AIインフラ:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

AI Infrastructure - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 200 Pages

- 納期

- 2~3営業日

- 商品コード

- 1689962

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

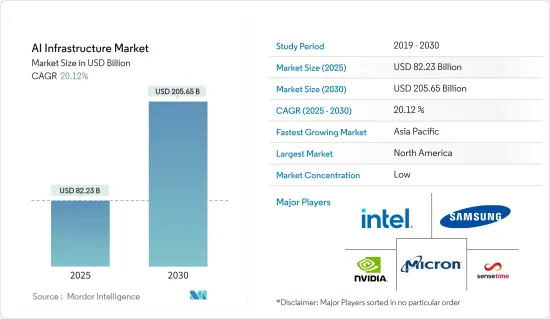

AIインフラの市場規模は2025年に822億3,000万米ドルと推計され、予測期間(2025年~2030年)のCAGRは20.12%で、2030年には2,056億5,000万米ドルに達すると予測されます。

AIインフラ市場イノベーションと効率化を促進

主なハイライト

- 高性能コンピューティング・データセンターの需要急増:AIインフラ市場は、ハイパフォーマンス・コンピューティング(HPC)データセンターにおけるAIハードウェアの需要増加に牽引され、飛躍的な成長を遂げています。企業は人工知能の変革の可能性を認識し、さまざまな業界への投資を促進しています。

- NvidiaのBlueField-3 DPU:世界初の400GbEデータ・プロセッシング・ユニット(DPU)であるこのテクノロジーは、従来のDPUよりも10倍高速であり、AIハードウェアの大幅な進歩を裏付けています。

- グーグル・クラウドとインテルの協業:これらの技術大手は、データセンターにおけるAI機能、セキュリティ、生産性を強化するために設計されたチップを共同開発し、戦略的パートナーシップの傾向を示しました。

- AMDのMI300Xシリーズ:アドバンスト・マイクロ・デバイセズ社はMI300Xチップ・シリーズを発表し、最大800億のパラメータを持つ生成AIモデルの実行を可能にし、AIモデルの複雑化が進んでいることを実証しました。

- 成長を促進するIIoTとオートメーション技術:産業用モノのインターネット(IIoT)とオートメーション技術の統合は、AIインフラ市場を大幅に押し上げています。これらの技術革新は、効率を高め、プロセスを最適化し、価値あるデータを生成しています。

- AFCOM 2021の調査結果:参加企業の40%以上が、2024年までにデータセンターの監視とメンテナンスにロボティクスと自動化を導入する予定であり、自動化の急激な高まりを示唆しています。

- アドバンテックとアクティリティ・インテグレーション:これらの企業は、機械の予後診断と健康管理のためのAIベースのソリューションを発表し、リアルタイムでの機械の状態監視を可能にしました。

- TD SYNNEXのData-IoTSolv:このソリューション・スイートは、データ分析とIoTを活用するためのツールをパートナーに提供するもので、AIを活用したIoTソリューションに対する需要の高まりを示します。

- イノベーションを推進する機械学習とディープラーニング:機械学習とディープラーニングの技術は、AIインフラの成長の重要な原動力であり、企業が膨大なデータセットから価値ある洞察を引き出せるようにします。

- TAZI.AIの資金調達の成功:TAZI.AIは、ヘルスケア、保険、製薬の分野で機械学習ソリューションを展開するために460万米ドルを獲得しており、分野別のAI採用を強調しています。

- 政府部門での活用:機械学習は、業務の自動化やデータ分析に活用され、人的リソースを中核機能に振り向けることができます。

- パンデミック時代の加速:パンデミックはネットワーク自動化のためのAIとMLの採用を加速させ、ネットワークプロバイダーは運用合理化におけるAIの重要な役割を認識しました。

- 自動車やヘルスケア分野でのデータ爆発:自動車やヘルスケアなどの業界ではデータ量が増加しており、データを効率的に管理・分析する高度なAI技術の必要性が高まっています。

- アルパイン・ヘルス・システムズのAI搭載プラットフォーム:このプラットフォームは、複雑な病状の患者の退院プロセスを簡素化し、ヘルスケア管理におけるAIの可能性を示しています。

- Intangles LabのEV向けアンビエント認知AI:このイノベーションは、電気自動車、特に商用EV分野での航続距離不安に対応します。

- ヘルスケア・アプリケーションにおけるAI:AIは臨床上の意思決定、疾病診断、患者データ管理への利用が増加しており、ヘルスケアにおけるその汎用性を示しています。

- 市場情勢と将来展望:AIインフラ市場は、最先端ソリューションを提供するハイテク大手、新興企業、クラウドプロバイダーが混在し、持続的な成長が見込まれています。

- クラウドセグメントの成長:AIインフラのクラウド市場は、2022年に161億2,000万米ドルと評価され、2028年にはCAGR 20.22%を反映して492億9,000万米ドルに達すると予測されます。

- 北米市場のリーダーシップ北米は2022年に195億7,000万米ドルでAIインフラ市場をリードし、2028年には565億9,000万米ドルに達し、CAGR 19.10%で成長すると予測されます。

- 新たなテクノロジー:量子コンピューティング、6Gコネクティビティ、高度なロボット工学などのイノベーションがAIインフラ機能の限界を押し広げ、新たなアプリケーションや使用事例を可能にすると予想されます。

AIインフラ市場の動向

AIインフラの要となるハードウェア・セグメント

- 市場規模と成長:ハードウェアセグメントは、AIインフラ市場の基幹です。2022年には市場シェアの73.70%を占め、345億2,000万米ドルとなりました。CAGR19.19%で成長し、2028年には1,002億9,000万米ドルに達すると予測されます。

- プロセッササブセグメントがリード:プロセッサーは2022年に207億3,000万米ドルと評価され、より強力な処理を必要とするAIアルゴリズムの複雑化により、2028年には575億6,000万米ドルに達すると予測されます。

- カスタマイズ動向:TensorFlowを使用して一般的なカードの2倍の学習速度を実証したファーウェイのAscend 910 AIプロセッサのように、企業はカスタムAIチップにシフトしています。

- エッジコンピューティングの影響力:エッジコンピューティングの台頭がAIプロセッサ開発を形成しています。各メーカーは、特にIoTアプリケーションにおいて、ユースポイントでのリアルタイムのデータ処理を可能にするプロセッサに注力しています。

- ハイブリッド・プロセッサー:各社は、CPUとGPUまたはNPU(Neural Processing Unit)を組み合わせたハイブリッドAIプロセッサを開発し、多様なAIアプリケーションの汎用性と効率性を高めています。

北米が主要市場シェアを占める

クラウドセグメント:AI民主化の起爆剤

- 急速な成長軌道:2022年に161億2,000万米ドルだったクラウド分野は、CAGR 20.22%で成長し、2028年には492億9,000万米ドルに達すると予測されます。この成長は市場全体のCAGRを上回っており、AIインフラにおけるクラウドソリューションの重要な役割を示しています。

- AIの民主化:クラウドベースのAIインフラは導入障壁を下げ、あらゆる規模の企業がAIテクノロジーにアクセスできるようにします。この民主化により、デジタルトランスフォーメーションが加速し、イノベーションが促進されます。

- 拡張性と柔軟性:クラウドプラットフォームは比類のないスケーラビリティを提供するため、企業はデータ集約型のモデルトレーニングや推論などのAIワークロードを容易に管理できます。

- AI-as-a-Serviceの普及:AI-as-a-Service(AIaaS)の台頭により、企業は事前に訓練されたモデルやツールセットにアクセスできるようになりました。例えば、NvidiaのDGX CloudはAIモデルのトレーニングのためのスーパーコンピューティングサービスを提供し、SalesforceのAI Cloudはエンタープライズ対応のAIツールを提供しています。

- 戦略的コラボレーション:Google CloudとシンガポールのSmart Nationイニシアチブの提携など、AIハードウェア・プロバイダーとクラウド・プラットフォーム間のコラボレーションにより、分野に特化したAIクラウド・ソリューションが構築されつつあります。

- 市場の展望:AIインフラ市場は、ハードウェアとクラウドの両分野が相乗的に発展することで、今後も進化を続けると思われます。AIアプリケーションの普及に伴い、スケーラブルで堅牢なインフラへの需要が高まり、AIハードウェアとクラウドネイティブ・ソリューションの専門化に拍車がかかると思われます。

AIインフラ業界の概要

ハイテク大手が市場をリードAIインフラ市場は、インテル、Nvidia、IBM、マイクロソフト、サムスンなどのハイテク大手が独占しています。これらの企業は、豊富なリソース、包括的なAIソリューション、世界のリーチにより、大きな市場シェアを占めています。

エヌビディアのDGXクラウドサービス:このAIスーパーコンピューティング・サービスは、企業が高度な生成AIモデルを訓練することを可能にし、エンド・ツー・エンドのAIインフラ・ソリューション提供における同社のリーダーシップを示します。

IBMとマイクロソフトのハイブリッドソリューション:両社はAI機能を統合したハイブリッドクラウドソリューションを開発し、企業がさまざまな環境にAIを効率的に展開できるようにしています。

多額の研究開発投資:大手企業は競争力を維持するために研究開発に多額の投資を行い、AI技術の進歩の最前線にいることを確実にしています。

イノベーションと専門化が市場の成功を促進AIインフラ市場での成功は、継続的なイノベーションと業界固有の専門性にかかっています。

シスコのジェネレーティブAIソリューションシスコは、ジェネレーティブAIを活用した新しいネットワーク、セキュリティ、観測可能性を発表し、競争優位性を獲得するためのイノベーションの重要性を強調しました。

Mphasis.aiの産業フォーカス:Mphasisは、既存の技術環境にAI機能を統合し、特定分野の業務効率を最適化することに注力しています。

戦略的パートナーシップ:グーグル・クラウドのAIコンサルティング・サービスの拡大は、企業が戦略的提携を活用して提供するサービスを拡大し、新たな市場を開拓する方法を例証しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響

第5章 市場力学

- 市場促進要因

- ハイパフォーマンスコンピューティング・データセンターにおけるAIハードウェア需要の増加

- IIoTとオートメーション技術の応用拡大

- 機械学習とディープラーニング技術の応用拡大

- 自動車やヘルスケアなどの産業で生成される膨大なデータ量

- 市場抑制要因

- 業界における熟練した専門家の不足

第6章 市場セグメンテーション

- 製品別

- ハードウェア

- プロセッサー

- ストレージ

- メモリー

- ソフトウェア

- ハードウェア

- 展開別

- オンプレミス

- クラウド

- ハイブリッド

- エンドユーザー別

- 企業

- 政府機関

- クラウドサービスプロバイダー

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- アジア

- 中国

- インド

- 韓国

- 日本

- オーストラリアとニュージーランド

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- イスラエル

- 南アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Intel Corporation

- Nvidia Corporation

- Samsung Electronics Co. Ltd

- Micron Technology Inc.

- Sensetime Group Inc.

- IBM Corporation

- Google LLC

- Microsoft Corporation

- Amazon Web Services Inc.

- Cisco Systems Inc.

- Arm Holdings

- Dell Inc.

- Hewlett Packard Enterprise Development LP

- Advanced Micro Devices

- Synopsys Inc.

第8章 投資分析

第9章 市場の将来

目次

The AI Infrastructure Market size is estimated at USD 82.23 billion in 2025, and is expected to reach USD 205.65 billion by 2030, at a CAGR of 20.12% during the forecast period (2025-2030).

AI Infrastructure Market: Driving Innovation and Efficiency

Key Highlights

- Demand Surge in High-Performance Computing Data Centers: The AI Infrastructure market is experiencing exponential growth, driven by increasing demand for AI hardware in high-performance computing (HPC) data centers. Businesses are realizing the transformative potential of artificial intelligence, fueling investments across various industries.

- Nvidia's BlueField-3 DPU: This technology, the world's first 400GbE data processing unit (DPU), is ten times faster than its predecessor, underscoring significant advancements in AI hardware.

- Google Cloud and Intel Collaboration: These tech giants jointly developed a chip designed to enhance AI capabilities, security, and productivity in data centers, marking a trend of strategic partnerships.

- AMD's MI300X Series: Advanced Micro Devices Inc. introduced the MI300X chip series, enabling the execution of generative AI models with up to 80 billion parameters, demonstrating the escalating complexity of AI models.

- IIoT and Automation Technologies Propelling Growth: The integration of Industrial Internet of Things (IIoT) and automation technologies is significantly boosting the AI Infrastructure market. These innovations are enhancing efficiency, optimizing processes, and generating valuable data.

- AFCOM 2021 Study Results: Over 40% of participants plan to deploy robotics and automation in data center monitoring and maintenance by 2024, signaling a sharp rise in automation.

- Advantech and Actility Integration: These companies launched an AI-based solution for machine prognostics and health management, enabling real-time machine status monitoring.

