|

市場調査レポート

商品コード

1692504

米国の超音波装置:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)United States Ultrasound Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国の超音波装置:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 95 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

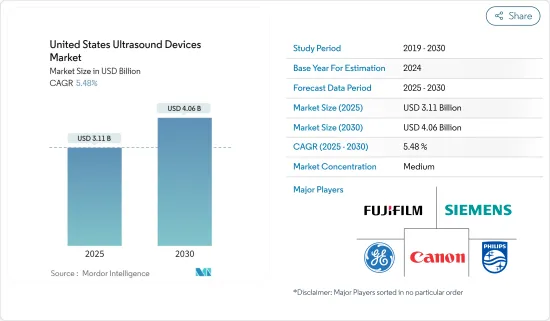

米国の超音波装置市場規模は、2025年に31億1,000万米ドルと推定され、予測期間(2025年~2030年)のCAGRは5.48%で、2030年には40億6,000万米ドルに達すると予測されています。

COVID-19は、パンデミックによって患者が超音波画像診断のような救命のための画像処置を待つことを余儀なくされ、患者のヘルスケア施設へのアクセスに影響を与えています。パンデミックは、患者が画像診断を受けるまでの待ち時間を増加させました。北米放射線学会(Radiology Society of North America)が2021年4月に発表した論文「The Economic Impact of the COVID-19 Pandemic on Radiology Practices」によると、パンデミックは全米の放射線診療所に多大な影響を与えました。病気のトランスミッションを遅らせるために採用された政策措置は、COVID-19とは無関係に画像診断の需要を減少させています。病院は危機的状況を拡大する準備を進めており、安全に実施できる適切な医療用画像の量はさらに減少しています。さらに、2020年5月にJournal of the American College of Radiologyに掲載されたJason J. Naidichの論文「Impact of the COVID-19,Pandemic on Imaging Case Volumes」によると、2020年上半期の総撮影件数は2019年から12.29%減少しました。COVID-19後の画像診断件数は、すべての患者診療部位とモダリティの種類で28.10%減少しました。これは、撮像技術が市場台数の減少をもたらしたことを示しています。記事はまた、モダリティタイプによって画像診断出来高の減少が異なり、マンモグラフィが第16週までに最も高い減少率(94%)を示し、核医学(85%)、MRI(74%)、超音波(64%)、インターベンショナルラジオロジー(56%)、CT(46%)、X線(22%)と続いた。しかし、放射線科クリニックはCOVID-19の流行による画像診断症例数への影響を緩和し、2021年に回復計画を策定しました。したがって、COVID-19は米国で調査された市場に大きな影響を与えたことが観察されます。

市場の成長に影響を与える主な要因は、慢性疾患の増加、技術の進歩、超音波の用途の拡大です。

さらに、この分野における新たな研究開発やイノベーション、主な市場参入企業による新製品の発売、米国食品医薬品局からの新たな承認と相まって、超音波市場は本調査の予測期間中にさらに成長すると予想されます。例えば、2021年10月、北米Mindray社は、ポイントオブケア(POC)市場における超音波の可能性を最大化する新製品、TE7 Max超音波システムを発売しました。この新製品は、他の追随を許さない21.5インチの縦型高精細LEDディスプレイと、臨床医が見ることができるものを真に最大化するための密封されたタッチベースのインターフェースを備えています。

したがって、上記のような要因から、この市場は予測期間中に健全な成長を遂げることが期待されます。

米国の超音波装置市場の動向

麻酔科が急成長を遂げる見込み

麻酔学は、手術前、手術中、手術後の患者の総合的な周術期ケアに関わる医療専門分野と呼ばれています。麻酔学には、麻酔、集中治療医学、重症救急医学、疼痛医学が含まれます。麻酔学には、周術期を通じて患者の生命機能を安全にサポートするための麻酔の研究と使用が含まれます。

同分野の成長を促進する主な要因は、革新的な製品の発売、技術の進歩、超音波装置の採用拡大です。

例えば、GE社は2021年3月に新しいワイヤレス携帯型超音波診断装置Vscan Airを発売しました。この装置は、局所麻酔やその他の手技のガイダンスに必要な手技ガイダンスを提供します。このような開発により、米国では麻酔科用途への超音波装置の導入が促進され、市場開拓が進むと予想されます。

さらに、2021年1月、コニカミノルタヘルスケアアメリカズ社は、Medovate Ltd.との間で、Medovate社の局所麻酔注射ソリューションSAFIRAとコニカミノルタの超音波ガイド下手技用ソリューションシリーズを米国で共同販売する契約を締結したと発表しました。この取り組みは、コニカミノルタのUGProソリューションに新たに加わったもので、教育、手技、小型超音波診断装置SONIMAGE HS2などの画像診断機器を組み合わせることで、局所麻酔のさらなる普及と患者の安全性向上を目指します。このような開発により、国内での麻酔科用途での超音波装置の使用拡大がさらに期待されます。

したがって、超音波に関する上記の開発は、今後数年間の市場成長を促進すると予想されます。

米国の超音波装置産業の概要

市場は少数の大手企業に集中しています。超音波画像診断がヘルスケアの基本になりつつあることから、公開会社や非公開会社が研究開発に投資し、技術の向上に努めています。最新技術を駆使したポータブル機器は世界的に高く評価されており、各社は先進国市場と新興国市場に幅広く進出しています。超音波診断装置に投資している主な企業には、フィリップス、シーメンス、キヤノン、富士フイルムなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 技術の進歩

- 慢性疾患の増加

- 市場抑制要因

- 厳しい規制

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 用途別

- 麻酔科

- 循環器科

- 婦人科/産科

- 筋骨格系

- 放射線学

- クリティカルケア

- その他の用途

- 技術別

- 2D超音波イメージング

- 3Dおよび4D超音波イメージング

- ドップラーイメージング

- 高密度焦点式超音波

- タイプ別

- 据置型超音波

- ポータブル超音波

第6章 競合情勢

- 企業プロファイル

- Canon Medical Systems Corporation

- Fujifilm Holdings Corporation

- GE Healthcare

- Koninklijke Philips NV

- Siemens Healthineers

- Carestream Health Inc.

- Samsung Electronics Co. Ltd

- Hologic Inc.

- Mindray Medical International Limited

- Esaote SpA

第7章 市場機会と今後の動向

The United States Ultrasound Devices Market size is estimated at USD 3.11 billion in 2025, and is expected to reach USD 4.06 billion by 2030, at a CAGR of 5.48% during the forecast period (2025-2030).

COVID-19 has impacted the patient's access to healthcare facilities as the pandemic has forced the patients to wait for life-saving imaging procedures such as ultrasound imaging. The pandemic has increased the waiting time for patients to have their imaging done. According to an article published by the Radiology Society of North America in April 2021, titled,' The Economic Impact of the COVID-19 Pandemic on Radiology Practices', The pandemic had a profound impact on radiology practices across the country. Policy measures adopted to slow the transmission of disease are decreasing the demand for imaging independent of COVID-19. Hospital preparations to expand crisis capacity are further diminishing the amount of appropriate medical imaging that can be safely performed. Furthermore, according to Jason J. Naidich's article titled 'Impact of the COVID-19,) Pandemic on Imaging Case Volumes,' published in the Journal of the American College of Radiology in May 2020, the total imaging volume in the first half of 2020 was down 12.29% from 2019. Imaging volumes decreased by 28.10% across all patient care sites and modality types after COVID-19. This indicates that imaging techniques resulted in a decline in market volumes. The article also noted that the imaging volume decline differed by modality type, with mammography showing the highest reduction (94%) by week 16, followed by nuclear medicine (85%), MRI (74%), ultrasound (64%), interventional radiology (56%), CT (46%), and x-ray (22%). However, the radiology clinics mitigated the impact of the COVID-19 epidemic on imaging case volumes and established recovery plans in 2021. Therefore, it is observed that COVID-19 significantly impacted the market studied in the United States.

The major factors affecting the growth of the market are the increasing incidences of chronic diseases, increasing technological advancements, and the growing applications of ultrasound.

Furthermore, with the new research and developments and innovations in the area, coupled with the launch of new products by the key market players and new approvals from the United States Food and Drug Administration, the ultrasound market is further expected to grow over the forecast period of the study. For instance, in October 2021, Mindray North America launched a new product that is maximizing the potential of ultrasound in the Point of Care (POC) market: the TE7 Max Ultrasound System. This new product has an unrivaled 21.5-inch vertically oriented high-definition LED display and a sealed touch-based interface to truly maximize what clinicians can see.

Therefore, owing to the above-mentioned factors, it is expected that the market studied will witness healthy growth over the forecast period.

US Ultrasound Devices Market Trends

Anesthesiology is Expected to Witness Rapid Growth

Anesthesiology is referred to as a medical specialty concerned with the total perioperative care of the patients before, during, and after surgery. It includes anesthesia, intensive care medicine, critical emergency medicine, and pain medicine. Anesthesiology includes the study and use of anesthesia to safely support a patient's vital functions through the perioperative period.

The major factors fueling the growth of the segment are innovative product launches, technological advancements, and the growing adoption of ultrasound devices.

For instance, in March 2021 General Electric launched its new wireless, hand-held ultrasound device, Vscan Air, as the company seeks to capture a leading position in the growing market in the United States and some other countries. The device provides the procedure guidance needed to deliver regional anesthesia and guidance for other procedures. Such developments are expected to boost the adoption of ultrasound devices for anesthesiology applications in the United States, thereby supporting the market growth.

Moreover, in January 2021, Konica Minolta Healthcare Americas, Inc. announced an agreement with Medovate Ltd. to jointly promote Medovate's SAFIRA regional anesthesia injection solution with Konica Minolta's range of solutions for ultrasound-guided procedures in the United States. This initiative is the latest addition to Konica Minolta's UGPro Solution, which brings together education, procedures, and imaging equipment, such as the SONIMAGE HS2 Compact Ultrasound System, to further expand the use of regional anesthesia and enhance patient safety. Such developments are further expected to expand the usage of ultrasound devices for anesthesiology applications in the country.

Hence, the above developments about ultrasound is expected to drive the market growth in the coming years.

US Ultrasound Devices Industry Overview

The market is concentrated with a few large players. Public and private companies are found investing in R&D to advance their technologies in the field of ultrasound imaging, as it is becoming one of the fundamental aspects of healthcare. The updated technological portable devices are praised globally, and the companies have a wide presence across the developed and emerging markets. Some of the major companies investing in ultrasound devices are Philips, Siemens, Canon, and Fujifilm.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Technological Advancements

- 4.2.2 Increasing Incidences of Chronic Diseases

- 4.3 Market Restraints

- 4.3.1 Strict Regulations

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Application

- 5.1.1 Anesthesiology

- 5.1.2 Cardiology

- 5.1.3 Gynecology/Obstetrics

- 5.1.4 Musculoskeletal

- 5.1.5 Radiology

- 5.1.6 Critical Care

- 5.1.7 Other Applications

- 5.2 By Technology

- 5.2.1 2D Ultrasound Imaging

- 5.2.2 3D and 4D Ultrasound Imaging

- 5.2.3 Doppler Imaging

- 5.2.4 High-intensity Focused Ultrasound

- 5.3 By Type

- 5.3.1 Stationary Ultrasound

- 5.3.2 Portable Ultrasound

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Canon Medical Systems Corporation

- 6.1.2 Fujifilm Holdings Corporation

- 6.1.3 GE Healthcare

- 6.1.4 Koninklijke Philips NV

- 6.1.5 Siemens Healthineers

- 6.1.6 Carestream Health Inc.

- 6.1.7 Samsung Electronics Co. Ltd

- 6.1.8 Hologic Inc.

- 6.1.9 Mindray Medical International Limited

- 6.1.10 Esaote SpA