|

市場調査レポート

商品コード

1690715

保険サードパーティアドミニストレーター(TPA):市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Insurance Third Party Administrators - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 保険サードパーティアドミニストレーター(TPA):市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

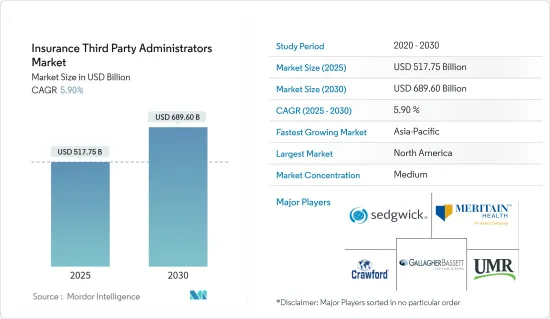

保険サードパーティアドミニストレーター(TPA)市場規模は2025年に5,177億5,000万米ドルと予測され、予測期間(2025-2030年)のCAGRは5.9%で、2030年には6,896億米ドルに達すると予測されます。

保険引受会社は、保険金請求事務のニーズに対応するために第三者機関(TPA)を利用しています。TPAの多くは、労災、財物、賠償責任に関連するリスクの一部を自己保証することを選択した大企業や中堅企業を相手にしています。また、歯科、健康保険などの福利厚生制度が自己資金で賄われている企業のクレーム管理も行っています。TPAの事業領域は、米国のような先進国市場で仲介役を務めた後、最終的に医療保険の引受保険会社に移行するものから、マレーシア、ベトナム、タイのような新興経済諸国でTPA/MBOが医師などの価格設定に圧倒的な影響力を持つものまで様々です。

ほとんどのTPAは追いつく必要があるが、保険ビジネスの進化するニーズに対応するために必要な労働力、テクノロジー、データ能力をまだ開発していないところもあります。米国のTPAの大半は、前年同期比の収益成長率が低下しています。この落ち込みは、伝染病の流行により今年に持ち越される可能性があります。TPAセクターは、キャリアのアウトソーシングやサービスの拡大など、いくつかの要因によって牽引されているが、いくつかの今後の課題によって開発の見通しは限定されています。保険ITプロバイダーやビジネス・プロセス・アウトソーシング・プロバイダーと比べて、TPAはデジタル主導の複雑でないユースケースを展開することが多いです。

保険サードパーティアドミニストレーター(TPA)の市場動向

ヘルスケア保険TPAの増加が市場を後押し

いくつかの要因により、医療保険TPAの需要は近年増加しています。主な理由の1つは、医療保険市場全体の成長です。健康保険への加入を希望する個人や企業が増えるにつれ、これらの保険契約を効率的かつ効果的に管理する必要性が高まっています。健康保険業界の複雑さもTPA市場の成長に寄与しています。テクノロジーの進歩もTPA市場の成長に大きな役割を果たしています。デジタル化と自動化により、管理業務の効率化と合理化が進みました。TPAはテクノロジーを活用して保険金請求を迅速に処理し、保険契約者にオンライン・サービスを提供し、保険会社にリアルタイム・レポートを作成します。このため、保険会社はこうした技術的進歩の導入を検討しており、TPAに対する需要はさらに高まっています。

北米で成長する保険サードパーティアドミニストレーター(TPA)市場

米国の保険サードパーティアドミニストレーター(TPA)業界は細分化が進んでおり、集中度は極めて低いです。競争の激化が米国のビジネスを苦しめている主な要因であるが、収益の変動が少ないことが主な要因です。米国では、基準年上半期現在、クレームアジャスターとして34万9,400人が働いています。消費者の可処分所得が増加するにつれて、住宅、自動車、その他保険を必要とする資産を購入します。一人当たりの可処分所得が増えれば、損害保険、傷害保険、医療保険、生命保険などの保険料をより高く支払えるようになるため、個人や世帯は保険を増やすことができます。

保険サードパーティアドミニストレーター(TPA)業界の概要

第三者保険管理者市場は適度に統合されています。本稿では、国際的なサードパーティ保険アドミニストレーターの概要が紹介されています。調査では、サービス、デジタル導入のレベル、適用される規則、本社、財務実績指標、全体的な利点と欠点に関する情報など、組織の詳細なプロファイルを提供しています。主要企業には、Sedgwick Claims Management Services Ltd、Crawford &Company、Maritain Health、UMR Inc.、Gallagher Bassett Services Inc.などがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 費用対効果の高いヘルスケアソリューションへの需要の高まり

- デジタル化と自動化の進展が市場を牽引

- 市場抑制要因

- データ漏洩とサイバーセキュリティ脅威の可能性

- 市場機会

- 専門サービスに対する需要の高まり

- 管理業務のアウトソーシング動向の高まりが大きなチャンスをもたらす

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- TPAにおけるデジタルの導入とその意義

- ビジネス・エコシステムを形成する規制状況

- COVID-19が市場に与える影響

第5章 市場セグメンテーション

- 保険タイプ別

- ヘルスケア保険

- 退職プラン

- 商業賠償責任保険

- その他保険タイプ(自動車保険)

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- その他欧州

- アジア太平洋

- 中国

- インド

- その他アジア太平洋地域

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- その他中東とアフリカ

- 世界のその他の地域(LATAM)

- 北米

第6章 競合情勢

- 市場集中の概要

- 企業プロファイル

- Sedgwick Claims Management Services Inc.

- UMR Inc.

- Crawford & Company

- Gallagher Bassett Services Inc.

- CorVel Corporation

- Helmsman Management Services LLC

- ESIS Inc.

- Healthscope Benefits

- Maritain Health*

第7章 市場機会と今後の動向

第8章 免責事項

The Insurance Third Party Administrators Market size is estimated at USD 517.75 billion in 2025, and is expected to reach USD 689.60 billion by 2030, at a CAGR of 5.9% during the forecast period (2025-2030).

Insurance underwriting companies use third-party administrators (TPAs) to handle claims administration needs. Many work with large or mid-sized businesses that have chosen to self-insure some of their risks related to workers' compensation, commercial property, and liability. In addition, they might handle claims administration for companies whose benefit plans-such as dental, health, or others are self-funded. The business scope of TPAs varies from developed markets like the United States, where they serve as an intermediary before eventually transitioning into an underwriter for health insurance, to developing economies like Malaysia, Vietnam, and Thailand, where TPAs/MBOs have a dominant hold on setting the price for doctors, etc.

Most TPAs need to catch up, but some have yet to develop the necessary workforce, technology, and data capabilities to meet the evolving needs of the insurance business. For the majority of TPAs in the United States, Y-o-Y revenue growth decreased. This drop can carry over into the current year due to the epidemic. The TPA sector is driven by several factors, including carrier outsourcing and service expansions, but several upcoming issues limit development prospects. Compared to insurance IT providers or business process outsourcing providers, TPAs often deploy less complex digital-led use cases.

Insurance Third Party Administrators Market Trends

Increasing Healthcare Insurance TPAs is Fuelling the Market

Due to several factors, the demand for health insurance TPAs has increased in recent years. One of the main reasons is the overall growth of the health insurance market. As more individuals and businesses seek health insurance coverage, there is a greater need for efficient and effective administration of these policies. The complexity of the health insurance industry has also contributed to the growth of the TPA market. The advancement of technology has also played a significant role in the growth of the TPA market. Digitalization and automation have made administrative tasks more efficient and streamlined. TPAs leverage technology to process claims faster, provide online services to policyholders, and generate real-time reports for insurance companies. This has further increased the demand for TPAs as insurance companies look to adopt these technological advancements.

Insurance Third-party Administrator Market is Growing in North America

The US insurance third-party administrators industry has high fragmentation and minimal concentration. Increased competition is the main element hurting the US business, although low revenue volatility is the main one helping it. In the United States, there were 349,400 positions as claims adjusters as of base year H1. As consumers' disposable income rises, they purchase homes, vehicles, and other assets that require insurance. Individuals and households can increase their coverage when per capita disposable income grows because higher per capita income allows them to pay better premiums for property, casualty, health, and life insurance.

Insurance Third Party Administrators Industry Overview

The third-party insurance administrator market is moderately consolidated. An overview of international third-party insurance administrators is provided in the paper. The research provides a detailed profile of the organizations, including information on their services, levels of digital adoption, rules that apply to them, their headquarters, financial performance measures, and overall benefits and drawbacks. Some of the major players include Sedgwick Claims Management Services Ltd, Crawford & Company, Maritain Health, UMR Inc., and Gallagher Bassett Services Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Cost Effective Healthcare Solutions

- 4.2.2 Rise in Digitalization and Automation is Driving the Market

- 4.3 Market Restraints

- 4.3.1 Potential for Data Breaches and Cybersecurity Threats

- 4.4 Market Oppotunities

- 4.4.1 Increasing Demand for Specialized Services

- 4.4.2 Growing Trend of Outsourcing Administrative Tasks Presents a Significant Opportunity

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Digital Adoption and its Significance in TPAs

- 4.7 Regulatory Landscape Shaping the Business Ecosystem

- 4.8 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Insurance Type

- 5.1.1 Healthcare Insurance

- 5.1.2 Retirement Plans

- 5.1.3 Commercial General Liability Insurance

- 5.1.4 Others Insurance Types (Motor Insurance)

- 5.2 By Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 Germany

- 5.2.2.3 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Rest of Asia-Pacific

- 5.2.4 Middle East and Africa

- 5.2.4.1 United Arab Emirates

- 5.2.4.2 Saudi Arabia

- 5.2.4.3 Rest of Middle East and Africa

- 5.2.5 Rest of the World (LATAM)

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Sedgwick Claims Management Services Inc.

- 6.2.2 UMR Inc.

- 6.2.3 Crawford & Company

- 6.2.4 Gallagher Bassett Services Inc.

- 6.2.5 CorVel Corporation

- 6.2.6 Helmsman Management Services LLC

- 6.2.7 ESIS Inc.

- 6.2.8 Healthscope Benefits

- 6.2.9 Maritain Health*