|

市場調査レポート

商品コード

1693395

スペインのシーラント:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Spain Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| スペインのシーラント:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 157 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

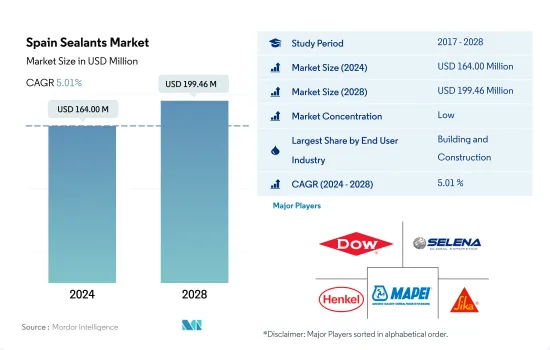

スペインのシーラント市場規模は2024年に1億6,400万米ドルと推定され、2028年には1億9,946万米ドルに達すると予測され、予測期間(2024年~2028年)のCAGRは5.01%で成長すると予測されます。

新規建設とインフラ開発が市場成長を牽引

- スペインのシーラント市場は、防水、耐候性シーリング、ひび割れシーリング、目地シーリングなど、建築・建設活動におけるシーラントの多様な用途により、建設業界が主要な牽引役となり、その他のエンドユーザー業界がそれに続きます。さらに、建築用シーラントは、耐用年数が長く、さまざまな基材に簡単に塗布できるように設計されています。スペインの建設産業は、2019年に同国のGDPの約5.7%を記録しました。COVID-19の間、建設生産高は2020年に19.5%減少し、同国における建設投資と住宅メンテナンス活動の増加により2021年に持続しました。このような動向は近い将来も続き、シーラント需要を徐々に増加させる可能性が高いです。

- 電気機器製造では、さまざまなシーラントがポッティングや保護用途に使用されています。センサーやケーブルのシールなどに使用されます。スペインの電子機器市場は、ワイヤレス電子機器の人気の高まりとウェアラブルガジェットの急速な普及により、大きな成長を記録しました。このことは、他のエンドユーザーセグメントにおけるシーラントの需要を促進します。さらに、機関車やDIY産業におけるシーラントのさまざまなアプリケーションは、2028年までに必要なシーラントの需要を押し上げると思われます。

- シーラントはヘルスケアと自動車産業で多様な用途があります。シーラントは、医療機器部品の組み立てやシールなどのヘルスケア用途で使用されています。自動車産業は、様々な基材へのシーラントの大きな適用性を示しており、主にエンジンや自動車のガスケットに使用されています。スペインは最近、これらの分野で有望な成長を記録しており、今後数年間も続くと思われます。したがって、このような傾向は、2028年までにシーラントの需要を増強すると思われます。

スペインのシーラント市場動向

手ごろな価格の住宅向けに10億ユーロ相当の国家復旧・復興計画(NRRP)などの投資が建設業界を牽引

- COVID-19パンデミックのスペイン建設セクターへの影響は甚大でした。建設業界は打撃を受け、2020年1~3月の投資額は9.6%減少しました。運輸・ホテル部門の2020年第1四半期の建設活動生産高は11%の減少を記録しました。

- 建設市場を回復させるため、スペイン政府は2022年12月31日までの延長を含む国家住宅計画2018-2021の修正を導入しました。同国はまた、欧州投資銀行(EIB)から社会住宅の開発・建設に対する財政支援を受けています。スペインの建設市場は2021年に力強く回復し、約24.9%の成長を遂げることになりました。2021年6月の時点で、EIBはバルセロナ市議会が3,620万ユーロを投資して約490戸の新しい公共賃貸住宅を建設することを支援する契約を締結しました。

- スペイン政府は、2021~2026年の国家復興レジリエンス計画(NRRP)の下、手頃な価格でエネルギー効率の高い賃貸住宅の建設に10億ユーロを割り当てた。このため、同国の建設市場は予測期間中(2022~2028年)に2%のCAGRで推移すると予想されます。

- スペインの建設業界の見通しは総じて良好です。公共インフラへの投資、デジタル化、エネルギー効率の高い住宅の改築、欧州連合(EU)の資金援助によるグリーンな循環型経済などが、今後の業界の成長を後押しすると予想されます。

EV需要の増加と240億ユーロに相当する公的・民間eモビリティ投資による自動車需要の拡大

- スペインはドイツに次いで欧州第2位の自動車生産国です。スペインの自動車サプライヤーは2019年に358億2,200万ユーロ相当の製品を生産し、そのうち60%が欧州域内外に輸出されました。

- 同国の自動車生産はここ数年ほぼ一定しています。2019年、同国の生産台数は約282万2,355台で、2018年比0.1%の微々たる成長率を記録しました。2020年の同国の自動車生産台数は約226万8,185台でした。COVID-19パンデミックによりサプライチェーンが停止したため、2020年の自動車生産台数は18.6%減少しました。

- 2021年第1~3四半期の自動車生産台数は、2020年第1~3四半期比で4%増加し、159万2,277台に達しました。同国の自動車産業は、予測期間中、緩やかな需要となりそうです。しかし、2021年の同国の自動車生産台数は約209万8,133台で、2020年から8%減少しました。半導体チップ不足とサプライチェーンの制約が、同国の自動車生産台数に悪影響を及ぼしました。

- 自動車生産台数の不足は最近悪化しており、2022年には生産台数が18%増加し、力強い回復が見込まれます。スペインの電気自動車市場は、サプライヤーのeモビリティへのシフトを支援する次世代EU基金の恩恵を受けるはずです。さらにスペイン政府は、今後3年間で240億ユーロに相当する公的および民間のeモビリティ投資を発表しています。

スペインのシーラント産業概要

スペインのシーラント市場は細分化されており、上位5社で35.13%を占めています。この市場の主要企業は以下の通り。 Dow, Grupa Selena, Henkel AG & Co. KGaA, MAPEI S.p.A. and Sika AG(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- エンドユーザー動向

- 航空宇宙

- 自動車

- 建築・建設

- 規制の枠組み

- スペイン

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- エンドユーザー産業

- 航空宇宙

- 自動車

- 建築・建設

- ヘルスケア

- その他のエンドユーザー産業

- 樹脂

- アクリル

- エポキシ

- ポリウレタン

- シリコーン

- その他の樹脂

第6章 競合情勢

- 主要な戦略的動き

- 市場シェア分析

- 企業情勢

- 企業プロファイル.

- 3M

- Dow

- Grupa Selena

- Henkel AG & Co. KGaA

- Industrias Quimicas del Adhesivo, S.A.-Quiadsa

- MAPEI S.p.A.

- QS Adhesives & Sealants SL

- RPM International Inc.

- Sika AG

- Soudal Holding N.V.

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界の接着剤とシーラント産業の概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 促進要因、阻害要因、機会

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

Product Code: 92451

The Spain Sealants Market size is estimated at 164.00 million USD in 2024, and is expected to reach 199.46 million USD by 2028, growing at a CAGR of 5.01% during the forecast period (2024-2028).

New construction and infrastructure development to lead the market growth

- The Spain sealants market is majorly driven by the construction industry, followed by other end-user industries due to diverse applications of sealants in building and construction activities such as waterproofing, weather-sealing, cracks-sealing, and joint-sealing. Moreover, construction sealants are designed for longevity and ease of application on different substrates. The construction industry of Spain registered around 5.7% of the country's GDP in 2019. During COVID-19, the construction output was reduced by 19.5% in 2020, sustained in 2021 owing to increasing construction investment and home maintenance activities in the country. Such trends will likely continue in the near future and gradually increase sealants demand.

- A variety of sealants are used in electrical equipment manufacturing for potting and protecting applications. They are used for sealing sensors and cables, etc. The Spanish electronics market registered significant growth, mostly due to the growing popularity of wireless electronic devices and the rapid adoption of wearable gadgets. This, in terms, will foster the demand for sealants in the other end-user segment. Moreover, a range of applications of sealants in the locomotive and DIY industries will boost the demand for required sealants by 2028.

- Sealants have diverse applications in the healthcare and automotive industries. Sealants are used in healthcare applications, such as assembling and sealing medical device parts. The automotive industry exhibits significant applicability of sealants to various substrates, mostly used for engines and car gaskets. Spain has registered promising growth in these sectors in recent times and is likely to continue in the upcoming years. Thus, such a trend will augment the demand for sealants by 2028.

Spain Sealants Market Trends

Investments including National Recovery and Resilience Plan (NRRP) worth EUR 1 billion for affordable housing to lead the construction industry

- The impact of the COVID-19 pandemic was huge on the Spanish construction sector. The construction industry pummeled and observed a decline of 9.6% in investments in the first three months of 2020. Construction activity output in the transport and hotel sector registered a decline of 11% in Q1 2020.

- To revive the construction market, the Spanish government introduced amendments to the State Housing Plan 2018-2021, including the program's extension until December 31, 2022. The country also receives financial support from the European Investment Bank (EIB) for developing and constructing social housing. The Spanish construction market was to rebound strongly in 2021 and grow about 24.9% in 2021. As of June 2021, the EIB signed an agreement to support Barcelona City Council in constructing nearly 490 new public rental homes with an investment of EUR 36.2 million.

- Under its 2021-2026 National Recovery and Resilience Plan (NRRP), the Spanish government allocated EUR 1 billion to construct affordable and energy-efficient rental housing. Thus, the construction market in the country is expected to register a 2% CAGR during the forecast period (2022-2028).

- The general outlook for the Spanish construction industry is favorable. Future industry growth is anticipated to be fueled by investments in public sector infrastructure, digitalization, energy-efficient housing renovations, and a green circular economy, all funded by the European Union.

Increasing EVs demand and government investment of public and private e-mobility investments worth EUR 24 billion to boost the automotive demand

- Spain is the second-largest automobile producer in Europe, after Germany. Spanish automotive suppliers produced EUR 35,822 million worth of products in 2019, of which 60% were exported inside and outside the European region.

- Automobile production in the country has been almost constant in the past few years. In 2019, the country produced about 28,22,355 units, registering a meager growth rate of 0.1% over 2018. The country produced about 22,68,185 units of vehicles in 2020. Automotive vehicle production contracted by 18.6% in 2020 as the COVID-19 pandemic halted the supply chain.

- In the first three quarters of 2021, automotive production increased by 4% over Q1-Q3 of 2020 and reached 1,592,277 vehicles. The country's automotive industry is likely to witness moderate demand during the forecast period. However, in 2021, the country produced about 2,098,133 vehicles, which was a decline of 8% from 2020. The semiconductor chip shortage and supply chain restrictions negatively affected the production of automotive vehicle units in the country.

- The automotive production shortfalls have recently worsened, and a strong rebound is expected in 2022, with output increasing by 18%. The Spanish electric vehicles market should benefit from the Next Generation EU fund, which supports suppliers in their shift toward e-mobility. Additionally, the Spanish government has announced public and private e-mobility investments worth EUR 24 billion over the coming three years.

Spain Sealants Industry Overview

The Spain Sealants Market is fragmented, with the top five companies occupying 35.13%. The major players in this market are Dow, Grupa Selena, Henkel AG & Co. KGaA, MAPEI S.p.A. and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.2 Regulatory Framework

- 4.2.1 Spain

- 4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Healthcare

- 5.1.5 Other End-user Industries

- 5.2 Resin

- 5.2.1 Acrylic

- 5.2.2 Epoxy

- 5.2.3 Polyurethane

- 5.2.4 Silicone

- 5.2.5 Other Resins

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 3M

- 6.4.2 Dow

- 6.4.3 Grupa Selena

- 6.4.4 Henkel AG & Co. KGaA

- 6.4.5 Industrias Quimicas del Adhesivo, S.A. - Quiadsa

- 6.4.6 MAPEI S.p.A.

- 6.4.7 QS Adhesives & Sealants SL

- 6.4.8 RPM International Inc.

- 6.4.9 Sika AG

- 6.4.10 Soudal Holding N.V.

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

- 8.1 Global Adhesives and Sealants Industry Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Drivers, Restraints, and Opportunities

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms