|

市場調査レポート

商品コード

1693426

シリコーンシーラント:市場シェア分析、産業動向、統計、成長予測(2025~2030年)Silicone Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| シリコーンシーラント:市場シェア分析、産業動向、統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 299 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

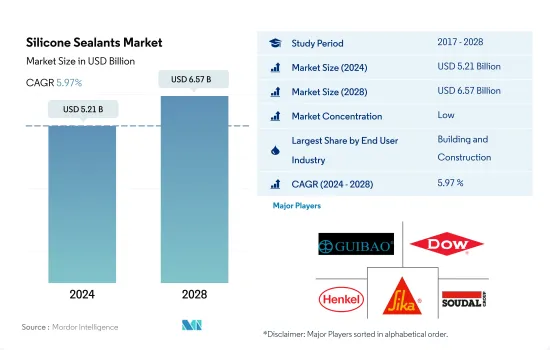

シリコーンシーラント市場規模は2024年に52億1,000万米ドルと推定され、2028年には65億7,000万米ドルに達すると予測され、予測期間(2024~2028年)のCAGRは5.97%で成長します。

シリコーンシーラントの消費を世界的に押し上げると予想される建設と自動車の最終用途部門の台頭

- シリコーンシーラントは、40度Fから140度Fの温度間で硬化し、乾燥のみで、多孔質表面への良好な接着性など、そのユニークな特性のために、最も使用されるタイプです。

- シリコーンシーラントは、防水、天候シール、ひび割れシールなどの用途があるため、建設産業で広く使用されています。世界の建設産業は2030年まで年率3.5%で成長すると予想されています。中国、インド、米国、インドネシアは、世界の建設の約58%を占めると予想されています。

- シリコーンシーラントは、ガラス、金属、プラスチック、塗装面に塗布できるため、自動車産業で広く使用されています。その特徴は、極端な耐候性、耐久性、長持ちなど、自動車産業で役立っています。エンジンや自動車のガスケットにも使われています。自動車産業の電気自動車セグメントは、成長経済圏での需要増加により、予測期間中に17.75%のCAGRで推移すると予想されています。これは、予測期間中に自動車用シリコーンシーラントの需要を押し上げると予想されます。

- シリコーンシーラントは、電子機器や電気機器の製造に広く使用されています。センサやケーブルのシールに使用されます。電子機器産業と民生用電子機器産業は、それぞれCAGR 2.51%と5.77%で世界的に成長すると予想されており、予測期間中にシリコーンシーラントの需要を促進する可能性があります。

- シリコーン樹脂ベースのシーラントは、医療産業で医療機器部品の組み立てやシールに使用されています。世界の医療投資の増加は、予測期間中の需要増加につながると予想されます。

中国の建設セクタと欧州の自動車産業からの需要の高まりが、シリコーンシーラントの世界の売上を牽引する可能性が高いです。

- シリコーンシーラントは、その強力なシーリング特性により世界中で消費されています。これらのシーラントは、建築・建設、自動車、電子機器など10以上の産業で使用されています。シリコーンシーラントは、主に建築・建設産業で消費されています。住宅・非住宅を含む新築床面積は、2022年には2021年比6.15%増の417億平方メートルに達すると予想されています。その結果、シリコーンシーラントの消費量は2022年に2021年比で8.33%の伸びを示しました。

- シリコーンシーラントの需要は、米国、ドイツ、中国、サウジアラビアを含む世界の多くの国々へのCOVID-19パンデミックの影響により、2020年には2019年比で9.09%減少しました。この間、多くの国でロックダウンのため生産施設が閉鎖され、生産用原料の供給が不規則になりました。

- シリコーンシーラントの消費量はアジア太平洋が最も多いが、これは建築・建設産業と自動車産業の増加によるものです。2022年には、世界の建設投資総額の約45%がこの地域からもたらされることになっています。中国は世界最大の建設産業であり、2022~2030年のCAGRは8.6%を記録すると予想されています。日本では、2021年の住宅着工戸数は85万6,480戸で、2020年より4.8%増加しました。このようなアジア太平洋の建設産業の成長は、予測期間にわたってシリコーンシーラントの需要を促進すると予想されます。

- シリコーンシーラントは欧州でも広く消費されています。自動車生産台数は2021年の1,630万台から2027年には1,920万台に達すると予想されています。これらの開発は、予測期間にわたってシリコーンシーラントの需要を押し上げると予想されます。

世界のシリコーンシーラント市場動向

住宅インフラ開発の進展による建設セクタの活性化

- 建築・建設産業は着実な成長を示し、2017~2019年のCAGRは2.6%でした。この成長の原動力となったのは、世界の経済活動の上向きと一戸建て住宅需要の増加です。2020年、COVID-19パンデミックは世界の建築・建設産業に大きな影響を与えました。労働力供給の制約、建設財政とサプライチェーンの混乱、経済の不確実性が世界の建築・建設産業にマイナスの影響を与えました。

- 2021年にはプラス成長を示したもの、パンデミックによるサプライチェーンへの影響は原料価格の高騰を招き、いまだ産業を悩ませています。しかし、建設産業は国の経済に大きな影響を与えるため、北米、アジア太平洋の国々は、支援制度を提供することで、経済サイクルを再起動させるために建設産業を利用してきました。支援制度には、オーストラリアのホームビルダープログラムやEU諸国の景気回復計画などがあります。

- アジア太平洋は建設活動量が最も多く、中国、インド、日本、インドネシア、韓国などの国々における膨大な人口、都市化の進展、インフラ開拓への投資の増加により、2028年まで最大の建設市場であり続けると予想されます。

- グリーンビルディングの重視が高まり、世界の建設活動からの排出を削減する取り組みが進むことで、予測期間中、よりサステイナブル運営手順が実現すると予想されます。例えば、フランスは低炭素エネルギー経済への転換を図るため、建設産業に75億ユーロの予算を計上しています。

電気自動車を促進する有利な政府施策が自動車産業を後押しする

- 2021年以降、世界の自動車産業は安定的に成長すると予想されるが、そのペースは鈍化しています。世界の自動車産業の成長率は年率2%で、予測期間中の総収益の付加価値は1兆5,000億米ドルに達すると予想されます。

- 2020年には、COVID-19パンデミックの影響により、自動車販売台数は減少したが、2021年には急速に回復しました。自動車市場は通常、GDPに大きく貢献しているため、各国政府が経済支援策を講じたからです。自動車販売台数は、2019年の乗用車9,000万台から2020年には7,800万台に減少しました。

- 世界の電気自動車の導入は、その安価なエネルギーコスト、エコフレンドリー性質、効率的なモビリティ機能により、世界の自動車市場全体の収益に大きく貢献しています。また、政府のさまざまな施策や基準も、電気自動車の生産を増加させる原動力となっています。例えば、EUのCO2排出量基準は、2021年に電気自動車の需要を増加させました。IEAのサステイナブルシナリオによれば、2030年までに2億3,000万台の電気自動車が燃焼燃料を使用する自動車に取って代わる必要があります。2021年には、最大のEVメーカーであるTeslaが、電気自動車の製造台数で157%の増加を記録しました。このように電気自動車を好む消費者の動向は、予測期間中(2022~2028年)にさらに高まると予想されます。

シリコーンシーラント産業概要

シリコーンシーラント市場は細分化されており、上位5社で29.40%を占めています。この市場の主要企業は、Chengdu Guibao Science、Technology、Dow、Henkel AG & Co. KGaA、Sika AG、Soudal Holding N.V.などです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主要調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- 規制の枠組み

- アルゼンチン

- オーストラリア

- ブラジル

- カナダ

- 中国

- EU

- インド

- インドネシア

- 日本

- マレーシア

- メキシコ

- ロシア

- サウジアラビア

- シンガポール

- 南アフリカ

- 韓国

- タイ

- 米国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- 医療

- その他

- 地域

- アジア太平洋

- オーストラリア

- 中国

- インド

- インドネシア

- 日本

- マレーシア

- シンガポール

- 韓国

- タイ

- その他のアジア太平洋

- 欧州

- フランス

- ドイツ

- イタリア

- ロシア

- スペイン

- 英国

- その他の欧州

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- 北米

- カナダ

- メキシコ

- 米国

- その他の北米地域

- 南米

- アルゼンチン

- ブラジル

- その他の南米

- アジア太平洋

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- 3M

- Arkema Group

- Chengdu Guibao Science and Technology Co., Ltd.

- Dow

- Guangzhou Jointas Chemical Co.,Ltd.

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Illinois Tool Works Inc.

- MAPEI S.p.A.

- Momentive

- RPM International Inc.

- Shin-Etsu Chemical Co., Ltd.

- Sika AG

- Soudal Holding N.V.

- Wacker Chemie AG

第7章 CEOへの主要戦略的質問

第8章 付録

- 世界の接着剤・シーラント産業概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 促進要因、抑制要因、機会

- 情報源と参考文献

- 図表一覧

- 主要な洞察

- データパック

- 用語集

目次

Product Code: 92485

The Silicone Sealants Market size is estimated at 5.21 billion USD in 2024, and is expected to reach 6.57 billion USD by 2028, growing at a CAGR of 5.97% during the forecast period (2024-2028).

Emerging construction and automotive end-use sector expected to boost the consumption of silicone sealants, globally

- Silicone sealants are the most used type because of their unique properties, such as curing between temperatures of 40 degrees F to 140 degrees F, with drying only, good adhesion to porous surfaces, etc.

- Silicone sealants are widely used in the construction industry because of their applications, such as waterproofing, weather sealing, and crack sealing. The global construction industry is expected to grow at 3.5% per annum up to 2030. China, India, the United States, and Indonesia are expected to account for about 58% of global construction.

- Silicone sealants are widely used in the automotive industry because they apply to glass, metal, plastic, and painted surfaces. Their features are helpful in the automotive industry, such as extreme weather resistance, durability, and long-lasting. They are used in engines and car gaskets. The electric vehicles segment of the automotive industry is expected to record a 17.75% CAGR during the forecast period because of the increase in demand for the same in growing economies. This is expected to boost demand for automotive silicone sealants in the forecast period.

- Silicone sealants are widely used in electronics and electrical equipment manufacturing. They are used for sealing sensors and cables. The electronics and household appliances industries are expected to grow at a CAGR of 2.51% and 5.77%, respectively, globally, which may drive the demand for silicone sealants during the forecast period.

- Silicone resin-based sealants are used in the healthcare industry for assembling and sealing medical device parts. The increase in healthcare investments worldwide is expected to lead to a rise in demand during the forecast period.

Inflating demand from China's construction sector and Europe's automotive industry likely to drive the global sales of silicone sealants

- Silicone sealants are consumed across the globe due to their strong sealing properties. These sealants are used in more than ten industries, including building and construction, automotive, and electronics. Silicone sealants are consumed mainly in the building and construction industry. The new floor area, including residential and non-residential buildings, was expected to reach 41.7 billion square footage in 2022, 6.15% more than in 2021. As a result, the consumption of silicone sealants witnessed a growth of 8.33% in 2022 compared to 2021.

- The demand for silicone sealants fell by 9.09% in 2020 compared to 2019 due to the COVID-19 pandemic's impact on many countries worldwide, including the United States, Germany, China, and Saudi Arabia. Production facilities were shut down during the period owing to lockdowns in many countries, which resulted in an irregular supply of raw materials for production.

- Asia-Pacific accounts for the highest silicone sealants consumption due to the rising building and construction and automotive industries. About 45% of the total construction investment in the world was set to come from this region in 2022. China is the world's largest construction industry, and it is expected to record a CAGR of 8.6% during the period 2022-2030. In Japan, the number of housing construction starts in 2021 were 856.48 thousand units, 4.8% more than in 2020. Such growth in the Asia-Pacific construction industry is expected to drive demand for silicone sealants over the forecast period.

- Silicone sealants are also widely consumed in Europe. Automotive production is expected to reach 19.2 million units by 2027 from 16.3 million units in 2021. These developments are expected to boost the demand for silicone sealants over the forecast period.

Global Silicone Sealants Market Trends

Growing residential and infrastructural development to thrive the construction sector

- The building and construction industry witnessed steady growth, with a CAGR of 2.6% from 2017 to 2019. This growth was driven by the upswing in global economic activity and increasing demand for single-family homes. In 2020, the COVID-19 pandemic had a major impact on the global building and construction industry. Constraints in labor supply, disruptions in construction finances and the supply chain, and economic uncertainty negatively impacted the global building and construction industry.

- Though the industry showed positive growth in 2021, the pandemic's effect on supply chains, which resulted in a hike in raw material prices, is still plaguing the industry. However, as the construction industry heavily influences a nation's economy, countries in Europe, North America, and Asia-Pacific have used the construction industry to restart their economic cycles by offering support schemes. Some support schemes include the Homebuilder Programme in Australia and the economic recovery plan of EU countries.

- The Asia-Pacific region experiences the highest volume of construction activities, and it is expected to remain the largest construction market till 2028 due to its huge population, increasing urbanization, and increasing investments in infrastructural development in countries like China, India, Japan, Indonesia, and South Korea.

- Increasing emphasis on green buildings and efforts to reduce emissions from global construction activities are expected to result in more sustainable operational procedures during the forecast period. For example, France has sanctioned EUR 7.5 billion for the construction industry to transform itself into a low-carbon energy economy.

Favorable government policies to promote electric vehicles will propel automotive industry

- Since 2021, the global automotive industry has been expected to grow steadily but at a slower pace because of the decline in consumers' preferences for individual ownership of passenger vehicles and their increased preference for shared mobility in transportation. The global automotive industry is expected to experience a growth rate of 2% annually, with an expected value addition of USD 1.5 trillion in total revenue during the forecast period.

- In 2020, due to the impact of the COVID-19 pandemic, vehicle sales declined but recovered rapidly in 2021 because the governments of various countries took measures to support their economies, as automotive markets usually contribute majorly to their GDP. Vehicle sales declined from 90 million units of passenger vehicles in 2019 to 78 million units in 2020.

- The introduction of electric vehicles worldwide has contributed significantly to the overall revenue of the global automotive market because of their cheaper energy costs, environmentally benign nature, and efficient mobility features. Various government policies and standards also work as driving factors to increase EV production. For instance, the EU standards for CO2 emissions increased the demand for electric vehicles in 2021. As per the IEA's Sustainable Scenario, 230 million electric vehicles are required to replace combustion fuel-based vehicles by 2030. In 2021, Tesla, the largest EV manufacturer, recorded a rise of 157% in the number of electric vehicles manufactured. This growing trend of consumers preferring electric vehicles is expected to rise further during the forecast period (2022-2028).

Silicone Sealants Industry Overview

The Silicone Sealants Market is fragmented, with the top five companies occupying 29.40%. The major players in this market are Chengdu Guibao Science and Technology Co., Ltd., Dow, Henkel AG & Co. KGaA, Sika AG and Soudal Holding N.V. (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.2 Regulatory Framework

- 4.2.1 Argentina

- 4.2.2 Australia

- 4.2.3 Brazil

- 4.2.4 Canada

- 4.2.5 China

- 4.2.6 EU

- 4.2.7 India

- 4.2.8 Indonesia

- 4.2.9 Japan

- 4.2.10 Malaysia

- 4.2.11 Mexico

- 4.2.12 Russia

- 4.2.13 Saudi Arabia

- 4.2.14 Singapore

- 4.2.15 South Africa

- 4.2.16 South Korea

- 4.2.17 Thailand

- 4.2.18 United States

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Healthcare

- 5.1.5 Other End-user Industries

- 5.2 Region

- 5.2.1 Asia-Pacific

- 5.2.1.1 Australia

- 5.2.1.2 China

- 5.2.1.3 India

- 5.2.1.4 Indonesia

- 5.2.1.5 Japan

- 5.2.1.6 Malaysia

- 5.2.1.7 Singapore

- 5.2.1.8 South Korea

- 5.2.1.9 Thailand

- 5.2.1.10 Rest of Asia-Pacific

- 5.2.2 Europe

- 5.2.2.1 France

- 5.2.2.2 Germany

- 5.2.2.3 Italy

- 5.2.2.4 Russia

- 5.2.2.5 Spain

- 5.2.2.6 United Kingdom

- 5.2.2.7 Rest of Europe

- 5.2.3 Middle East & Africa

- 5.2.3.1 Saudi Arabia

- 5.2.3.2 South Africa

- 5.2.3.3 Rest of Middle East & Africa

- 5.2.4 North America

- 5.2.4.1 Canada

- 5.2.4.2 Mexico

- 5.2.4.3 United States

- 5.2.4.4 Rest of North America

- 5.2.5 South America

- 5.2.5.1 Argentina

- 5.2.5.2 Brazil

- 5.2.5.3 Rest of South America

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 Chengdu Guibao Science and Technology Co., Ltd.

- 6.4.4 Dow

- 6.4.5 Guangzhou Jointas Chemical Co.,Ltd.

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 Illinois Tool Works Inc.

- 6.4.9 MAPEI S.p.A.

- 6.4.10 Momentive

- 6.4.11 RPM International Inc.

- 6.4.12 Shin-Etsu Chemical Co., Ltd.

- 6.4.13 Sika AG

- 6.4.14 Soudal Holding N.V.

- 6.4.15 Wacker Chemie AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms