|

市場調査レポート

商品コード

1690703

ASEAN諸国のエネルギー貯蔵:市場シェア分析、産業動向、成長予測(2025年~2030年)ASEAN Energy Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ASEAN諸国のエネルギー貯蔵:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

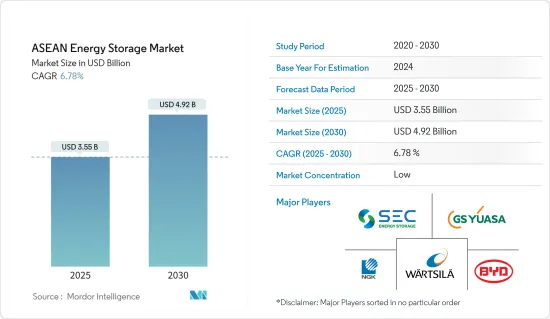

ASEAN諸国のエネルギー貯蔵市場規模は、2025年に35億5,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは6.78%で、2030年には49億2,000万米ドルに達すると予測されます。

2020年には、COVID-19パンデミックのため、カンボジア、インドネシア、ミャンマー、フィリピン、ベトナムという多くの発電プロジェクトが停止し、今後数年間は容量追加が予定より遅れる可能性が高いです。市場の主要促進要因としては、住宅、商業・工業の両セグメントにおける無停電電源装置に対する需要の高まりが挙げられます。しかし、ASEAN地域で大規模なエネルギー貯蔵施設を設置するには多額の資本が必要であることが、予測期間中の市場調査の主要抑制要因になると予想されます。

主要ハイライト

- 電気自動車市場の拡大と、住宅・商業部門の双方における無停電電力供給への需要の高まりにより、電池は予測期間中に市場で大きな成長を遂げる可能性が高いです。

- パリ協定に沿って、世界各国はエネルギーミックスにおける再生可能エネルギーの割合を増やす努力をしています。例えば、インドネシアは2050年までに再生可能エネルギーの比率を31%まで高める目標を掲げています。太陽光発電のような再生可能エネルギーの増加は、国の送電網にアクセスできない農村の孤立した送電網に電力を供給するため、近い将来、エネルギー貯蔵設備にとって好機となる可能性が高いです。

- フィリピンは2021年に最大の市場シェアを占め、予測期間中も同じ傾向が続くと予想されます。

ASEAN諸国のエネルギー貯蔵市場動向

著しい成長が期待されるバッテリーエネルギー貯蔵セグメント

- 電池エネルギー貯蔵システム(BESS)は、ASEAN諸国で急速に台頭している市場セグメントです。再生可能エネルギー消費の増加は、予測期間中のBESS需要を大きく押し上げると予想されます。しかし、リチウムイオン電池とBESS技術のコスト低下にもかかわらず、人為的に低く設定された関税水準と化石燃料補助金により、ASEAN諸国市場におけるBESS技術の競合力は低下すると予想されます。

- 2022年7月、エネルギー効率を高め、同国の港湾からの排出を削減するプロジェクトの一環として、シンガポールに大規模な電池システムが設置されました。2MW/2MWhのバッテリーエネルギー貯蔵システム(BESS)は、PSAシンガポールが運営する4つの主要施設の1つ、パシル・パンジャン・ターミナルに導入されました。これはスマートグリッド管理システムの一部でもあり、港湾業務のエネルギー効率を2.5%改善し、港湾の二酸化炭素排出量を年間1,000トン(CO2換算)削減することができます。

- ASEAN地域では、インドネシアの再生可能エネルギー設備容量が急速に増加しています。2022年には12481MWとなり、前年比8%増、2013年比では約51%増となります。2023年、トタル・エレンSAはインドネシアの電力会社PLNと提携し、70MWの風力発電所と10MWhの蓄電池を統合したタナ・ラウトプロジェクトを建設します。このようなプロジェクトの市場開拓が、予測期間におけるASEAN諸国のエネルギー貯蔵市場の成長を後押しすることは間違いないと考えられます。

- 同様に、2022年6月、シンガポールを拠点とするエネルギー都市開発グループのセンブコープは、ジュロン島で200MWhの蓄電池システムの建設を開始しました。シンガポールエネルギー市場庁(EMA)は5月、200MWと200MWhの蓄電池を建設するための関心表明書(EOI)を発行しました。

- したがって、上記の点から、バッテリーエネルギー貯蔵セグメントは予測期間中に大きく成長すると予想されます。

フィリピンが市場を独占する見込み

- 再生可能エネルギー発電は断続的な電源であるため、余剰発電のための蓄電が必要です。同国は、2030年までに再生可能エネルギーを発電構成の35%、2040年までに50%にすることを目標としており、これは2030年までに風力と太陽光で約15GWに相当します。フィリピンの2022年時点の再生可能エネルギー設備容量は約7670MWで、その大半は水力発電と地熱発電です。

- 再生可能エネルギープロジェクトへの投資は、同国のエネルギー貯蔵市場への道を開く可能性が高いです。2023年、フィリピンエネルギー省(DOE)は、政府が再生可能エネルギー資産の100%外国人所有を許可した1ヵ月後に、エネルギー貯蔵に関する新しい市場ルールと施策を考案しました。この改革を受け、中国企業グループはフィリピンの再生可能エネルギーとエネルギー部門に137億米ドルの投資を約束しました。

- 2022年、SN Aboitiz Power Group(SNAP)は、イサベラ州ラモンのマガット水力発電所に位置する容量20MWのBESSプロジェクトの最終投資決定を完了しました。同国では同様のプロジェクトが開発されており、ASEANにおけるエネルギー貯蔵市場の開拓に貢献すると考えられます。

- 2022年4月、フィリピンの投資家所有の電力会社AboitizPowerとノルウェーの再生可能エネルギーグループScatecは、20MW/20MWhの蓄電池システムを建設するためのEPC契約をHitachi Energyと締結し、2024年の稼動を目指しています。両社の合弁会社SNアボイティスパワーグループ(SNAP)は、フィリピン北部のイサベラ州ラモンにある360MWのマガット水力発電所において、バッテリー蓄電システム(BESS)プロジェクトの最終投資決定を行りました。

- 以上のことから、予測期間中、フィリピンがASEAN諸国のエネルギー貯蔵市場を独占すると予想されます。

ASEAN諸国のエネルギー貯蔵産業概要

ASEAN諸国のエネルギー貯蔵市場は適度にセグメント化されています。同市場の主要企業には、GS Yuasa Corporation、Wartsila Oyj Abp、BYD、SEC Battery Company、NGK Insulators Ltd.などがあります(順不同)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2028年までの市場規模と需要予測

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- 住宅、商業、工業用消費者からの電力需要の伸び

- 予定外の停電と送電網の不安定化によるエネルギー貯蔵ソリューションの需要増

- 抑制要因

- 投資不足がエネルギー貯蔵市場の成長を妨げる可能性

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ

- 揚水発電

- バッテリー蓄電システム

- その他

- 用途

- 住宅

- 商業・産業

- 地域

- インドネシア

- ベトナム

- フィリピン

- マレーシア

- その他のASEAN諸国

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- GS Yuasa Corporation

- Wartsila Oyj Abp

- BYD Co. Ltd.

- SEC Battery Company

- Contemporary Amperex Technology Co. Ltd.(CATL)

- NGK Insulators Ltd.

- LG Chem Ltd.

第7章 市場機会と今後の動向

- 再生可能エネルギー容量を増やすための長期的な政府施策

The ASEAN Energy Storage Market size is estimated at USD 3.55 billion in 2025, and is expected to reach USD 4.92 billion by 2030, at a CAGR of 6.78% during the forecast period (2025-2030).

In 2020, due to the COVID-19 pandemic, many power projects were halted because of pandemic, namely in Cambodia, Indonesia, Myanmar, Philippines, and Vietnam, which is likely to cause the capacity additions to fall behind schedule in the coming years. The primary driver for the market includes the rising demand for uninterrupted power supply in both residential, and commercial and industrial sectors. However, the requirement of high capital to set up a large-scale energy storage facility in ASEAN region is expected to act as a major restraint for the market studied during the forecast period..

Key Highlights

- With the expansion of the electric vehicle market and growing demand for uninterrupted power supply, both in the residential and commercial sectors, batteries are likely to witness significant growth in the market during the forecast period.

- In line with the Paris agreement, countries around the globe are putting effort to increase renewable energy share in its energy mix. For instance, Indonesia has set a target to increase its renewable share to 31% by 2050. An increase in renewable energy like solar PV to power isolated grids in rural villages, inaccessible to the national grid, is likely to create an opportunity for the energy storage facilities in the near future.

- Philippines held the largest market share in 2021 and is expected to continue the same trend during the forecast period.

ASEAN Energy Storage Market Trends

Battery Energy Storage Segment Expected to Witness Significant Growth

- Battery Energy Storage Systems (BESS) is a rapidly emerging market segment in ASEAN countries. The rise in renewable energy consumption is expected to boost BESS demand during the forecast period significantly. However, despite the falling costs of lithium-ion batteries and BESS technology, artificially low tariff levels and fossil fuel subsidies are expected to reduce the competitiveness of BESS technologies in the ASEAN market.

- In July 2022, a large-scale battery system was installed in Singapore as part of a project to increase energy efficiency and reduce emissions from the country's seaports. The 2 MW/2MWh battery energy storage system (BESS) was deployed at Pasir Panjang Terminal, one of four major facilities operated by PSA Singapore. It is also part of the smart grid management system, which can improve the energy efficiency of port operations by 2.5 percent and reduce the port's carbon footprint by 1,000 metric tonnes of CO2 equivalent per year.

- In the ASEAN region, Indonesia is witnessing rapid growth in renewable energy installed capacity. It stood at 12481 MW in 2022, an increase of 8% from the previous year and approx 51% from 2013. In 2023, Total Eren SA got associated with PLN, an Indonesian power utility, to construct The Tanah Laut project consisting of a 70 MW wind power plant integrated with a 10 MWh Battery Energy Storage System that would produce approx. 158 GWh of electricity. The development of such projects would undoubtedly help the ASEAN energy storage market to grow in the forecast period.

- Similarly, In June 2022, Singapore-based energy and urban development group Sembcorp began building 200 MWh of battery storage systems on Jurong Island. The Singapore Energy Markets Authority (EMA) issued an expression of interest (EOI) in May to build 200 MW and 200 MWh of battery storage.

- Therefore, owing to the above points, the battery energy storage segment is expected to grow significantly during the forecast period.

Philippines Expected to Dominate the Market

- Renewable energy is an intermittent source that requires storage for surplus electricity generation. The country is targeting renewables to make up 35% of the generation mix by 2030 and 50% by 2040, which equates to about 15 GW of wind and solar by 2030. The Philippines has about 7670 MW of installed renewable energy capacity as of 2022, where the majority of that is hydroelectric and geothermal energy.

- Investments in renewable energy projects likely pave the way for energy storage markets in the country. In 2023, the Philippines Department of Energy (DOE) devised new market rules and policies for energy storage, a month after the government permitted 100% foreign ownership of renewable energy assets. Following the reform, a group of Chinese companies committed to investing USD 13.7 billion in the country's renewable and energy sectors.

- In 2022, SN Aboitiz Power Group (SNAP) completed its final investment decision for a BESS project of 20 MW capacity located at the Magat Hydropower plant in Ramon, Isabela. 'The energy storage project is expected to commence operation in 2024. Similar projects are being developed in the country, which would benefit the development of the energy storage market in ASEAN.

- In April 2022, Philippines investor-owned utility AboitizPower, and Norwegian renewables group Scatec signed an EPC agreement with Hitachi Energy for it to build a 20 MW/20MWh battery storage system, set to go online in 2024. The joint venture (JV) between the companies, SN Aboitiz Power Group (SNAP), has made the final investment decision on the battery energy storage system (BESS) project at the 360 MW Magat hydropower plant in Ramon, Isabela, in the north Philippines.

- Therefore, owing to the above points, the Philippines is expected to dominate the ASEAN energy storage market during the forecast period.

ASEAN Energy Storage Industry Overview

The ASEAN energy storage market is moderately fragmented. Some of the key players in the market include (in no particular order) GS Yuasa Corporation, Wartsila Oyj Abp, BYD Co. Ltd., SEC Battery Company, and NGK Insulators Ltd., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Growth in Power Demand from Residential, Commercial and Industrial Consumers

- 4.5.1.2 Unscheduled Power Outages and Grid Instability would Demand Energy Storage Solutions

- 4.5.2 Restraints

- 4.5.2.1 Lack of Investments could Hamper the Growth of Energy Storage Market

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Pumped-Hydro Storage

- 5.1.2 Battery Energy Storage Systems

- 5.1.3 Other Types

- 5.2 Application

- 5.2.1 Residential

- 5.2.2 Commercial and Industrial

- 5.3 Geography

- 5.3.1 Indonesia

- 5.3.2 Vietnam

- 5.3.3 Philippines

- 5.3.4 Malaysia

- 5.3.5 Rest of ASEAN

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 GS Yuasa Corporation

- 6.3.2 Wartsila Oyj Abp

- 6.3.3 BYD Co. Ltd.

- 6.3.4 SEC Battery Company

- 6.3.5 Contemporary Amperex Technology Co. Ltd. (CATL)

- 6.3.6 NGK Insulators Ltd.

- 6.3.7 LG Chem Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Long-term Government Policies to Add Renewable Energy Capacity