鉱業におけるコンベヤベルト:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Conveyor Belt In Mining Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 111 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690805

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

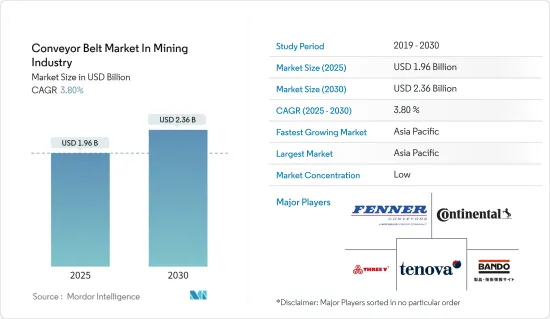

鉱業におけるコンベヤベルト市場は、2025年の19億6,000万米ドルから2030年には23億6,000万米ドルに成長し、予測期間(2025-2030年)のCAGRは3.8%になると予想されます。

インドなどでは、政府の取り組みや炭鉱の数が増加しているため、需要が高まっています。例えば、第2次パンデミックの波において、Coal Indiaが発表したTechnology Roadmap文書によると、Coal Indiaでは毎時4,500 tphまでの石炭を扱えるコンベヤが計画されています。従来のコンベヤは傾斜角度が16~18度程度に制限されています。先進的なコンベヤベルトによる鉱山のアップグレードに注力していることが、市場の成長を後押ししています。

主なハイライト

- 鉱業の実務では、必要な出力が求められ、採掘業者は回転速度を設計パラメータとして指定し、放散する熱を決定します。これは、寸法決定プロセスに強く影響する可能性があります。その結果、本来必要な出力よりも大きなギヤユニットを使用することが望ましい運転条件となります。コンベアベルトが異常に暖かい気候帯で使用される場合、あるいは極端な熱寒暖差が発生しやすい気候帯で使用される場合、冷却に多くの注意を払わなければなりません。このため、シーメンスは、46サイズのコンベアベルトドライブからなる3つのギアユニットシリーズに対応する効率的な冷却ソリューションを開発しました。そのため、様々なケースにおいて、より小型のギアユニットで十分な場合もあります。

- 2047年までに先進国になるためのインドの旅は、インフラの改善にかかっています。これは、経済成長の原動力となる、住みやすく、気候変動に強く、包括的な都市を育成するための礎石です。2024会計年度にGDPの3.3%をインフラ部門に割り当て、ハイエンドの産業分野の建設に重点を置いていることからも、政府のコミットメントがうかがえます。

- 労働安全衛生の確保は、鉱業における最優先事項です。採掘作業は本質的に困難であり、労働者にさまざまな危険やリスクをもたらします。安全を優先し、効果的な安全対策を実施することで、企業は労働者を保護し、事故や負傷を防ぎ、事業全体の持続可能性に貢献することができます。

- 鉱業は、安全、環境保護、責任ある慣行を確保するために、重要な規制や基準の下で運営されています。これには、米国の鉱山安全衛生管理局(MSHA)などの鉱山安全衛生規制が含まれます。

- 初期コストが高いことが、コンベアベルトやシステムを含む自動マテリアルハンドリングシステムの使用を大規模な組織のみに制限してきた主な理由です。同時に、長期的なメリットも考慮されています。中小規模の企業は、このバーゲンから利益を得られないかもしれないです。これらのシステムは高レベルのメンテナンスを必要とします。

- 世界のパンデミックは、さまざまな市場に直接的な影響を与えるだけでなく、長期的な影響も与えると予想されます。例えば、パンデミック以来、大きな影響を感じている複数の国々の経済は、いまだに予想通りに回復することができず、特に北米と欧州地域に景気後退の影をもたらしています。

- たとえば、国際通貨基金(IMF)の試算によると、米国の実質GDP成長率は、勢いを取り戻すまで2024年まで鈍化すると予想されています。このような動向は、新規の金属・鉱業プラントへの投資を減少させ、市場を鈍化させる可能性があります。

- 国際通貨基金(IMF)の2023年7月の更新によると、世界経済成長率は2022年の3.5%から2023年と2024年の両方で約3%に低下すると予想され、これはインフレと戦うために中央銀行の政策金利が上昇し、経済活動が鈍化しているためです。

鉱業用コンベヤベルトの市場動向

テキスタイル補強コンベヤベルトが著しい成長を遂げる

- テキスタイル補強コンベヤベルトは、一般的に研磨材や重量物に使用されます。テキスタイル補強コンベヤベルトは、スチールコード・ベルトよりも輸送距離が短く、容量も小さいため、手頃な価格で入手できます。テキスタイル補強コンベヤベルトは、採鉱、鉱物処理、採石部門に理想的です。耐グリース性、耐熱性、耐摩耗性、耐衝撃性、耐火性など、さまざまな品質があります。高強度ベルトを補強するための基本的な構造には、コード織物、直線経糸織物、ソリッド織物、ケーブルコードの4種類があります。

- ファブリックベルトのカーカスまたは織物の内部構造は、ゴムベースの衝撃吸収層の間に挟まれた単層または多層の一連の合成繊維層で構成されています。ベルトの上側と下側は、耐久性、耐摩耗性、耐切創性に優れたゴム製カバーで構成されています。このカバーは、特にコンベヤのローディングポイントでの損傷からベルトを保護します。これは、鉱業で使用されるコンベヤベルトに引張強度を提供します。

- 技術用織物に使用される合成繊維の強度、伸長性、柔軟性は、以前に使用されていた天然繊維よりも高いです。主な繊維は、綿、ビスコースレーヨン、ナイロン、ポリエステル、ガラス、アラミドです。アラミドの粘り強さはスチールの7倍で、アラミドはスチールより軽いです。400~500℃の温度、湿気、化学薬品に強く、耐摩耗性も高いです。そのため、鉱業用コンベヤーベルトに使用されています。その強度は、鉱業におけるコンベヤベルトの搬送能力と作業の安全性に大きく影響します。したがって、テキスタイル補強コンベヤベルトのような素材は、コンベヤベルトの強度を高めるために、より普及すると予想されます。

- ベルトメーカーは、ベルト上で搬送されるさまざまな種類と等級の材料に基づいて、ベルトに提案されるプライの数を反映した織物ベルトの表を供給しています。織物は、コンベヤベルトのスチール補強材よりもはるかに柔軟で、高強度、エネルギー効率、耐腐食性、軽量であるため優れています。

- いくつかの地域で鉱業活動が活発化し、鉱業への投資が増加していることから、テキスタイル補強コンベヤベルトのニーズは予測期間中に高まると予想されます。

アジア太平洋地域が大きな成長を記録

- 政府の野心的な「メイド・イン・チャイナ2025」イニシアチブは、部分的にドイツに触発されたもので、インダストリー4.0に向けたものであり、工業分野における中国の競争力を高めることを目的としています。2015年5月に導入されたこの10カ年計画は、世界の産業バリューチェーンの中ハイエンドに産業をシフトさせ、いくつかの先進的な製造業クラスターを育成するための政府の入札です。工業化の進展は、鉱業セクター向けのコンベヤベルト・ソリューション市場を成長させると思われます。

- 2024年4月、国家開発改革委員会によると、中国は国内供給の増加と価格上昇の抑制を推進するため、より多くの炭鉱を建設すると発表しました。世界最大の石炭生産・消費国である中国は、2030年までに「緊急備蓄用」として年間約3億トンの採掘能力を追加する目標を設定しました。

- 政府のインフラ投資と産業界からの投資の増加は、「メイク・イン・インディア」イニシアティブと相まって、市場の研究を促進すると予想されます。インド政府は、国内総生産(GDP)に占める産業部門の割合を2018年の17%から2022年までに25%に引き上げました。

