|

市場調査レポート

商品コード

1693446

キャノーラ種子(播種用種子):市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Canola Seed (seed For Sowing) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| キャノーラ種子(播種用種子):市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 379 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

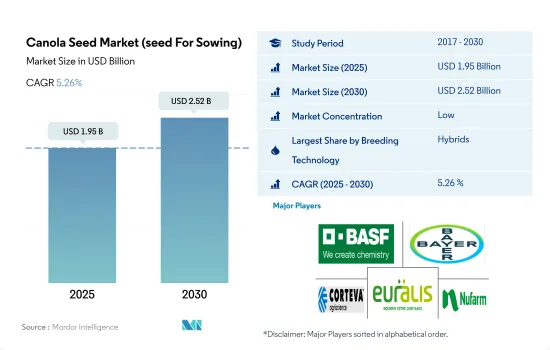

キャノーラ種子市場(播種用種子)の市場規模は2025年に19億5,000万米ドルと推定・予測され、2030年には25億2,000万米ドルに達し、予測期間(2025-2030年)のCAGRは5.26%で成長すると予測されます。

ハイブリッド種子が世界のキャノーラ種子市場を独占し、遺伝子組み換え種子の承認数が最も多い北米が大きなシェアを占める。

- 高い収量と適応性で知られるハイブリッド種子がキャノーラ栽培の主流を占めており、開放受粉品種(OPV)とその派生品種の両方を上回っています。

- 2022年のキャノーラ種子市場では、非遺伝子組換えハイブリッドが遺伝子組換え品種を上回りました。この嗜好は、トランスジェニック作物の栽培が世界的に禁止され、非遺伝子組み換え食品に対する消費者の需要が高まっていることに起因しており、非遺伝子組換え品種の播種面積が拡大すると予想されます。

- 2022年には、北米が遺伝子組換えハイブリッド作物市場をリードし、市場の88.7%を占めました。この優位性は、この地域の数多くの承認とFDAの寛大な政策に起因しています。

- アジア太平洋は34.4%のシェアを占め、2022年にはキャノーラOPVのリーダーとして浮上しました。この地域は主に、遺伝子組み換え種子の使用を禁止している有機農業部門の拡大により、OPVの採用が大幅に進んでいることが要因です。

- 世界規模では、ハイブリッドがOPVを成長率で上回っており、予測期間中のキャノーラ種子市場のCAGRはそれぞれ5.3%と5.1%と予測されます。高収量、省農薬種子、有機栽培への要望を背景としたハイブリッド導入の急増が、この動向に拍車をかけています。

- CAGRが9.3%と予測されるメキシコは、今後数年間、ハイブリッド・キャノーラ種子の最も急成長する市場になる見込みです。この成長を支えているのは、非遺伝子組換えハイブリッドへの嗜好の高まりです。

- 家畜飼料とキャノーラ油の需要の増加は、トウモロコシや小麦のような競合作物と比較して栽培が容易であることと相まって、予測期間中にCAGR 5.3%でキャノーラ種子市場を推進すると予想されます。

カナダがキャノーラ栽培を独占、ハイブリッド種子が世界的に牽引役となる

- 北米は最大のキャノーラ、菜種、マスタード生産国で、2022年には世界のキャノーラ種子市場の56.1%を占める。これは、北米ではキャノーラが輪作に多く使用されているためです。さらに、輸出市場が好調であることも、農家がキャノーラの生産を継続する大きな経済的インセンティブとなっています。

- アジア太平洋は2022年に4億8,570万米ドルとなり、世界第2位のキャノーラ種子市場を占めました。これは、キャノーラの栽培面積が広いためです。

- カナダは2022年の金額で世界のキャノーラ種子市場の47.1%を占め、キャノーラ種子の主要輸出国です。カナダ・キャノーラ協議会によると、同国は2022年に約840万トンのキャノーラ種子を輸出したが、主な輸入国は米国、中国、日本でした。

- 南米と欧州はキャノーラ種子市場で最も高い成長率を記録する見通しであり、予測期間中のCAGRはそれぞれ6.9%と6.7%と予測されます。この急成長は、食用油としてのキャノーラに対する消費者需要の高まりが原動力となっています。特に欧州では、バイオ潤滑油の利用拡大が後押しとなり、2017年から2022年にかけてキャノーラ種子市場が21.8%増加しました。

- 2022年には、ハイブリッド種子が世界のキャノーラ種子市場の主要シェアを占め、主要国であるカナダと中国が牽引しました。世界的に、キャノーラ、菜種、マスタードのハイブリッド種子分野は、様々な病気への耐性、干ばつへの耐性、高収量により、予測期間中にCAGR 5.3%を記録すると予測されています。

- したがって、加工産業からの需要の増加と栽培面積の増加が、予測期間中のキャノーラ種子市場を後押しする可能性があります。

世界のキャノーラ種子市場(播種用種子)動向

高い国内需要と適切な気候条件により、アジア太平洋地域がキャノーラの栽培面積を独占

- キャノーラ、菜種、マスタードは世界中で栽培されている著名な油糧作物です。2016年から2022年にかけて、世界のキャノーラ栽培面積は15.4%急増し、アジア太平洋地域がその先頭を走っています。2022年には、この地域のキャノーラ作付面積は1,920万ヘクタールに達し、世界シェアの49.0%を占める。アジア太平洋地域内では、インドと中国が主要企業として台頭し、2022年の栽培面積はそれぞれ800万ヘクタールと690万ヘクタールとなります。両者を合わせると、同地域全体の77.5%に相当します。特にインドは世界最大のキャノーラ生産国であり、2016年から2022年にかけて栽培面積が39.1%増加しました。この急増は、特にキャノーラが食用油として人気の高いインド北部での堅調な国内需要が主因です。

- 北米は第2位のキャノーラ生産地域であり、2022年には世界の作付面積の25.6%を占める。2016年から2022年の間に、この地域は9.3%の成長を示しました。カナダがこの地域を支配しており、2022年には同地域のキャノーラ作付面積の91.0%を占める。カナダの作付面積は2016年から2022年にかけて8.1%増加し、世界のキャノーラ生産量の20%に寄与したが、これは主に食品および燃料セクターからの需要急増によるものです。

- 2022年には、欧州が世界のキャノーラ作付面積の24.0%を占め、2017年から2022年にかけて11.8%増加しました。ロシアはこの地域の主要生産者として浮上し、キャノーラ作付面積全体の21.4%を占め、2016年から2022年にかけて93%急増しました。南米とアフリカは、2022年の世界のキャノーラ作付面積のそれぞれ0.7%と0.4%という控えめなシェアでした。石油産業からの需要が増加していることから、作付面積は予測期間中にさらに増加すると予想されます。

キャノーラの収量を向上させるために、耐病性、品質特性、高オレイン酸含量、耐乾燥性などの形質に対する需要が増加しています。

- キャノーラはいくつかの国で主要な油糧種子作物として支配的な地位を占めており、食用油、飼料、飼料ミールに用途を見出しています。Bayer AG、Land O'Lakes、Corteva Agriscienceなどの大手企業は、草丈、葉や穂の大きさ、形、色、成熟度、耐寒性など、主要な品質特性を重視しています。特に、コルテバ・アグリスサイエンス社のPT279CLとバイエル社のTruflexは、これらの品質特性の一例です。

- 病害抵抗性は、キャノーラが光葉斑、クラブルーツ、ブラックレッグ、バーティシリウム・ステムストライプ、スクレロチニアなどの病害に弱いことを考えると、極めて重要な特性です。コルテバ・アグリスサイエンスのPT303とPX131nは、軽葉斑点病と硬化病に対する抵抗性を示します。一方、Nufarm社のNuseedブランドは、黒脚病、クラブルーツ病、飛散防止病に対する抵抗性を示しています。さらに、進化する気象パターンと地域間の多様な土壌タイプに後押しされ、より広い適応性という形質が人気を集めています。

- 高オレイン酸含量、耐宿宿主性、耐乾性など、その他の求められる形質もプレミアム価格で取引されています。例えばオーストラリアでは、キャノーラの形質として干ばつ耐性と早生が求められており、これは同国の気候の変化と乾燥の深刻化に対応しています。Land O'Lakesの種子品種は、SurtやRoundup Readyなど、干ばつ耐性と宿根抵抗性を誇っています。

- 種苗会社は、耐病性を高め、高品質な特性を示す形質を生産者に提供しており、これが今後数年間の市場成長を促進する可能性があります。

キャノーラ種子(播種用種子)産業概要

キャノーラ種子(播種用種子)市場は細分化されており、上位5社で27.66%を占めています。この市場の主要企業は以下の通り。 BASF SE, Bayer AG, Corteva Agriscience, Euralis Semences and Nufarm(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 栽培面積

- 最も人気のある形質

- 育種技術

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 育種技術

- ハイブリッド

- 非遺伝子組み換え雑種

- 遺伝子組み換え雑種

- 除草剤耐性雑種

- その他の形質

- 開放受粉品種とハイブリッド派生品種

- ハイブリッド

- 地域

- アフリカ

- 育種技術別

- 国別

- エチオピア

- ケニア

- 南アフリカ

- その他のアフリカ

- アジア太平洋地域

- 育種技術別

- 国別

- オーストラリア

- バングラデシュ

- 中国

- インド

- 日本

- ミャンマー

- パキスタン

- ベトナム

- その他アジア太平洋地域

- 欧州

- 育種技術別

- 国別

- フランス

- ドイツ

- イタリア

- オランダ

- ポーランド

- ルーマニア

- ロシア

- スペイン

- トルコ

- ウクライナ

- 英国

- その他欧州

- 中東

- 育種技術別

- 国別

- イラン

- 北米

- 育種技術別

- 国別

- カナダ

- メキシコ

- 米国

- 南米

- 育種技術別

- 国別

- アルゼンチン

- ブラジル

- その他南米

- アフリカ

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Advanta Seeds-UPL

- Anhui Tsuen Yin Hi-Tech Seed Industry Co. Ltd

- BASF SE

- Bayer AG

- Corteva Agriscience

- Euralis Semences

- KWS SAAT SE & Co. KGaA

- Land O'Lakes Inc.

- Nufarm

- RAGT Group

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要洞察

- データパック

- 用語集

目次

Product Code: 92508

The Canola Seed Market (seed For Sowing) size is estimated at 1.95 billion USD in 2025, and is expected to reach 2.52 billion USD by 2030, growing at a CAGR of 5.26% during the forecast period (2025-2030).

Hybrids dominated the global canola seed market, with North America accounting for a major share due to its highest number of GM seed approvals

- Hybrids, known for their high yields and adaptability, dominate canola cultivation, surpassing both open-pollinated varieties (OPVs) and their derivatives.

- Within the canola seed market in 2022, non-transgenic hybrids outshone their transgenic counterparts. This preference stems from the global ban on transgenic crop cultivation and the rising consumer demand for non-GMO food, which is expected to expand the sowing area for non-transgenic varieties.

- In 2022, North America led the way in transgenic hybrids, capturing 88.7% of the market. This dominance can be attributed to the region's numerous approvals and lenient FDA policies.

- Asia-Pacific, with a 34.4% share, emerged as the leader in canola OPVs in 2022, driven by the region's significant adoption of OPVs, primarily due to the expanding organic farming sector, which prohibits the use of transgenic seeds.

- On a global scale, hybrids are outpacing OPVs in terms of growth rates, with projected CAGRs of 5.3% and 5.1% in the canola seed market, respectively, during the forecast period. The surge in hybrid adoption, driven by the desire for higher yields, farm-saved seeds, and organic cultivation, is fueling this trend.

- With a projected CAGR of 9.3%, Mexico is poised to be the fastest-growing market for hybrid canola seeds in the coming years. This growth is underpinned by a rising preference for non-transgenic hybrids.

- The increased demand for animal feed and canola oil, coupled with its ease of cultivation compared to competing crops like corn or wheat, is expected to propel the canola seed market at a CAGR of 5.3% during the forecast period.

Canada dominates canola cultivation, hybrid seeds gain traction globally

- North America is the largest canola, rapeseed, and mustard producer, accounting for 56.1% of the global canola seed market in 2022. This is because canola is highly used for crop rotation practices in North America. Additionally, the strong export market provides a significant economic incentive for farmers to continue producing canola.

- Asia-Pacific accounted for the second-largest canola seed market globally, with a value of USD USD 485.7 million in 2022. This is due to its large area dedicated to canola cultivation.

- Canada accounted for 47.1% of the global canola seed market by value in 2022, and it is the leading exporter of canola seeds. According to the Canola Council of Canada, the country exported about 8.4 million metric ton of canola seeds in 2022, while the major importing countries were the United States, China, and Japan.

- South America and Europe are poised to witness the highest growth rates in the canola seed market, with projected CAGRs of 6.9% and 6.7%, respectively, during the forecast period. This surge is driven by rising consumer demand for canola as an edible oil. Europe, in particular, saw a notable 21.8% uptick in its canola seed market from 2017 to 2022, buoyed by its expanding usage of bio-lubricants.

- In 2022, hybrids accounted for the major share of the global canola seed market, led by Canada and China, which are the major countries. Globally, the hybrid seed segment for canola, rapeseed, and mustard is projected to record a CAGR of 5.3% during the forecast period due to their resistance to different diseases, tolerance to drought, and higher yield.

- Therefore, higher demand from the processing industries and increased cultivation areas may help boost the canola seed market during the forecast period.

Global Canola Seed Market (seed For Sowing) Trends

Asia-Pacific dominated the area under canola cultivation due to high domestic demand and suitable climatic conditions

- Canola, rapeseed, and mustard are prominent oilseed crops cultivated worldwide. From 2016 to 2022, global canola acreage witnessed a 15.4% surge, with Asia-Pacific leading the way. In 2022, the region's canola acreage reached 19.2 million hectares, capturing a commanding 49.0% of the global share. Within Asia-Pacific, India and China emerged as the key players, with cultivated areas of 8.0 million hectares and 6.9 million hectares, respectively, in 2022. Together, they accounted for a significant 77.5% of the region's total. India, in particular, stands as the world's largest canola producer, experiencing a remarkable 39.1% growth in acreage from 2016 to 2022. This surge was primarily driven by robust domestic demand, especially in northern India, where canola is a popular cooking oil.

- North America ranks as the second-largest canola-producing region, representing 25.6% of the global acreage in 2022. Over the 2016-2022 period, the region witnessed a 9.3% growth. Canada dominates this landscape, commanding a staggering 91.0% of the region's canola acreage in 2022. Canadian acreages saw an 8.1% rise from 2016 to 2022, contributing to 20% of the world's canola production, largely driven by surging demand from the food and fuel sectors.

- In 2022, Europe accounted for 24.0% of the global canola acreage, marking an 11.8% increase from 2017 to 2022. Russia emerged as the major producer in the region, commanding 21.4% of the total canola acreage, with a notable 93% surge from 2016 to 2022. South America and Africa held a modest 0.7% and 0.4% share, respectively, of the global canola acreage in 2022. Given the rising demand from the oil industry, a further uptick in acreages is anticipated during the forecast period.

The demand for traits with disease resistance, quality attributes, high oleic content, and drought tolerance for improving the yield of canola is increasing

- Canola dominates as the primary oilseed crop in several countries, finding applications in edible oil, feed, and feed meals. Key quality attributes, including plant height, leaf and ear size, shape, color, maturity, and winter resilience, are being emphasized by major players like Bayer AG, Land O' Lakes, and Corteva Agriscience. Notably, Corteva Agriscience's PT279CL and Bayer AG's Truflex exemplify these quality attributes.

