世界の金属プリント包装:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

Global Metal Print Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 109 Pages

- 納期

- 2~3営業日

- 商品コード

- 1690112

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

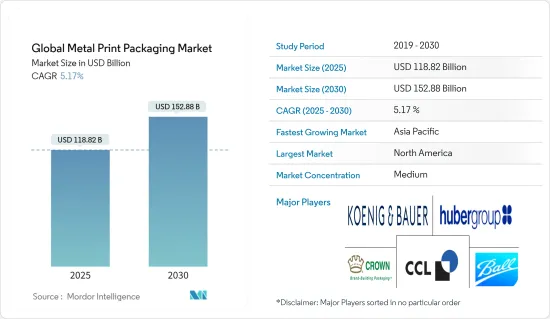

金属プリント包装の世界市場規模は、2025年に1,188億2,000万米ドルと推定され、予測期間(2025年~2030年)のCAGRは5.17%で、2030年には1,528億8,000万米ドルに達すると予測されます。

主なハイライト

- 世界の金属プリント包装市場は、カスタマイズやプレミアム化、金属包装の採用拡大、リサイクルや再利用可能な素材への注目の高まりなどの要因によって上昇基調にあります。さらに、印刷技術の進歩は、市場ベンダーに機会拡大をもたらしています。

- 視覚的に魅力的でパーソナライズされた缶詰食品や飲食品に対する需要の高まりは、予測期間中の金属プリント包装市場の成長をさらに促進する見通しです。印刷インキ、特に金属包装用に調整されたインキの技術革新が市場の需要を促進しています。印刷設備のデジタル化が進み、金属プリント包装への意欲が著しく高まっています。

- 金属包装固有の装飾の利便性は、特定の市場や機会に対応した多様な効果や仕上げを可能にします。製品参入を迅速化するため、ベンダーは最先端の金属印刷技術を採用するようになっています。このシフトは、ベンダーの社内生産能力を強化し、スケジューリングの課題を巧みに管理し、金属包装製品のタイムリーな市場投入を可能にしています。

- 大手飲料メーカーは、棚の視認性を高め、消費者を魅了するためにカスタマイズされた包装に傾倒しており、金属プリント包装の重要性が浮き彫りになっています。この動向の先駆者として、コカ・コーラはデジタルインクジェット印刷の金属缶を中心としたいくつかのキャンペーンを展開しました。著名なアルミ包装メーカーであるBall Corp.によると、プラスチック包装に対するブランドの不安の高まりと代替品の追求により、アルミ缶の需要は増加すると予想されています。

- 市場は手ごわい課題に直面しています。金属サプライヤーの価格上昇は、インキメーカーに価格戦略の調整を迫っています。多くのインキメーカーはこうしたコスト上昇を吸収しようとしているが、値上げやサーチャージに頼っているところも多いです。

金属プリント包装市場動向

オフセット・リソグラフィは大幅な成長が見込まれる

- オフセットリソグラフィは、包装印刷において支配的な手法としての地位を固めています。オフセットリソグラフィは、最小限のメンテナンスで高品質の印刷物を大量に提供できることで人気があります。この効率性により、先進地域、特に欧州と北米で特に支持されています。これらの地域では、金属缶への印刷にはオフセット・リソグラフィが主に採用されているが、これは素材の硬さと非吸収性の性質が大きく影響しています。

- 市場をリードするクラウン・ホールディングス社などは、2ピースと3ピースの金属パッケージの両方にオフセット印刷を採用しています。このプロセスでは、印刷版からブランケットにインクを転写し、その後金属表面に塗布します。特に、2ピース缶は成形後に印刷されるが、3ピース缶はあらかじめシートに印刷されます。クラウン・フード・欧州は、スナック菓子業界の様々なクライアントに対応しており、Bier Nuts社のカリカリにコーティングされたピーナッツ用の100%リサイクル可能な金属容器を製造したり、Satisfied Snacks社のSalad Crispコンセプトの金属缶入り印刷パッケージを納入したりしています。

- オフセット印刷は高品質な出力で定評があるが、グラビア印刷やフォトグラビア印刷のような最先端の方法との厳しい競争に直面しています。さらに、アルマイト印刷版は酸化による錆の影響を受けやすく、入念なメンテナンスが必要です。このような課題は、このセグメントの拡大を妨げる可能性があります。

- ブリキやアルミシートへの高品質保護ラッカーや鮮やかなリソグラフィーを専門とする金属プリントのような企業は、金属包装の幅広い需要に対応しています。金属プリントの製品は、飲食品缶から化学容器、装飾缶まで多岐にわたる。顕著な動向は、オーガニック食品業界が軽量金属缶を好むことであり、優れたバリア特性と環境に優しいことが評価されています。

- オーガニック・トレード・アソシエーションの報告書によると、米国のオーガニック・パッケージ食品市場は大幅な成長を遂げました。2019年の消費額は184億4,180万米ドルで、2025年には250億6,040万米ドルに増加すると予想されています。このようなオーガニック包装食品需要の増加は、食品包装業界におけるオフセット印刷への依存度を高める構えです。

アジア太平洋が著しい成長を遂げる

- アジア太平洋は、世界の金属プリント包装市場で大きなシェアを占めているが、これは主にメーカーがコスト効率の高い包装・ソリューションを重視しているためです。先進国の成熟市場ではデジタル印刷包装市場の停滞が見られるが、中国とインドでは今後7~8年の間に活発な拡大が見込まれます。電子小売販売の急増と便利な食品包装への欲求の高まりに後押しされ、この地域は予測期間中に最も顕著な成長を遂げようとしています。

- アジア太平洋の金属印刷包装市場を牽引する主な要因には、包装食品(冷凍品とチルド品を含む)の売上増加、可処分所得の増加、ライフスタイルの変化、安定した経済成長、アルコール飲料とノンアルコール飲料の両方の消費の増加などがあります。

- ビールのパッケージは、味を保つ優れた能力から、金属缶が主に好まれます。カナダ農業・農業食品省の予測によると、インドのビール消費量は2020年の16億3,000万リットルから、2025年には34億リットルへと飛躍的に増加します。これにより、印刷金属缶の需要が増加すると予想されます。

- デジタル印刷技術によって印刷プロセス全体が自動化され、3D印刷は次のフロンティアとして台頭しつつあります。日本、インド、中国、ベトナムのような国々は、デジタル印刷技術の進歩によって急成長を示しています。特に、三菱電機は最近、AZ600デジタルワイヤーレーザー金属3Dプリンターの新モデル2機種を発表しました。

- アジア太平洋諸国は近年、効率的な金属加工技術への取り組みを強化しており、金属加工産業におけるCO2排出量の削減を目指しています。これは、エネルギー消費を抑制し、枯渇しつつある天然資源を保護しようとするものです。その結果、3D形状データから造形物を製作できる金属3Dプリンターの需要増加が見込まれています。これらのプリンターは、従来の製造工程を大幅に迅速化するだけでなく、廃棄物を最小限に抑え、設計の柔軟性を高め、複数の部品の統合や全体的な重量の軽減を可能にします。

金属プリント包装産業の概要

世界の金属プリント包装市場は、小規模から大規模まで存在する断片的な市場です。大きな市場シェアを持つ大手企業は、世界の消費者層の拡大に積極的に取り組んでいます。主な企業は、東洋製罐、Ball Corporation、Hubergroup Deutschland GmbH、Envases Group、CCL Container(CL Industries Inc.の一部門)、Koenig &Bauer AGなどです。これらの企業は、戦略的パートナーシップ、革新的ソリューションへの投資、新製品の発売を通じて市場での存在感を高めており、これらはすべて予測期間中に競争力を獲得することを目的としています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場促進要因

- デジタル印刷技術の急速な進化

- 市場の課題

- 印刷インキの価格変動

- 代替パッケージソリューションの存在

第6章 市場セグメンテーション

- 印刷プロセス別

- オフセット・リソグラフィー

- グラビア

- フレキソ印刷

- デジタル

- その他の印刷技術

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Hubergroup Deutschland GmbH

- Crown Holdings Inc.

- CCL Container(CCL Industries Inc.)

- Ball Corporation

- Koenig & Bauer AG

- Toyo Seikan Group Holdings, Ltd

- Envases Group

- Real Pad Printer

- Ardagh Metal Packaging(AMP)

第8章 投資分析

第9章 市場の将来

目次

The Global Metal Print Packaging Market size is estimated at USD 118.82 billion in 2025, and is expected to reach USD 152.88 billion by 2030, at a CAGR of 5.17% during the forecast period (2025-2030).

Key Highlights

- The global metal print packaging market is on an upward trajectory driven by factors such as customization and premiumization, the growing adoption of metal packaging, and a heightened focus on recycling and reusable materials. Moreover, advancements in printing technologies are providing market vendors with expanded opportunities.

- The rising demand for visually appealing and personalized canned foods and beverages is poised to further propel the growth of the metal print packaging market during the forecast period. Innovations in printing inks, particularly those tailored for metal packaging, are fueling market demand. The increasing digitization of printing facilities has significantly heightened the appetite for metal print packaging.

- Metal packaging's inherent convenience in decoration enables a diverse range of effects and finishes, catering to specific markets or occasions. To expedite product entry, vendors are increasingly adopting state-of-the-art metal printing technologies. This shift is enhancing vendors' in-house production capabilities, enabling them to adeptly manage scheduling challenges and ensure timely market readiness of their metal-packaged products.

- Leading beverage manufacturers are gravitating toward customized packaging to boost shelf visibility and captivate consumers, underscoring the critical importance of metal print packaging. Pioneering this trend, Coca-Cola rolled out several campaigns centered on digitally inkjet-printed metal cans. According to Ball Corp., a prominent aluminum packaging manufacturer, the demand for aluminum cans is expected to rise owing to brands' growing apprehensions about plastic packaging and their pursuit of alternatives.

- The market faces formidable challenges. Rising prices from metal suppliers are compelling ink producers to adjust their pricing strategies. While many ink manufacturers are attempting to absorb these escalating costs, many have resorted to price hikes and surcharges.

Metal Print Packaging Market Trends

Offset Lithography is Expected to Record Significant Growth

- Offset lithography has solidified its position as the dominant method in packaging printing. It is popular for delivering high-quality prints in bulk with minimal upkeep. This efficiency has made it especially favored in developed regions, notably Europe and North America. In these areas, offset lithography is predominantly employed for printing on metal cans, a choice largely influenced by the material's hard and non-absorbent nature.

- Market leaders, such as Crown Holdings Inc., harness offset printing for both 2-piece and 3-piece metal packaging. The process involves transferring ink from a printing plate to a blanket and subsequently applying it to the metal surface. Notably, while 2-piece cans are printed post-formation, 3-piece cans are printed on sheets beforehand. Crown Food Europe caters to a variety of clients in the snacks industry, producing 100% recyclable metal containers for Bier Nuts' crunchy, coated peanuts and delivering print packaging for Satisfied Snacks' Salad Crisp concept in metal tins.

- Despite its reputation for high-quality output, offset printing faces stiff competition from cutting-edge methods like rotogravure and photogravure. Additionally, the anodized aluminum printing plates, susceptible to rust from oxidation, demand careful maintenance. Such challenges could hinder the expansion of the segment.

- Companies like Metal-Print, specializing in high-quality protective lacquering and vibrant lithography on tinplate or aluminum sheets, address a wide array of metal packaging demands. Metal-Print's offerings span from food and beverage cans to chemical containers and decorative tins. A prominent trend is the organic food industry's preference for lightweight metal cans, lauded for their excellent barrier properties and eco-friendliness.

- According to a report by the Organic Trade Association, the US organic packaged food market witnessed significant growth. The consumption value was USD 18,441.8 million in 2019, which is expected to increase to USD 25,060.4 million by 2025. This increase in demand for organic packaged food is poised to boost the reliance on offset printing in the food packaging industry.

Asia-Pacific to Witness Significant Growth

- Asia-Pacific commands a significant share of the global metal printing packaging market, primarily due to manufacturers' emphasis on cost-effective packaging solutions. While mature markets in established nations see the digital printing packaging market plateauing, China and India are gearing up for vigorous expansion in the coming seven to eight years. Bolstered by a surge in e-retail sales and a growing appetite for convenient food packaging, the region is on track to experience the most pronounced growth during the forecast period.

- Key factors driving the metal print packaging market in Asia-Pacific include rising sales of packaged foods (encompassing frozen and chilled items), growing disposable incomes, shifting lifestyles, consistent economic growth, and an uptick in beverage consumption, both alcoholic and non-alcoholic.

- Beer packaging predominantly favors metal cans, attributed to their superior ability to preserve taste. Projections from Agriculture and Agri-Food Canada indicate a leap in India's beer consumption from 1.63 billion liters in 2020 to a staggering 3.4 billion liters by 2025. This is expected to increase the demand for printed metal cans.

- With digital printing technology automating the entire printing process, 3D printing is emerging as the next frontier. Countries like Japan, India, China, and Vietnam are witnessing a surge driven by advancements in digital printing technologies. Notably, Mitsubishi Electric recently launched two new AZ600 digital wire-laser metal 3D printer models.

- Asia-Pacific countries have ramped up their efforts on efficient metalworking techniques in recent years, aiming to slash CO2 emissions in the metal fabrication industry. This pivot seeks to curtail energy consumption and safeguard dwindling natural resources. Consequently, there is an anticipated uptick in demand for metal 3D printers, which can craft objects from 3D shape data. These printers not only significantly expedite traditional manufacturing processes but also minimize waste and boost design flexibility, allowing the integration of multiple parts and a reduction in overall weight.

Metal Print Packaging Industry Overview

The global metal print packaging market is fragmented in nature, with the presence of both small and large players. Major players holding significant market shares are actively working to broaden their global consumer base. Key players include Toyo Seihan Co. Ltd, Ball Corporation, Hubergroup Deutschland GmbH, Envases Group, CCL Container (a division of CCL Industries Inc.), and Koenig & Bauer AG. These companies are bolstering their market presence through strategic partnerships, investments in innovative solutions, and new product launches, all aimed at gaining a competitive edge during the forecast period.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rapid Evolution of Digital Print Technology

- 5.2 Market Challenges

- 5.2.1 Fluctuations in the Prices of Printing Inks

- 5.2.2 Presence of Alternate Packaging Solutions

6 MARKET SEGMENTATION

- 6.1 By Printing Process

- 6.1.1 Offset Lithography

- 6.1.2 Gravure

- 6.1.3 Flexography

- 6.1.4 Digital

- 6.1.5 Other Printing Technologies

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia

- 6.2.4 Australia and New Zealand

- 6.2.5 Latin America

- 6.2.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Hubergroup Deutschland GmbH

- 7.1.2 Crown Holdings Inc.

- 7.1.3 CCL Container (CCL Industries Inc.)

- 7.1.4 Ball Corporation

- 7.1.5 Koenig & Bauer AG

- 7.1.6 Toyo Seikan Group Holdings, Ltd

- 7.1.7 Envases Group

- 7.1.8 Real Pad Printer

- 7.1.9 Ardagh Metal Packaging (AMP)

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 109 Pages

- 納期

- 2~3営業日