|

市場調査レポート

商品コード

1690857

口腔内スキャナー:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Intraoral Scanners - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 口腔内スキャナー:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 115 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

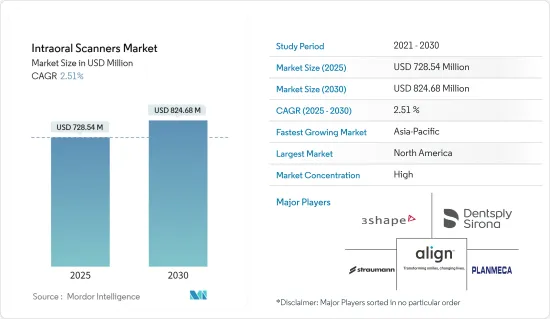

口腔内スキャナー市場規模は、2025年に7億2,854万米ドルと推定され、予測期間(2025-2030年)のCAGRは2.51%で、2030年には8億2,468万米ドルに達すると予測されています。

COVID-19の大流行は、口腔内スキャナー市場の成長転換に大きく貢献しました。当初、COVID-19の大流行は口腔内スキャナー市場に大きな影響を及ぼしたが、これは世界の社会的距離と政府による封鎖措置により、患者の歯科クリニックや病院への来院が大幅に減少したためです。パンデミックの初期段階において、米国歯科医師会(ADA)は歯科の緊急および非緊急治療に関する推奨事項を発表しました。急性の痛み、感染、外傷を伴う状態を除けば、症状のない歯の抜歯、無症状のむし歯病変の治療や審美歯科処置を含む修復歯科は、米国歯科医師会(ADA)によってすべて非緊急治療とみなされました。

しかし、COVID-19のパンデミックでは、歯の破折、歯科治療のセメント充填、歯根膜炎などが緊急歯科処置とされました。したがって、COVID-19パンデミックは調査した市場に大きな影響を与えたことが観察されました。しかし現在、口腔内スキャナーの需要という点では、市場はパンデミック以前に達しています。

さらに、口腔内スキャナー市場の成長をもたらす重要な要因には、老人人口の増加、歯科疾患の増加、技術の進歩などがあります。例えば、不健康な食事や口腔ケア不足によるう蝕の有病率の高さは、様々な国の人々の間で、市場の成長を促進する重要な要因となっています。例えば、2022年に英国で行われた5歳児を対象とした全国歯科疫学プログラムの調査によると、エナメル質および歯質の虫歯を持つ子どもの全国有病率は29.3%でした。同じ情報源によると、地域別では、イングランド南西部の23.3%から北西部の38.7%に及んでいます。歯科機器市場における口腔内スキャナーの導入は、歯科診療の状況を近代化しました。口腔内スキャナーの導入により、歯型採取の制約がなくなり、歯科医が瞬時にデータを転送・操作できるようになりました。したがって、このような機能は、ヘルスケア施設全体で口腔内スキャナーの採用を増加させ、それによって市場の成長に貢献する可能性が高いです。

高齢者人口の増加は市場成長を促進すると予想されます。高齢者人口は、加齢に関連した唾液の変化、粗食の摂取、歯肉退縮による歯根への露出のため、歯科疾患を開発しやすいからです。例えば、世界経済フォーラムが2023年9月に発表した報告書によると、日本では2023年に10人に1人以上が80歳以上となります。また、国立社会保障・人口問題研究所は、2040年には65歳以上の高齢者が総人口の34.8%を占めると予測しています。したがって、高齢者人口と歯の喪失やその他の歯科関連疾患の発生率の増加との間には正の相関関係があり、市場の成長にプラスの影響を与えると予想されます。

このように、高齢者人口の増加に起因する歯科疾患有病率の上昇、製品の上市、予測期間中の承認などの要因は、市場の成長を促進する可能性が高いです。しかし、インドや中国などの新興経済諸国では熟練した専門家が不足しており、口腔内スキャナーのコストが高いことが市場成長を抑制する可能性があります。

口腔内スキャナー市場動向

スタンドアロン型デバイスセグメントは今後数年で力強い成長が見込まれる

スタンドアロン型デバイスは、口腔スキャン手順における歯科専門家のワークフロー改善と、これらのデバイスの出力向上により、有望な成長が見込まれます。さらに、小型ポータブル口腔内スキャナーの市場導入により、小型口腔内スキャナーに側面指向チップを組み込むことで、頬側表面のスキャンがより利用しやすく、迅速かつ効果的になりました。このように、これらの機器によって提供される強化された出力は、このセグメントの成長を促進すると予想されます。

口腔疾患は生涯を通じて人々に影響を与え、痛み、苦しみ、醜状、時には死をもたらします。口腔疾患は、多くの国々にとって大きな健康上の負担となっています。例えば、2022年4月にNational Institute of Dental and Craniofacial Researchが発表したデータによると、米国では毎年、20歳から64歳の成人の約90%が虫歯に罹患し、45歳から64歳の成人の約50%が歯周病に罹患していることが確認されています。このように、歯科疾患の増加は、効果的な疾患検出のための口腔内スキャナーの需要を押し上げる可能性が高いです。

さらに、口腔内スキャナーは、チェアサイドでの作業時間を短縮し、最終的な修復物の精度を向上させることができるため、歯科印象市場でも人気が高まっています。従来の印象材は依然として広く使用されていますが、口腔内スキャナーの採用はデジタル歯科医療への大きなシフトを意味し、精度、患者の快適性、歯科医療全体の質を向上させます。技術の進歩に伴い、口腔内スキャナーの役割はさらに拡大し、歯科における印象の将来的な展望に影響を与える可能性が高いです。例えば、2022年9月、3ShapeはTRIOS 5と呼ばれるワイヤレス口腔内スキャナーを発売しました。TRIOS 5はScanAssistインテリジェントアライメント技術を搭載し、最高の画像性能と感染管理基準を実現します。同社によると、TRIOS 5 Wirelessは、FDA認可のオートクレーブ可能な密閉型スキャナチップを採用し、傷のないサファイアガラスで保護されているため、新しい衛生レベルが実現されています。

したがって、スキャナーに関連するメリット、スキャナー需要の高まり、改良型スキャナーの開発・販売に注力する大手企業の増加により、調査対象サブセグメントは予測期間中に増加すると予想されます。

予測期間中、北米が大きな市場シェアを占める見込み

北米は予測期間中に大きな成長を記録する見込みです。口腔障害に罹患しやすい老年人口の増加、歯の問題に悩む患者の増加、先進的なヘルスケアインフラが市場成長を促進する主な要因です。

老年人口における虫歯の増加は、いくつかの理由から米国における口腔内スキャナーの需要を促進する可能性があります。第一に、高齢化が進むにつれて、虫歯や歯の喪失など口腔の健康問題が発生する可能性が高くなり、歯科治療が必要となります。例えば、米国国立衛生研究所(NIH)が2022年4月に発表した最新情報によると、米国では20歳から64歳の成人10人のうち約9人が過去2年間に虫歯を経験しています。同様に、国連人口基金が発表した2022年の統計によると、カナダでは2022年に人口の約19%が65歳以上となります。このように、高齢化社会の進展は歯科疾患の負担を増加させると予想され、市場の成長に寄与する可能性が高いです。したがって、高齢化社会における虫歯の増加は、この疾患を検出するための口腔内スキャナーの需要を増加させ、予測期間中の市場成長に貢献すると予想されます。

さらに、米国のヘルスケアシステムが発展し、歯の問題がよりよく知られるようになるにつれて、より多くの人々が歯科医や病院を訪れるようになると予想され、この地域の口腔内スキャナー市場の拡大をサポートします。例えば、2022年10月、米国糖尿病協会(ADA)はパシフィックデンタルサービス(PDS)との共同口腔保健キャンペーンを発表しました。このキャンペーンは、歯周病(歯周病)に対する認識を高め、この慢性的な健康状態を予防・管理するために、口腔保健プロバイダーがどのように患者を支援できるかを目指すものです。従って、このような取り組みは、国内における歯の健康に対する意識を高め、歯科受診者数を増加させ、最終的に市場成長に寄与する可能性が高いです。

さらに、歯科治療に対する有利な償還政策も市場の成長に寄与すると予想されます。例えば、カナダ政府は2022年9月、カナダの低所得世帯(年間世帯収入9万米ドル未満)に対し、12歳未満の子供1人につき260~650米ドルの保険金を支給する当面の措置である「カナダ歯科給付金」を導入しました。この給付は、2022年10月1日から遡及して歯科医療費をカバーするもので、2回の報告期間のみ利用できます。

技術の進歩により、同国の主要な市場関係者は新しく先進的なスキャナーを発売しており、この地域の調査市場の成長にも大きな影響を与えると予想されます。例えば、2023年4月、Ori Dental社は、従来の歯科用ポリビニルシロキサン(PVS)印象に代わる近代的なものとして、Ori口腔内スキャナーを発売しました。この口腔内歯科用スキャナーは、従来のPVS歯科用印象よりも速く、軽く、正確で、安価に作られています。

そのため、歯科疾患にかかりやすい高齢者人口の増加、政府の支援イニシアティブ、および償還金が、この地域における口腔内スキャナー市場の成長を促進すると予想されています。

口腔内スキャナー産業概要

口腔内スキャナー市場は競争が激しく、複数の大手企業が参入しています。市場シェアでは、少数の大手企業が市場を独占しています。現在市場を独占している企業には、3 Shape AS、Align Technology Inc.、Dentsply Sirona Inc.、PLANMECA OYなどがあります。さらに、各社は市場拡大のため、買収、提携、協力、新製品の発売など、さまざまな戦略的手段を採用しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 急速な技術進歩

- 高齢人口の増加

- 歯科疾患の増加

- 市場抑制要因

- 熟練した専門家の不足

- 口腔内スキャナーの高コスト

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- モダリティ

- スタンドアロン型

- ポータブル

- エンドユーザー

- 歯科医院

- 病院

- その他のエンドユーザー

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Medit Corp.

