|

市場調査レポート

商品コード

1910924

ライセンス管理:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)License Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ライセンス管理:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 124 Pages

納期: 2~3営業日

|

概要

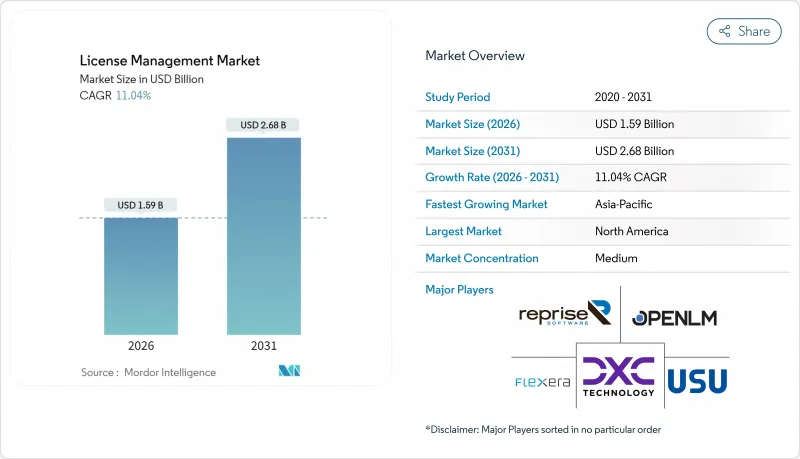

ライセンス管理市場は、2025年の14億3,000万米ドルから2026年には15億9,000万米ドルへ成長し、2026年から2031年にかけてCAGR 11.04%で推移し、2031年までに26億8,000万米ドルに達すると予測されています。

デジタル化の加速、SaaSインフレの拡大、EUデジタル業務レジリエンス法などの新たな規制要件により、ハイブリッドIT環境全体における自動化されたガバナンスへの需要が高まっています。規制当局の監視強化、監査頻度の増加、リアルタイムのコスト管理の必要性により、ソフトウェア資産ガバナンスはサポート機能から取締役会レベルの優先事項へと移行しています。ベンダー各社は、プラットフォーム統合、AIを活用した検出機能、サブスクリプション型ビジネスモデルを通じて対応を進めており、これにより企業はコンプライアンスリスクを抑制しつつ最適化のメリットを享受できます。同時に、FinOps導入の拡大と未使用ライセンスのコスト増加(大企業1社あたり年間1億2,730万米ドルと推定)は、積極的なライセンスインテリジェンスによる具体的なコスト削減効果を浮き彫りにしています。これらの要因が相まって、ライセンス管理市場は2030年まで持続的な成長軌道が確固たるものとなるでしょう。

世界のライセンス管理市場の動向と洞察

SaaSおよびサブスクリプション型ライセンシングへの加速的な移行

SaaS支出は2023年から2025年にかけて31%増加し、3,000億米ドルに達し、現在では平均的な企業のコスト基盤の25%を占めています。サブスクリプションの更新、使用量ベースの価格設定、多層的な利用権限により、調達チームはライセンス状況を最新の状態に保つための自動化を推進しています。顧客の27%に影響を与えるシュリンクフレ(価格上昇を隠す戦略)は、契約内容の微調整によって値上げを隠蔽するため、コスト予測可能性には詳細な使用状況の洞察が不可欠です。その結果、請求データを機能レベルまで解析できるクラウドネイティブプラットフォームが、ライセンス管理市場全体で普及しつつあります。

ベンダー監査の頻度とコストの増加

出版社による収益回復策の一環として監査頻度が増加しており、米国政府監査院が指摘した公共部門の不足分がこれを後押ししています。ハイブリッドクラウドの拡大は複雑性を増しており、従来の発見ツールでは仮想化環境、コンテナ化環境、SaaS資産を容易に整合させられません。そのため企業は、発見機能・権限データ・契約ロジックを単一の管理基盤で統合するソリューションに、より大きなコンプライアンス予算を割り当てています。この監視強化が、ライセンス管理市場における持続的な二桁成長を支えています。

不透明なベンダー固有のライセンス条項と測定基準

頻繁なメトリクスの再設計(ユーザー数ベース、コア数ベース、使用量ベースなど)はコスト可視性を低下させます。ブロードコムによるVMware販売の一週間停止は、サプライヤーのシステム変更が顧客のガバナンスワークフローを阻害する事例を示しました。組織は契約文言の解読に不釣り合いな法的・技術的労力を費やし、最適化サイクルを遅延させます。これにより、専門的な助言を得られない中小企業のライセンシング市場への参入に抑制的な圧力が生じています。

セグメント分析

ソフトウェアプラットフォームは、コアとなる発見・標準化・照合エンジンがガバナンス運用において依然として基盤的役割を担っていることから、2025年においてもライセンス管理市場シェアの61.74%を維持しました。この優位性は、2025年のライセンス管理市場規模のうち8億8,000万米ドルを占める基盤となっており、企業が設定可能なポリシー駆動型自動化を大規模に必要としていることを反映しています。しかしながら、サービスセグメントは14.56%のCAGRで拡大が見込まれており、企業が希少な専門知識を持つパートナーに最適化業務を委託する動きが、ライセンス管理市場規模を急速に拡大させています。

マネージドサービスプロバイダーはAIを組み込み、更新ピークを予測し、ベンダー監査前にコンプライアンス違反を検知します。この継続的監視モデルは、特にアジア太平洋地域やラテンアメリカにおいて、認定ソフトウェア資産管理人材の慢性的な不足に直面する組織のニーズに合致します。その結果、サービス収益は2031年までにソフトウェア収益との差を縮め、従来ライセンシングに重点を置いてきたベンダーの競合戦略を変革すると予想されます。

2025年時点で、クラウド導入はライセンス管理市場シェアの57.36%を占めました。これは、永続的なオンプレミスツールから、より広範なIT戦略を反映したサブスクリプション型SaaSプラットフォームへの移行を進める企業によって推進されています。クラウドアーキテクチャは即時更新、弾力的なスケーリング、APIレベルの統合を実現し、マルチクラウド環境におけるリアルタイム消費分析を可能にします。これにより14.02%のCAGRが維持され、本セグメントはライセンス管理市場において中核的な位置付けを維持する見込みです。

オンプレミスソリューションは、ローカルデータ保持が要求される高度に規制された業界や、レガシーインフラ依存を維持する分野で引き続き採用されています。しかし、クラウド分析とオンプレミス検出を組み合わせ、俊敏性を犠牲にすることなく主権要件を満たすハイブリッドモデルが注目を集めています。クラウドファーストガバナンスを採用する企業では、管理オーバーヘッドが40%削減されると報告されており、継続的な移行の経済的根拠を強化し、ライセンス管理市場全体の規模拡大に寄与しています。

地域別分析

北米におけるライセンス管理市場規模は2025年に5億4,000万米ドルに達し、成熟した企業IT支出と活発な監査文化に支えられ、37.68%という圧倒的なシェアを占めました。SECのサイバーリスク開示規則による厳しい期限設定が、ソフトウェアの完全な可視化達成に緊急性を加えています。カナダの公共部門近代化プログラムは地域需要をさらに押し上げていますが、大企業への浸透が飽和状態に達したため、成長率は一桁台に鈍化しています。

アジア太平洋地域は2025年のベース値は小規模でしたが、2031年までに市場をリードする13.29%のCAGRを達成すると予測されています。生成AIへの投資は34億米ドルと3倍に増加し、中国では前年比160%の支出増が見込まれます。このような急速な導入は、言語モデル、データパイプライン、分析テナント全体でライセンスの複雑性を高めています。現地ベンダーは、ライセンシングの専門家と提携し、権利追跡やコストガバナンスのギャップを解消することで、地域的な勢いを加速させています。

欧州はDORA(デジタル・オペレーション・レジリエンス法)の遵守期限を背景に、ライセンス管理市場で大きなシェアを占めています。金融機関は厳格なレジリエンス指標を満たすため、資産ログと監査ワークフローの再構築を進めています。一方、ラテンアメリカ、中東・アフリカではクラウド普及が進む中、スプレッドシート管理から商用プラットフォームへの移行が進んでいます。これらの地域はまだ発展途上ではありますが、今世紀末までに世界のライセンス管理市場規模に漸増的な成長をもたらすと予想されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3か月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- SaaSおよびサブスクリプション型ライセンシングへの移行加速

- ベンダー監査の頻度とコストの増加

- FinOps方針に基づくIT資産最適化の義務化

- AIを活用した「シャドーIT」ライセンスの発見

- EUデジタル運用レジリエンス法(DORA)の遵守期限

- IIoTプラットフォームにおける組込みデバイスライセンシングの収益化

- 市場抑制要因

- 不透明なベンダー固有のライセンス条項と測定基準

- 断片化されたポイントツールのエコシステムは統合コストを増加させます

- 認定されたSAM人材の供給不足

- オープンソースの採用増加により商用ライセンスの需要が減少

- 業界バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- コンポーネント別

- ソフトウェア

- サービス

- 展開別

- オンプレミス

- クラウド

- 用途別

- 監査サービス

- アドバイザリーサービス

- コンプライアンス管理

- ライセンス権限と最適化

- オペレーションズとアナリティクス

- その他の用途

- エンドユーザー産業別

- 銀行・金融サービス・保険(BFSI)

- ヘルスケアおよびライフサイエンス

- ITおよび通信

- メディアとエンターテイメント

- その他のエンドユーザー産業

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- その他のアジア

- 中東

- イスラエル

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- エジプト

- その他アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Flexera Software LLC

- USU Software AG

- Snow Software AB

- IBM Corporation

- ServiceNow Inc.

- Oracle Corporation

- Broadcom Inc.(CA Technologies)

- Micro Focus International plc

- DXC Technology Company

- OpenLM Ltd

- SAP SE

- Thales Group(Gemalto)

- Quest Software Inc.

- Reprise Software Inc.

- Ivanti, Inc.

- License Dashboard Ltd

- Certero Ltd

- Zylo Inc.

- LeanIX GmbH

- OpenText Corporation