|

市場調査レポート

商品コード

1693455

北米の油糧種子(播種用種子)市場シェア分析、産業動向、成長予測(2025年~2030年)North America Oilseed (seed For Sowing) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米の油糧種子(播種用種子)市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 202 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

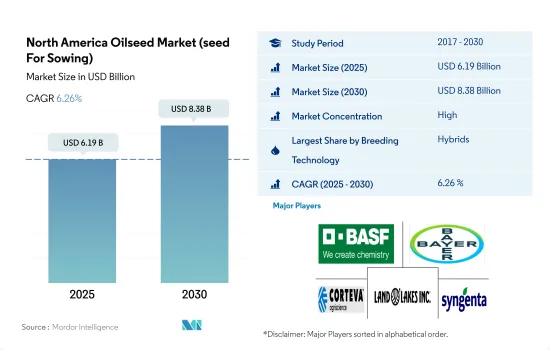

北米の油糧種子市場(播種用種子)規模は2025年に61億9,000万米ドルと推定・予測され、2030年には83億8,000万米ドルに達し、予測期間(2025~2030年)のCAGRは6.26%で成長すると予測されます。

種子の技術革新と栽培面積の増加が市場成長を促進

- 油糧種子は2022年の北米種子市場の22.9%を占め、予測期間中に成長が予測されます。2022年の油糧種子の栽培面積は4,980万ヘクタールで、高収量ハイブリッドの利用可能性の増加とGMハイブリッドの採用により2020年から5.6%増加しました。

- 2022年の油糧種子市場では、ハイブリッド種が48億4,000万米ドルの市場規模を占めました。市場の主要企業はハイブリッド品種を導入しています。例えば、シンジェンタ・シードは2022年にカナダ市場で新しい在来種大豆ブランド「シルバーライン」を発売しました。このブランドは高タンパク大豆とNK処理大豆品種を提供しています。

- 米国とカナダは、カノーラやダイズなどの遺伝子組換え油糧種子を承認・商業化している世界の主要国です。主要形質は除草剤耐性と昆虫抵抗性で、その他に高油分、高オレイン酸、ラウリン酸含有などの形質があり、加工産業では高値で取引されています。2022年のハイブリッド油糧種子の総栽培面積は2,970万ヘクタールで、2017年と比較して20.3%増加しました。

- 米国は、北米における開放受粉品種とハイブリッド派生品種の栽培面積で最大の国です。これは、油糧種子の総栽培面積が米国の方が多いためです。

- 米国とメキシコでは、予測期間中、有機農業と遺伝子組み換え作物の禁止によりOPVの増加が見込まれます。カナダでは、トランスジェニックハイブリッドが、その高い油分含有量と市場価格により、生産者に最も採用されています。そのため、油糧種子市場は予測期間中、ハイブリッドとOPVの両方でこの地域で成長すると予測されます。

米国は北米最大の油糧種子市場

- 2022年、北米は世界の油糧種子市場の40.3%を占めました。同市場は、主に油糧種子作物の栽培面積の増加により、2017年と比較して2022年には65%成長しました。北米は油糧種子の主要輸出国であり、様々な形態での消費需要が高いです。さらに、油糧種子の栽培面積は4,980万ヘクタールを占め、2019年と比較して12.8%増加しています。

- 2022年には、米国が北米の油糧種子需要の74.4%を占めたが、これは消費需要が高く、主要輸出国であり、利益率が高いためです。大豆とカノーラは同国で栽培される主要な油糧種子であり、合わせて同国の油糧種子市場の95.3%を占めています。

- カナダは2022年の北米の油糧種子市場の24.7%を占め、カノーラは7億8,420万米ドルを占める主要油糧種子市場です。カナダは世界最大のカノーラ油糧種子の生産国で、バイオ燃料産業からの需要が高いためです。加えて、同国は遺伝子組み換えカノーラ種子を採用しており、これが同国の油糧種子市場の大きな成長に寄与しています。

- メキシコと、キューバ、ドミニカ共和国、コスタリカ、ジャマイカ、パナマ、ハイチといった北米の主要国は、この地域の油糧種子市場で0.8%のシェアを占めています。これらの国々では、油糧種子は主に国内消費に利用されています。

- 米国、カナダ、メキシコ間の貿易協定により、これらの国々は自由貿易が可能であり、3国間で種子を輸出する際に必要な承認も限られています。

- したがって、油糧作物に対する高い需要、貿易協定、遺伝子組み換え油糧種子品種の採用が、予測期間中にCAGR 6.1%で市場の成長を促進すると予想される主要因です。

