|

市場調査レポート

商品コード

1690726

南アジアおよび東南アジアの種子:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)South And Southeast Asia Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 南アジアおよび東南アジアの種子:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

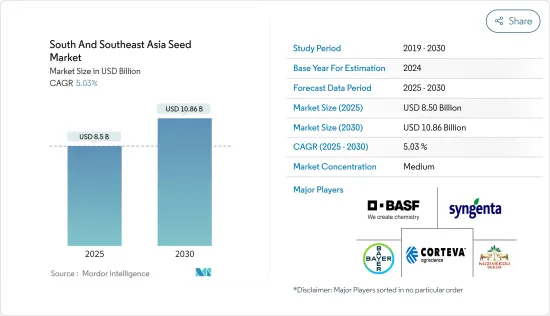

南アジアおよび東南アジアの種子市場規模は2025年に85億米ドルと推定され、予測期間(2025-2030年)のCAGRは5.03%で、2030年には108億6,000万米ドルに達すると予測されます。

種子の生産、認証、流通、コストは、南アジアおよび東南アジアの農業セクターの開発において重要な役割を果たしています。国際貿易は、輸送の遅れや不足、労働力不足、植物や種子の市場縮小のために苦しんでいます。農業部門、種子生産、貿易、国際協定の改善といったいくつかの要因が、種子技術の開発とともに、業界の成長の勢いを増しました。インド、タイ、インドネシア、ベトナム、フィリピン、バングラデシュの6カ国は、インデックス企業による生産、育種、加工活動がこれらの国に集中していることから、東南アジアにおける種子のハブとみなされています。非GM/ハイブリッド種子セグメントは、近年の食糧需要の増加により市場を独占しています。この需要の増加に対応するため、作物の収量向上が必要となっています。市場の主要企業は、Bayer Crop Science SE、Syngenta International AG、Corteva AgriScience、BASF SE、Nuziveedu Seeds Ltdなどです。

南アジアおよび東南アジアの種子市場動向

ハイブリッド種子の採用増加と政府支援

ハイブリッド作物の栽培意欲と関心は、調査対象国の多くで政府の法律と政策に大きく左右されます。パキスタンは、ハイブリッド作物および製品の生産国であると同時に輸入国でもあります。パキスタンの種子部門は、種子改正法2015と植物育種家権利法2018という2つの重要な規制に依存しています。2016年、パキスタン国民議会は、新しい植物品種の開発を奨励し、そのような品種の育種家の権利を保護するための植物育種家権利法を採択しました。この法律は、新品種の保護を規定すると同時に、農家が農場で保存した種子を保存、使用、交換、販売する権利を尊重しています。これにより農民は、工夫して生産された種子を使用するのと同時に、高品質のハイブリッド種子を入手することができます。ハイブリッド種子の輸入が増加しているのは、こうした措置の直接的な影響です。国会食糧安全保障・調査常任委員会は2019年、健康と環境の問題を理由にトウモロコシの遺伝子組み換え(GM)種子の輸入を禁止しました。これは、収穫量を一定に保つために、これらの遺伝子組み換え種子の代替としてハイブリッド種子を使用するための推進力として機能する可能性があります。

市場を独占する非GM/ハイブリッド種子セグメント

南アジアおよび東南アジア地域では、食糧需要が近年急激に増加しています。この需要を満たすため、安全基準を維持しながら作物の収量を増やすことが政府にとって必要となっています。フィリピンには国際稲研究所があり、増大する需要に対応するため、この地域でハイブリッド米種子を最も多く使用している国のひとつです。インドでは緑の革命によってハイブリッド種子の使用が促進されました。同国では人口が急速に増加しており、気候条件に適合した国産ハイブリッド種子の需要が高まっています。パキスタンに輸入されるハイブリッド種子は、国内で生産されるものより高価です。農民の所有地が限られているため、こうしたハイブリッド種子を購入する能力が低下しています。政府が開始した農業革新プログラムにより、農家によるハイブリッド・トウモロコシ種子の導入が進むと期待されています。これにより、国内のハイブリッド種子生産がさらに増加することが期待されます。南アジアや東南アジア地域では、有機製品に対する世界の需要の高まりや、同地域での作物収量向上の必要性から、ハイブリッド種子の使用が年々増加しています。この継続的な動向は、同地域のハイブリッド非遺伝子組み換え種子市場を押し上げると予想されます。

南アジアおよび東南アジアの種子産業の概要

南アジアおよび東南アジアの種子市場は、認証済み種子を販売する多数の地元企業が存在するため断片化されています。しかし、トウモロコシや野菜など、市場内で統合されている分野もあります。市場の主要企業は、Bayer Crop Science SE、Syngenta International AG、Corteva AgriScience、BASF SE、Nuziveedu Seeds Ltdなどです。さらに、著名企業による投資の増加が、種子市場の成長をさらに強めています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 作物タイプ

- 穀物・穀類

- 豆類と油糧種子

- 綿花

- 野菜

- その他の種子

- 製品タイプ

- 非GM/ハイブリッド種子

- GM種子

- 品種種子

- 植物成長調整剤

- 地域

- バングラデシュ

- パキスタン

- インド

- ネパール

- ベトナム

- インドネシア

- タイ

- ミャンマー

- フィリピン

- その他の南アジアおよび東南アジア

第6章 競合情勢

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- East-West Seed International Limited

- Bayer Crop Science

- Syngenta AG

- Alamgir Seed Company

- Rallis India Ltd

- Advanta Seeds(UPL)

- Nuziveedu Seeds Ltd

- Kaveri Seeds Co. Ltd

- Bioseed

- Evogene Seeds

第7章 市場機会と今後の動向

第8章 COVID-19が市場に与える影響

The South And Southeast Asia Seed Market size is estimated at USD 8.50 billion in 2025, and is expected to reach USD 10.86 billion by 2030, at a CAGR of 5.03% during the forecast period (2025-2030).

The production, certification, distribution, and cost of seeds, play a key role in developing the agricultural sector in South and Southeast Asian countries. International trade suffered due to slow or lack of transportation, labor shortages, and a contraction in the market for plants and seeds. Several factors, such as improvements in the agricultural sector, seed production, trade, and international agreements, along with the developments in seed technology, increased the momentum of the industry's growth. Six countries, namely India, Thailand, Indonesia, Vietnam, the Philippines, and Bangladesh, are considered seed hubs in Southeast Asia based on the concentration of production, breeding, and processing activities by index companies in these countries. The non-GM/hybrid seeds segment has dominated the market due to the increased demand for food over recent years. To meet this growing demand, crop yield enhancement has become a necessity. The major players in the market are Bayer Crop Science SE, Syngenta International AG, Corteva AgriScience, BASF SE, and Nuziveedu Seeds Ltd, among others.

South & South East Asia Seed Market Trends

Increasing Adoption of Hybrid Seeds and Government Support

The willingness and interest to grow hybrid crops are, to a large extent, governed by government legislation and policy in many of the countries studied. Pakistan is both a producer and importer of hybrid crops and products. The Pakistani seed sector is dependent on two key regulations, namely, the Seed Amendment Act 2015 and the Plant Breeders Rights Act 2018. In 2016, the Pakistan National Assembly adopted a Plant Breeders' Rights Act to encourage the development of new plant varieties and protect the rights of breeders of such varieties. The Act provides protection for new plant varieties while at the same time respecting the right of farmers to save, use, exchange, and sell farm-saved seeds. This ensures farmers get access to high-quality hybrid seeds alongside using ingeniously produced ones. The rising import of hybrid seeds is a direct impact of these measures. The National Assembly Standing Committee on National Food Security and Research banned the import of genetically modified (GM) seeds of maize owing to health and environmental issues in 2019. This may act as a driver for the use of hybrid seeds as an alternative to these GM seeds for keeping the yield constant.

Non-GM/Hybrid Seeds Segment Dominating the Market

In the South and Southeast Asian regions, the demand for food has increased exponentially over recent years. To meet this demand, crop yield enhancement has become a necessity for governments while maintaining safety standards. The Philippines is home to the International Rice Research Institute and is one of the most prolific users of hybrid rice seeds in the region to meet growing demand. The Green Revolution in India promoted the use of hybrid seeds in the country. The fast-growing population in the country has increased the demand for domestically produced hybrid seeds compatible with the climate conditions. Hybrid rice seeds imported to Pakistan are more expensive than those produced locally. The limited landholdings of farmers reduce their ability to purchase these hybrid seeds. The Agricultural Innovation Program launched by the government is expected to increase the adoption of hybrid maize seeds by farmers. This is expected to further increase the domestic hybrid seed production in the country. The use of hybrid seeds has been increasing over the years in the south and southeast Asian regions, with the increasing global demand for organic products and the need for enhanced crop yields in the region. This continued trend is expected to boost the market for hybrid-non-GMO seeds in the region.

South & South East Asia Seed Industry Overview

The South and Southeast Asian seed market is fragmented because of the presence of a large number of local players marketing certified seeds. However, there are segments within the market that are consolidated, such as maize and vegetables. The major players in the market are Bayer Crop Science SE, Syngenta International AG, Corteva AgriScience, BASF SE, and Nuziveedu Seeds Ltd, among others. Furthermore, increasing investments by prominent companies are further intensifying the growth of the seed market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Crop Type

- 5.1.1 Grains and Cereals

- 5.1.2 Pulses and Oilseeds

- 5.1.3 Cotton

- 5.1.4 Vegetables

- 5.1.5 Other Seeds

- 5.2 Product Type

- 5.2.1 Non-GM/Hybrid Seeds

- 5.2.2 GM Seeds

- 5.2.3 Varietal Seeds

- 5.2.4 Plant Growth Regulators

- 5.3 Geography

- 5.3.1 Bangladesh

- 5.3.2 Pakistan

- 5.3.3 India

- 5.3.4 Nepal

- 5.3.5 Vietnam

- 5.3.6 Indonesia

- 5.3.7 Thailand

- 5.3.8 Myanmar

- 5.3.9 Philippines

- 5.3.10 Rest of South and Southeast Asia

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 East-West Seed International Limited

- 6.3.2 Bayer Crop Science

- 6.3.3 Syngenta AG

- 6.3.4 Alamgir Seed Company

- 6.3.5 Rallis India Ltd

- 6.3.6 Advanta Seeds (UPL)

- 6.3.7 Nuziveedu Seeds Ltd

- 6.3.8 Kaveri Seeds Co. Ltd

- 6.3.9 Bioseed

- 6.3.10 Evogene Seeds