|

市場調査レポート

商品コード

1910828

北米鉱山機械市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)North America Mining Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米鉱山機械市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

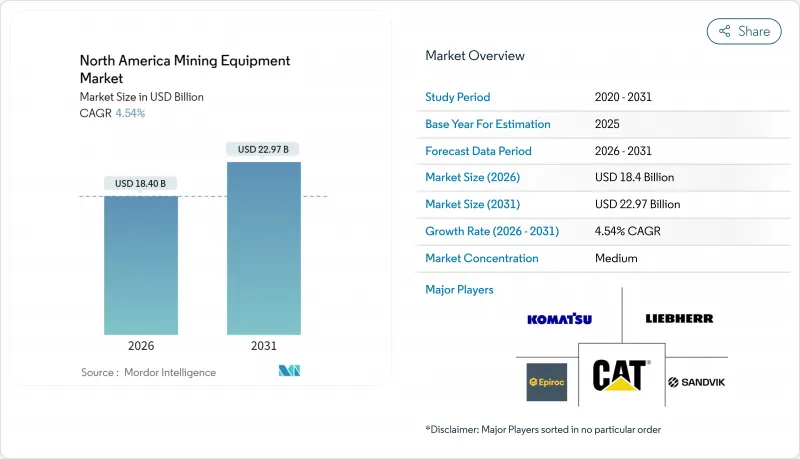

北米の鉱山機械市場は、2025年に176億米ドルと評価され、2026年の184億米ドルから2031年までに229億7,000万米ドルに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは4.54%と見込まれます。

車両の電動化が進行中であること、自動化の導入が加速していること、エネルギー転換に伴う重要鉱物への需要が、この着実な拡大を支えています。これは、事業者が設備投資を抑制し、設備全体の効率性に注力している状況下でも同様です。ディーゼル排出ガスに対する規制監視の強化と、地下鉱山における換気コスト削減の推進が、バッテリー式電気運搬ソリューションの導入を加速させています。同時に、デジタル鉱山プラットフォームは予知保全やリアルタイム鉱石追跡を通じて生産性向上を実現します。鉱山企業は金属価格の変動に対応するため、車両のライフサイクル延長や柔軟な所有モデルの導入を進めており、OEMメーカーにとっては慎重ながらも堅調な販売パイプラインが形成されています。世界の機械メーカーが自律技術と排出ゼロパワートレインを単一のサービスパッケージに統合することで、購入者にとってより明確な総所有コスト(TCO)上の優位性が提供され、競合の激化が予想されます。

北米鉱山設備市場の動向と洞察

鉱山車両の電動化

換気コストの削減、トン当たりコストの65%削減、10~15%のメンテナンス費用削減により、規制圧力がない場合でも、バッテリー式電気運搬トラックはディーゼル車に代わる有力な選択肢となっています。リン酸鉄リチウム電池は現在24時間稼働サイクルをサポートしており、電気式ユニットがディーゼル車と同等の稼働時間を実現可能にしています。カナダでは、ゼロエミッション大型車両に対し30%の還付可能な税額控除が適用され、導入をさらに加速させています。これにより、早期導入企業は運用面およびESG面での優位性を獲得できます。こうしたメリットがあるにもかかわらず、現在稼働中の電動車両は限られており、オンタリオ州、ケベック州、ネバダ州の鉱山現場で急速充電インフラが整備されるにつれ、成長の余地が非常に大きいことを示しています。このため、OEM各社はモジュール式バッテリーパックと車載エネルギー管理ソフトウェアを優先的に開発し、交換時間の短縮とパワートレインの耐久性向上に取り組んでおります。

自動化とデジタル鉱山への移行

自律走行運搬車両は、パイロットプロジェクトからミッションクリティカルな生産資産へと規模を拡大しています。オペレーターからは、無人トラック導入後、生産性の向上と人的オペレーターによる負傷事故の完全な根絶が報告されています。デジタルツインは掘削、運搬、処理のデータをリアルタイムで統合し、予知保全分析による計画外のダウンタイム削減を実現します。遠隔地における労働力不足は自律型ソリューションの有効性をさらに裏付けており、米国中西部やカナダ北部では熟練職の確保が困難な状況です。クラウド連携型IoTセンサーはベアリング振動、油圧、積載重量分布を常時監視し、ルート最適化と資産寿命延長を実現するAIアルゴリズムにデータを供給します。

厳格な排出ガス規制と安全基準

米国環境保護庁(EPA)が提案するTier 5ディーゼル基準は、高度な排気後処理システムを義務付け、中堅鉱山企業にとって単位コストの上昇と資本予算編成の複雑化をもたらします。地下鉱山事業者も、ディーゼル微粒子排出量の下限値達成のため通風量を増やす必要があり、電力需要の増加と利益率の低下を招いています。米国およびカナダ各州で異なる施行時期が設定されているため、規制順守の不確実性が高まっており、複数管轄区域で事業を展開する企業は、可能な限りゼロエミッション車両への標準化を迫られています。大企業はより広範な資産基盤でこれらのコストを分散できる立場にあるため、北米鉱山機械市場における統合が加速する可能性があります。一方、中小企業は大規模な初期投資を伴わずに規制順守を維持するため、レンタル契約や部品の改造を選択する傾向にあります。

セグメント分析

2025年時点で、露天掘採掘機器は北米鉱山機械市場シェアの44.86%を占めておりますが、鉱物処理ユニットは2031年までに最高となる8.14%のCAGRで拡大が見込まれております。この勢いは、鉱山企業が変動する商品価格と低品位鉱石に直面する中、下流工程での価値獲得に向けた戦略的転換を反映しております。エンドユーザーは金属回収率を最大化するため、高容量クラッシャー、省エネルギー型SAGミル、モジュラー式浮選セルを注文しています。自律型掘削装置やリアルタイム鉱石センシング技術も普及が進み、オペレーターは破砕粒度の改善やトン当たりエネルギー消費量の削減を実現しています。

鉱業企業が原料鉱石の輸出のみに依存せず、バリューチェーン全体への影響力を拡大する中、処理設備の需要増加が北米鉱山機械市場を牽引しています。OEMメーカーは、粉砕・分級・脱水工程を単一の制御環境へ統合するプラグアンドプレイ型デジタルモジュールでこれに対応しています。地表設備の需要は、ネバダ州、アリゾナ州、ケベック州北部における銅・リチウムプロジェクトを背景に堅調を維持しております。地下作業の深度化に伴い、自律機能を備えたより強力かつコンパクトな機械が求められる中、地下用ローダーやドリルの需要も着実に増加しております。

2025年時点でディーゼルプラットフォームが北米鉱山機械市場の71.88%を占めていますが、電気式ユニットは2031年までCAGR8.66%で拡大すると予測されています。バッテリー式電気運搬トラックは瞬時トルクが高く、燃料費の変動を排除するため、コスト安定性を求める事業者から支持を集めています。地下鉱山では換気要件の削減や労働者の健康指標改善により最大の恩恵を受け、地上作業では過渡的措置としてハイブリッド駆動システムの改造が導入されています。

充電インフラは依然として主要なボトルネックです。送電網許可の遅延を補うため、利害関係者は現場設置型太陽光発電システムと蓄電池を備えたマイクログリッドの試験運用を進めています。OEMメーカーはブランドを超えたフリートの柔軟性を確保するため、相互運用可能な充電規格に注力しています。鉱山内における電気式軽車両の導入基盤拡大は、高出力機器の広範な展開に向けた土台を築き、北米鉱山機械市場全体で利用データと投資信頼性の好循環を生み出しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 鉱山車両の電動化

- 自動化とデジタル鉱山への移行

- エネルギー転換に向けた重要鉱物の需要

- 老朽化した機械の交換サイクル

- 北極圏永久凍土地域向け超低接地圧設備

- 米国IRA関連探鉱設備投資の急増

- 市場抑制要因

- 厳格な排出規制および安全規制

- 金属価格の変動が設備投資計画に与える影響

- 初期設備コストの高さと資金調達ギャップ

- 高電力電化鉱山における送電網許可のボトルネック

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 機器別

- 露天掘採掘設備

- 地下鉱山設備

- 鉱物処理設備

- ドリル、ブレーカー及び破砕工具

- サポート・補助設備

- その他の特殊機器

- 動力源別

- ディーゼル

- 電気式

- ハイブリッド

- 用途別

- 金属鉱業

- 工業用鉱物採掘

- 石炭採掘

- 骨材・採石

- その他

- 所有形態別

- 新規機器販売

- レンタル・リース

- 再生品・再製造品

- 国別

- 米国

- カナダ

- その他北米地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Caterpillar Inc.

- Komatsu Ltd.

- Liebherr Group

- Epiroc AB

- Sandvik AB

- Hitachi Construction Machinery Co., Ltd.

- Volvo Construction Equipment Ltd.

- Terex Corporation

- SANY Group

- FLSmidth & Co. A/S

- Metso Corporation

- Joy Global Inc.(Komatsu Mining Corp.)

- Mining Equipment Ltd.

- Deere & Company

- Doosan Bobcat(HD Hyundai)

- Astec Industries Inc.

- The Weir Group PLC

- J C Bamford Excavators Ltd

- Wirtgen Group(John Deere)