北米の油糧種子市場(播種用種子)の動向

油糧種子の作付面積では大豆が大きなシェアを占めるが、カナダとメキシコではそれぞれカノーラとヒマワリに成長の可能性があります。

- 北米は、主にその良好な気候条件により、世界的に重要な油糧種子生産国です。2022年には、油糧種子作物の耕作面積は全体の28.8%を占め、4,980万ヘクタールに及びました。しかし、2017年と比較すると、大豆栽培の減少により、2018年と2019年の油糧種子栽培はそれぞれ3.3%と15%減少しました。この減少の背景には、中国の貿易制限があり、米国品種の大豆に対する世界の需要が減少し、大豆価格の下落につながったことがあります。さらに、2019年の春の大雨が大豆栽培の減少にさらに貢献しました。

- 米国は2022年に75.3%を占め、3,750万ヘクタールで最大国でした。大豆はこの地域の主要作物であり、2022年の油糧種子作付面積の94.1%を占めました。大豆のシェアが高いのは、遺伝子組換え大豆が承認されたことと、食用油と家畜飼料用濃縮タンパク質の需要により農業従事者への収益が高いためです。

- カナダの2022年の油糧種子栽培面積は1,180万ヘクタールで、そのうち77.4%をカノーラが占めています。カナダは世界最大のカノーラ生産国です。植物油と飼料としてのカノーラの需要が、予測期間中のカノーラ栽培面積を押し上げると予想されます。しかしメキシコでは、ベニバナ、ヒマシ、アマニなどの他の油糧種子が大きなシェアを占めています。ベニバナの栽培面積が増加しているのは、その油の需要に加え、遺伝子組み換え綿花が禁止されたため、綿花から油糧種子へのシフトが進んでいるためです。

- したがって、食用油と飼料用途の増加が、この地域の油糧種子栽培面積を押し上げています。

北米の油糧種子(播種用種子)産業概要

北米の油糧種子市場(播種用種子)はかなり統合されており、上位5社で76.34%を占めています。この市場の主要企業は、BASF SE、Bayer AG、Corteva Agriscience、Land O'Lakes Inc.、Syngenta Groupなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 耕作面積

- 耕作作物

- 最も人気のある形質

- 大豆

- 育種技術

- 列作物

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 育種技術

- ハイブリッド

- 非トランスジェニックハイブリッド

- 遺伝子組み換え雑種

- 除草剤耐性雑種

- 昆虫抵抗性雑種

- その他の形質

- 開放受粉品種とハイブリッド派生品種

- ハイブリッド

- 作物

- カノーラ、菜種、マスタード

- 大豆

- ヒマワリ

- その他の油糧種子

- 生産国

- カナダ

- メキシコ

- 米国

- その他の北米地域

第6章 競争情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Advanta Seeds-UPL

- BASF SE

- Bayer AG

- Corteva Agriscience

- Groupe Limagrain

- Land O'Lakes Inc.

- Nufarm

- S& W Seed Co.

- Stine Seed Company

- Syngenta Group

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92517

The North America Oilseed Market (seed For Sowing) size is estimated at 6.19 billion USD in 2025, and is expected to reach 8.38 billion USD by 2030, growing at a CAGR of 6.26% during the forecast period (2025-2030).

Increased innovation of seeds and increased area under cultivation are driving the market growth

- Oilseeds accounted for 22.9% of the North American seed market in 2022, which is projected to grow during the forecast period. The acreage under cultivation of oilseeds was 49.8 million ha in 2022, which increased by 5.6% from 2020 due to the increased availability of high-yielding hybrids and the adoption of GM hybrids.

- In 2022, hybrids dominated the oilseeds market with a market value of USD 4.84 billion in the region. Major companies in the market are introducing hybrid varieties. For instance, in 2022, Syngenta Seeds launched a new conventional soybean brand, "Silverline," in the Canadian market. This brand offers high-protein soybeans and NK-treated soybean varieties.

- The United States and Canada are the major countries in the world that have approved and commercialized genetically modified oilseeds such as canola and soybean. The major traits are herbicide tolerance and insect resistance, and other traits, such as high oil content, high oleic acid, and lauric acid content, fetch high prices in the processing industry. The total acreage under hybrid oilseed cultivation in 2022 was 29.7 million hectares, which increased by 20.3% compared to 2017.

- The United States is the largest country in terms of area under open-pollinated varieties and hybrid derivatives in North America. This is because the total acreage of oilseeds is higher in the United States.

- OPVs are expected to increase in the United States and Mexico due to organic farming and the prohibition of GMOs during the forecast period. In Canada, transgenic hybrids are most adopted by growers due to their high oil content and market prices. Therefore, the oilseed market is estimated to grow in the region in both hybrids and OPVs during the forecast period.

The United States is the largest oilseed market in North America

- In 2022, North America accounted for 40.3% of the global oilseeds market. The market grew by 65% in 2022, compared to 2017, mainly due to the increased cultivation area of oilseed crops. North America is the major exporter of oilseeds, and there is a high demand for consumption in different forms. Moreover, the area under oilseeds accounted for 49.8 million hectares, which has increased by 12.8% compared to 2019.

- In 2022, the United States accounted for 74.4% of the North American oilseed seed demand due to the high demand for consumption, being a leading exporter, and high-profit margins. Soybean and canola are the major oilseeds grown in the country, together contributing 95.3% of the country's oilseed market.

- Canada accounted for 24.7% of the North American oilseed market in 2022, with canola being a major oilseed market, accounting for USD 784.2 million. Canada is the world's largest producer of canola oilseeds, as it has high demand from the biofuel industry. In addition, the country has adopted transgenic canola seeds, which has contributed to major growth in the country's oilseed market.

- Mexico and other major North American countries, such as Cuba, Dominican Republic, Costa Rica, Jamaica, Panama, and Haiti, held a 0.8% market share of the region's oilseed market. Oilseeds are mainly used for domestic consumption in these countries.

- The trade agreement between the United States, Canada, and Mexico is helping these countries have free trade and limited approvals required for exporting seeds from one to another between the three countries.

- Therefore, the high demand for oil crops, trade agreements, and adoption of transgenic oilseed cultivars are the major factors anticipated to drive the growth of the market during the forecast period with a CAGR of 6.1%.

North America Oilseed Market (seed For Sowing) Trends

Soybean occupied the major share of oilseed acreage, with growth potential toward canola and sunflower in Canada and Mexico, respectively

- North America is a significant global producer of oilseeds, primarily due to its favorable climate conditions. In 2022, oilseed crops covered 28.8% of the total cultivated area, spanning 49.8 million hectares. However, compared to 2017, there was a decrease in oilseed cultivation in 2018 and 2019 by 3.3% and 15%, respectively, due to the decline in soybean cultivation. This reduction was driven by China's trade restrictions, which reduced global demand for US varieties of soybeans, leading to lower soybean prices. Additionally, heavy spring rains in 2019 further contributed to the decline in soybean cultivation.

- The United States was the largest country in the region, which accounted for 75.3% in 2022, with 37.5 million hectares. Soybean was the major crop in the region, with 94.1% of the oilseed acreage in 2022. The higher share of soybeans was because of the approval of transgenic soybeans and higher returns for farmers owing to their demand for edible oil and protein concentrate for livestock feeding.

- Canada had an area of 11.8 million hectares under the cultivation of oilseeds segment in 2022, of which 77.4% of the acreage was occupied by canola. Canada is the largest producer of canola in the world. The demand for canola as vegetable oil and feed is anticipated to drive the area under canola cultivation during the forecast period. However, in Mexico, other oilseeds such as safflower, castor, and linseed have a major share. The area under safflower cultivation has increased because of the demand for its oil and the shift from cotton to oilseeds, as GM cotton is banned.

- Therefore, the increase in the number of edible oil and feed applications is driving the area under oilseed cultivation in the region.

North America Oilseed (seed For Sowing) Industry Overview

The North America Oilseed Market (seed For Sowing) is fairly consolidated, with the top five companies occupying 76.34%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, Land O'Lakes Inc. and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.1.1 Row Crops

- 4.2 Most Popular Traits

- 4.2.1 Soybean

- 4.3 Breeding Techniques

- 4.3.1 Row Crops

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.1.1 Non-Transgenic Hybrids

- 5.1.1.2 Transgenic Hybrids

- 5.1.1.2.1 Herbicide Tolerant Hybrids

- 5.1.1.2.2 Insect Resistant Hybrids

- 5.1.1.2.3 Other Traits

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.1.1 Hybrids

- 5.2 Crop

- 5.2.1 Canola, Rapeseed & Mustard

- 5.2.2 Soybean

- 5.2.3 Sunflower

- 5.2.4 Other Oilseeds

- 5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Advanta Seeds - UPL

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 Groupe Limagrain

- 6.4.6 Land O'Lakes Inc.

- 6.4.7 Nufarm

- 6.4.8 S&W Seed Co.

- 6.4.9 Stine Seed Company

- 6.4.10 Syngenta Group

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms