自動車産業におけるビッグデータ:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

Big Data In The Automotive Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690751

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

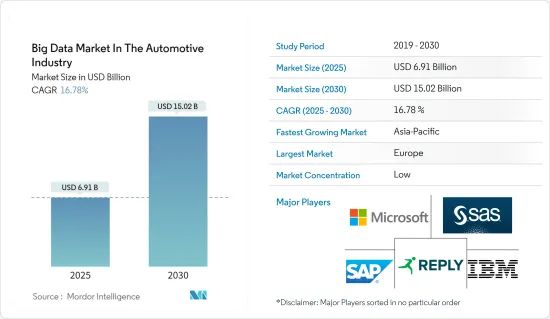

自動車産業におけるビッグデータ市場は、2025年の69億1,000万米ドルから2030年には150億2,000万米ドルに成長し、予測期間中(2025~2030年)のCAGRは16.78%になると予測されます。

自動車産業は、センサから人工知能、ビッグデータ分析に至るまで、技術、アプリケーション、サービスを採用することで変貌を遂げつつあります。そのため、エコシステムには新たな参入企業が着実に流入しており、その結果、未来の自動車が継続的に進化しています。コネクテッドカーの設置台数の増加と相まって、車両が生成するデータの活用に向けた様々な利害関係者の取り組みが活発化していることが、市場成長の原動力となっています。

主要ハイライト

- ビッグデータ分析により、自動車製造産業はERPシステムからデータを収集し、事業の複数の機能単位とサプライチェーンメンバーからの情報を組み合わせることができます。ネットワーク化されたシステムである産業IoTとM2M通信の出現により、自動車産業はインダストリー4.0に向けたポジショニングをとっています。センサ、RFID、バーコードリーダー、ロボットは今や産業の製造現場で標準となっています。これらのデバイスにより、データ生成ポイントは指数関数的に増加しています。

- 民生用電子機器産業は需給要因に大きく左右されます。ビッグデータ分析の活用は、この産業セグメントを劇的に助け、プッシュ型市場戦略からプル型市場戦略への転換を可能にしました。ビッグデータ分析によって、この産業は消費者の行動パターンをより意識するようになり、それに基づいて生産計画を立てることができるようになりました。IoTの進化や電子部品が自動車に不可欠な部品となったことで、自動車セグメントでも同様の可能性が露呈しています。

- さらに、ビッグデータ分析は、自動車メーカーが販売やマーケティングの面で効率を高めるのに役立ちました。また、予知保全やサービススケジュールのような公益事業の組み込みを支援することで、業務も改善されました。また、自動車ベンダーが需要予測のためにデータを分析することで、調達プロセスを合理化し、コスト効率を高めるのにも役立ちました。

- OEMにとってデータはますます重要になってきています。そのため、強力なプライバシー戦略を通じて一般データ保護規則(GDPR)を確実に遵守することが不可欠です。データ保護、特にGDPRの詳細については、産業の多くが既存の規制と施策にまだ精通していないため、明らかな理解が必要です。これは一般社会とのミスコミュニケーションにつながる可能性があります。そのため、コネクテッドモビリティや自律走行モビリティでは、自動的に取得されるデータの幅が膨大になるため、データ保護法が重要になります。

自動車ビッグデータ市場動向

製品開発、サプライチェーン、製造セグメントが主要シェアを占める

- ビッグデータは、技術主導の現代企業環境において、製造業者の生産性と効率性を高める重要な原動力の1つです。センサやコネクテッドデバイスの急速な導入、マシンツーマシン(M2M)通信の促進により、自動車産業のデータポイント数は大幅に増加しています。

- 自動車産業は、製造、マーケティング、サプライチェーンなどのセグメントでデータ分析を採用することで大きく前進してきたが、製品自体でのデータ生成と分析の活用は比較的初期段階にとどまっていました。しかし、モノのインターネット(IoT)の普及とコンピューティングの進歩により、より費用対効果の高いデータ収集方法が登場し始めています。

- コネクテッドカーによって、ユーザーエクスペリエンスが大きく変わる可能性があります。AP通信によると、2023年までに、自動車産業によって世界中で7,630万台のコネクテッドカーが生産されると予測されています。ギアとソフトウェアを提供することで、それらをクラウドに接続し、データを生成して有用な洞察を得ることができます。自動車会社がリアルタイムの路上データにアクセスできるようになれば、製品開発がスピードアップし、性能のモニタリング、製品品質の維持、安全性の確保に革命をもたらす可能性があります。

- アメリカ最大の自動車メーカーであるGeneral Motorsは、自動車セグメントにおけるビッグデータと分析の活用におけるパイオニアです。最近では、自動車にセンサと中央処理装置(CPU)を搭載するのが普通になっています。自動車内のセンサとテレマティクスを中心に据えることで、General Motorsは自動車の安全性と信頼性を向上させながら、多くのコストを削減することができます。例えばDataFlairは、テレマティクスは車両1台当たり最大800米ドルの大幅な節約を実現するため、金鉱のようなものだと主張しています。

アジア太平洋セグメントは予測期間中に大きな成長が見込まれる

- 全地域の中でアジア太平洋が最も人口が多いです。アジア太平洋は、都市人口の増加と購買力の上昇により、自動車産業にとって最大の市場のひとつとみなされています。

- 中国汽車工業協会(CAAM)によると、2022年4月に中国で販売された乗用車は約96万5,000台、商用車は約21万6,000台で、この数字は前月からそれぞれ48%、42%減少しています。このような大規模な自動車販売は、調査中のセクタにとって成長機会となることが予想されます。

- 各企業は、市場シェアを拡大し、多様な市場に参入し、提供する製品を多様化するために、多くのセグメントで存在感を高めようと協力しています。例えば、2022年6月、Nippon Telegraph & Telephone(NTT)とToyota Motorは、データを収集・共有するコネクテッドカーの開発で協力しました。NTTのデータネットワークデータ部門の最高経営責任者である本間陽氏は、海外市場への進出を急ぐため、M&Aを積極的に検討するとインタビューで述べました。本間氏によると、同社は今後4年間で4,000億円(30億米ドル)もの取引を行う可能性があるといいます。

- 例えば、SG Holdings Co.傘下のSagawa Express Co.は、すべての小型配送バンを電動化するという目標の一環として、2021年6月に同社初の電気自動車のプロトタイプを初公開しました。この車両は東京のスタートアップ企業ASFと共同で製作されました。国内最大の宅配サービスは、2030年までに電気自動車に切り替え、年間2万8,000トンのCO2排出量を削減する意向です。このような変化により、研究対象市場の拡大が可能になるはずです。

自動車産業におけるビッグデータ概要

自動車産業におけるビッグデータ市場は競争が激しく、多くの世界と地域参入企業で構成されています。これらの参入企業はかなりの市場シェアを占めており、顧客基盤の拡大に注力しています。これらのベンダーは、予測期間中に競合を獲得するために、研究開発活動、戦略的パートナーシップ、その他の有機的・無機的成長戦略に注力しています。

2022年3月、National Instruments Corporation(NIC)によるハインツィンガーGmbHの電子車両システム部門の買収が公表されました。この買収により、NICは電動化、バッテリー検査、持続可能エネルギーに関する能力を高めると同時に、顧客基盤を拡大することになります。自動車産業のコンポーネントのテストに関しては、NIとハインジンガーは互いに極めて補完的な役割を担っています。これにより、自動車の電動化とビジョン・ゼロの達成に向けた迅速なイノベーションが可能になります。

2022年1月、北米での足跡を増やすため、Reply SpAは、SAP技術によるソリューションのアドバイスと構築を専門とするEnowa LLCの買収を発表しました。エノワLLCはSAPの技術を活用し、付加価値サービスやクラウドデザインを提供しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の産業への影響評価

第5章 市場力学

- 市場の促進要因

- 様々な利害関係者による車両生成データ活用への取り組みの増加

- コネクテッドカーの設置台数の増加

- 市場課題

- プライバシー問題と車両データ保護に関する規制

第6章 市場セグメンテーション

- 用途別

- 製品開発、サプライチェーン、製造

- OEM保証、アフターセールス/ディーラー

- コネクテッドカーとインテリジェント輸送

- 販売、マーケティング、その他の用途

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- N-iX LTD

- Future Processing Sp.z.o.o

- Reply SpA(Data Reply)

- Phocas Ltd

- Positive Thinking Company

- Qburst Technologies Private Limited

- Monixo SAS

- Allerin Tech Private Limited

- Driver Design Studio Limited

- Sight Machine Inc.

