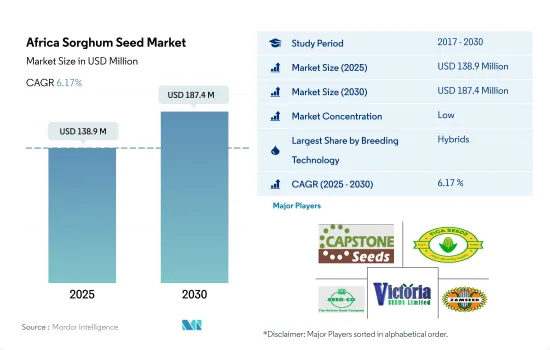

アフリカのソルガムきび種子市場規模は2025年に1億3,890万米ドルと推定され、2030年には1億8,740万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは6.17%で成長する見込みです。

グルテンフリーや高抗酸化物質など、ソルガムきび種子の改良ハイブリッド品種に対する需要の増加が市場を牽引しています。

- ハイブリッド種子品種がアフリカのソルガムきび種子市場を独占し、2022年の市場金額の約56.6%を占めたが、同年の開放受粉種子のシェアは43.4%でした。

- ハイブリッド市場を牽引しているのは、同地域の収量と生産量を高めるための新品種開発に対する民間企業の投資増加、ハイブリッド種子の商業化、有利な政府施策です。ソルガム種子のトランスジェニックハイブリッドは、この地域では商業栽培が承認されていないため、この地域の非トランスジェニックハイブリッド種子市場を牽引しています。

- ソルガム非トランスジェニックハイブリッドの市場規模は2017~2022年の間に約42.5%増加しています。非遺伝子組み換えハイブリッド種子の市場は、飼料産業や加工産業からのソルガムきびに対する需要の増加や、非遺伝子組み換え品種、グルテンフリー品種、高抗酸化品種に対する消費者の嗜好により拡大すると予測されます。

- ソルガムきびの開放受粉品種とハイブリッド派生品種の作付面積は、2017年の190万ヘクタールから2022年には200万ヘクタールに増加しています。これは主に、同国における有機栽培またはサステイナブル方法で栽培されたソルガムきびに対する需要の高まりによるものです。

- 金額ベースでは、ナイジェリアは最大のOPV種子市場で、2022年にはアフリカの開放受粉ソルガム種子市場の51.5%の市場シェアを占めます。小規模農業従事者がOPV種子の使用を好むのは、ハイブリッド種子に比べて低コストであるためであり、小規模農業従事者の大半は開放受粉品種を購入する代わりに農場保存種子を利用しています。

- 同国では遺伝子組み換え作物が入手できないことと、非遺伝子組み換え作物に対する需要の高まりが相まって、予測期間中の市場の牽引役となることが予想されます。

ナイジェリアがアフリカのソルガム種子市場を独占しているのは、ハイブリッド品種の入手可能性が高まっていることと政府の施策が好意的であるためです。

- 2022年、ソルガム種子はアフリカの種子市場で4.1%のシェアを占めました。このセグメントの市場規模は2017~2022年の間に37.1%増加しました。この背景には、アフリカで半発酵パン、クスクス、発酵・非発酵ポリッジなど、幅広く快適で健康的な伝統料理にソルガムきびの利用が増加していることがあります。

- ナイジェリアはアフリカ最大のソルガムきび生産国です。ナイジェリアは2022年のアフリカのソルガムきび種子市場の金額ベースで51.4%のシェアを占めています。これは、同国でハイブリッド品種が入手しやすくなっていることと、政府の施策が好意的であることによる。その結果、開放受粉品種に比べてハイブリッド品種が大きなシェアを占めています。

- 2022年、エチオピアはアフリカで2番目に大きなソルガム生産国です。エチオピアはアフリカのソルガムきび市場金額の16.0%を占め、予測期間中は44.9%の成長が見込まれます。これはエチオピアのソルガム価格がこの地域の他のどの国よりも高いためです。そのため、数量は比較的少ないです。

- 2022年には、タンザニアはアフリカのソルガム種子市場の金額ベースで3.0%のシェアを占めました。2017年のソルガム栽培面積は75万3,700haであったが、2022年には100万haに増加します。その結果、産業用に利用されるソルガムきびの量は同国で25%増加しました。

