|

市場調査レポート

商品コード

1911700

接着剤:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 接着剤:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

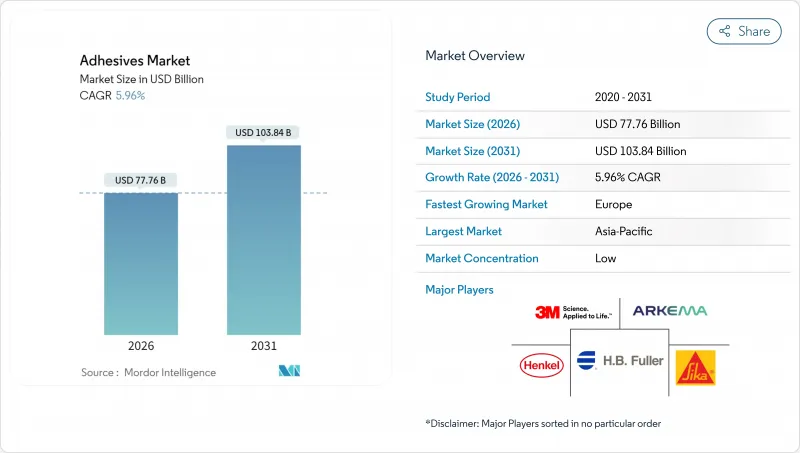

接着剤市場は、2025年の733億9,000万米ドルから2026年には777億6,000万米ドルへ成長し、2026年から2031年にかけてCAGR5.96%で推移し、2031年までに1,038億4,000万米ドルに達すると予測されております。

電子商取引に伴う包装自動化の拡大、インフラ事業における構造接着の優先度向上、自動車メーカーによる軽量複合材料設計を支える接着剤使用量の増加により、需要は加速しています。ブランドがVOC規制値を満たす必要性から水性化学品が主流を占める一方、溶剤不要の加工性と高速ライン対応によりホットメルトプラットフォームのシェアが拡大しています。樹脂分野では、アクリル系が高性能用途で引き続き主導的地位を維持する一方、VAE/EVA系は柔軟性とコスト効率の高さから建設分野での使用量を獲得しています。地域別の動向は分岐しており、アジア太平洋地域が数量成長を牽引する一方、欧州では規制対応の高付加価値グレードが拡大しております。

世界の接着剤市場の動向と洞察

Eコマースの急成長が安全で高速な包装用接着剤の需要を拡大

オンライン小売倉庫では、ミリ秒単位で硬化しながらもコンベア衝撃や複合輸送に耐え、箱の完全性を維持するホットメルト・感圧接着剤グレードが採用されています。フルフィルメントセンターでは二桁の注文増加が報告され、主要EC回廊における包装用接着剤の需要量は15~20%増加しています。インドのオンライン小売セクターだけでも、2024年に包装用接着剤の需要を18%押し上げました。これは、ブランドオーナーが熱帯気候に適した改ざん防止シールを義務付けたためです。持続可能性目標は、紙リサイクル工程と互換性のある水性およびバイオ由来の選択肢にさらなる勢いを加えています。包装業者は現在、基材を清潔な状態で残し、二次繊維回収を容易にする、容易に剥離可能なグレードを指定しています。

世界の建設アップサイクルが構造用・床用接着剤の消費を増加

アジア太平洋地域におけるメガプロジェクトの計画が加速し、機械的締結が非効率または故障リスクの高いコンクリート・鋼材・複合材接合向けに、高強度・速硬化型配合の需要が高まっています。大型タイルやプレハブパネルには、施工サイクル短縮と構造的完全性を高めるせん断抵抗性接着剤が求められています。ワッカー・ケミー社は2024年、タイルおよび断熱システム向け建設用接着剤の需要増に対応するため、南京とカルバートシティにおけるVAE生産能力を拡大いたしました。欧州および北米におけるエネルギー改修インセンティブは、気流遮断シーラントおよび断熱接着剤の需要を持続させております。一方、改訂された建築基準法は、耐震性と熱橋低減のための接着接合を推奨しております。

石油原料価格の変動がメーカーの利益率を圧迫

エチレンやプロピレンなどの原油連動型モノマーは、接着剤原料コストの最大60%を占めます。2024年にはアクリル酸価格が25~30%変動し、特にヘッジ能力のない中小コンバーター企業において、四半期ごとの追加料金が利益率を圧迫しました。為替変動は、世界のに調達しながら現地で請求を行う企業にとって負担を増大させます。変動リスクを緩和するため、メーカーは二重調達や在庫リスク戦略を採用していますが、これらは物流の複雑化と運転資金需要の増加を招いています。

セグメント分析

アクリル系システムは、建築ファサード、自動車内装材、感圧ラベルにおける耐候性性能に支えられ、2025年の世界接着剤市場で22.60%のシェアを占めました。VAE/EVA製品ラインは、柔軟性のある床材、タイル固定、包装フィルムラミネーションの需要拡大により、2031年までCAGR6.28%で成長しています。ポリウレタン系グレードは、高い接着強度、耐薬品性、弾性が重要な輸送機器および航空宇宙分野で確固たる地位を維持しております。エポキシ系は、極端な熱や疲労に直面する電子機器や風力ブレード接合部に使用されますが、硬化サイクルが長いため成長は遅れております。ハイブリッド化学技術は現在、アクリルの紫外線耐性とポリウレタンの強靭性、あるいはVAEの柔軟性とエポキシの剛性を組み合わせ、配合設計者のツールキットを拡大しております。