- SAS Institute Inc.

- IBM Corporation

- SAP SE

- Microsoft Corporation

- National Instruments Corp.

第8章 投資分析

第9章 市場機会と今後の動向

目次

The Big Data Market In The Automotive Industry is expected to grow from USD 6.91 billion in 2025 to USD 15.02 billion by 2030, at a CAGR of 16.78% during the forecast period (2025-2030).

The automobile industry is being transformed by adopting technologies, applications, and services ranging from sensors to artificial intelligence to big data analysis; thus, the ecosystem is witnessing a steady influx of new players, resulting in the continuous evolution of the future car. Increasing efforts from various stakeholders in utilizing the vehicle-generated data coupled with a growing installed base of connected cars drive the market growth.

Key Highlights

- Big data analytics allows the automobile manufacturing industry to collect data from ERP systems to combine information from multiple functional units of the business and the supply chain members. With the emergence of industry IoT, a networked system, and M2M communication, the automotive industry is positioning itself toward industry 4.0. Sensors, RFIDs, barcode readers, and robots are now standard on the industry's manufacturing floor. These devices have increased data generation points exponentially.

- The consumer electronics industry is highly dependent on the demand and supply factors. The use of big data analytics helped this industry segment drastically and allowed it to switch to a pull market strategy instead of the push market strategy. With big data analytics, the industry is now more aware of consumer behavior patterns and may plan production based on these. A similar potential has been exposed in the automotive sector, with IoT evolutions and electronics components becoming an integral part of automobiles.

- Furthermore, big data analytics helped automobile manufacturers boost their efficiency in terms of sales and marketing. It also improved its operations by aiding in the incorporation of utilities like predictive maintenance and service schedule. It also aided automotive vendors in streamlining the procurement process, making it more cost-efficient by analyzing the data for demand prediction.

- Data is increasingly becoming crucial for OEMs. Therefore, it is essential to ensure that they comply with the General Data Protection Regulation (GDPR) through a strong privacy strategy. An evident appreciation for data protection, and in particular the details of the GDPR, are required, as many in the industry are not yet familiar with existing regulations and internal policies. This may lead to miscommunication with the public. Therefore, data protection law is important in connected and autonomous mobility because the breadth of data captured automatically is tremendous.

Big Data in Automotive Market Trends

Product Development, Supply Chain and Manufacturing Segment Accounts for a Major Share

- Big data is one of the key drivers of productivity and efficiency for manufacturers in the contemporary technology-driven corporate climate. There has been a significant increase in the number of data points for the automobile industry due to the rapid adoption of sensors and connected devices, as well as the facilitation of machine-to-machine (M2M) communication.

- While the car industry has made significant strides in adopting data analytics in areas such as manufacturing, marketing, and supply chain, the utilization of data generation and analysis within the product itself has been relatively nascent. However, with the increasing popularity of the Internet of Things (IoT) and advancements in computing, more cost-effective data collection methods are beginning to emerge.

- A significant change in the user experience may result from connected automobiles. According to the Associated Press, by 2023, it is predicted that 76.3 million connected cars will be produced worldwide by the automobile industry. By offering gear and software, you can connect them to the cloud so they can generate data and gain useful insight. When automotive companies get access to real-time, on-the-road data, it speeds up product development and may revolutionize how they monitor performance, maintain product quality, and ensure safety.