- 2024年2月、インドの国営企業コール・インディアは、化石燃料の需要増に対応するため、新たに5つの炭鉱で操業を開始し、少なくとも16の既存炭鉱の生産能力を拡大すると発表しました。同炭鉱は、来年度中に新たに5つの炭鉱で操業を開始する予定で、その合計年間生産能力は1,430万トンです。インドの鉱業セクターにおけるこうした開発は、この地域での市場調査を推進すると思われます。

鉱業用コンベヤベルト産業の概要

鉱業用コンベヤベルト市場は、中小企業や世界企業が存在するため、非常に断片化されています。市場の主要企業には、Sanwei Holding Group、Fenner Dunlop Australia Pty Ltd(ミシュラン・グループ)、Bando Chemical Industries Ltd、Contitech Deutschland GMBH(continental AG)、Tenova SPA(Techint Group)などがあります。市場のプレーヤーは、製品ラインナップを強化し、持続可能な競争優位性を獲得するために、買収やパートナーシップなどの戦略を採用しています。

- 2024年1月-Fenner Dunlop BVとFenner Dunlop Americasは、2024年1月1日よりFenner Dunlop Conveyor Beltingブランドに統合すると発表しました。この動きは、より強固な世界プレゼンスに向けて、地域や部門を越えてブランドを統一することを目的としています。両事業部はフェナー・ダンロップ・コンベヤベルトの名称で取引を行い、一貫したブランディングのための戦略を一致させる。この変更は、フェナー・グループの連携強化と市場への影響力強化へのコミットメントを強調するものです。

- 2023年11月-Gebr.Kufferath AGはDurensiteのIATF 16949認証取得を発表。この認証は、様々な産業における最高品質基準へのGKDのコミットメントを確認するものです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- COVID-19の影響とその他のマクロ経済動向の市場への影響

- 鉱業で扱われる様々な積載量に対応する様々なタイプのコンベヤソリューション

- 採掘セットアップにおけるコンベヤシステムの平均コスト

第5章 市場力学

- 市場促進要因

- インフラ開発と建築産業の増加

- 職場の安全性重視の高まり

- 市場抑制要因

- 高い資本要件と熟練労働者の不足

- COVID-19が業界に与える影響の評価

第6章 市場セグメンテーション

- タイプ別

- スチールコード

- テキスタイル強化

- その他のタイプ

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Sanwei Holding Group Co. Ltd

- Fenner Dunlop Australia Pty Ltd(Michelin group)

- Bando Chemical Industries Ltd

- ContiTech Deutschland GmbH(Continental AG)

- Tenova SpA(Techint Group)

- Dynamic Rubbers Pvt. Ltd

- Oriental Rubber Industries Pvt. Ltd

- Zhejiang Double Arrow Rubber Co. Ltd

- Bridgestone Corporation

- GKD Gebr. Kufferath AG

第8章 投資分析

第9章 市場機会と今後の動向

目次

The Conveyor Belt Market In Mining Industry is expected to grow from USD 1.96 billion in 2025 to USD 2.36 billion by 2030, at a CAGR of 3.8% during the forecast period (2025-2030).

The demand is boosted owing to increasing government initiatives and the number of coal mines in countries such as India. For instance, during the second pandemic wave, the Technology Roadmap document released by Coal India outlines that conveyors that may handle coal up to 4,500 tph/hr have been planned in Coal India. Conventional conveyors are limited to inclined angles around 16 to 18 degrees. The focus on upgrading the mines with advanced conveyor belts is aiding the market's growth.

Key Highlights

- In mining industry practices, the required output is desired, and the mining operator specifies rotary speed as a design parameter, determining the heat to be dissipated. This may strongly influence the dimensioning processes. This resulted in operating conditions that make a gear unit advisable larger than the output originally necessitates. If the conveyor belts operate in climatic zones that are unusually warm or even prone to extreme heat-cold fluctuations, much attention must be paid to cooling. For this reason, Siemens developed correspondingly efficient cooling solutions for its three gear-unit series, comprising 46 conveyor belt drive sizes. Therefore, in various cases, a smaller gear unit may be sufficient.

- India's journey toward becoming a developed nation by 2047 depends on improving its infrastructure. This is a cornerstone for fostering liveable, climate-resilient, and inclusive cities that drive economic growth. The government's commitment is evident through its allocation of 3.3% of GDP to the infrastructure sector in the fiscal year 2024, focusing on building high-end industrial segments.

- Ensuring occupational health and safety is a top priority in the mining industry. Mining operations are inherently challenging and pose various hazards and risks to workers. By prioritizing safety and implementing effective safety measures, companies may protect their workers, prevent accidents and injuries, and contribute to the overall sustainability of their operations.

- The mining industry operates under critical regulations and standards to ensure safety, environmental protection, and responsible practices. These include mine safety and health regulations, such as the Mine Safety and Health Administration (MSHA) in the United States.

- High initial costs have been the primary reason for restricting the use of automated material-handling systems, including conveyor belts and systems, to only large-scale organizations. At the same time, their long-term benefits are also considered. Small-and medium-scale enterprises may not benefit from this bargain. These systems require high levels of maintenance.

- Besides the direct impact on various market verticals, the global pandemic is also anticipated to have a long-term effect. For instance, since the pandemic, economies of multiple countries, which feel significant, are still unable to recover as anticipated, bringing a shadow of economic recession, especially in North American and European regions.

- For instance, according to the International Monetary Fund (IMF) estimates, the US real GDP growth is anticipated to remain slowed until 2024 before regaining momentum. Such trends may slow down the market by reducing investments in new metal and mining plants.

- According to the International Monitory Fund's (IMF's) July 2023 update, global economic growth was anticipated to fall from 3.5% in 2022 to about 3% in both 2023 and 2024 owing to the rising central bank policy rates to fight inflation, which is slowing down economic activities.

Mining Conveyor Belt Market Trends

Textile-reinforced Conveyor Belts to Witness Significant Growth

- Conveyor belts with textile reinforcement are typically used for abrasive and heavy-duty goods. They are a more affordable alternative to steel cord belts for shorter transporting distances and lesser capacities. The textile-reinforced conveyor belt is ideal for mining, mineral processing, and quarrying sectors. It may be blended with many different qualities, such as covers that are grease, heat, abrasion, impact, and fire-resistant quality. There are four basic types of construction for reinforcing high-strength belts: cord fabrics, straight warp fabrics, solid woven fabric, and cabled cords.

- The internal structure of a fabric belt carcass or textile consists of a single or multi-layered series of synthetic fabric layers interlaced between rubber-based shock-absorbent layers. The top and bottom sides of the belt consist of hard-wearing, abrasion, and cut-resistant rubber covers. The covers protect the belt from damage, especially at the loading points of the conveyor. This provides the tensile strength to the conveyor belt used in the mining industry.

- The strength, extension, and flexibility of synthetic fibers used in technical woven fabrics are higher than natural fibers used earlier. The primary fibers are cotton, viscose rayon, nylon, polyester, glass, and aramid. The aramid tenacity is seven times that of steel, and aramid is lighter than steel. It resists temperatures of 400-500 0C, dampness, and chemicals and has high abrasion resistance. Thus, it is used in mining conveyor belts. Its strength significantly influences the mining industry's carrying capacity and operating safety of conveyor belts. Therefore, materials like textile-reinforced conveyor belts are anticipated to become more prevalent to boost the conveyor belt's strength.

- The belting manufacturers supply tables for fabric belting, reflecting the number of plies proposed for a belt based on the different types and grades of materials to be transported on the belt. The fabric is better than steel reinforcement in conveyor belts as textiles make it much more flexible, high-strength, energy-efficient, corrosion-resistant, and lightweight.