樹脂の継続的な革新により、コンバーターが特定の基材や使用環境に合わせて性能を微調整する中で、世界の接着剤市場は拡大を続けております。アクリル系メーカーは耐水白化性を高める自己架橋性エマルションに投資し、VAEサプライヤーは低表面エネルギーフィルムへの接着性を向上させるため極性モノマー含有量を増やしています。バイオベース原料の需要は増加していますが、コストと供給量の拡大可能性が急速な普及を制限しています。戦略的な樹脂選定では、規制適合性、使用温度、総適用コストのバランスがますます重視され、メーカーはコモディティ化した最終用途において差別化を図ることが可能となっています。

本接着剤レポートは、樹脂別(ポリウレタン、エポキシ、アクリル、シアノアクリレート、VAE/EVAなど)、技術別(水性、溶剤系、反応性など)、エンドユーザー産業(建築・建設、包装、自動車、航空宇宙、木工・建具など)、地域(アジア太平洋、北米、欧州など)で構成されています。市場予測は金額(米ドル)で提供されます。

地域別分析

アジア太平洋地域は、中国、インド、東南アジアにおける集中的な製造クラスターと公共インフラ投資により、世界の接着剤市場の36.30%を占めております。中国の都市鉄道および住宅プロジェクトは構造用アクリル樹脂の需要を促進し、インドのタイル用接着剤セグメントは急速な都市住宅建設により年間15%以上の成長を見せております。ヘンケル社やテサ社などの新規工場を含む地域サプライヤーは、現地での供給体制を強化し、リードタイムを短縮しています。特にEVAやアクリルエマルジョンでは、計画中の増産が下流需要の減速により過剰在庫リスクを伴うため、生産能力過剰への懸念が継続しています。

欧州は2031年まで年平均CAGR6.25%と最も高い伸びが見込まれております。規制強化により加工業者が再生可能で低排出のシステムへ移行しているためです。2026年施行のEU包装・包装廃棄物規制では、機械的リサイクル工程で完全に分離可能かつPFAS含有量ゼロの接着剤が要求されます。ドイツのEV移行は熱伝導性・難燃性接着剤の需要を牽引し、フランスの建築改修補助金制度は断熱材用接着剤の需要を刺激しています。

北米では関税によるモノマー投資が供給安定性を強化し、着実な成長を維持しています。2025年以降に稼働開始予定のアクリル酸生産能力(米国メキシコ湾岸地域)は輸入依存度を低減し、輸送時間の短縮により地域の配合メーカーを支援します。メキシコは自動車輸出拠点としての役割から構造用・ヘムフランジ用接着システムの需要を押し上げており、一方カナダでは寒冷地建築基準によりパネル化住宅向け凍結耐性接着剤が好まれています。この動向はインフラ法案の進捗や自動車生産サイクルに左右されますが、生産回帰と持続可能性への取り組みを背景に引き続き好調を維持する見込みです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 電子商取引の急成長により、安全で高速な包装用接着剤の需要が拡大しております

- 世界の建設景気の好転により、構造用・床用接着剤の消費量が増加しております

- 軽量化とEVプラットフォームが自動車用接着剤の普及を加速

- AIを活用した配合最適化により、研究開発期間とカスタム接着コストが大幅に削減されています

- 2025年以降の米国関税後のアクリルモノマー供給のニアショアリングが地域生産能力を再構築

- 市場抑制要因

- 石油原料価格の変動が接着剤メーカーの利益率を圧迫

- 揮発性有機化合物(VOC)及び化学物質規制の強化が溶剤系接着剤の販売を抑制

- 上級接着剤調合技術者の世界の不足により、商品化サイクルが遅延しております

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 樹脂別

- ポリウレタン

- エポキシ樹脂

- アクリル

- シアノアクリレート

- VAE/EVA

- シリコーン

- その他の樹脂

- 技術別

- 水系

- 溶剤系

- 反応性

- ホットメルト

- UV硬化型接着剤

- エンドユーザー業界別

- 建築・建設

- 包装

- 自動車

- 航空宇宙産業

- 木工および建具

- 履物・皮革製品

- ヘルスケア

- その他のエンドユーザー産業

- 地域別

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- インドネシア

- マレーシア

- シンガポール

- タイ

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/順位分析

- 企業プロファイル

- 3M

- Aica Kogyo Co..Ltd.

- Arkema

- AVERY DENNISON CORPORATION

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- Illinois Tool Works Inc.

- Jowat SE

- MAPEI S.p.A.

- NANPAO RESINS CHEMICAL GROUP

- Pidilite Industries Ltd.

- Sika AG

- Soudal Holding N.V.

- Wacker Chemie AG