- 2022年には、アフリカのその他の中東・アフリカがアフリカのソルガム種子市場の25.2%を占めます。ソルガムでは、開放受粉品種(59.5%)の使用率がハイブリッド品種(40.5%)よりも高いです。

- ソルガムの耕作地面積の増加と国内市場からの消費需要の増加が、予測期間中のCAGRを6.2%として同セグメントを牽引すると予測されます。

アフリカのソルガム種子市場の動向

政府のイニシアティブと改良品種への需要、加工産業におけるソルガムきびの利用が栽培面積を押し上げています。

- アフリカの穀物ソルガム栽培面積は2022年には2,840万ヘクタールで、同年の穀物・穀類セグメントの22.5%を占めました。グレインソルガムの栽培面積は、2017年の2,790万ヘクタールから2022年には2.1%増加しました。しかし、農業従事者がトウモロコシや油糧種子など、より収益性の高い作物の作付けを優先したため、2019年の作付面積は前年(2018年)に比べ6.1%減少しました。この減少はまた、改良種子品種に対する認識不足と、2018~2022年にかけての干ばつによるもので、アフリカでの栽培面積に影響を与えました。エチオピアやケニアなどの新興諸国は生育期に干ばつに見舞われ、アフリカの栽培面積に影響を与えています。

- ナイジェリアはソルガム栽培面積に関する主要国で、2022年にはこの地域の20.3%を占めていました。2018年のソルガム栽培面積は2017年と比較して3.9%減少し、2019年は2018年と比較して3.5%減少しました。作付面積の減少は、国内の主要なソルガム生産地域でボコ・ハラム(BH)の活動が復活したことと関連しています。エチオピアはナイジェリアに次いで2番目に大きな国で、2022年にはアフリカのソルガム栽培面積の5.9%を占めました。ソルガム栽培面積は、ガーナのような国が国内の需要を満たすためにソルガム生産者により多くのソルガムを栽培するよう補助金を提供しているため、増加すると推定されます。ケニアやナイジェリアのような他の国々では、これらの国々で操業している産業からの需要を満たすためにソルガムきびの需要が増加しています。

- 醸造産業からの需要と政府の栽培補助金が、この地域のソルガム作付面積を押し上げると推定されます。

ソルガム栽培では病害による収量減が増加しているため、耐病性形質が最も好まれます。

- ソルガムはアフリカでは重要な主食作物です。ソルガムきびでは、病害が生産物の収量と品質を決定する上で重要な役割を果たしています。ソルガムきびは、作物サイクルに感染する多数の真菌、細菌、ウイルス性病原体の宿主です。耐病性品種はより良い収量を得るのに役立ち、その結果需要が高まります。ソルガムきびでは、ウイルス性・細菌性病害に比べ、真菌性病害がより一般的で、高い収量損失を引き起こします。ソルガムきびの一般的な病害は、穀カビ病、エルゴ病、スマット病、べと病などで、これらは収量損失を引き起こします。その結果、この地域では耐病性形質を持つ品種の需要が急増する可能性があります。

- スーダン、ナイジェリア、ニジェール、エチオピアはこの地域の主要なソルガム生産国です。耐病性品種とハイブリッドの開発は、この地域のソルガム病害管理の主要焦点です。2020年、シード社はICRISATと共同で、ジンバブエと南部アフリカの多様な農業生態系に適応し、収量が23~34%高い耐病性ソルガムハイブリッドを開発しました。

- 異なる土壌への適応性が広く、タンニンの含有量が低く、また高いソルガム品種、早熟で、均一性の高いソルガム品種は、他の主要な人気形質であり、大きな需要があります。Sekedo、Seso 1、Seso 3はウガンダのVictoria Seeds Limitedが開発した耐虫・耐病性品種であり、Kuyuma、Sima、ZSV 15はZamseedsが開発した適応性の高い品種です。

- したがって、生物・生物ストレスによる損失の増加を防ぎ、生産性を向上させるために、先進的形質を持つソルガム種子の需要は予測期間中に増加すると予測されます。

アフリカのソルガム種子産業概要

アフリカのソルガム種子市場はセグメント化されており、上位5社で22.14%を占めています。この市場の主要企業は、Capstone Seeds、FICA SEEDS、Seed Co Limited、Victoria Seeds Limited、Zambia Seed Company Limited(Zamseed)などです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 栽培面積

- 最も人気のある形質

- 育種技術

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 育種技術

- ハイブリッド

- 非トランスジェニックハイブリッド

- 開放受粉品種とハイブリッド派生品種

- ハイブリッド

- 国名

- エジプト

- エチオピア

- ガーナ

- ケニア

- ナイジェリア

- 南アフリカ

- タンザニア

- その他のアフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Advanta Seeds-UPL

- Capstone Seeds

- Corteva Agriscience

- FICA SEEDS

- S& W Seed Co.

