|

市場調査レポート

商品コード

1910894

欧州のREIT市場シェア分析、業界動向、統計、成長予測(2026年~2031年)Europe REIT - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のREIT市場シェア分析、業界動向、統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

概要

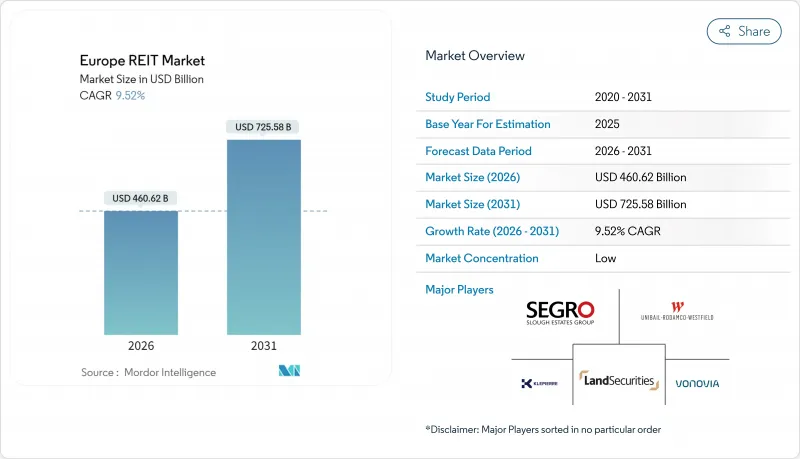

欧州のREIT市場は、2025年の4,206億米ドルから2026年には4,606億2,000万米ドルへ成長し、2026年から2031年にかけてCAGR9.52%で推移し、2031年までに7,255億8,000万米ドルに達すると予測されています。

この成長を後押しする6つの相互に関連する要因があります。欧州中央銀行(ECB)による慎重に段階的に進められた利下げサイクル下での抑制された借入コスト、インフレ調整後の利回りに対する機関投資家の強い需要、持続的な電子商取引物流需要、増加するデータセンターの建設、手頃な価格の住宅のための自治体パートナーシップの拡大、そしてELTIF 2.0などのEU全域での資本市場改革による支援です。2024年以降の借り換えコスト上昇は短期的な変動をもたらしましたが、十分な資本基盤を持つ投資事業体は、依然として20年平均を下回るスプレッドで借り換えを実施し、キャッシュフローのカバー率を保護するとともに分配金の可視性を維持しました。産業用資産やデータセンター資産へのセクターローテーションにより、小売やセカンダリーオフィスセグメントよりもキャップレートが急速に圧縮され、現在ではハイブリッドワークによる空室リスクが価格に織り込まれています。上場投資法人は、グリーン改修資金調達のためサステナビリティ連動債への依存度を高めており、これによりエネルギー性能規制はコスト負担から、テナントや投資家双方に対する競争上の差別化要因へと転換しつつあります。市場構造は依然として分散しており、主要企業の資本化シェアはわずか31%に留まっています。これは、より厳格な契約条件を負担できるスポンサーによる統合の余地が十分にあることを示しています。

欧州のREIT市場の動向と洞察

欧州中央銀行(ECB)の持続的な利下げ姿勢

欧州中央銀行(ECB)は2024年から2025年にかけて政策金利を50ベーシスポイント引き下げました。これにより、高格付けのREITは4%未満のクーポンで満期延長が可能となり、実質利回りを求める海外資本を引き続き惹きつけています。負債管理により加重平均債務満期は5年以上に延長され、予想される金融引き締めサイクル中のキャッシュフローを保護しています。大西洋を挟んだ金利差が相対的価値の魅力を高め、米国の年金基金は戦略的配分比率を引き上げました。ドイツのVonoviaはこの動向を体現し、有利なスプレッドで16億米ドルのシンジケートローンを調達、投資適格格付けを維持しました。インフレ期待が再び低下方向に定着した場合、キャリートレードが縮小し資金流入が減少する可能性がありますが、基本シナリオでは信用スプレッドが20年平均を下回る状態が続くと想定されています。その結果、資金調達の可視性が欧州のREIT市場全体の配当安定性を引き続き支えています。

Eコマース主導の物流拡張

欧州におけるオンライン販売の浸透率は2024年に小売売上高の16%に達し、実店舗型フォーマットと比較して倉庫需要を3倍に拡大させました。人口密集地から50キロ圏内のグレードA施設では、年間8%を超える賃料上昇率を示しており、総合消費者物価指数(CPI)を上回っています。セグロ社はこの動向を加速させ、ドイツとオランダで15区画のインフィル用地を取得し、配送半径を20分未満に短縮しました。開発計画は引き続き慎重に進められております。土地制約やゾーニング規制が投機的供給を抑制し、稼働率を97%以上で維持しているためです。EU関税同盟下の越境フルフィルメント基準は、高度な自動化を備えた広域ハブへの需要をさらに刺激しております。その結果、当面の間、物流は欧州のREIT市場の成長を支える基幹分野であり続けるでしょう。

ハイブリッドワークがオフィス稼働率に変化をもたらす

2025年までにオフィスの平均出勤率は2019年基準の65%前後で安定する見込みですが、中心業務地区(CBD)の優良タワーと郊外物件の稼働率格差は拡大しています。ランド・セキュリティーズのウエストエンド資産は待機リストを維持する一方、ロンドン郊外の二次的ブロックでは15%を超える構造的空室率に直面しています。テナントは健康増進設備や高効率換気システムを優先するため、オーナー側は初期利回りを低下させる資本集約的な内装工事を提供せざるを得ません。フレキシブルリース提供業者は一部リスクを吸収しますが、月単位契約はホストREITの収益変動要因となります。オフィス依存型投資商品は現在、複合用途やライフサイエンス施設への転換により存在意義を維持しています。適応戦略がなければ、オフィス資産の保有は欧州のREIT市場の総合成長率を引き続き圧迫するでしょう。

セグメント分析

産業用資産(その他の商業セクターに分類)は2025年に欧州のREIT市場シェアの24.86%を占め、消費拠点に近い電子商取引の物流ニーズが代替不可能であることを示しています。ドイツのライン・ルール回廊では賃料上昇率が前年比平均8%を記録し、キャップレート圧縮が4%未満の水準で持続しています。データセンター(その他商業部門)は最も高い成長率を示し、高密度電力供給を必要とするハイパースケール/エッジ展開を背景に、2031年までの予測CAGRは10.18%に達します。多様な投資手段ではラストマイル倉庫とマイクロデータハブを組み合わせ、消費支出サイクルに耐性のある複合収益構造を構築しています。住宅REITは24.73%の安定したシェアを維持しており、都市部の住宅供給不足とインフレヘッジとなる物価連動型賃貸借契約を活用しています。一方、小売店舗網は合理化が進み、体験型モールがレジャー施設からの波及効果で集客力を高め、従来型ショッピングセンターを上回る業績を上げています。このセクター間の優劣関係は、技術革新と人口動態の制約が欧州のREIT市場における資本配分をいかに形作っているかを示しています。

産業用不動産の優位性が持続する背景には、主要港湾近郊のブラウンフィールド用地が希少であるため、供給過剰による市場混乱が生じにくい点が挙げられます。セグロ社のクロスドッキング設計は平均配送時間を22分短縮し、厳しい納期を求められるテナントにとって確かな経済的優位性をもたらしています。データセンター分野では、デジタル・リアルティ社がブリュッセルとウィーンで相互接続ノードを拡充し、クロスコネクト料金を収益化することでEBITDAマージンを60%超に高めています。医療系REITは高齢化という基盤によりCAGR8.21%を記録し、エディフィカとコフィニモの合併により128億4,000万米ドル(120億ユーロ)規模の地域横断型リーダーが誕生しました。オフィス分野では二極化が進み、中心業務地区(CBD)の優良タワーは価格決定力を維持する一方、周辺ブロックでは代替用途の模索が続いています。各サブセクターの異なるキャッシュフローの周期性により、ポートフォリオマネージャーはリスク調整後のパフォーマンスを設計でき、欧州のREIT市場における高まる配当期待に応えることが可能です。

欧州のREITレポートは、エクスポージャーのセクター別(小売、工業、オフィス、住宅、多角化、その他セクター、データセンター、ヘルスケア)、時価総額別(大型株、中型株、小型株)、地域別(英国、ドイツ、フランス、スペイン、イタリア、ベネルクス、北欧諸国、その他欧州)に分類されています。市場予測は金額ベース(米ドル)で提供されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 持続的な低金利環境

- 電子商取引の加速が物流REITを後押し

- インフレヘッジ利回りを求める機関投資家の資金流入

- EU ELTIF 2.0資本に向けた規制の転換

- 注目度の低い動向:自治体支援による低所得者向け住宅供給義務

- 注目度の低い動向:トークン化された不動産二次市場

- 市場抑制要因

- 2024年以降の利上げに伴う借り換えコストの上昇

- ハイブリッド勤務がオフィス稼働率に圧力をかけている

- 注目されていない動向:自治体支援による低所得者向け住宅供給義務

- 注目度の低い動向:ESG連動型債務契約条項の強化

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- セクター別

- 商業用

- オフィス

- 小売り

- ホスピタリティ

- ヘルスケア

- その他の商業セクター

- 住宅用

- 商業用

- 時価総額別

- 大型株(100億米ドル以上)

- 中型株(20億~100億米ドル)

- 小型株(20億米ドル未満)

- 地域別

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ベネルクス

- ベルギー

- オランダ

- ルクセンブルク

- 北欧諸国

- デンマーク

- フィンランド

- アイスランド

- ノルウェー

- スウェーデン

- その他欧州

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Unibail-Rodamco-Westfield

- Segro plc

- Vonovia SE

- Land Securities Group plc

- Klepierre SA

- Merlin Properties

- Gecina SA

- Aroundtown SA

- Castellum AB

- LEG Immobilien SE

- Fabege AB

- Covivio SA

- Tritax Big Box REIT plc

- Hammerson plc

- Cofinimmo SA

- CPI Property Group

- Swiss Prime Site AG

- Shaftesbury Capital plc

- Aedifica SA

- Globalworth Real Estate Investments