|

市場調査レポート

商品コード

1690114

硫黄回収技術-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Sulphur Recovery Technologies - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 硫黄回収技術-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

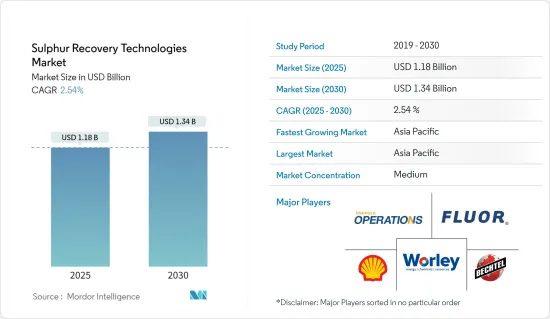

硫黄回収技術の市場規模は2025年に11億8,000万米ドルと推定され、予測期間(2025年~2030年)のCAGRは2.54%で、2030年には13億4,000万米ドルに達すると予測されます。

主なハイライト

- 長期的には、環境問題への関心の高まり、厳しい汚染基準、今後の新しい製油所や拡張プロジェクトが、硫黄回収技術市場を牽引すると予想されます。

- 一方、硫黄回収プロセスの限界と硫黄含有量削減のための高コストが市場を抑制すると予想されます。

- とはいえ、新興市場における未開発の石油・ガスの潜在力は、予測期間以降も急速に増加すると予想されます。このような開発は、市場成長に大きな機会をもたらすと予想されます。

- アジア太平洋は予測期間中最大の市場になると予想され、石油・ガス生産の高水準化、環境規制の強化、精製能力の向上により、需要の大半は中国とインドからもたらされます。

硫黄回収技術の市場動向

製油所セグメントが著しい成長を遂げる見込み

- 硫黄回収技術は製油所で極めて重要な役割を果たしており、硫黄回収装置(SRU)は硫黄回収の要となっています。特に、ガソリンやディーゼルの硫黄レベルを下げることは、排ガス規制を強化し、製品使用時の大気汚染を抑制します。

- 石油・ガス精製プラントの拡張に向けた投資が増加し、環境規制が世界的に強化される中、製油所は今後も優位性を維持する構えです。

- 石油精製所の硫黄回収装置(SRU)は、様々な精製プロセスの製品別であるサワーガスからH2Sを抽出し、工業グレードの溶融硫黄に変換することを任務としています。クラウス・プロセス」として知られるこの装置で採用されている主な方法では、ガス流から95~99.9%の硫化水素を除去することができます。クラウス・プロセスの改良版では、硫化水素を多く含むサワーガスを酸素で燃焼させ、得られたガスを冷却し、溶融硫黄を回収します。

- 例えば、石油輸出国機構によると、製油所の原油処理能力は2023年には日量8,076万バレル、2022年には7,908万バレルでした。この処理能力に大きく貢献しているのは、米国、中国、インド、日本、サウジアラビア、その他ASEAN諸国です。これらの国々は主に炭化水素とその派生物に依存しています。

- 多くの国々が、将来の需要に対応するため、硫黄回収などの技術を中心に石油精製能力を増強しています。例えば、2024年7月、バーラト・ペトロリアム・コーポレーション(BPCL)は、約59億8,000万米ドル(50,000カロールインドルピー)を投じて、インドに年産1,200万トン(MMTPA)の製油所を新設する計画を発表しました。同社はアンドラ・プラデシュ州、ウッタル・プラデシュ州、グジャラート州で立地を検討しています。

- 2024年6月、BPCLは2029年度までに精製能力を4,500万トン/年に増強する意欲を表明しました。BPCLはムンバイ、高知、ビナ(マディヤ・プラデシュ)で製油所を運営しており、合計で約3,600万トンの精製能力を誇っています。

- BPCLは、今後5年間に約200億米ドル(1兆7,000億カロールインドルピー)の投資を予定しています。このうち、製油所と石油化学プロジェクトに75,000カロールインドルピー、パイプライン構想に9億5,700万米ドル(8,000カロールインドルピー)、マーケティング活動に24億米ドル(20,000カロールインドルピー)以上が割り当てられています。

- ウガンダは、2024年1月にドバイの王族が率いる投資会社と交渉していました。その協議の中心は、ウガンダの原油埋蔵量の一部に対する40億米ドルの製油所の開発計画でした。

- 2023年11月までに、スリランカの内閣は中国の巨大エネルギー企業であるシノペックからの45億米ドルの投資を承認しました。この承認は、シノペックが戦略的に重要なハンバントタ港に新しい石油精製所を設置する道を開いた。

- したがって、クリーン燃料の需要増加に伴い、硫黄回収技術市場は予測期間中に大幅に拡大すると予想されます。

アジア太平洋が市場を独占する見込み

- アジア太平洋は広い地域情勢別で、多様な景観、気候、社会、文化、宗教、経済を持っています。世界人口の50%以上がこの地域に住んでいます。また、この地域には硫黄の一次供給源である石油・ガス精製所が数多くあります。このため、クラウスやテールガス処理装置などの硫黄回収技術の需要が高いです。

- この地域には、石油・ガス部門に多額の投資を行っているインドや中国などの新興経済国が多数あります。その結果、環境への影響を低減する必要性から、硫黄回収技術に対する需要が高まっています。また、この地域には大規模な石油化学プロジェクトがいくつかあり、環境基準を満たすために硫黄回収技術が必要とされています。

- アジア太平洋地域は、インドや中国のような新興諸国と、日本、韓国、オーストラリアのような先進国が存在するため、世界で最も急成長している地域の一つです。2023年、中国は世界第2位の石油消費国であり、世界第6位の石油生産国でした。同国は、輸入への依存を減らし、エネルギー安全保障を向上させるため、炭化水素需要の50%近くを輸入しています。アジア太平洋は、硫黄回収技術市場において重要な地域のひとつであり、製油所のようなエネルギー集約型産業の急速な成長により、今後もその優位性が続くと思われます。

- 中国は、四川盆地のような様々な内陸シェール盆地にわたる国内埋蔵量を開発することで、シェールの潜在力を最大限に引き出そうとしています。中国におけるシェールガス開発はここ数年着実に増加しており、2017年以降毎年21%の成長を記録しています。2023年、中国は2,324億3,000万立方メートルの天然ガスを生産します。

- インドの石油精製・石油化学産業にとって、有害な硫黄の排出を削減し、よりクリーンな燃料を生産するための硫黄回収技術は極めて重要です。2022年3月、インドの多国籍エンジニアリング会社であるThermax Ltdは、政府のNorth East Hydrocarbon Vision 2030の一環として、インドの公的部門製油所から硫黄回収ブロックを設置する1億4,902万米ドルの受注を締結しました。

- 2024年2月、マレーシアの国営ペトロナスは、マレーシア石油管理を通じて、半島マレーシア沖に潜在的なガス埋蔵量を持つ2つの発見資源機会クラスターの生産分与契約(PSC)に調印しました。BIGST DROクラスターは、推定回収量4兆立方フィートで、ペトロナス・カリガリと上流企業のJX日鉱日石開発がそれぞれ50%の参加権益を獲得しました。このクラスターは、ブジャン油田、イナス油田、グリン油田、セパト油田、トゥジョー油田の5つの未開発高CO2ガス田で構成されています。

- したがって、大規模な石油・ガス精製産業と、よりクリーンな化石燃料に対する需要の増加により、アジア太平洋が市場を独占すると予想されます。

硫黄回収技術産業の概要

硫黄回収技術市場は細分化されています。この市場の主要企業(順不同)には、Enersul Limited Partnership、WorleyParsons Limited、Shell PLC、Bechtel Corporation、Fluor Corporationなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2029年までの市場規模および需要予測

- 2029年までの製油所設置容量と予測

- 2029年までの精製製品中の硫黄分許容量(百万トン/年)

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 環境問題への関心の高まりと公害に関する厳格な規範

- 抑制要因

- 硫黄回収プロセスの限界

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- 用途

- 製油所

- ガス処理プラント

- 発電所

- その他

- 地域

- 北米

- 米国

- カナダ

- その他の北米

- アジア太平洋

- インド

- 中国

- 韓国

- 日本

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 欧州

- ドイツ

- フランス

- 英国

- スペイン

- ノルディック

- トルコ

- ロシア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- ナイジェリア

- オマーン

- 南アフリカ

- エジプト

- アルジェリア

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 市場シェア分析

- 企業プロファイル

- Enersul Limited Partnership

- Worley Limited

- Shell Plc

- Bechtel Corporation

- Fluor Corporation

- Sulfur Recovery Engineering Inc.

- Honeywell UOP

- Air Liquide S.A.

- List of Other Prominent Companies(Company Name, Headquarters, Revenue, Relevant Products and Services, Operating Sector, Recent Trends, Technology or Projects, Contact Details, etc.)

- 市場ランキング分析

第7章 市場機会と今後の動向

- 新興市場における石油・ガスの未開発ポテンシャル

目次

Product Code: 69995

The Sulphur Recovery Technologies Market size is estimated at USD 1.18 billion in 2025, and is expected to reach USD 1.34 billion by 2030, at a CAGR of 2.54% during the forecast period (2025-2030).

Key Highlights

- Over the long term, growing environmental concerns, strict pollution norms, and upcoming new refinery and expansion projects are expected to drive the sulfur recovery technologies market.

- On the other hand, the limitations of the sulfur recovery process and the high cost of reducing the sulfur content are expected to restrain the market.

- Nevertheless, untapped oil and gas potential in emerging markets is expected to increase rapidly beyond the forecast period. Such developments are expected to provide considerable opportunities for market growth.

- Asia-Pacific is expected to be the largest market during the forecast period, with most demand coming from China and India due to high oil and gas production, increased environmental regulations, and increased refining capacity.

Sulphur Recovery Technologies Market Trends

The Refineries Segment is Likely to Witness Considerable Growth

- Sulfur recovery technologies play a pivotal role in refineries, with the sulfur recovery unit (SRU) being a linchpin for sulfur recovery. Notably, lowering sulfur levels in gasoline and diesel enhances emission controls, subsequently curbing air pollution upon product usage.

- With the rising investments in expanding oil and gas refining plants and the global push for stricter environmental regulations, refineries are poised to maintain their dominance in the future.

- The sulfur recovery unit (SRU) in a petroleum refinery is tasked with extracting H2S from sour gases, a byproduct of various refinery processes, and transforming it into industrial-grade molten sulfur. The predominant method employed in these units, known as the "Claus Process," eliminates a substantial 95-99.9% of hydrogen sulfide from gas streams. In a modified version of the Claus Process, the H2S-rich sour gas is combusted with oxygen, followed by the resulting gas being cooled; molten sulfur is then recovered.

- For instance, according to the Organization of the Petroleum Exporting Countries, refinery crude throughput was 80.76 million barrels per day in 2023 and 79.08 million in 2022. Key contributors to this capacity were the United States, China, India, Japan, Saudi Arabia, and other ASEAN nations. These countries predominantly rely on hydrocarbons and their derivatives.

- Many nations are ramping up their oil refining capabilities, with a focus on technologies like sulfur recovery, to meet future demands. For example, in July 2024, Bharat Petroleum Corporation Limited (BPCL) unveiled plans for a new 12 million metric tons per annum (MMTPA) refinery in India, with an investment of approximately USD 5.98 billion (INR 50,000 crore). The company is scouting locations in Andhra Pradesh, Uttar Pradesh, and Gujarat.

- In June 2024, BPCL announced its ambition to boost its refining capacity to 45 mmtpa by FY 2029. BPCL, which operates refineries in Mumbai, Kochi, and Bina (Madhya Pradesh), boasts a collective refining capacity of about 36 mmtpa.

- BPCL has earmarked around USD 20 billion (INR 1.7 trillion) for investments over the next five years. Of this, INR 75,000 crore is allocated to refinery and petrochemical projects, USD 957 million (INR 8,000 crore) to pipeline initiatives, and over USD 2.4 billion (INR 20,000 crore) to its marketing endeavors.

- Uganda was in talks with an investment firm spearheaded by a member of Dubai's royal family in January 2024. The discussions centered around the development of a planned USD 4 billion refinery for a portion of its crude oil reserves.

- By November 2023, the Sri Lankan cabinet had greenlit a USD 4.5 billion investment from China's energy behemoth, Sinopec. The approval paved the way for Sinopec to set up a new petroleum refinery at the strategically vital Hambantota port.

- Therefore, with the increase in demand for clean fuel, the sulfur recovery technologies market is expected to expand considerably during the forecast period.

Asia-Pacific is Expected to Dominate the Market

- Asia-Pacific covers a wide geographical area and has diverse landscapes, climates, societies, cultures, religions, and economies. More than 50% of the world's population lives in this region. The region is also home to a large number of oil and gas refineries, which are the primary source of sulfur. This resulted in a high demand for sulfur recovery technologies, such as Claus and Tail Gas Treating Units.

- The region is home to a number of emerging economies, such as India and China, which are investing heavily in the oil and gas sector. This has resulted in increased demand for sulfur recovery technologies due to the need to reduce environmental impact. The region is also home to several large-scale petrochemical projects, which require sulfur recovery technologies in order to meet their environmental standards.

- Asia-Pacific is one of the fastest-growing regions in the world, owing to the presence of emerging countries, like India and China, and developed countries, such as Japan, South Korea, and Australia. In 2023, China was the world's second-largest oil consumer and the sixth-largest oil producer. The country imported nearly 50% of its hydrocarbon demand to reduce dependence on imports and improve energy security. Asia-Pacific is one of the significant regions in the sulfur recovery technologies market and is likely to continue its dominance owing to the rapid growth in energy-intensive industries like refineries.

- China has been trying to maximize its shale potential by exploiting its domestic reserves across various inland shale basins, such as the Sichuan Basin. Shale gas development in China has increased steadily over the past few years, recording a growth of 21% annually since 2017. In 2023, China produced 232.43 billion cubic meters of natural gas.

- Sulfur recovery technologies are crucial for India's oil refining and petrochemical industries to reduce harmful sulfur emissions and produce cleaner fuels. In March 2022, Thermax Ltd, an Indian multinational engineering company, concluded a USD 149.02 million order from an Indian public sector refinery to set up a sulfur recovery block as a part of the Government's North East Hydrocarbon Vision 2030.

- In February 2024, Malaysia's state-owned Petronas, through Malaysia Petroleum Management, signed production sharing contracts (PSCs) for two discovered resource opportunity clusters with potential gas reserves offshore peninsular Malaysia. The BIGST DRO cluster has an estimated recovery of 4 trillion cubic feet and was awarded to Petronas Carigali and upstream firm JX Nippon Oil and Gas Exploration, each with a 50% participating interest. The cluster is made up of five undeveloped high-CO2 gas fields, namely the Bujang, Inas, Guling, Sepat, and Tujoh fields.

- Hence, Asia-Pacific is expected to dominate the market due to its large oil and gas refining industry and increasing demand for cleaner fossil fuels.

Sulphur Recovery Technologies Industry Overview

The sulfur recovery technologies market is semi-fragmented. Some of the key players in this market (not in particular order) include Enersul Limited Partnership, WorleyParsons Limited, Shell PLC, Bechtel Corporation, and Fluor Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Refinery Installed Capacity and Forecast, Till 2029

- 4.4 Allowed Sulphur Content in Refined Products in Million Tons Per Year, Till 2029

- 4.5 Recent Trends and Developments

- 4.6 Government Policies and Regulations

- 4.7 Market Dynamics

- 4.7.1 Drivers

- 4.7.1.1 Growing Environmental Concerns and Strict Norms on Pollution

- 4.7.2 Restraints

- 4.7.2.1 Limitations of Sulphur Recovery Process

- 4.7.1 Drivers

- 4.8 Supply Chain Analysis

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Consumers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes Products and Services

- 4.9.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Refineries

- 5.1.2 Gas Processing Plants

- 5.1.3 Power Plants

- 5.1.4 Others

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Asia-Pacific

- 5.2.2.1 India

- 5.2.2.2 China

- 5.2.2.3 South Korea

- 5.2.2.4 Japan

- 5.2.2.5 Malaysia

- 5.2.2.6 Thailand

- 5.2.2.7 Indonesia

- 5.2.2.8 Vietnam

- 5.2.2.9 Rest of Asia-Pacific

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 France

- 5.2.3.3 United Kingdom

- 5.2.3.4 Spain

- 5.2.3.5 NORDIC

- 5.2.3.6 Turkey

- 5.2.3.7 Russia

- 5.2.3.8 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Colombia

- 5.2.4.4 Rest of South America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 United Arab Emirates

- 5.2.5.2 Saudi Arabia

- 5.2.5.3 Nigeria

- 5.2.5.4 Oman

- 5.2.5.5 South Africa

- 5.2.5.6 Egypt

- 5.2.5.7 Algeria

- 5.2.5.8 Rest of Middle East & Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 Enersul Limited Partnership

- 6.4.2 Worley Limited

- 6.4.3 Shell Plc

- 6.4.4 Bechtel Corporation

- 6.4.5 Fluor Corporation

- 6.4.6 Sulfur Recovery Engineering Inc.

- 6.4.7 Honeywell UOP

- 6.4.8 Air Liquide S.A.

- 6.5 List of Other Prominent Companies (Company Name, Headquarters, Revenue, Relevant Products and Services, Operating Sector, Recent Trends, Technology or Projects, Contact Details, etc.)

- 6.6 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Untapped Oil And Gas Potential In Emerging Markets