|

市場調査レポート

商品コード

1690194

自動車オンボードチャージャー:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Automotive On-board Charger - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 自動車オンボードチャージャー:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

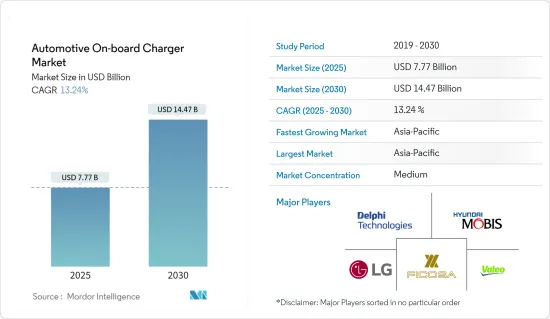

自動車オンボードチャージャーの市場規模は2025年に77億7,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは13.24%で、2030年には144億7,000万米ドルに達すると予測されます。

長期的には、電気自動車の急速な販売、バッテリー技術の進歩、充電インフラの改善、厳しい排ガス規制がオンボードチャージャーの需要を促進すると予想されます。先進国では電気自動車の普及が進んでいます。EV業界の大手企業や新興企業は、今後数年間に新たな電気自動車モデルの投入を計画しています。

国際エネルギー機関(IEA)によると、バッテリー式電気自動車の世界販売台数は、2021年の460万台に対し、2022年には730万台に達し、2021年から2022年にかけて前年比30.3%の伸びを示します。

米国政府は、2030年に温室効果ガス排出量を2005年比で50~52%削減することを約束しました。政府は2050年までにネット・ゼロ経済を達成する目標を発表しました。

市場に高出力の商用車が導入されたことで、これらの車両に組み込むのに適した高度なオンボードチャージャーに対する需要が急増しています。そのため、いくつかのメーカーは、これらの車両の効率を向上させ、オンボードチャージャーのコスト削減に役立つデュアルオンボードチャージャーを組み込む戦略をとっています。今後、電気自動車推進技術の普及が進むにつれて、オンボードチャージャーの需要は世界中で増加すると思われます。

しかし、オンボードチャージャーのコストが高いことは、市場のプレーヤーにとって大きな課題となっています。高コストの問題に対処するため、市場の様々なプレーヤーがこれらの充電器のコストを削減するための先進技術を開発しています。電気自動車の購入者からの高い需要に対応するため、いくつかのOEMは充電時間を短縮するために急速充電技術を搭載した自動車を導入しており、これは予測期間中のオンボードチャージャーの需要にプラスの影響を与えると思われます。今後数年間、アジア太平洋地域は、急速な都市化、一人当たりの可処分所得の増加、新エネルギー車の導入にシフトする消費者の嗜好により、急成長を示すと予想されます。

自動車オンボードチャージャー市場動向

オンボードチャージャー市場をリードする乗用車セグメント

交通セクターの脱炭素化に向けた政府の積極的な後押しと、新エネルギー車の導入に向けた消費者の嗜好の変化により、電気乗用車の普及が近年急速に進んでいます。より多くの消費者が乗用車を採用する傾向にあるため、高度なオンボードチャージャーなど、乗用車の充電効率を向上させるために乗用車に組み込まれる部品の需要が大幅に増加します。

電気自動車製造者協会(SMEV)によると、インドにおける電動四輪車の販売台数は、2023年度の4万7,499台に対し、2024年度には8万8,114台に達し、2023年度と2024年度の前年比成長率は85.5%です。

米国におけるバッテリー式電気自動車の販売台数は、2022年第4四半期の22万6,700台に対し、2023年第1四半期は25万8,800台となり、2022年第4四半期から2023年第1四半期にかけて前期比14.1%の伸びを記録しました。

世界的にEV充電インフラ開発への投資が増加しており、ガソリン/ディーゼル車から電気自動車へのスムーズな移行を支援しています。消費者は、自動車の充電不足によって移動に影響が出ないよう、公共のEV充電ステーションを数多く配備する必要があります。そのため、世界各国の政府はEV充電網の整備に資金を投入しており、これが今後数年間の乗用車用オンボードチャージャーの急成長に寄与することになります。

米国政府は2024年1月、運輸部門の脱炭素化に向けた取り組みを補完するため、さまざまな電気自動車用充電ポイントの全国展開を促進するために6億2,300万米ドルを投資する計画を発表しました。同政府は、オレゴン州での急速充電器の配備や、テキサス州での貨物トラック用水素燃料充電器の配備など、充電インフラを改善するため、全国22州への助成金を通じてこの資金を支出すると述べた。

例えば、英国は2040年までにすべてのガソリン車とディーゼルエンジン車の販売を禁止する予定です。インド政府は、2027年までにインドの全都市からディーゼル車を禁止する案を検討する予定です。ノルウェーなど他の欧州諸国は、2025年までにゼロ燃焼車のみを販売する枠組みをすでに確立しています。二酸化炭素排出量削減を推進するために各国政府が策定している包括的な戦略は、電気乗用車の販売増につながっており、ひいてはオンボードチャージャー市場の需要にプラスに寄与しています。

アジア太平洋地域が自動車オンボードチャージャー市場をリードする見通し

アジア太平洋は、低価格の原材料が入手可能であることから、電気自動車産業の中心地であり、オンボードチャージャー市場をリードすると予想される、

多数の電気自動車メーカーが存在し、人口が増加し、政府も参入しています。そのため、中国、インド、日本などの国々で電気乗用車や商用車産業が拡大するにつれて、オンボードチャージャー市場はアジア太平洋全域で今後数年間に急成長を見せると予想されます。

中国汽車工業協会(CAAM)によると、商用バッテリー電気自動車(BEV)の月次販売台数は、2023年6月の3万3,000台に対し、2023年7月は3万8,000台に達し、6月から7月にかけて前月比15.1%の伸びを示しました。

日本自動車検査登録情報協会によると、日本で使用されているバッテリー電気自動車は、2022年の13万8,330台に対し、2023年には16万2,390台となり、2022年から2023年にかけて前年比17.3%の伸びを記録しました。

BYDやTata Motorsなど、互換性のある電気自動車を提供する複数の自動車メーカーがこの地域に存在することも、EV市場の拡大につながり、オンボードチャージャーの需要を促進しています。物流やラスト・マイル・デリバリー・サービス会社など、この地域の商用フリート・オペレーターは、二酸化炭素排出量削減に対する政府の取り組みを補完するため、電気バンやトラックをフリート内に配備することをますます好むようになっています。今後数年間で、多数のトラックやバンの配備が予想されるため、アジア太平洋全域でオンボードチャージャーの需要が増加すると思われます。

中国がアジア太平洋のオンボードチャージャー市場を独占すると予想されるのは、電気自動車保有台数の増加とEV製造ハブの設立に向けた有利な政策によるものです。同国のオプションのEV充電インフラもEVの普及に貢献すると予想され、それが今後数年間のオンボードチャージャー需要にプラスの影響を与えると思われます。

自動車オンボードチャージャー産業の概要

オンボードチャージャー市場は、エコシステムで事業を展開する様々な国際的メーカーの存在により、断片化され、競争が激しいです。主なプレーヤーには、Delphi Technologies(BorgWarner Inc)、Hyundai Mobis、LG Corporation、STMicroelectronics、Ficosa International S.A.、Valeo SE、Toyota Industries Corporation、Bel Fuse Inc.などがあります。様々な新型電気モデルの市場参入に伴い、オンボードチャージャーメーカーは他のプレーヤーと戦略的提携を結び、新しいオンボードチャージャーを発売することで存在感を高めています。

2023年11月、ボルグワーナーは北米を拠点とする相手先商標製品製造会社(OEM)と提携し、そのOEMが製造する乗用車モデル向けに双方向800Vオンボードチャージャー(OBC)を供給すると発表しました。同社は、オンボードチャージャーには炭化ケイ素パワースイッチが搭載され、車両の効率を高め、電力変換と安全コンプライアンスを改善すると述べています。

2023年6月、ルノーとモビライズは、ルノーが製造するモデル5にR5の双方向オンボードチャージャーを搭載する提携を発表しました。Mobilizeは、同社の双方向充電器、双方向充電ステーション、V2Gサービスは、この技術が電力を送電網に送り返すのに役立つため、顧客の充電コスト削減を支援すると述べた。

オンボードチャージャー市場は、電気自動車の効率を改善し、電気乗用車や商用車の充電時間を短縮する先進技術を統合するための研究開発に大規模な投資が行われると予想されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 電気自動車の普及に向けた政府の積極的な取り組みが市場成長を促進

- 市場抑制要因

- オンボードチャージャーの高コストが市場成長の阻害要因

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 自動車タイプ別

- 乗用車

- 商用車

- パワートレイン別

- バッテリー電気自動車(BEV)

- プラグインハイブリッド車(PHEV)

- 定格出力別

- 3.3 kW未満

- 3.3~11 kW

- 11kW以上

- 販売チャネル別

- 相手先ブランド製造(OEM)

- アフターマーケット

- 地域別

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 世界のその他の地域

- ブラジル

- メキシコ

- アラブ首長国連邦

- その他の国

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Delphi Technologies(BorgWarner Inc.)

- Hyundai Mobis

- LG Corporation

- STMicroelectronics

- Ficosa International S.A.

- Valeo SE

- Delta Energy Systems AG

- Toyota Industries Corporation

- Brusa Elektronik AG

- VisIC Technologies Ltd

- Bel Fuse Inc.

第7章 市場機会と今後の動向

- オンボードチャージャー技術の急速な向上が市場の需要を促進

第8章 サプライヤー情報

The Automotive On-board Charger Market size is estimated at USD 7.77 billion in 2025, and is expected to reach USD 14.47 billion by 2030, at a CAGR of 13.24% during the forecast period (2025-2030).

Over the long term, rapid sales of electric vehicles, advancements in battery technology, improving charging infrastructure, and stringent emission regulations are expected to fuel the demand for automotive on board chargers. The market has been witnessing the adaptation of electric passenger vehicles in developed countries. Major players and new start-ups in the EV industry plan to introduce new electric models in the coming years.

As per the International Energy Agency (IEA), battery electric vehicle sales worldwide touched 7.3 million units in 2022 compared to 4.6 million units in 2021, representing a Y-o-Y growth of 30.3% between 2021 and 2022.

The US government committed to reducing greenhouse gas emissions 50-52% below 2005 levels in 2030. The government announced its target to achieve a net-zero economy by 2050.

With the introduction of high-power commercial vehicles in the market, there is a massive demand for advanced on board chargers suitable for integration into these vehicles. Thus, several manufacturers are strategizing to incorporate dual on board chargers that improve the efficiency of these vehicles and help reduce the cost of the on board chargers. With the growing electric vehicle propulsion technology penetration in the coming years, the demand for on board chargers worldwide will increase.

However, the high cost of on board chargers imposes a significant challenge for players in the market. To tackle the issue of high costs, various players in the market are developing advanced technologies to reduce the cost of these chargers. To keep up with the high demand from buyers for electric vehicles, several OEMs are introducing cars with fast charging technologies to reduce the charging time, which will positively impact the demand for on board chargers during the forecast period. In the coming years, Asia-Pacific is expected to showcase surging growth owing to the rapid urbanization rate, increasing per capita disposable income, and the consumer preference shifting toward the adoption of new-energy vehicles.

Automotive On-board Charger Market Trends

The Passenger Cars Segment is Leading the On Board Charger Market

The penetration of electric passenger cars rapidly increased in recent years, owing to the government's aggressive push toward decarbonizing the transportation sector and consumers' shifting preference toward the adoption of new-energy vehicles. As more consumers are inclined to adopting passenger cars, the demand for components integrated into these cars, such as advanced on board chargers, to improve the charging efficiency of these cars will significantly increase.

As per the Society of Manufacturers of Electric Vehicles (SMEV), the electric four-wheeler sales in India touched 88,114 units in FY 2024 compared to 47,499 units in FY 2023, representing a Y-o-Y growth of 85.5% between FY 2023 and FY 2024.

The battery electric vehicle sales in the United States touched 258.8 thousand units in Q1 2023 compared to 226.7 thousand units in Q4 2022, recording a Q-o-Q growth of 14.1% between Q4 2022 and Q1 2023.

The rising investments in developing EV charging infrastructure globally are assisting the smooth transition from gasoline/diesel cars to electric cars. Consumers need to deploy many public EV charging stations so that their travel is not impacted due to the lack of charge in their vehicles. Hence, governments worldwide are investing in funding to develop the EV charging network, which, in turn, will contribute to the surging growth of on board chargers for passenger cars in the coming years.

In January 2024, the US government announced its plan to invest USD 623 million to foster the deployment of various electric vehicle charging points across the country, complementing its effort to decarbonize the transportation sector. The government stated that this funding will be disbursed through grants to 22 states nationwide to improve charging infrastructure, such as the deployment of rapid chargers in Oregon and hydrogen fuel chargers for freight trucks in Texas.

Globally, governments of many countries plan to promote green mobility by banning diesel vehicles and providing incentives to EV buyers; for instance, the United Kingdom plans to ban sales of all types of gasoline and diesel engine cars by 2040. The Government of India plans to consider a proposal to ban diesel vehicles from all Indian cities by 2027. Other European countries, such as Norway, are already establishing a framework to sell only zero-combustion cars by 2025. The comprehensive strategies being established by the governments to promote the reduction of carbon emissions are leading to increasing sales of electric passenger cars, which, in turn, is positively contributing to the demand for on board chargers in the market.

Asia-Pacific Is Expected to Lead the Automotive On Board Charger Market

Asia-Pacific is expected to lead the automotive on board charger market as it is the hub of the electric vehicle industry owing to the availability of lower-priced raw materials,

numerous electric vehicle manufacturers, growing population, and government participation. Therefore, with the expanding electric passenger cars and commercial vehicles industry in countries such as China, India, and Japan, the market for on board chargers is expected to showcase a rapid surge in the coming years across the Asia-Pacific.

As per the China Association of Automobile Manufacturers (CAAM), the monthly sales of commercial battery electric vehicles (BEVs) touched 38.000 in July 2023 compared to 33,000 units in June 2023, representing an M-o-M growth of 15.1% between June and July 2023.

According to the Japanese Automobile Inspection & Registration Information Association, the number of battery electric cars in use in Japan stood at 162.39 thousand units in 2023 compared to 138.33 thousand units in 2022, recording a Y-o-Y growth of 17.3% between 2022 and 2023.

The presence of several auto manufacturers in the region, such as BYD and Tata Motors, among others, involved in offering compatible electric vehicles is also leading in expanding the EV market, thereby fuelling the demand for on board chargers. Commercial fleet operators in the region, such as logistics and last-mile delivery service companies, are increasingly preferring to deploy electric vans and trucks in their fleet to complement the government's effort in reducing carbon emissions. With the deployment of a large number of trucks and vans expected in the coming years, the demand for on board chargers across the Asia-Pacific will increase during the forest period.

China is expected to dominate the on board chargers market in Asia-Pacific, owing to its growing electric vehicle parc and favorable policies toward establishing an EV manufacturing hub. The country's optional EV charging infrastructure is also expected to contribute to a greater adoption of EVs, which, in turn, will positively impact the demand for on board chargers in the coming years.

Automotive On-board Charger Industry Overview

The on board charger market is fragmented and highly competitive due to the presence of various international manufacturers operating in the ecosystem. Some of the major players include Delphi Technologies (BorgWarner Inc.), Hyundai Mobis, LG Corporation, STMicroelectronics, Ficosa International S.A., Valeo SE, Toyota Industries Corporation, and Bel Fuse Inc., among others. With the entry of various new electric models in the market, on board charger companies are expanding their presence by forming strategic alliances with other players and launching new automotive on board chargers.

In November 2023, BorgWarner announced its partnership with a North American-based original equipment manufacturer (OEM) to supply its bi-directional 800V Onboard Charger (OBC) for the passenger vehicle models manufactured by the OEM. The company stated that its on board chargers are equipped with silicon carbide power switches to enhance the efficiency of the vehicle and improve power conversion and safety compliance.

In June 2023, Renault and Mobilize announced its partnership to incorporate the R5's bi-directional onboard chargers into the model 5 manufactured by Renault. Mobilize stated that its bi-directional chargers, bidirectional charging station, and V2G service will assist customers reduce their charging costs since this technology helps send back electricity to the power grid.

The on board charger market is anticipated to witness massive investments in research and development to integrate advanced technology to improve the efficiency of electric vehicles and reduce the time to charge electric passenger cars or commercial vehicles.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Aggressive Government Focus to Promote the Adoption of Electric Vehicles Fosters the Growth of the Market

- 4.2 Market Restraints

- 4.2.1 High Cost of On Board Chargers Hampers the Growth of the Market

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value - USD and Volume - Units)

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Commercial Vehicles

- 5.2 By Powertrain Type

- 5.2.1 Battery Electric Vehicles (BEVs)

- 5.2.2 Plug-In Hybrid Electric Vehicles (PHEVs)

- 5.3 By Power Rating

- 5.3.1 Less than 3.3 kW

- 5.3.2 3.3-11 kW

- 5.3.3 More than 11 kW

- 5.4 By Sales Channel

- 5.4.1 Original Equipment Manufacturer (OEM)

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Rest of the World

- 5.5.4.1 Brazil

- 5.5.4.2 Mexico

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Other Countries

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Delphi Technologies (BorgWarner Inc.)

- 6.2.2 Hyundai Mobis

- 6.2.3 LG Corporation

- 6.2.4 STMicroelectronics

- 6.2.5 Ficosa International S.A.

- 6.2.6 Valeo SE

- 6.2.7 Delta Energy Systems AG

- 6.2.8 Toyota Industries Corporation

- 6.2.9 Brusa Elektronik AG

- 6.2.10 VisIC Technologies Ltd

- 6.2.11 Bel Fuse Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rapid Enhancement in On Board Charger Technology to Fuel the Market Demand