- Seed Co Limited

- Victoria Seeds Limited

- Zambia Seed Company Limited(Zamseed)

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92539

The Africa Sorghum Seed Market size is estimated at 138.9 million USD in 2025, and is expected to reach 187.4 million USD by 2030, growing at a CAGR of 6.17% during the forecast period (2025-2030).

The increasing demand for improved hybrid varieties of sorghum seeds, such as gluten-free and high antioxidants, is driving the market

- Hybrid seed varieties dominated the African sorghum seed market, which accounted for about 56.6% of the market value in 2022, while open-pollinated seeds held a share of 43.4% in the same year.

- The hybrid market is being driven by increased investment by private industries in developing new varieties to boost yield and production in the region, commercialization of hybrid seeds, and favorable government policies. The transgenic hybrids of sorghum seeds are not approved for commercial cultivation in the region, driving the non-transgenic hybrid seed market in the region.

- The market value of sorghum non-transgenic hybrids has increased by about 42.5% between 2017 and 2022. The market for non-transgenic hybrids is projected to grow due to increased demand for sorghum from the feed and processing industries, as well as consumer preference for non-GMO, gluten-free, and high-antioxidant varieties.

- The acreage of open-pollinated varieties and hybrid derivatives of sorghum has increased from 1.9 million hectares in 2017 to 2.0 million hectares in 2022. This is primarily due to the rise in demand for organic or sustainably grown sorghum in the country.

- In terms of value, Nigeria had the largest OPV seed market, with a 51.5% market share of the African open-pollinated sorghum seed market in 2022. Small-scale farmers mostly prefer the use of OPV seeds due to their lower cost compared to hybrid seeds, and the majority of small-scale farmers utilize farm-saved seeds instead of buying open-pollinated varieties.

- The unavailability of transgenic crops combined with the growing demand for non-GMO crops in the country is anticipated to drive the market during the forecast period.

Nigeria dominates the African sorghum seed market due to the increased availability of hybrid varieties and favorable government policies

- In 2022, the sorghum segment accounted for a 4.1% share value of the African seed market. The market value of this segment increased by 37.1% between 2017 and 2022. This is because of the increasing usage of sorghum in a wide range of pleasant and healthy traditional dishes in Africa, such as semi-leavened bread, couscous, and fermented and non-fermented porridges.

- Nigeria is the largest producer of sorghum in Africa. It accounted for a 51.4% share in terms of the value of the African sorghum seed market in 2022. This is because of the increased availability of hybrid varieties in the country and favorable government policies. As a result, hybrids hold a major share compared to open-pollinated varieties.

- In 2022, Ethiopia is the second-largest sorghum-producing country in Africa. It accounted for a 16.0% share of the African sorghum market value, which is estimated to grow by 44.9% during the forecast period. This is because sorghum prices are higher in Ethiopia than in any other country in the region. Thus, the volume is comparatively low.

- In 2022, Tanzania accounted for a share of 3.0% in terms of the value of the African sorghum seed market. The area under cultivation of sorghum was 753.7 thousand ha in 2017, which increased to 1.0 million ha in 2022. As a result, the quantity of sorghum utilized for industrial purposes increased by 25% in the country.

- In 2022, the rest of Africa accounted for 25.2% of the African sorghum seed market. The usage of open-pollinated varieties (59.5%) is higher than hybrid varieties (40.5%) in sorghum.

- The rise in the area under cultivation land of sorghum and the increase in the demand from domestic markets for consumption are estimated to drive the segment with a CAGR of 6.2% during the forecast period.

