|

市場調査レポート

商品コード

1693396

中国のシーラント:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)China Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中国のシーラント:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 159 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

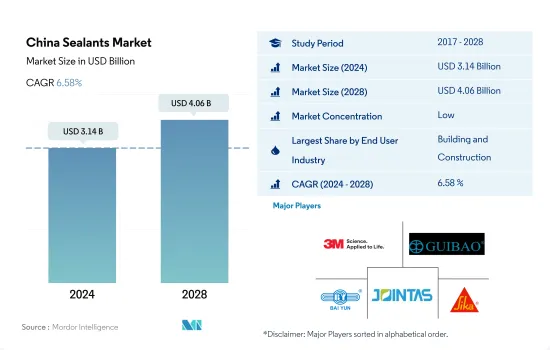

中国のシーラント市場規模は2024年に31億4,000万米ドルと推計され、2028年には40億6,000万米ドルに達すると予測され、予測期間(2024~2028年)のCAGRは6.58%で成長する見込みです。

防水、ひび割れシール、目地シールの用途で建設用シーラントがシーラントを押し上げる

- 中国のシーラント市場は、防水、クラックシーリング、ジョイントシーリングなど、建築・建設活動におけるシーラントの多様な用途により、建設業界が主要な牽引役となり、その他のエンドユーザー業界がそれに続きます。さらに、建設用シーラントは、耐用年数が長く、さまざまな基材に簡単に塗布できるように設計されています。COVID-19の影響によるサプライチェーンの混乱や生産停止にもかかわらず、建設セクターは2020年に6.9%のGDPを達成しました。

- 電気機器製造では、ポッティングや保護用途にさまざまなシーラントが使用されています。これらはセンサーやケーブルなどのシールに使用されます。中国のエレクトロニクス市場は2020年に世界で41%の市場シェアを記録し、巨大な労働力を持つ製造エコシステムの広範な存在により、今後数年間は持続的な成長が見込まれます。このことは、他のエンドユーザーセグメントにおけるシーラント需要を促進すると思われます。さらに、中国は世界の機関車や海洋産業のための大規模な生産能力を持っており、必要なシーラントの需要を後押ししています。

- シーラントはヘルスケアと自動車産業において多様な用途があります。シーラントは、医療機器部品の組み立てやシーリングといったヘルスケア用途で使用されています。自動車産業は、シーラントが様々な基材に使用されており、主にエンジンや自動車のガスケットに使用されています。中国は近年、これらの分野、特に自動車産業で有望な成長を記録しており、今後数年間も続くと見られ、2028年までにシーラントの需要を増大させると思われます。

中国のシーラント市場動向

中国政府によるヘルスケア、病院、医療施設の建設計画が中国の建設を牽引

- 中国は、住宅および商業建設セクターの豊富な開発によって大きく牽引されており、経済成長に支えられています。中国は継続的な都市化のプロセスを推進しており、2030年の目標率は70%です。都市化の結果、都市部で必要とされる居住空間が拡大し、都市部の中産階級住民が生活環境の改善を望むようになることは、住宅市場に大きな影響を与え、それによって国内の住宅建設が増加する可能性があります。

- 非住宅インフラは大幅に拡大する可能性が高いです。高齢化が進む中国では、ヘルスケア施設や病院の増設が必要となります。中国政府は2019年に約1,420億米ドルに相当する26のインフラプロジェクトを承認し、2023年に完了する予定です。同国は世界最大の建設市場を誇り、全世界の建設投資の20%を占めています。

- 中国では、香港の住宅当局が低価格住宅の建設を推進するためにいくつかの施策を開始しました。当局は2030年までに30万1000戸の公共住宅を供給することを目指しています。世帯所得水準の上昇と農村部から都市部への人口移動が相まって、同国の住宅建設セクターの需要は引き続き拡大すると予想されます。2030年までに、同国は建設に13兆米ドル以上を投じると推定されています。そのため、建設市場は予測期間中(2022~2028年)にCAGR 4.48%を記録すると予想されます。

政府の政策により、中国でのEV需要が高まり、自動車生産が促進される可能性が高い

- 中国の乗用車市場は2021年に2,141万台を占め、日本、米国、ドイツなど他の主要な世界企業と比較して世界最大です。中国の電気自動車メーカーであるBYDは、世界の電気自動車生産台数の8.84%を占めています。

- COVID-19パンデミックの震源地である中国では、全国的な操業停止、サプライチェーンの混乱、人材不足などが発生し、2020年の自動車産業で莫大な損失が発生しました。これが2020年の中国の前年比成長率がマイナスとなった理由です。

- 中国政府による電気自動車所有者に対する期間限定の購入補助金、交通規制の免除、充電リベートなどの政策は、中国における電気自動車の販売と需要を促進しました。電気自動車の販売台数は、2027年には752万6,000台に達すると予想されています。中国のEV生産台数は2019年の100万台から2021年には350万台に増加し、予測期間(2022~2028年)のCAGRは15.07%を記録すると予想されます。

- 上海汽車工業公司は生産台数で中国最大の自動車会社です。SAICが生産する乗用車と商用車の台数の伸びは著しく、2019年の約200万台から2021年には700万台に増加しています。この成長動向は、中国自動車市場が予測期間中に安定的に成長すると予想されることを示しています。

中国のシーラント業界の概要

中国のシーラント市場は細分化されており、上位5社で20.34%を占めています。この市場の主要企業は以下の通りです。 3M, Chengdu Guibao Science and Technology, Guangzhou Baiyun Chemical Industry, Guangzhou Jointas Chemical and Sika AG(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- 規制の枠組み

- 中国

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- ヘルスケア

- その他のエンドユーザー産業

- 樹脂

- アクリル

- エポキシ

- ポリウレタン

- シリコーン

- その他の樹脂

第6章 競合情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- 3M

- Arkema Group

- Chengdu Guibao Science and Technology Co., Ltd.

- Dow

- Guangzhou Baiyun Chemical Industry Co.,ltd.

- Guangzhou Jointas Chemical Co.,Ltd.

- H.B. Fuller Company

- Hangzhou Zhijiang Advanced Material Co., ltd.

- Henkel AG & Co. KGaA

- Sika AG

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の接着剤とシーラント産業の概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 促進要因、阻害要因、機会

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

The China Sealants Market size is estimated at 3.14 billion USD in 2024, and is expected to reach 4.06 billion USD by 2028, growing at a CAGR of 6.58% during the forecast period (2024-2028).

Construction sealants to boost the sealants, owing to waterproofing, cracks-sealing, and joint-sealing applications

- The China sealants market is majorly driven by the construction industry, followed by other end-user industries due to diverse applications of sealants in building and construction activities, such as waterproofing, cracks-sealing, and joint-sealing. Moreover, construction sealants are designed for longevity and ease of application on different substrates. The construction sector achieved a GDP of 6.9% in 2020 despite supply chain disruption and production suspension due to COVID-19 impacts.

- A variety of sealants are used in electrical equipment manufacturing for potting and protecting applications. They are used for sealing sensors and cables, etc. The Chinese electronics market registered a market share of 41% globally in 2020 and is likely to have sustainable growth in the upcoming years due to the extensive presence of the manufacturing ecosystem with a huge labor force. This, in terms, will foster the demand for sealants in the other end-user segment. Moreover, China has a massive production capacity for locomotive and marine industries in the world, boosting the demand for required sealants.

- Sealants have diverse applications in the healthcare and automotive industries. Sealants are used in healthcare applications such as assembling and sealing medical device parts. The automotive industry exhibits significant applicability of sealants to various substrates, mostly used for engines and car gaskets. China registered promising growth in these sectors, specifically in automotive, in recent times and is likely to continue in the upcoming years, which will augment the demand for sealants by 2028.

China Sealants Market Trends

Housing, hospitals, and healthcare facilities schemes by the Chinese government to lead the construction in the country

- China has been majorly driven by the ample developments in the residential and commercial construction sectors and supported by the growing economy. China is promoting and undergoing a process of continuous urbanization, with a target rate of 70% for 2030. The increased living spaces required in the urban areas resulting from urbanization and the desire of middle-class urban residents to improve their living conditions may have a profound effect on the housing market and thereby increase the residential construction in the country.

- Non-residential infrastructure is likely to expand significantly. The country's aging population necessitates the construction of additional healthcare facilities and hospitals. The Chinese government approved 26 infrastructure projects worth approximately USD 142 billion in 2019, with completion due in 2023. The country boasts the world's largest construction market, accounting for 20% of all worldwide construction investments.

- In China, the housing authorities of Hong Kong launched several measures to push start the construction of low-cost housing. The officials aim to provide 301,000 public housing units by 2030. The rising household income levels, combined with the population migrating from rural to urban areas, are expected to continue to drive the demand for the residential construction sector in the country. By 2030, the country is estimated to spend over USD 13 trillion on construction. Thus, the construction market is expected to register a 4.48% CAGR during the forecast period (2022-2028).

Owing to government policies, EVs demand in China is rising and is likely to propel the automotive production

- China's automotive market for passenger vehicles is the largest in the world, as it accounted for 21.41 million units in 2021 compared to other major global players such as Japan, the United States, and Germany. This number is expected to grow at the same pace because of the increasing production capacity of automotive companies post-pandemic in China, as BYD, which is a local electric vehicle manufacturer in China, holds 8.84% of total electric vehicle production in the world.

- China, being the epicenter of the COVID-19 pandemic, witnessed huge losses in the automotive industry in 2020 as it led to nationwide lockdowns, supply chain disruptions, lack of human resources availability, etc. This was the reason for the negative Y-o-Y growth rate in China in 2020.

- The Chinese government's policies for electric vehicle owners, such as time-limited purchase subsidies, traffic regulations waivers, and charging rebates for EV owners, have encouraged the sale and demand for EVs in China. The sales of electric vehicles are expected to reach 7,526 thousand in 2027. EV production in China increased from 1 million units in 2019 to 3.5 million units in 2021, and it is expected to record a 15.07% CAGR in the forecast period (2022-2028).

- Shanghai Automotive Industry Corporation is China's largest automotive company in terms of production. The growth in the number of both passenger and commercial vehicles manufactured by SAIC is significant, as it increased from nearly 2 million units in 2019 to 7 million units in 2021. This growth trend shows that the Chinese automotive market is expected to grow steadily during the forecast period.

China Sealants Industry Overview

The China Sealants Market is fragmented, with the top five companies occupying 20.34%. The major players in this market are 3M, Chengdu Guibao Science and Technology Co., Ltd., Guangzhou Baiyun Chemical Industry Co.,ltd., Guangzhou Jointas Chemical Co.,Ltd. and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.2 Regulatory Framework

- 4.2.1 China

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Healthcare

- 5.1.5 Other End-user Industries

- 5.2 Resin

- 5.2.1 Acrylic

- 5.2.2 Epoxy

- 5.2.3 Polyurethane

- 5.2.4 Silicone

- 5.2.5 Other Resins

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Arkema Group

- 6.4.3 Chengdu Guibao Science and Technology Co., Ltd.

- 6.4.4 Dow

- 6.4.5 Guangzhou Baiyun Chemical Industry Co.,ltd.

- 6.4.6 Guangzhou Jointas Chemical Co.,Ltd.

- 6.4.7 H.B. Fuller Company

- 6.4.8 Hangzhou Zhijiang Advanced Material Co., ltd.

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Sika AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms