|

市場調査レポート

商品コード

1910926

欧州のビルオートメーションシステム市場- シェア分析、業界動向、統計、成長予測(2026年~2031年)Europe Building Automation Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のビルオートメーションシステム市場- シェア分析、業界動向、統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 161 Pages

納期: 2~3営業日

|

概要

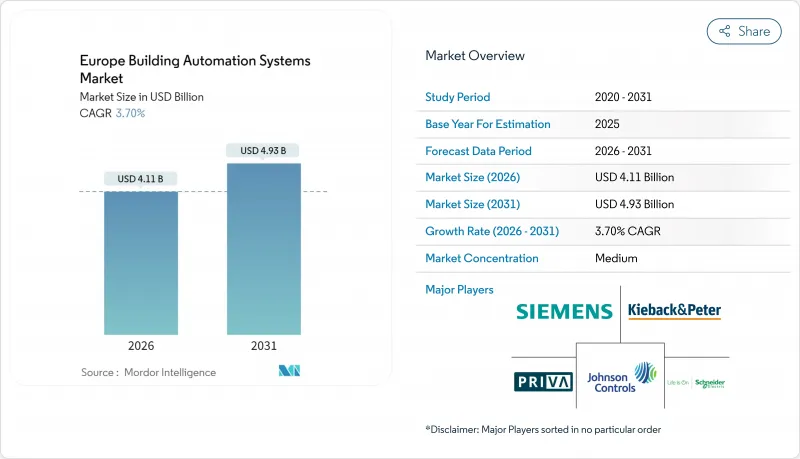

欧州のビルオートメーションシステム市場は、2025年に39億6,000万米ドルと評価され、2026年の41億1,000万米ドルから2031年までに49億3,000万米ドルに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは3.70%と見込まれます。

改訂された「建物のエネルギー性能指令」に基づくコンプライアンス義務の強化、電気料金の上昇、企業のネットゼロ目標が、投資判断の大部分を導いています。同地域の建築ストックの4分の3が1990年以前に建設されたものであるため、改修需要が主流となっていますが、イノベーションはクラウド対応分析、ワイヤレスセンサー、AI駆動型最適化に集中しています。ハードウェアが収益の基盤であり続ける一方、SaaS(サービスとしてのソフトウェア)は継続的な収入源をもたらし、中規模不動産ポートフォリオの投資回収期間を短縮します。競合は中程度です:コアコントローラーやフィールドデバイスを供給する世界のメーカーは数社ですが、数百の地域インテグレーターが納期、プロジェクトコスト、ユーザートレーニングの成果を形作っています。持続的な労働力不足とサイバーセキュリティ上の責任が、プロジェクトの進捗速度に対する短期的なブレーキとして作用していますが、製品の標準化とエコシステムパートナーシップにより、リスク認識は徐々に軽減されつつあります。

欧州ビルオートメーションシステム市場の動向と洞察

EPBD改正におけるBACS義務化

2025年に施行される改正エネルギー性能指令(EPBD)により、暖房負荷290kWを超える非住宅施設は相互運用可能な自動化・制御システムの導入が義務付けられます。ドイツとフランスではさらに厳しい基準が採用され、官公庁・学校・医療施設における入札活動が加速しています。BACnetやKNXなどのオープンプロトコルソリューションは補助金プログラムで優遇措置を受け、建物所有者は計画的な改修時に独自規格ネットワークの置き換えを促されています。適合期限は2027年頃に集中しており、エンジニアリング需要の顕著なピークを生み出し、専門的な研修イニシアチブを喚起しています。施行の厳格さは加盟国によって異なりますが、全体的な義務付けにより欧州ビルオートメーションシステム市場の成長は規制スケジュールに組み込まれています。現地設置パートナーと多言語対応の試運転ソフトウェアを有するベンダーは、明らかな競争優位性を獲得しています。

無線センサー価格の急落

マルチテクノロジー対応の在室検知・温度・照度センサーの平均販売価格は、2023年から2025年にかけて約30%下落しました。主な要因は、東アジアにおける200mmウェーハ生産量の増加と、システムオンチップ(SoC)アーキテクチャへの移行です。北欧の不動産所有者は早期導入者であり、長期間の暖房シーズン中にエネルギー集約型施設を監視するため、電池駆動センサーを活用しています。配線工事や天井コア掘削コストの削減により、小規模プロジェクトの投資回収期間が短縮され、顧客基盤がAグレードオフィスタワー以外にも拡大しています。新チップに組み込まれたエッジ処理機能は、遅延の低減、誤検知のスクリーニング、機密性の高い建物使用データの施設内保持を実現し、GDPR準拠を支援します。部品価格は2021-2022年の供給逼迫時ほど変動しなくなりましたが、特殊なRFマイクロコントローラーの断続的な不足により、インテグレーター向けのリードタイムが小幅に上昇するケースが依然として発生しています。

分断された既存建築ストック

パリ、ローマ、バルセロナなどの歴史的石造建築では、コア掘削や大規模な配管工事が制約されることが多く、センサー設置や配線作業が複雑化します。ラジエーターから可変風量ボックスまで、異なる時代の機械設備が混在しているため、入念なインターフェース設計が必要となり、設計工数と予備予算が増加します。オーナー様は、大規模なテナント入れ替え時まで高度な自動化を延期されることがあり、意思決定サイクルが従来の会計年度を超えて長期化します。地域の職人組合が保存基準を厳格に適用するため、侵襲的な改修は制限されます。その結果、インテグレーターは無線式・電池不要のアクチュエーターや、歴史的建造物ガイドラインに準拠した可逆マウントキットに投資しますが、こうした特殊部品は価格プレミアムが付き、投資回収期間を短縮します。

セグメント分析

ハードウェアは2025年の収益の65.58%を占め、信頼性の高いコントローラー、アクチュエーター、マルチスタンダードゲートウェイが欧州ビルオートメーションシステム市場規模のあらゆる機能層を支えています。コントローラーは日常的に数千のI/Oポイントを管理するため、サプライヤーはリアルタイム処理とサイバーセキュリティ強化の高度化を迫られています。並行して、センサーは超低消費電力ワイヤレスチップへ移行し、ケーブルトレイが不足する1910年以前の建物内における改修可能性を拡大しています。

クラウド型分析サービスとリモートファームウェア更新が、SaaSサブスクリプションのCAGR6.02%を牽引しています。建物所有者は資本支出よりも運用経費を重視し、AIベースの最適化機能を継続契約で購入しています。予測可能な課金体系は予算計画を容易にし、継続的な機能拡張を促進します。建物のHVACループがオンライン化されると、照明、セキュリティ、EV充電器モジュールが迅速に追随します。ベンダーはエッジAI推論機能をルームコントローラーに統合し、ハイパースケールデータセンターからの計算負荷を軽減するとともに、地域のデータ主権法への準拠を実現しています。

2025年時点で欧州ビルオートメーションシステム市場の44.92%を商業施設が占めており、義務化されたエネルギー監査と競合環境がこれを後押ししています。施設管理者はハイブリッドワーク環境における入居者誘致のため、熱的快適性と室内空気品質ダッシュボードを優先的に導入。病院では陰圧制御のための重要区域をアップグレードし、小売業界では食品廃棄削減のためAIベースの冷蔵監視システムを導入しています。

住宅需要は、スマートメーター導入の補助金や国家的な電化促進策を契機に、2031年までCAGR5.59%で拡大します。集合住宅では光熱費を正確に配分するため集中プラント制御を導入し、一戸建て住宅では音声操作シーンや需要応答ウィジェットが主流となります。単体あたりの導入ポイントは少ないもの、世帯全体の導入規模は小規模商業施設に匹敵するため、家電メーカーは従来のBASサプライヤーとの提携を推進しています。

欧州ビルオートメーションシステム報告書は、構成要素(ハードウェア:コントローラーおよびフィールドデバイス、SaaS型ソフトウェア)、エンドユーザー(住宅、商業、産業)、ビルライフサイクル(新築、改修)、通信プロトコル(BACnet、KNX ClassicおよびIoT、Modbus/LonWorks)、地域別に分類されています。市場予測は金額ベース(米ドル)で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3か月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- エネルギー性能指令(EPBD)改正におけるBACSの義務化

- 無線センサー価格の急激な下落

- 企業のネットゼロ目標

- エッジAI分析による運用コスト削減効果

- スマートホーム改修の増加

- ESG連動型金融インセンティブ

- 市場抑制要因

- 分散した既存建築ストック

- サイバーセキュリティ上の責任に関する懸念

- ベンダー固有のプロトコルによるロックイン

- 熟練労働者の不足

- 業界バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- コンポーネント別

- ハードウェア

- コントローラー

- フィールドデバイス

- サービスとしてのソフトウェア(SaaS)

- ハードウェア

- エンドユーザー別

- 住宅用

- 商業用

- 産業用

- 建物ライフサイクル別

- 新築

- 改修

- 通信プロトコル別

- BACnet

- KNX(クラシックおよびIoT)

- Modbus/LonWorks

- 地域別

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- ベルギー

- スウェーデン

- フィンランド

- デンマーク

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Siemens AG

- Johnson Controls International plc

- Schneider Electric SE

- Honeywell International Inc.

- ABB Ltd

- Robert Bosch GmbH

- Trane Technologies plc

- Kieback and Peter GmbH and Co. KG

- Priva Holding B.V.

- Belimo Holding AG

- Fr. Sauter AG

- Lynxspring Inc.

- Delta Controls Inc.

- Legrand SA

- Distech Controls Inc.

- Regin AB

- Danfoss A/S

- Beckhoff Automation GmbH and Co. KG

- Somfy SA

- Crestron Electronics Inc.