Africa Sorghum Seed Market Trends

Government initiatives and demand for improved varieties, along with the usage of sorghum in processing industries, are driving the acreage

- The area under cultivation of grain sorghum in Africa was 28.4 million hectares in 2022, which accounted for 22.5% of the area under the grains & cereals segment in the same year. The acreage under grain sorghum increased by 2.1% from 27.9 million hectares in 2017 to 2022. However, the acreage declined by 6.1% in 2019 compared to the previous year (2018) because farmers preferred to plant more profitable crops such as corn and oilseed. The decrease was also due to a lack of awareness about improved seed varieties and the drought during 2018-2022, which impacted the cultivation area in Africa. Developing countries such as Ethiopia and Kenya suffer from drought in the growing season, impacting the cultivation area in Africa.

- Nigeria was the major country concerning the acreage under sorghum, accounting for 20.3% of the region in 2022. The area under sorghum in 2018 declined by 3.9% compared to 2017, and it declined by 3.5% in 2019 compared to 2018. The decrease in the acreage is associated with the resurgence of Boko Haram (BH) activities in the major sorghum-producing regions in the country. Ethiopia was the second-largest country after Nigeria, occupying 5.9% of the African sorghum acreage in 2022. The cultivation area under sorghum is estimated to increase as countries such as Ghana have been providing subsidies to sorghum producers to cultivate more sorghum to satiate the demand in the country. Other countries, such as Kenya and Nigeria, are witnessing an increase in the demand for sorghum to meet the demand from industries operating in these countries.

- The demand from brewing industries and government subsidies for cultivation is estimated to drive the acreage under sorghum in the region.

Disease resistant traits are the most preferred segment in sorghum cultivation due to the rising yield losses caused by diseases

- Sorghum is an important staple food crop in Africa. In sorghum, diseases play a significant role in deciding the yield and quality of produce. Sorghum is the host of numerous fungal, bacterial, and viral pathogens that infect the crop cycle. Disease-resistant varieties help get a better yield, thus boosting their demand. In sorghum, fungal diseases are more common and cause high yield loss compared to viral and bacterial diseases. The common sorghum diseases are grain mold, ergot, smut, downy mildew, etc., which cause yield losses. Consequently, the demand for varieties with disease-resistant traits may surge in the region.

- Sudan, Nigeria, Niger, and Ethiopia are the major sorghum-producing countries in the region. The development of disease-resistant varieties and hybrids is the main focus for the management of sorghum diseases in the region. In 2020, Seed Co. company, in partnership with ICRISAT, developed a disease-resistant sorghum hybrid with a 23-34% higher yield and adaptability to diverse agroecologies in Zimbabwe and southern Africa.

- Sorghum varieties with wider adaptability to different soils, low and high tannin content, early maturity, and high uniformity are the other major popular traits that are in huge demand. Sekedo, Seso 1, and Seso 3 are insect and disease-resistant varieties developed by Victoria Seeds Limited in Uganda, Kuyuma, Sima, and ZSV 15 are some of the wider adaptable cultivars developed by Zamseeds, where the farmers prefer these varieties to get better yields.

- Therefore, to prevent increasing losses from biotic and abiotic stresses and increase productivity, the demand for sorghum seeds with advanced traits is projected to increase during the forecast period.

Africa Sorghum Seed Industry Overview

The Africa Sorghum Seed Market is fragmented, with the top five companies occupying 22.14%. The major players in this market are Capstone Seeds, FICA SEEDS, Seed Co Limited, Victoria Seeds Limited and Zambia Seed Company Limited (Zamseed) (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.2 Most Popular Traits

- 4.3 Breeding Techniques

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.1.1 Non-Transgenic Hybrids

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.1.1 Hybrids

- 5.2 Country

- 5.2.1 Egypt

- 5.2.2 Ethiopia

- 5.2.3 Ghana

- 5.2.4 Kenya

- 5.2.5 Nigeria

- 5.2.6 South Africa

- 5.2.7 Tanzania

- 5.2.8 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Advanta Seeds - UPL

- 6.4.2 Capstone Seeds

- 6.4.3 Corteva Agriscience

- 6.4.4 FICA SEEDS

- 6.4.5 S&W Seed Co.

- 6.4.6 Seed Co Limited

- 6.4.7 Victoria Seeds Limited

- 6.4.8 Zambia Seed Company Limited (Zamseed)

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms