|

市場調査レポート

商品コード

1690753

米国のMEPサービス:市場シェア分析、産業動向、成長予測(2025年~2030年)United States (US) MEP Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国のMEPサービス:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

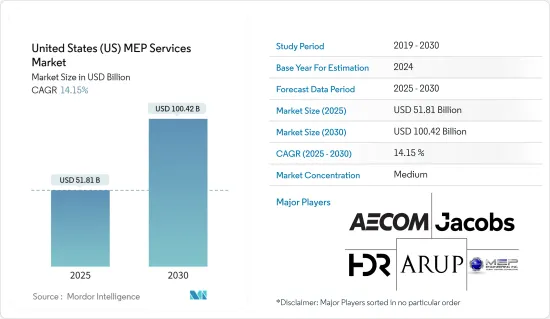

米国のMEPサービス市場規模は2025年に518億1,000万米ドルと推定され、2030年には1,004億2,000万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは14.15%です。

主要ハイライト

- 機械・電気・配管(MEP)には、建物のさまざまなMEPシステムの計画、設計、管理が含まれ、建物の建設、計画、管理にBIMを取り入れる動きが活発化する中、MEPサービスはさらに牽引力を増しています。

- MEPはプロジェクトの建設コストの大部分を占めます。この地域では、デンバー国際空港の改修やニューヨーク市の輸送のアップグレードなど、建設プロジェクトが増加しており、市場の成長を促進すると予想されます。

- COVID-19の流行は、サプライチェーンの混乱に関してMEPサービス市場に影響を与えました。工場の操業停止により、一部の製品のリードタイムが延びた。しかし、現在は工場がフル稼働しているため、生産レベルは大幅に改善し始めています。

- 設計はMEPサービスにおいて重要な役割を果たしています。どのサービスプロバイダにとっても、収益のかなりの部分はMEP設計から生み出されているからです。Consulting-Specifying Engineerの調査によると、2019年中のMEPジャイアンツを合わせた収益の半分以上(58%)がMEP設計から生み出され、1社当たりの平均MEP設計収益は8,390万米ドルとなり、前年に比べ大幅な増加が観察されました。

- 米国のMEPサービスの需要は、新築と改修・改築の需要によって牽引され、両セグメントが市場で大きなシェアを占めています。しかし、同国のMEPサービス市場シェアに関しては、新築セグメントがやや優勢です。

- 建設設計産業では、持続可能性というコンセプトが勢いを増しています。エコフレンドリーシステムを導入すれば、最終的には環境にも予算にもプラスになるというのが産業のコンセンサスです。米国環境保護庁(EPA)によると、米国の発電量はエネルギー消費全体の40%を占めています。そのため、各地域のベンダーは、ソーラー捕収剤や熱回収換気などのMEP技術を活用し、需要に対応するサービスを提供しています。

- 米国エネルギー情報局(EIA)によると、商業ビルでエネルギーを消費する主要部門は、空調設備がビル全体の35%、照明が11%、冷蔵庫、給湯器、冷凍庫などの電化製品が18%で、残りはその他の電子機器に分配されます。そこで、消費者のコスト削減を可能にする強固な設計を開発する上で、MEPサービスプロバイダが不可欠となります。

- しかし、現在の市場シナリオでは、COVID-19が建設プロジェクトを請け負った企業や政府機関に及ぼした影響により、建設プロジェクトの一部が遅延し、キャンセルに至ったものもあります。例えば、サプライチェーンの制約により、エンドユーザー企業が中国から導入した輸入建設資材の30%近くが、製造業の生産高を減少させています。こうした事例は、市場成長を妨げる可能性を秘めたMEPサービス市場のネガティブな展望の一部を示しています。

米国のMEPサービス市場動向

新規建設が市場成長を牽引

- 米国ゼネコン協会(AGC)によると、建設産業は米国経済に大きく貢献しています。同産業には73万3,000以上の雇用主があり、700万人以上の従業員を抱え、毎年約1兆4,000億米ドル相当の建造物を生み出しています。建設業は、製造業、鉱業、さまざまなMEPサービスの主要顧客のひとつです。また、不況期における重要な経済活性化要因ともなっています。

- 住宅建設部門は、米国のCOVID-19危機からの経済回復の主役であり、2020年第3四半期以降2桁の成長率を記録し、経済の回復と建設産業全体の成長に大きく貢献しています。多くの建設プロジェクトがロックダウンの機会を利用するために急ピッチで進められ、COVID-19の局面では増収となりました。予測期間中、市場は請け負ったプロジェクトの急激な増加を修正すると予想されます。

- さらに、企業収益は着実に増加しており、最終ラインは依然としてかなりの圧力下にあります。産業が直面する課題の中には、持続的なコスト圧力、生産性に影響を及ぼす継続的な労働力不足、従来のシステムでは困難なレベルの価格設定と業務精度がしばしば要求される固定入札プロジェクトの動向などがあります。デジタル技術の継続的な導入は、こうした問題のいくつかを軽減する可能性があります。

- また、導入の成功や、技術を吸収するための従業員のスキルアップという点で、さらなるハードルが立ちはだかる可能性もあります。こうした課題にもかかわらず、MEP企業は、米国の交通インフラ改善イニシアティブやスマートシティ・メガプロジェクトの成長など、産業のさまざまな大きな機会から潜在的な利益を得る態勢を整えています。

医療機関からの需要が市場成長を牽引

- この地域の医療部門は、経済が最適に機能するために重要な部門のひとつと考えられています。しかし、医療施設における非効率的な計画とリソース不足という大きな問題に直面しています。例えば、ヒューマナ社とピッツバーグ大学の研究者は、2012年1月から2019年5月までのデータに基づき、医療費の約25%が非効率的であると報告しました。

- そのため、医療部門のエンドユーザーは、施設内の非効率を活用するためにMEPサービスが提供する可能性に気づき始めています。さらに、医療施設では、手術室、婦人科、小児科など、各部門に固有の要件があります。さらに、不適切な設計は、患者の治療に致命的な影響を及ぼす可能性があります。例えば、内部の空気の質が低ければ、患者の健康に悪影響を及ぼす可能性があります。このように、MEPサービスは、医療業務の基幹となるシステムをサポートする可能性を秘めています。

- さらに、現在進行中のパンデミックCOVID-19は、この地域のパンデミック対策の準備不足を露呈し、医療システムの非効率性と不公平性を露呈しました。例えば、医療インフラはCOVID-19患者を受け入れることができず、他の先進諸国に比べて一人当たりの病床数が少ないです。

- そのため、この地域の政府機関は効率的な医療施設の建設に多くの資源を割り当て始めており、こうした事例によってMEPサービスの需要が急増すると予想されます。例えば、2020年5月、AECOMはニューヨーク市設計建設局(DDC)がCOVID-19緊急施設として機能することを目的とした2つの仮設病院を建設するプロジェクトを完了したと発表しました。

米国MEPサービス産業概要

米国のMEPサービス市場は適度にセグメント化されています。主要企業は、Jacobs Engineering Group Inc、HDR Inc、AECOM、Arup Groupなどです。同市場のベンダーは、パートナーシップやコラボレーションを活用して市場シェアを獲得しています。最近の市場動向は以下の通りです。

- 2020年6月、AECOMは、世界のオルタナティブ資産運用会社であるCanyon Partners, LLCと共同で、The Martin Groupと共同で、中層学生住宅プロジェクトであるWexlerの交通指向型開発を開始すると発表しました。同社は、Pacific Western Bankから7,330万米ドルのシニア建設ローンを借りたと発表しました。プロジェクトは2020年秋までに完成予定。

- 2020年10月、カリフォルニア大学サンフランシスコ校(UCSF)は、新病院「UCSF Helen Diller Medical Center at Parnassus Heights(パルナサスハイツのUCSFヘレン・ディラー・メディカルセンター)」の主任MEPエンジニアとして、アラップとサンフランシスコを拠点とする医療スペシャリストのMazzettiを選定。アラップはまた、土木工学サービスや音響・振動、ロジスティクスコンサルティングなどの追加サービスをプロジェクトに提供する可能性もあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の設計・エンジニアリングサービス産業への影響評価

- 米国におけるMEPエンジニアの現在の雇用指数

- 技術の進歩がMEPサービス産業に与える影響(CAD、BIM、MEPソフトウェアなど)

第5章 市場力学

- 市場の促進要因

- MEPサービスのアウトソーシング重視の高まりによるコアサービスの集中化

- 商業施設や医療施設からの安定した需要

- ビジネスモデルの進化と企業とサービスベンダーの協力関係

- 市場抑制要因

- 高い市場集中度とエンド・ツー・エンド・オファリングへの需要拡大における経営課題が中小企業に影響

第6章 市場セグメンテーション

- タイプ別

- 新築

- 改修・改装

- コミッショニング活動

- その他

- 産業別

- 医療

- 商業オフィス

- 教育機関

- 公共スペース・施設

- 工業施設・倉庫

- その他の商業施設(データセンター、調査など)

第7章 競合情勢

- 企業プロファイル

- Jacobs Engineering Group Inc.

- HDR Inc

- Arup Group

- AECOM

- MEP Engineering

- Stantec Inc.

- Affiliated Engineers Inc.

- Macro Services

- WSP Group

- AHA Consulting

- Burns Engineering

- Wiley Wilson

第8章 投資分析

第9章 市場の将来

The United States MEP Services Market size is estimated at USD 51.81 billion in 2025, and is expected to reach USD 100.42 billion by 2030, at a CAGR of 14.15% during the forecast period (2025-2030).

Key Highlights

- Mechanical electrical and plumbing (MEP) involves planning, designing, and managing various MEP systems of a building, and with the increasing incorporation of BIM in building construction, planning, and management, MEP services are further gaining traction.

- The MEP contribute to the significant portion of projects' construction cost. With the growing number of construction projects in the region, such as Denver International Airport renovation and New York City transit upgrades, it is expected to drive the growth of the market.

- The COVID-19 pandemic has impacted the MEP services market with respect to disruptions in the supply chain. Lead times for some products were increased due to factory shutdowns. However, now with factories functioning at full capacities, production levels are beginning to see significant improvements.

- Design plays a vital role in MEP services as a significant share of the revenue for any service provider is generated from MEP design. According to a study by Consulting-Specifying Engineer, over half (58%) of the revenue from all of MEP giants combined during 2019 was generated from MEP design, with an average MEP design revenue of USD 83.9 million per firm and observed a significant increase compared to the previous year.

- The US demand for MEP services is driven by new construction and retrofit and renovation demand with both segments, driving a prominent share of the market. However, the new construction segment commands a slight upper hand when it comes to the MEP services market share in the country.

- The concept of sustainability is gaining momentum in the construction design industry; the industry consensus is that installing eco-friendly systems would eventually benefit the environment and the budget. According to the EPA, electricity generation in the US accounts for 40% of the total energy consumption. Thereby vendors in the regions are leveraging the MEP technologies such as solar collectors and ventilation with heat recovery accompanied by their services to counter the demand.

- According to the US Energy Information Administration (EIA), in a commercial building, major energy-consuming sections are HVAC systems at 35% of the total building energy, lighting at 11%, appliances, such as refrigerators, water heaters, and freezers at 18%, and the remaining is shared among various other electronics. This is where MEP service providers become vital in developing robust designs that enable consumers to reduce costs.

- However, in the current market scenario, some of the construction projects have been delayed, and some resulted in cancellation as the result of the impact of COVID-19 on the companies and government bodies that commissioned them. For instance, nearly 30% of imported construction material deployed by the end-user firms from China due to supply chain constraints manufacturing output has declined. These instances showcase some of the negative outlooks of the MEP services market that holds the potential to hinder market growth.

US MEP Services Market Trends

New Construction to Drive the Market Growth

- As per the Associated General Contractors (AGC) of America, the construction industry is a major contributor to the US economy. The industry has more than 733,000 employers with over 7 million employees and creates nearly USD 1.4 trillion worth of structures each year. Construction is one of the major customers for manufacturing, mining, and a variety of MEP services. It is also seen as a significant economic reviver during the recession period.

- The residential construction sector has been the star performer of the United States' economic recovery from the COVID-19 crisis, posting double-digit growth rates since the third quarter of 2020 and making significant contributions to the rebound of the economy and the overall construction industry growth. Many construction projects were fast-tracked to utilize the opportunity of the lockdown and resulted in an increased revenue during the COVID-19 phase. Over the forecast period, the market is expected to correct the sudden increase in projects undertaken.

- Moreover, firm revenues are steadily rising, and the bottom lines are still under considerable pressure. Among the challenges that the industry face is sustained cost pressures, ongoing labor shortages that affect productivity, and trends toward fixed-bid projects that often demand a level of pricing and operations precision that is difficult to obtain with traditional systems. While the industry still trails broader digital acceptance maturity, the continued adoption of digital technologies could alleviate some of these issues.

- It can also present additional hurdles in terms of successful implementations and upskilling the workforce to absorb the technologies. Despite these challenges, MEP firms are poised to potentially benefit from various significant industry opportunities, including the US transportation and infrastructure upgrade initiative and the growth of smart city mega-projects.

Demand from Healthcare Institutions to Drive Market Growth

- The healthcare sector in the region is considered one of the crucial sectors for the optimal functioning of the economy. However, it faces the huge problem of inefficient planning and insufficient resources at the healthcare facilities. For instance, Humana and the University of Pittsburgh researchers reported that based on the data from January 2012 to May 2019, approximately 25% of healthcare spending could be characterized as inefficient.

- Thereby, end-user from the healthcare sector are starting to realize the potential offered by MEP services to leverage inefficiencies in the facilities. Moreover, In a healthcare facility, each department has its specific requirements: operation theatre, Gynaecological Department, or the Paediatrics Department. Additionally, incompetent designs could lead to a catastrophic effect on patient treatment. For instance, low internal air quality could cause adverse effects on the health of the patients. Thus, MEP services hold the potential to support the systems that are the backbone of healthcare operations.

- Furthermore, the ongoing pandemic COVID-19 has showcased the region's lack of preparation to counter the pandemic and has exposed the health system's inefficiencies and inequities. For instance, the healthcare infrastructure cannot accommodate COVID-19 patients and has fewer hospital beds per capita than other developed countries.

- Thereby these instances are expected to surge the demand for MEP service as the government bodies in the region are starting to allocate many resources into the construction of efficient medical facilities. For instance, In May 2020, AECOM announced it had completed the New York City Department of Design and Construction's (DDC) project to construct two temporary hospitals that are aimed to serve as COVID-19 emergency facilities.

US MEP Services Industry Overview

The United States MEP Services Market is moderately fragmented. The major companies include Jacobs Engineering Group Inc, HDR Inc, AECOM, and Arup Group. Vendors in the market are leveraging partnerships and collaborations to capture the market share. Some of the recent developments in the market are:

- June 2020: AECOM, in partnership with Canyon Partners, LLC, a global alternative asset management firm, announced a joint venture with The Martin Group to begin the transit-oriented development of Wexler, a mid-rise student housing project. The company announced that it had taken a USD 73.3 million senior construction loan from Pacific Western Bank. The project is scheduled to be completed by fall 2020.

- October 2020: The University of California, San Francisco (UCSF) selected Arup and San Francisco-based healthcare specialists Mazzetti as the lead MEP engineers of record for its new hospital, UCSF Helen Diller Medical Center at Parnassus Heights (Parnassus Heights). Arup could also be providing additional services for the project, including civil engineering services and acoustics/vibration and logistics consulting.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Design and Engineering Services Industry

- 4.4 Current Employment Index of MEP Engineers in the United States

- 4.5 Impact of Technological Advancements on the MEP Services Industry (CAD, BIM, MEP Software, etc.)

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Emphasis on Outsourcing of MEP Services to Focus on Core Offering

- 5.1.2 Steady Demand from Commercial and Healthcare Institutions

- 5.1.3 Evolving Business Models and Nature of Collaboration between Firms and Service Vendors

- 5.2 Market Restraints

- 5.2.1 Operational Challenges in High Market Concentration and Growing Demand for End-to-end Offering Affect Smaller Firms

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 New Construction

- 6.1.2 Retrofit & Renovation

- 6.1.3 Commissioning Activity

- 6.1.4 Other Types

- 6.2 By End-user Vertical

- 6.2.1 Healthcare

- 6.2.2 Commercial Offices

- 6.2.3 Educational Institutions

- 6.2.4 Public Spaces and Institutions

- 6.2.5 Industrial establishments & Warehouses

- 6.2.6 Other Commercial entities (Data centers, Research, etc.)

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Jacobs Engineering Group Inc.

- 7.1.2 HDR Inc

- 7.1.3 Arup Group

- 7.1.4 AECOM

- 7.1.5 MEP Engineering

- 7.1.6 Stantec Inc.

- 7.1.7 Affiliated Engineers Inc.

- 7.1.8 Macro Services

- 7.1.9 WSP Group

- 7.1.10 AHA Consulting

- 7.1.11 Burns Engineering

- 7.1.12 Wiley Wilson