- The largest American automaker, General Motors, was a pioneer in the use of big data and analytics in the automotive sector. These days, sensors and central processing units (CPUs) in cars are the norm. With sensors and telematics within the automobile as its focus, General Motors can save a lot of money while also improving the safety and dependability of its vehicles. For instance, DataFlair claims that telematics is like a gold mine because it offers significant savings of up to USD 800 per vehicle.

Asia Pacific Segment is Expected to Grow at a Significant Rate Over the Forecast Period

- Of all the regions, the Asia-Pacific has the largest population. Asia-Pacific is regarded as one of the biggest markets for the automotive industry due to the region's growing urban population and rising purchasing power.

- Around 965,000 passenger cars and 216,000 commercial vehicles were sold in China in April 2022, according to the China Association of Automobile Manufacturers (CAAM); these figures reflect a 48% and a 42% reduction, respectively, from the previous month. Such massive vehicle sales are anticipated to present a growth opportunity for the sector under investigation.

- Businesses are working together to grow their presence in numerous areas to increase their market share, penetrate diverse markets, and diversify their product offerings. For instance, in June 2022, Nippon Telegraph & Telephone (NTT) and Toyota Motor collaborated to develop connected cars to collect and share data. Yo Honma, the chief executive of NTT's data networking and data division, stated in an interview that the business would actively investigate mergers and acquisitions to hasten its drive into foreign markets. According to Honma, the company could spend as much as JPY 400 billion (USD 3 billion) on deals over the next four years.

- For instance, Sagawa Express Co. of SG Holdings Co. debuted a prototype of its first electric vehicle in June 2021 as part of its goal to electrify all small delivery vans. This vehicle was constructed in collaboration with the Tokyo startup ASF. The biggest delivery service in the country intends to switch to electric vehicles by 2030 and reduce its CO2 emissions by 28,000 tonnes yearly. These changes should make it possible for the market under study to expand.

Big Data in Automotive Industry Overview

The big data market in the automotive industry is competitive and consists of many global and regional players. These players account for a considerable market share and focus on expanding their customer base. These vendors focus on research and development activities, strategic partnerships, and other organic and inorganic growth strategies to earn a competitive edge over the forecast period.

In March 2022, the purchase of Heinzinger GmbH's electronic vehicle systems division by National Instruments Corporation (NIC) was made public. The acquisition would increase NIC's capacity for electrification, battery testing, and sustainable energy while increasing its customer base. When it comes to testing automotive industry components, NI and Heinzinger play roles that are extremely complementary to one another. This allows for quick innovation to electrify vehicles and achieve vision zero.

In January 2022, to increase its footprint in North America, Reply SpA announced the acquisition of Enowa LLC, a business that specializes in advising and building solutions based on SAP technology. Enowa LLC uses SAP technology to provide value-added services and cloud design.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Efforts from Various Stakeholders in Utilizing the Vehicle Generated Data

- 5.1.2 Growing Installed-Base of Connected Cars

- 5.2 Market Challenges

- 5.2.1 Privacy Issues and Regulations on Vehicle Data Protection

6 MARKET SEGMENTATION

- 6.1 By Application

- 6.1.1 Product Development, Supply Chain and Manufacturing

- 6.1.2 OEM Warranty and Aftersales/Dealers

- 6.1.3 Connected Vehicle and Intelligent Transportation

- 6.1.4 Sales, Marketing and Other Applications

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia

- 6.2.4 Australia and New Zealand

- 6.2.5 Latin America

- 6.2.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 N-iX LTD

- 7.1.2 Future Processing Sp.z.o.o

- 7.1.3 Reply SpA (Data Reply)

- 7.1.4 Phocas Ltd

- 7.1.5 Positive Thinking Company

- 7.1.6 Qburst Technologies Private Limited

- 7.1.7 Monixo SAS

- 7.1.8 Allerin Tech Private Limited

- 7.1.9 Driver Design Studio Limited

- 7.1.10 Sight Machine Inc.

- 7.1.11 SAS Institute Inc.

- 7.1.12 IBM Corporation

- 7.1.13 SAP SE

- 7.1.14 Microsoft Corporation

- 7.1.15 National Instruments Corp.

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日