|

市場調査レポート

商品コード

1910905

医薬品用プラスチック包装:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Pharmaceutical Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 医薬品用プラスチック包装:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 132 Pages

納期: 2~3営業日

|

概要

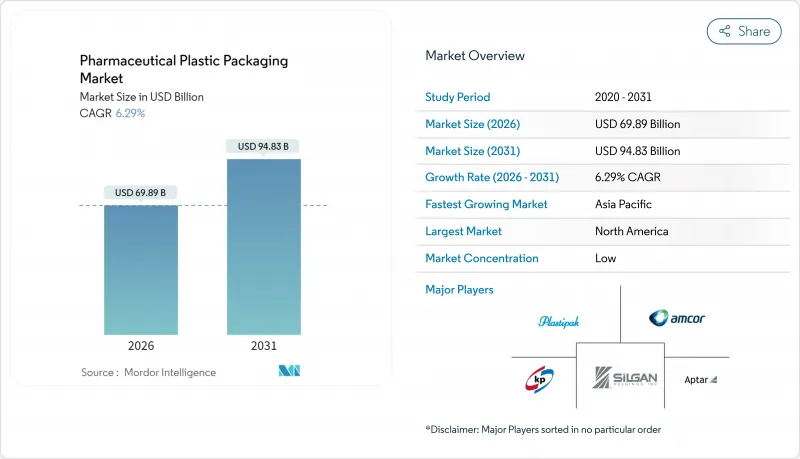

医薬品用プラスチック包装市場は、2025年の657億5,000万米ドルから2026年には698億9,000万米ドルへ成長し、2026年から2031年にかけてCAGR6.29%で推移し、2031年には948億3,000万米ドルに達すると予測されております。

成長の背景には、バイオ医薬品や注射剤のシェア拡大、より厳格なトレーサビリティ規制、リサイクル可能かつバイオベースのポリマーを推奨する持続可能性要件の急速な成熟化が挙げられます。2025年2月にはEUの包装・包装廃棄物規制(PPWR)が発効し、2030年までの完全リサイクル可能性を義務付け、材料代替プログラムを加速させています。北米の需要は、2025年11月の医薬品供給チェーン安全法(DSCSA)の期限により、スマートでシリアル化対応可能なフォーマットが推進される恩恵を受けています。アジア太平洋地域の製造業者は、規制の調和と急増するジェネリック医薬品の生産量を活用し、同地域の成長見通しを押し上げています。中堅コンバーター間の統合(例:アムコールによるベリー・世界のとの135億米ドル規模の合併)は、PFASフリーの配合や循環型経済への投資に取り組むための規模をもたらしています。

世界の医薬品用プラスチック包装市場の動向と展望

バイオ医薬品および注射剤向けプラスチック包装の需要拡大

新規承認医薬品に占めるバイオ医薬品の割合が増加しており、アルカリ溶出、剥離、破損に対する感受性から、高度なポリマーが優先的な一次容器として位置づけられています。ゲレスハイマー社のシクロオレフィンポリマー製注射器は、ガラスのような透明性と優れた耐破損性を兼ね備え、高価な生物学的製剤の損失を最小限に抑えます。世界のバイオ医薬品市場は2030年までに8,561億米ドルに達すると予測されており、高信頼性注射剤包装への需要を後押ししています。バリデーション済みのブロー・フィル・シール容器は、モノクローナル抗体において9ヶ月間にわたる効力やpHのドリフトを示さず、無菌用途におけるポリマーの採用範囲を拡大しています。パンデミック期間中、ガラスバイアルの不足がサプライチェーンのリスクを浮き彫りにし、同等の規制承認を得たプラスチック製容器を優先するデュアルソーシング政策を促しました。

新興市場におけるジェネリック医薬品生産の拡大

中国における規制改革、特に販売承認保持者制度の導入により承認サイクルが短縮され、受託製造提携が促進され包装需要が増加しています。北京が発表した2025年指針には、2027年までの医薬品監視体制近代化に向けた24の施策が盛り込まれており、適合包装ラインの明確な目標が設定されています。インドとASEANの相互承認プログラムにより規格調和がさらに進み、コンバーターは単一設計を複数市場で展開可能となりました。価格に敏感なジェネリック医薬品では、長距離輸出輸送中も堅牢性を維持するコスト効率の高いプラスチックも優先されます。

拡大プラスチック廃棄物規制(EU SUP、EPR等)

PPWR(プラスチック廃棄物規制)は、2030年までにEUで販売される全ての包装材のリサイクル義務化を規定し、EPR(拡大生産者責任)費用と再生材含有率基準(PET食品包装は30%以上)を導入し、資本負担とコンプライアンス負担を増加させます。医薬品容器については医療分野の例外規定がありますが、ブランド所有者は依然として回収スキームへの資金提供、多層ラミネートの再設計、2026年までに接触材料におけるPFASの段階的廃止が求められます。2028年に導入予定の統一シンボルはアートワークの変更を必要とし、5%の材料削減目標は既に薄肉化された壁厚仕様にさらなる圧迫を与えます。

セグメント分析

ポリプロピレンは、滅菌耐性と規制対応の既知性により、2025年時点で医薬品プラスチック包装市場の30.12%を占め主導的地位を維持しました。しかしながら、バイオベースおよび再生グレードは9.05%のCAGRで既存素材を凌駕し、2031年までに医薬品プラスチック包装市場を再構築する見込みです。アビエント社のメボピュア製品群は、ISO 10993およびUSP VI認証を維持しつつ最大120%のカーボンフットプリント削減を実現し、循環性とコンプライアンスの共存を実証しています。EUの再生材含有率義務化やFDAの染料使用禁止方針により、再生原料の需要が加速。UPM社の木材由来ボトル発売は、リグニン豊富な化学技術の商業的実現性を裏付けています。

第二世代バイオポリオレフィンと化学的再生PETは医薬品グレードの純度に到達し、設備変更なしでの直接置換を可能にしております。しかしながら、医薬品グレード再生材の供給が限られているため、即時的な規模拡大は抑制され、価格プレミアムが生じております。樹脂大手は物流短縮のため欧州・北米拠点近郊で生産能力を拡大する一方、アジア企業は急増する受注獲得に向け輸出向け再生樹脂認証の取得を模索しています。これにより医薬品プラスチック包装市場は、従来型ポリプロピレン(PP)の優位性と、PPWR(プラスチック包装再生利用)や企業のネットゼロ公約に沿った再生可能ポリマーの慎重ながら加速する浸透との均衡が図られています。

2025年時点では、経口固形製剤の普及により、ボトルおよび固形容器が医薬品プラスチック包装市場の26.05%を占めました。しかしながら、プレフィルドシリンジおよびカートリッジが成長の主役であり、バイオ医薬品、GLP-1注射剤、在宅投与薬の普及に伴い、CAGR年平均8.29%で拡大しています。BD社のRFID対応iDFillシリンジはデバイスと包装を一体化し、DSCSA(医薬品安全追跡法)の要件に適合するリアルタイム追跡性を提供します。

デジタル接続性、高粘度耐性、体内注入器との互換性により、これらの容器は汎用品から高付加価値のエンジニアリングシステムへと進化しています。一方、バイアルやアンプルは病院調剤において依然として不可欠ですが、用量帯別バイオ医薬品では、充填・仕上げ工程を効率化するゲレスハイマー社のポリマー製EZ-fillスマートバイアルへの移行が進んでいます。スティックパック、サシェ、パウチは、郵便料金や緩衝材コストが硬質容器を不利にする遠隔薬局の郵送用包装材として、足場を固めつつあります。

地域別分析

北米は2025年時点で医薬品プラスチック包装市場の36.05%を占めており、先進的なGMPプラント、DSCSAシリアル化期限、リショアリング奨励策に支えられています。FDAガイダンスは連続製造とスマートセンサーを推奨しており、現地コンバーターは包装壁へのRFID埋め込みやPFASフリーフィルムの適格性評価を推進しています。輸入樹脂への関税は国内設備稼働率を向上させ、バイオベース原料への投資を促進し、地政学的ショックに脆弱なサプライチェーンを安定化させています。

欧州では規制の厳格さと持続可能性におけるリーダーシップが相まって、強固でありながら進化を続ける市場基盤が形成されています。PPWR(プラスチック包装規制)はリサイクル性、EPR(拡大生産者責任)費用、PFAS禁止を義務付け、地域コンバーターにおける研究開発予算を刺激する再設計を促します。使い捨てプラスチック指令の規制は単一素材ブリスターフィルムを促進し、各国のエコモジュレーション制度は低炭素フォーマットを奨励します。北欧およびDACH諸国は使用済み吸入器・注射器のパイロット回収制度を主導し、ポリプロピレンのクローズドループ経路を提供します。

アジア太平洋地域は2031年までに医薬品プラスチック包装市場で最高となるCAGR9.76%を達成します。中国は2025年行動計画の下で加速し、包装品質監査をICH Q9に整合させると同時にグリーン工場への資金提供を進めています。インドは薬局方試験とデジタルトレーサビリティを強化し、スマートラベル供給業者に機会を創出しています。ASEAN相互承認により数か月に及ぶ書類作業が削減され、輸出業者は加盟国間で適合包装を出荷できるようになりました。日本のEPR制度は医療用包装材にも拡大され、PCRグレードPP調達の促進要因となります。これらの追い風が相まって、アジア太平洋地域の発展途上国・成熟国を問わず、医薬品用プラスチック包装市場を強化しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- バイオ医薬品および注射剤向けプラスチック包装材の需要拡大

- 新興国におけるジェネリック医薬品生産の拡大

- 軽量で割れにくい物流上の優位性

- 在宅医療および電子商取引における単回投与単位の採用

- 個別化医療向けオンサイトBFSおよび3Dプリント金型

- 抗菌性/スマートポリマー対応包装材

- 市場抑制要因

- 拡大するプラスチック廃棄物規制(EUのSUP、EPR等)

- 揮発性ポリマー原料価格の変動性

- バイオロジック・グラスからCOPバイアルへの政策転換

- 医薬品グレードの再生樹脂供給不足

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の激しさ

- 地政学的シナリオの評価

第5章 市場規模と成長予測

- 原材料別

- ポリプロピレン(PP)

- ポリエチレンテレフタレート(PET)

- 高密度ポリエチレン(HDPE)

- 低密度ポリエチレン(LDPE)

- 環状オレフィン系ポリマー/コポリマー(COP/COC)

- バイオベースおよび再生プラスチック

- 製品タイプ別

- ボトルおよび固形容器

- バイアルおよびアンプル

- プレフィルドシリンジおよびカートリッジ

- ブリスター包装およびストリップ包装

- パウチ/ スティックパック/ サシェ

- キャップ、蓋、および蓋類

- IVバッグおよびフレキシブルバッグ

- 包装形態別

- 硬質

- 軟質

- 薬剤送達経路別

- 経口

- 注射剤/注射用

- 眼科/鼻科

- 局所的/経皮的

- エンドユーザー別

- 製薬メーカー

- 受託開発製造機関(CDMO)

- 病院および診療所

- 在宅医療環境

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリアおよびニュージーランド

- その他アジア太平洋

- 中東・アフリカ

- 中東

- アラブ首長国連邦

- サウジアラビア

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- エジプト

- その他アフリカ

- 中東

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Amcor PLC

- Gerresheimer AG

- AptarGroup Inc.

- West Pharmaceutical Services Inc.

- Klockner Pentaplast Group

- Comar LLC

- O.Berk Company LLC

- Pretium Packaging LLC

- Drug Plastics and Glass Co. Inc.

- Gil-Pack Ltd.

- Alpla Group

- Silgan Holdings Inc.

- Placon Corporation

- Sealed Air Corporation

- Plastipak Holdings