- Disease resistance is a pivotal trait, given canola's vulnerability to ailments like light leaf spots, club roots, black legs, verticillium stem stripe, and sclerotinia. Corteva Agriscience's PT303 and PX131n showcase resistance to light leaf spot and Sclerotinia. Nufarm's Nuseed brand, on the other hand, offers resistance to black legs, club roots, and anti-shatter diseases. Additionally, the trait of wider adaptability is gaining traction, driven by evolving weather patterns and diverse soil types across regions.

- Other sought-after traits, such as high oleic content, lodging resistance, and drought tolerance, are commanding premium prices. In Australia, for instance, canola traits in demand include drought tolerance and early maturity, aligning with the country's changing climate and escalating dry spells. Land O' Lakes' seed varieties, like Surt and Roundup Ready, boast drought tolerance and lodging resistance.

- Seed companies are equipping growers with traits that enhance disease resistance and exhibit high-quality attributes, which may foster market growth in the coming years.

Canola Seed (seed For Sowing) Industry Overview

The Canola Seed Market (seed For Sowing) is fragmented, with the top five companies occupying 27.66%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, Euralis Semences and Nufarm (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.2 Most Popular Traits

- 4.3 Breeding Techniques

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.1.1 Non-Transgenic Hybrids

- 5.1.1.2 Transgenic Hybrids

- 5.1.1.2.1 Herbicide Tolerant Hybrids

- 5.1.1.2.2 Other Traits

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.1.1 Hybrids

- 5.2 Region

- 5.2.1 Africa

- 5.2.1.1 By Breeding Technology

- 5.2.1.2 By Country

- 5.2.1.2.1 Ethiopia

- 5.2.1.2.2 Kenya

- 5.2.1.2.3 South Africa

- 5.2.1.2.4 Rest of Africa

- 5.2.2 Asia-Pacific

- 5.2.2.1 By Breeding Technology

- 5.2.2.2 By Country

- 5.2.2.2.1 Australia

- 5.2.2.2.2 Bangladesh

- 5.2.2.2.3 China

- 5.2.2.2.4 India

- 5.2.2.2.5 Japan

- 5.2.2.2.6 Myanmar

- 5.2.2.2.7 Pakistan

- 5.2.2.2.8 Vietnam

- 5.2.2.2.9 Rest of Asia-Pacific

- 5.2.3 Europe

- 5.2.3.1 By Breeding Technology

- 5.2.3.2 By Country

- 5.2.3.2.1 France

- 5.2.3.2.2 Germany

- 5.2.3.2.3 Italy

- 5.2.3.2.4 Netherlands

- 5.2.3.2.5 Poland

- 5.2.3.2.6 Romania

- 5.2.3.2.7 Russia

- 5.2.3.2.8 Spain

- 5.2.3.2.9 Turkey

- 5.2.3.2.10 Ukraine

- 5.2.3.2.11 United Kingdom

- 5.2.3.2.12 Rest of Europe

- 5.2.4 Middle East

- 5.2.4.1 By Breeding Technology

- 5.2.4.2 By Country

- 5.2.4.2.1 Iran

- 5.2.5 North America

- 5.2.5.1 By Breeding Technology

- 5.2.5.2 By Country

- 5.2.5.2.1 Canada

- 5.2.5.2.2 Mexico

- 5.2.5.2.3 United States

- 5.2.6 South America

- 5.2.6.1 By Breeding Technology

- 5.2.6.2 By Country

- 5.2.6.2.1 Argentina

- 5.2.6.2.2 Brazil

- 5.2.6.2.3 Rest of South America

- 5.2.1 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Advanta Seeds - UPL

- 6.4.2 Anhui Tsuen Yin Hi-Tech Seed Industry Co. Ltd

- 6.4.3 BASF SE

- 6.4.4 Bayer AG

- 6.4.5 Corteva Agriscience

- 6.4.6 Euralis Semences

- 6.4.7 KWS SAAT SE & Co. KGaA

- 6.4.8 Land O'Lakes Inc.

- 6.4.9 Nufarm

- 6.4.10 RAGT Group

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms