|

市場調査レポート

商品コード

1690197

エンジニアードウッド:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Engineered Wood - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| エンジニアードウッド:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

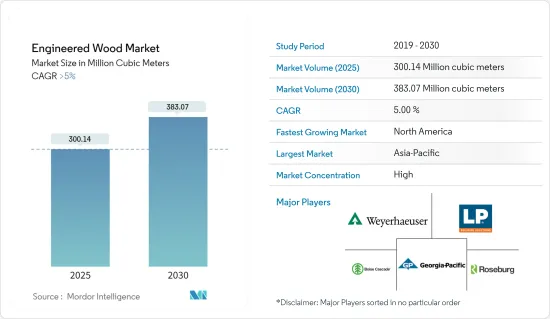

エンジニアードウッド市場規模は、2025年には3億14万立方メートルと推定され、2030年には3億8,307万立方メートルに達すると予測され、予測期間中(2025年~2030年)のCAGRは5%を超えると予測されます。

COVID-19の大流行は市場にマイナスの影響を与えました。しかし、パンデミック後の建設・修復活動の増加により、エンジニアードウッド市場は現在、パンデミック前の水準に達しようとしています。

主なハイライト

- 中期的には、非住宅分野からの需要の増加と、建築材料としてのCLT(クロスラミネートティンバー)の使用の増加が、予測期間中の市場を牽引すると思われます。

- その反面、ホルムアルデヒドの排出に関する厳しい環境問題が市場成長の妨げになる可能性が高いです。

- インドと中国における住宅建設の増加は、予測期間中にチャンスとなることが予想されます。

- アジア太平洋地域は世界市場を独占する可能性が高く、北米は予測期間中にエンジニアードウッドの消費が最も速くなると予想されます。

エンジニアードウッド市場の動向

市場を独占する住宅セグメント

- エンジニアードウッドは、家具、壁、フローリング、ドア、屋根、キャビネット、柱、梁、階段など幅広い用途に使用されています。

- 集成材の用途は急速に拡大しています。低層建築の場合、CLT壁パネルの耐荷重性の向上は、従来のスタッドフレームの壁よりもさらに大きなメリットをもたらします。

- 欧州や北米の中層住宅分野では、CLTはすでに確立されたシステムとなっています。さらに、高さ150メートルを超える超高層ビルの建設にクロスラミネート・ティンバーが使われる例も増えています。

- 壁、床、屋根など様々な住宅用途でOSBの用途が拡大していることが、市場を牽引すると推定されます。

- あらゆる種類のエンジニアードウッドが、住宅分野の様々な用途に大きく使用されています。人口の73%が都市部に住む欧州は、2050年までに80%以上が都市部になると予想されています。

- 欧州の家具企業は非常に成功しており、革新的です。ドイツ、イタリア、北欧の家具会社は、高級デザインの分野におけるベンチマークとして機能しています。

- 米国国勢調査局が発表したデータによると、2023年の米国における民間建築の年間総額は、前年比で4.7%増加しました。

- 2023年の建設総額は1兆9,787億米ドルで、2022年の建設総額を7%上回りました。

- 2023年12月には、2022年の1兆8,409億米ドルに対し2兆960億米ドルが支出され、建設支出は13.9%増加しました。

- このように、前述の側面から、住宅セグメントが予測期間中に市場を牽引すると予想されます。

アジア太平洋が市場を独占する

- アジア太平洋には、中国、インド、ASEAN、日本などの主要国があります。

- 中国は、住宅および商業建設部門の十分な開発が主な原動力となっており、経済成長に支えられています。中国では、香港の住宅当局が低価格住宅の建設を推進するため、いくつかの施策を開始しました。当局は、2030年までに30万1,000戸の公共住宅を供給することを目指しています。

- また、2025年までに7,000ヵ所以上のショッピングセンターが建設される見込みです。

- インドでは、2024年までに手頃な価格の住宅が70%程度増加すると予想されています。Invest Indiaによると、2025年までにインドの建設産業は1兆4,000億米ドルに達すると予想されています。

- また、2030年までに人口の30%以上がインドの都市部に住むようになると予想され、2,500万戸の中級住宅と手頃な価格の追加需要が生まれるため、予測期間中にエンジニアードウッド製品の需要が高まる。

- アジア太平洋では、日本と中国がOSB市場でかなりのシェアを占めています。ノルボンドは20年以上前から日本でOSBパネルを販売しており、様々なエンドユーザーの建築で高い実績を上げています。

- したがって、アジア太平洋が世界市場を独占すると予想されます。

エンジニアードウッド業界の概要

エンジニアードウッド市場は部分的に統合されており、ほとんどの企業がわずかな市場シェアを占めています。市場の主要企業(順不同)には、ウェアハウザー・カンパニー、ボイセ・カスケード、ジョージア・パシフィック、ローズバーグ・フォレスト・プロダクツ、ルイジアナ・パシフィック・コーポレーションなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 非住宅分野からの需要の高まり

- 建設資材としての集成材(CLT)の使用増加

- その他の機会

- 抑制要因

- ホルムアルデヒド排出に関する厳しい環境問題

- その他の阻害要因

- 産業バリューチェーン分析

- ポーターファイブフォース

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- タイプ

- 合板

- 配向性ストランドボード(OSB)

- グルラム

- クロスラミネート・ティンバー(CLT)

- ラミネート・ベニア・ランバー(LVL)

- パーティクルボード

- その他(ファイバーボード、パラレルストランド、その他)

- 用途

- 非住宅用

- 住宅用

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- トルコ

- ロシア

- 北欧諸国

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- ナイジェリア

- カタール

- エジプト

- アラブ首長国連邦

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Binderholz GmbH

- Boise Cascade

- Georgia-Pacific(Georgia-Pacific Wood Products LLC)

- HASSLACHER Holding GmbH

- Havwoods India Pvt. Ltd

- Huber Engineered Woods LLC

- KLH Massivholz Wiesenau GmbH

- Kronoplus Limited

- Louisiana-Pacific Corporation

- Mayr-Melnhof Holz Holding AG

- Nordic Structures

- Pacific Woodtech Corporation

- Resolute Forest Products

- Roseburg

- Stora Enso

- West Fraser

- Weyerhaeuser Company

第7章 市場機会と今後の動向

- インドと中国における住宅建設の成長

- その他の機会

The Engineered Wood Market size is estimated at 300.14 million cubic meters in 2025, and is expected to reach 383.07 million cubic meters by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

The COVID-19 pandemic had a negative impact on the market. However, the market for engineered wood has now been close to reaching pre-pandemic levels because of increasing construction and restoration activities in the post-pandemic period.

Key Highlights

- Over the medium term, growing demand from the non-residential sector and increasing use of cross-laminated timber (CLT) as a construction material are likely to drive the market during the forecast period.

- On the flip side, stringent environmental concerns related to formaldehyde emissions are likely to hinder market growth.

- The growing residential construction in India and China is expected to act as an opportunity in the forecast period.

- Asia-Pacific is likely to dominate the global market, while North America is expected to witness the fastest consumption of engineered wood during the forecast period.

Engineered Wood Market Trends

The Residential Segment to Dominate the Market

- Engineered wood is used for a wide range of applications, including furniture, walls, flooring, doors, roofs, cabinets, columns, beams, and staircases.

- The application of cross-laminated wood has been increasing rapidly. For low-rise construction, the increased loadbearing capacity of CLT wall panels adds further benefits over conventional stud-framed walls.

- Cross-laminated timber is now an established system in the mid-rise residential sector in Europe and North America. In addition, there are increasing examples of cross-laminated timber being used to construct skyscrapers for buildings over 150 meters tall.

- The growing application of OSB in various residential applications, such as walls, flooring, and roofs, is estimated to drive the market.

- All types of engineered woods are significantly used in various applications in the residential sector. With 73% of its population living in urban areas, Europe is expected to be over 80% urban by 2050.

- European furniture companies are very successful and innovative. The German, Italian, and Nordic furniture companies act as benchmarks in the field of high-class design.

- According to the data released by the United States Census Bureau, the total annual value of private construction in the country increased by 4.7% in 2023 compared to the previous year.

- The total value of construction in 2023 was USD 1,978.7 billion, which was 7% above the total value of construction in 2022.

- In December 2023, a total of USD 2,096 billion was spent compared to USD 1,840.9 billion in 2022, registering a 13.9% rise in construction spending.

- Thus, based on the aforementioned aspects, the residential segment is expected to drive the market during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific has several major countries, such as China, India, ASEAN, and Japan.

- China has been majorly driven by ample developments in the residential and commercial construction sectors and is supported by a growing economy. In China, the housing authorities of Hong Kong launched several measures to push start the construction of low-cost housing. The officials aim to provide 301,000 public housing units by 2030.

- China is also likely to witness the construction of 7,000 more shopping centers, which are estimated to start functioning by 2025.

- In India, the availability of affordable housing is expected to rise by around 70% by 2024. By 2025, India's construction industry is expected to reach USD 1.4 trillion, as per Invest India.

- Also, by 2030, more than 30% of the population is expected to live in urban India, creating a demand for 25 million additional mid-end and affordable units, thus bolstering the demand for engineered wood products during the forecast period.

- In Asia-Pacific, Japan and China have a considerable share of the OSB market. Norbond has been marketing its OSB panels in Japan for over 20 years, and it has established a track record of high performance in a variety of end-user construction.

- Hence, Asia-Pacific is expected to dominate the global market.

Engineered Wood Industry Overview

The engineered wood market is partially consolidated, with most players accounting for a marginal market share. Major companies in the market (in no particular order) include Weyerhaeuser Company, Boise Cascade, Georgia-Pacific, Roseburg Forest Products, and Louisiana-Pacific Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from the Non-residential Sector

- 4.1.2 Increasing Use of Cross-laminated Timber (CLT) as Construction Materials

- 4.1.3 Other Opportunities

- 4.2 Restraints

- 4.2.1 Stringent Environmental Concerns Related to Formaldehyde Emissions

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter Five Forces

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Plywood

- 5.1.2 Oriented Strand Board (OSB)

- 5.1.3 Glulam

- 5.1.4 Cross-laminated Timber (CLT)

- 5.1.5 Laminated Veneer Lumber (LVL)

- 5.1.6 Particleboard

- 5.1.7 Other Types (Fiber Board, Parallel Strand, Others)

- 5.2 Application

- 5.2.1 Non-residential

- 5.2.2 Residential

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Turkey

- 5.3.3.7 Russia

- 5.3.3.8 NORDIC Countries

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Nigeria

- 5.3.5.3 Qatar

- 5.3.5.4 Egypt

- 5.3.5.5 United Arab Emirates

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Binderholz GmbH

- 6.4.2 Boise Cascade

- 6.4.3 Georgia-Pacific (Georgia-Pacific Wood Products LLC)

- 6.4.4 HASSLACHER Holding GmbH

- 6.4.5 Havwoods India Pvt. Ltd

- 6.4.6 Huber Engineered Woods LLC

- 6.4.7 KLH Massivholz Wiesenau GmbH

- 6.4.8 Kronoplus Limited

- 6.4.9 Louisiana-Pacific Corporation

- 6.4.10 Mayr-Melnhof Holz Holding AG

- 6.4.11 Nordic Structures

- 6.4.12 Pacific Woodtech Corporation

- 6.4.13 Resolute Forest Products

- 6.4.14 Roseburg

- 6.4.15 Stora Enso

- 6.4.16 West Fraser

- 6.4.17 Weyerhaeuser Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Residential Construction in India and China

- 7.2 Other Opportunities