|

市場調査レポート

商品コード

1940695

データセンター用発電機:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Data Center Generator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| データセンター用発電機:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

概要

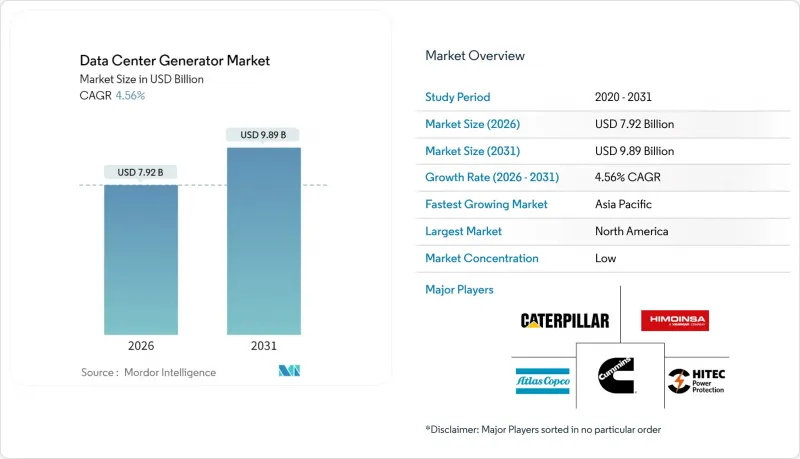

2026年のデータセンター用発電機市場規模は79億2,000万米ドルと推定され、2025年の75億7,000万米ドルから成長し、2031年には98億9,000万米ドルに達すると予測されています。

2026年から2031年にかけてCAGR4.56%で拡大する見込みです。

この着実な成長は、ハイパースケール施設の急増と、ラック密度をメガワット級に押し上げる新たな人工知能クラスターの波に起因しており、バックアップ電源設計を根本的に変革しています。ディーゼルユニットは依然として大半の設置基盤を担っていますが、炭素削減政策、変動する燃料価格、より厳格なTier 4規制により、天然ガス、水素、HVO対応プラットフォームへの関心が加速しています。大口径エンジンの供給網不足により納期が長期化する中、事業者様は複数年にわたる枠組み契約の締結や、地域組立拠点から出荷されるモジュラーブロックへの転換を進めております。一方、銅価格の過去最高値更新が発電機製造コストを圧迫し、OEMメーカーは垂直統合の動きを強化するとともに、技術要件が許容する範囲でアルミ巻線の採用を拡大しております。競合圧力は純粋な馬力から、燃料柔軟性、排出規制適合性、予測保全分析による発電機の稼働保証を伴うデジタルサービス提供といった幅広い要素へと移行しています。

世界のデータセンター発電機市場の動向と洞察

急増するハイパースケールおよびコロケーション施設の建設

ハイパースケールプロジェクトは現在、100MWを超えることが常態化しており、事業者は数十台の2.5MWユニットを集約し、停電時でも稼働時間を保証するN+2構成のリングを構築せざるを得ません。2024年にはGoogleがシンガポールの容量を35%増強するため50億米ドルを計上し、これは150MW以上の追加予備発電容量に相当します。コロケーション専門企業も同様の規模で展開しており、プリンストン・デジタル・グループがマレーシアに建設中の150MWキャンパスでは、負荷遮断シーケンスを効率化するため並列開閉装置を配置しています。契約形態では、発電機の供給・試運転・長期保守を一括提供するケースが増加しており、これによりリードタイムリスクと価格変動の抑制を図っています。ハイパースケール施設の建設需要が拡大する中、OEM各社は物流ボトルネックの解消と国内調達優遇措置への対応を目的に、東南アジアや米国中西部における現地組立拠点を強化しています。

AIワークロードによるラック電力密度の増加

1 MWもの電力を消費するGPUを多数搭載したラックは、従来の発電機群の安全マージンを圧迫し、容量の再評価や全面的な交換を必要としています。カミンズは、2025年第1四半期のパワーシステム事業の収益が19%増加したことを発表し、その要因はAIによるデータセンターの受注増であると述べています。事業者たちは、電圧低下に耐えられない何千もの相互接続されたアクセラレータを保護するために、より厳格な電圧調整帯域と10秒未満の動的応答時間を指定するようになっています。そのため、発電機スキッドには、より大型のオルタネーター、アクティブ高調波フィルタ、および高くなった固定子の熱を放散する液冷回路が組み込まれています。また、ファームウェアのアップグレードにより、フライホイールUPSバッファとのリアルタイム同期が可能になり、グリッドでイベントが発生した場合でもシームレスな移行が保証されます。

ディーゼル発電機を対象とした炭素排出規制

カリフォルニア州大気資源局は非緊急時の稼働時間を制限し、リアルタイム監視を義務付けるため、事業者は高価なSCR(選択的触媒還元)装置や微粒子フィルタースタックの設置を余儀なくされています。欧州連合では産業排出指令により許可審査が厳格化され、ディーゼル依存度の高いキャンパスでは承認が最大14ヶ月遅延しています。排気後処理部品はエンジン稼働時間15,000時間ごとに交換が必要なため、規制対応によりライフサイクル所有コストが増加します。一部のキャンパスでは規制の緩い地域へ予備発電設備を移転する対応を取る一方、この戦略は遅延に敏感なユーザー要求と衝突し、OEMメーカーに対しクリーン燃焼技術やハイブリッドソリューションの革新を迫る圧力となっています。

セグメント分析

2025年の需要の81.25%をディーゼル発電機が占めておりますが、事業者が炭素負債を財務面で定量化するにつれ、その成長余地は頭打ちとなっております。より厳しい割当量が確定する2028年以降は、ディーゼルソリューション向けデータセンター発電機市場規模は小幅な拡大の後、横ばい状態になると予測されます。水素およびHVO対応プラットフォームは、小規模な基盤からのスタートながら、即時ドロップイン互換性と政府の税制優遇策に後押しされ、突出した成長を示しています。欧州のガス網で1%混合が普及するにつれ、水素対応ユニットのデータセンター発電機市場シェアは着実に上昇すると予測されます。

規制上の優遇措置がさらに勢いを加速させております。ドイツの資金枠494では、5億5,000万ユーロがグリーンバックアップ電源の改修に充てられ、メタン・水素混合燃料に自動調整するデュアル燃料エンジンへの発注を促進しております。同時に、ハイパースケーラー企業は2030年までの価格可視性を確保するため、再生可能ディーゼルの購入契約を締結しています。メーカーは燃料特性変化時に噴射マップを再調整する無線ファームウェア更新で対応し、エンジン寿命の延長とバイオディーゼル汚染による保証保護を実現しています。ディーゼルはエネルギー密度と普遍的な入手可能性から依然重要ですが、代替燃料がイノベーションの注目を集めています。

1MW未満のユニットが依然として主流を占めております。これは数千に及ぶ小規模エッジサイトがローカルコンテンツ配信を保証する必要があるためです。しかしながら、ハイパースケール事業の合理化が進む中、2MWを超える単一ブロック定格への需要が加速しております。データセンター発電機市場における2MW超セグメントは年率13.78%の複合成長が見込まれ、2031年までに長らく首位を維持してきた1MW未満セグメントにほぼ匹敵する規模に達すると予測されております。事業者様はこの大型フレームを好まれます。エンジン数が少ないため燃料物流が簡素化され、予備部品在庫が削減され、設置面積が縮小されるからです。これは沿岸部の光ファイバー陸揚げ地点付近の高コスト区画において重要な考慮事項となります。

OEMメーカーは、配電盤や制御装置を工場出荷時に配線済みのモジュール式受入試験ブースを導入し、現場での試運転期間を10日未満に短縮することで、サプライチェーンの混雑対策に取り組んでいます。レンタルフリート提供者は同時に1~2MWクラスのポートフォリオを拡大し、納期ギャップを埋めています。契約には恒久設備の出荷後に購入オプションが付帯する場合が多く、こうした柔軟なモデルにより資本予算の予測可能性が保たれ、設定期日までにラック準備を約束するコロケーション契約における遅延ペナルティから守られます。

データセンター発電機市場は、製品タイプ(ディーゼル、天然ガス、水素・HVO対応、その他)、容量(1MW未満、1-2MW、2MW超)、ティアタイプ(Tier I/II、Tier III、Tier IV)、データセンタータイプ(ハイパースケール、エンタープライズ、コロケーション)、地域別に分類されます。市場予測は金額(米ドル)ベースで提供されます。

地域別分析

北米は、バージニア州北部、ダラス、フェニックスにおける高密度データセンター回廊の強みを背景に、2025年の収益の40.55%を占めました。投資は現在、新規用地取得ではなく電力密度の向上に重点が置かれており、事業者は老朽化した2MWディーゼル発電機を3.5MWのTier 4-Finalモデルに交換することで、壁を拡張せずにホワイトスペースを確保しています。水素およびバイオガスに対する連邦生産税額控除は、低炭素発電機への切り替えをさらに促進しています。

アジア太平洋地域は2031年までCAGR10.42%と最も強い勢いを見せております。シンガポールは効率性向上を条件にデータセンター許可のモラトリアムを解除し、5プロジェクト合計300MWの計画を推進中です。インドの「デジタル個人データ保護法」は国内クラウド構築を促進し、ムンバイだけで700MWの新規IT負荷が計画されています。日本ではソフトバンクの北海道キャンパス(300MW)が水力発電を基盤としたグリッドを統合しつつも、地震関連の停電対策としてデュアル燃料バックアップを規定しています。一方、マレーシアとインドネシアは、ハイパースケーラー向けに土地譲与や再生可能エネルギー証明書を提供することで、コスト競争力のある拠点として台頭しています。欧州は絶対額では3位ながら、持続可能性要件では主導的立場にあります。アムステルダム市はディーゼル稼働時間に上限を設け、年間500トン超のCO2排出量に課税することで、事業者に対しガスエンジンやバッテリーハイブリッドへの移行を促しています。ダブリンの送電容量逼迫は開発業者をスペインやポルトガルへ押しやり、発電需要を南方に再配分する結果となっています。中東地域は豊富な天然ガスと太陽光資源を活用しています。ドバイのデジタルパークでは、廃熱を地域冷房システムに再利用する吸収式冷凍機を備えたガス発電機を設置しています。アフリカは依然として初期段階ながら有望であり、ナイロビとラゴスでは不安定な電力網を克服するため、400kVAディーゼル発電機を備えたマイクロモジュラー型データセンターを導入しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 急増するハイパースケールおよびコロケーション施設の建設

- AIワークロードによるラック電力密度の増加

- 新興市場におけるエッジデータセンターの拡大

- 持続可能性のための天然ガスおよびHVO発電機への移行

- トレーラー搭載型仮設発電機群の導入

- モジュラー型マイクログリッド対応発電ユニットの採用

- 市場抑制要因

- ディーゼル発電機を対象とした炭素排出規制

- バッテリーおよび燃料電池代替技術への移行

- 高出力エンジンのサプライチェーンにおけるボトルネック

- 騒音および大気質に関する都市部での許可取得の障壁

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

第5章 市場規模と成長予測

- 製品タイプ別

- ディーゼル

- 天然ガス

- 水素およびHVO対応

- その他の製品タイプ

- 容量別

- 1MW未満

- 1~2MW

- 2MW超

- ティアタイプ別

- ティアIおよびII

- ティアIII

- ティアIV

- データセンタータイプ別

- ハイパースケール(自社所有およびリース)

- エンタープライズ(オンプレミス)

- コロケーション

- 地域別

- 北米

- 南米

- 欧州

- アジア太平洋地域

- 中東・アフリカ

第6章 競合情勢

- 市場シェア分析

- 企業プロファイル

- Caterpillar Inc.

- Cummins Inc.

- Generac Power Systems Inc.

- Rolls-Royce plc(mtu Solutions)

- Kohler Co.

- Mitsubishi Heavy Industries Group

- Atlas Copco AB

- Himoinsa SL

- Aksa Power Generation

- HITEC Power Protection BV

- INNIO Group(Jenbacher/Waukesha)

- Aggreko Ltd.

- Wartsila Corp.

- ABB Ltd.

- Doosan Enerbility Co., Ltd.

- FG Wilson

- Yanmar Holdings Co., Ltd.

- Perkins Engines Co. Ltd.

- Briggs & Stratton LLC

- Baudouin(Weichai)

- HIPOWER SYSTEMS

- GE Vernova