- With rising mining activities across several regions and increased investments in the mining industry, the need for textile-reinforced conveyor belts is expected to rise in the forecast period.

Asia-P acific to Register Major Growth

- The government's ambitious 'Made in China 2025' initiative, partially inspired by Germany, for Industry 4.0 aims to boost the country's competitiveness in the industrial sector. The ten-year plan, introduced in May 2015, is the government's bid to shift the industries up to the medium-high end of the global industry value chain and foster several advanced manufacturing clusters. The increase in industrialization will grow the market for conveyor belt solutions for the mining sector.

- In April 2024, according to the National Development and Reform Commission, China announced it would build more coal mines to push for higher domestic supply and tame price increases. The world's biggest coal producer and consumer set targets to add about 300 million tons of annual mining capacity for "emergency storage reserves" by 2030.

- The increased government's infrastructure investments and investments from industries, coupled with the 'Make in India' initiative, are expected to drive the market studied. The Government of India increased the industrial sector's share of the gross domestic product (GDP) to 25% by 2022, from 17% in 2018.

- In February 2024, Indian state-run company Coal India announced it would begin operations at five new coal mines and expand the capacity of at least 16 existing mines to help meet the growing demand for fossil fuel. The miner plans to start operations at five new mines in the next fiscal year, with a combined annual capacity of 14.3 mt. These developments in the mining sector in India are likely to drive the market studied in the region.

Mining Conveyor Belt Industry Overview

The mining conveyor belt market is highly fragmented due to the presence of small and medium-sized enterprises and global players. Some of the major players in the market are Sanwei Holding Group Co. Ltd, Fenner Dunlop Australia Pty Ltd (Michelin Group), Bando Chemical Industries Ltd, Contitech Deutschland GMBH (continental AG), and Tenova SPA (Techint Group). Players in the market are adopting strategies such as acquisitions and partnerships to enhance their product offerings and gain sustainable competitive advantage.

- January 2024 - Fenner Dunlop BV and Fenner Dunlop Americas announced they would merge under the Fenner Dunlop Conveyor Belting brand starting January 1, 2024. The move aims to unify the brand across regions and divisions for a more robust global presence. Both divisions will trade under the Fenner Dunlop Conveyor Belting name, aligning their strategies for consistent branding. This change underscores the Fenner Group's commitment to enhanced coordination and market impact.

- November 2023 - Gebr. Kufferath AG announced the successful certification from IATF 16949 for the Durensite. The certification confirms GKD's commitment to the highest quality standards in various industries.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Trends on the Market

- 4.5 Various Types of Conveyor Solutions for Various Payloads Handled in the Mining Industry

- 4.6 Average Cost for Conveyor Systems in a Mining Setup

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rise in Infrastructure Development and the Building Industry

- 5.1.2 Increased Emphasis on Workplace Safety

- 5.2 Market Restraints

- 5.2.1 High Capital Requirements and Unavailability for Skilled Workforce

- 5.3 Assessment of the Impact of COVID-19 on the Industry

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Steel Cord

- 6.1.2 Textile Reinforced

- 6.1.3 Other Types

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia

- 6.2.4 Australia and New Zealand

- 6.2.5 Latin America

- 6.2.6 Middle East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Sanwei Holding Group Co. Ltd

- 7.1.2 Fenner Dunlop Australia Pty Ltd (Michelin group)

- 7.1.3 Bando Chemical Industries Ltd

- 7.1.4 ContiTech Deutschland GmbH (Continental AG)

- 7.1.5 Tenova SpA (Techint Group)

- 7.1.6 Dynamic Rubbers Pvt. Ltd

- 7.1.7 Oriental Rubber Industries Pvt. Ltd

- 7.1.8 Zhejiang Double Arrow Rubber Co. Ltd

- 7.1.9 Bridgestone Corporation

- 7.1.10 GKD Gebr. Kufferath AG

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 111 Pages

- 納期

- 2~3営業日