- 3Shape A/S

- Align Technology Inc.

- BLZ Dental

- Condor Technologies NV

- Densys Ltd

- Institut Straumann AG

- Dentsply Sirona Inc.

- Guangdong Launca Medical Device Technology Co. Ltd.

- Planmeca Oy

第7章 市場機会と今後の動向

The Intraoral Scanners Market size is estimated at USD 728.54 million in 2025, and is expected to reach USD 824.68 million by 2030, at a CAGR of 2.51% during the forecast period (2025-2030).

The COVID-19 pandemic contributed largely to transforming the growth of intraoral scanners markets. Initially, the outbreak of COVID-19 showed a substantial effect on the intraoral scanner market because patients' visits to dental clinics and hospitals were significantly reduced due to the global social distancing and lockdown measures taken by governments. During the initial phase of the pandemic, the American Dental Association (ADA) published recommendations for dental emergency and non-emergency care. Apart from conditions involving acute pain, infection, or trauma, the removal of teeth not showing any symptoms, and restorative dentistry, which includes the treatment of asymptomatic carious lesions and cosmetic dental procedures, all were considered non-emergencies by the American Dental Association (ADA).

However, during the COVID-19 pandemic, tooth fractures, dental treatment cementation, pericoronitis, etc., were identified as emergency dental procedures. Hence, it was observed that the COVID-19 pandemic had a significant impact on the market studied. However, currently, the market has reached pre-pandemic in terms of demand for the intraoral scanner.

Additionally, the significant factors responsible for the growth of the intraoral scanner market include an increase in the geriatric population, a rise in dental disorders, and technological advancements. For instance, the high prevalence of dental caries due to unhealthy eating and lack of oral care among populations in various countries is the key factor driving the market's growth. For instance, as per the National Dental Epidemiology Program survey of 5-year-old children in England in 2022, the national prevalence of children with enamel and dentinal decay was 29.3%. As per the same source, regionally, this ranged from 23.3% in the Southwest to 38.7% in Northwest England. The introduction of intraoral scanners in the dental devices market has modernized the dental practice landscape. These have eliminated the limitations of taking tooth impressions and helped dentists instantly transfer and manipulate data. Thus, such features are likely to increase the adoption of intraoral scanners across healthcare facilities, thereby contributing to market growth.

The increasing geriatric population is expected to facilitate market growth as the elderly population is prone to developing dental disorders because of salivary changes related to aging, consumption of a poor diet, and exposure to dental roots due to gingival recession. For instance, according to the report published by the World Economic Forum in September 2023, more than 1 in 10 people in Japan are aged 80 or over in 2023. In addition, the National Institute of Population and Social Security Research projected that those aged 65 or older will account for 34.8% of the total population in 2040. Thus a positive correlation between the senior population and an increase in incidences of tooth loss and other dental-related disorders is expected to positively impact the market growth.

Thus, factors such as rising dental disease prevalence owing to the rising geriatric population, product launches, and approvals over the forecast period are likely to facilitate market growth. However, the lack of skilled professionals in developing economies such as India and China and the high cost of intraoral scanners may restrain market growth.

Intraoral Scanners Market Trends

Standalone Devices Segment is Expected to Witness Strong Growth in The Coming Years

Standalone devices are expected to witness promising growth due to the improved workflow of dental professionals in oral scanning procedures and improved outputs of these devices. Furthermore, due to the introduction of miniature portable intraoral scanners in the market, incorporating the side-oriented tip in small intraoral scanners has made buccal surface scans much more accessible, quicker, and more effective. Thus, the enhanced output offered by these devices is expected to fuel the segment's growth.

Oral illnesses affect people throughout their lives, causing pain, suffering, disfigurement, and sometimes death. They are a significant health burden for many nations. For instance, according to the data published by the National Institute of Dental and Craniofacial Research in April 2022, it has been observed that tooth decay affects about 90% of adults aged 20 to 64 years, and gum diseases affect almost 50% of adults aged 45 to 64 years, annually, in the United States. Thus, the rising dental diseases are likely to boost the demand for intraoral scanners for effective disease detection.

Furthermore, intraoral scanners have become increasingly popular in the dental impression market due to their ability to reduce chairside time and improve the accuracy of final restorations. While traditional impression materials are still widely used, the adoption of intraoral scanners represents a significant shift toward digital dentistry, offering precision, patient comfort, and the overall quality of dental care. As technology continues to advance, the role of intraoral scanners is likely to expand further, influencing the future landscape of dental impressions in dentistry. For instance, in September 2022, 3Shape launched a wireless intraoral scanner called TRIOS 5, which features ScanAssist intelligent alignment technology that delivers the highest imaging performance and infection control standard. According to the company, TRIOS 5 Wireless features an FDA-cleared, closed autoclavable scanner tip protected by scratch-free sapphire glass to define a new level of hygiene and includes ultra-thin, snug, and near-invisible single-use sleeves to cover the scanner body and minimize the risk for cross-contamination.

Therefore, the studied sub-segment is anticipated to rise over the forecast period due to the benefits associated with scanners, the rising demand for scanners, and the growing focus by significant players on developing and marketing improved scanners.

North America is Expected to Hold a Significant Market Share During the Forecast Period

North America is expected to register significant growth over the forecast period. A rise in the geriatric population susceptible to oral disorders, an increasing number of patients suffering from dental problems, and advanced healthcare infrastructure are the key factors propelling the market growth.

The increasing tooth decay in the geriatric population can drive the demand for intraoral scanners in the United States for several reasons. Firstly, as the aging population grows, there is a higher likelihood of oral health issues, including tooth decay and loss, necessitating dental interventions. For instance, as per the April 2022 update by the National Institutes of Health (NIH), about 9 out of 10 adults aged 20 to 64 experienced tooth decay in the United States over the past 2 years. Similarly, according to the 2022 statistics published by the United Nations Population Fund, in Canada, about 19% of the population is aged 65 years and above in 2022. Thus, the growing aging population is expected to increase the burden of dental diseases and is likely to contribute to market growth. Thus, growing tooth decay in the aging population is expected to increase the demand for intraoral scanners to detect the disease and contribute to market growth over the forecast period.

Additionally, as the United States healthcare system develops and dental problems become more well-known, more people are anticipated to visit dentists and hospitals, which will support the expansion of the intraoral scanner market in the region. For instance, in October 2022, the American Diabetes Association (ADA) announced a collaborative Oral Health campaign with Pacific Dental Services (PDS). The campaign aims to increase awareness of periodontal disease (gum disease) and how oral health providers can assist patients in preventing and managing this chronic health condition. Thus, such initiatives are likely to increase awareness about dental health in the country, which is likely to augment the number of dental visits and ultimately contribute to the market growth.

Moreover, favorable reimbursement policies for dental procedures are expected to contribute to the market's growth. For instance, in September 2022. the government of Canada introduced the Canadian Dental Benefit, an immediate measure to provide low-income families (under USD 90,000 annual family income) in Canada with USD 260 - USD 650 of coverage per child under 12 years. This benefit is retroactive to cover dental expenses from October 1, 2022, and is only available for two reporting periods.

Due to technological advancements, the key market players in the country are launching new and advanced scanners, which are also expected to have a significant impact on the growth of the studied market in the region. For instance, in April 2023, Ori Dental launched the Ori Intraoral Scanner as a modern alternative to traditional dental Polyvinyl Siloxane (PVS) impressions. This intraoral dental scanner is made to be faster, lighter, more accurate, and less expensive than traditional PVS dental impressions.

Therefore, the rising geriatric population, which is more prone to dental diseases, government support initiatives, and reimbursements are anticipated to fuel the intraoral scanners market growth in the region.

Intraoral Scanners Industry Overview

The intraoral scanner market is competitive and consists of several major players. In terms of market share, a few major players dominate the market. Some companies currently dominating the market are 3 Shape AS, Align Technology Inc., Dentsply Sirona Inc., and PLANMECA OY. Furthermore, the companies adopt various strategic measures such as acquisitions, partnerships, collaborations, and new product launches to expand in the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Technological Advancements

- 4.2.2 Increase in Geriatric Population

- 4.2.3 Rise in Dental Disorders

- 4.3 Market Restraints

- 4.3.1 Lack of Skilled Professionals

- 4.3.2 High Cost of Intraoral Scanners

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Modality

- 5.1.1 Standalone

- 5.1.2 Portable

- 5.2 End User

- 5.2.1 Dental Clinics

- 5.2.2 Hospitals

- 5.2.3 Other End Users

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Medit Corp.

- 6.1.2 3Shape A/S

- 6.1.3 Align Technology Inc.

- 6.1.4 BLZ Dental

- 6.1.5 Condor Technologies NV

- 6.1.6 Densys Ltd

- 6.1.7 Institut Straumann AG

- 6.1.8 Dentsply Sirona Inc.

- 6.1.9 Guangdong Launca Medical Device Technology Co. Ltd.

- 6.1.10 Planmeca Oy