- TD SYNNEX's Data-IoTSolv: This solution suite equips partners with tools for leveraging data analytics and IoT, illustrating the growing demand for AI-powered IoT solutions.

- Machine Learning and Deep Learning Driving Innovation: Machine learning and deep learning technologies are critical drivers of AI infrastructure growth, empowering companies to extract valuable insights from massive datasets.

- TAZI.AI's Funding Success: The startup secured $4.6 million to roll out machine learning solutions in healthcare, insurance, and pharmaceuticals, highlighting sector-specific AI adoption.

- Government Sector Utilization: Machine learning is increasingly used in government sectors to automate operations and analyze data, freeing human resources for core functions.

- Pandemic-Era Acceleration: The pandemic sped up AI and ML adoption for network automation, with network providers recognizing the essential role of AI in operational streamlining.

- Data Explosion in Automotive and Healthcare Sectors: The growing volume of data in industries like automotive and healthcare is propelling the need for advanced AI technologies to manage and analyze data efficiently.

- Alpine Health Systems' AI-Powered Platform: This platform simplifies hospital discharge processes for patients with complex medical conditions, demonstrating AI's potential in healthcare management.

- Intangles Lab's Ambient Cognitive AI for EVs: This innovation addresses range anxiety in electric vehicles, particularly in the commercial EV sector.

- AI in Healthcare Applications: AI is increasingly used for clinical decision-making, disease diagnosis, and patient data management, showcasing its versatility in healthcare.

- Market Landscape and Future Outlook: The AI Infrastructure market is poised for sustained growth, led by a mix of tech giants, startups, and cloud providers delivering cutting-edge solutions.

- Cloud Segment Growth: The AI Infrastructure cloud market, valued at $16.12 billion in 2022, is forecasted to reach $49.29 billion by 2028, reflecting a CAGR of 20.22%.

- North American Market Leadership: North America led the AI infrastructure market in 2022 with $19.57 billion in value, projected to hit $56.59 billion by 2028, growing at a 19.10% CAGR.

- Emerging Technologies: Innovations like quantum computing, 6G connectivity, and advanced robotics are expected to push the boundaries of AI infrastructure capabilities, enabling new applications and use cases.

AI Infrastructure Market Trends

Hardware Segment Cornerstone of AI Infrastructure

- Market Size and Growth: The hardware segment is the backbone of the AI Infrastructure market. In 2022, it accounted for 73.70% of the market share, valued at $34.52 billion. It is expected to grow at a CAGR of 19.19%, reaching $100.29 billion by 2028.

- Processor Subsegment Leads: Processors were valued at $20.73 billion in 2022 and are forecasted to reach $57.56 billion by 2028, driven by the increasing complexity of AI algorithms requiring more powerful processing.

- Customization Trend: Companies are shifting towards custom AI chips, like Huawei's Ascend 910 AI processor, which demonstrated twice the training speed of common cards using TensorFlow.

- Edge Computing Influence: The rise of edge computing is shaping AI processor development. Manufacturers are focusing on processors that enable real-time data processing at the point of use, particularly in IoT applications.

- Hybrid Processors: Companies are developing hybrid AI processors that combine CPUs with GPUs or Neural Processing Units (NPUs), enhancing versatility and efficiency for diverse AI applications.

North America to Hold Major Market Share

Cloud Segment: Catalyst for AI Democratization

- Rapid Growth Trajectory: The cloud segment, valued at $16.12 billion in 2022, is projected to grow at a 20.22% CAGR, reaching $49.29 billion by 2028. This growth is outpacing the overall market CAGR, signaling the critical role of cloud solutions in AI infrastructure.

- Democratization of AI: Cloud-based AI infrastructure lowers adoption barriers, making AI technologies accessible to businesses of all sizes. This democratization accelerates digital transformation and fosters innovation.

- Scalability and Flexibility: Cloud platforms offer unmatched scalability, enabling enterprises to easily manage AI workloads, such as model training and inference, which are data-intensive.

- AI-as-a-Service Proliferation: The rise of AI-as-a-Service (AIaaS) allows companies to access pre-trained models and toolsets. For example, Nvidia's DGX Cloud offers supercomputing services for AI model training, while Salesforce's AI Cloud delivers enterprise-ready AI tools.

- Strategic Collaborations: Collaborations between AI hardware providers and cloud platforms, such as Google Cloud's partnership with Singapore's Smart Nation initiative, are creating sector-specific AI cloud solutions.

- Market Outlook: The AI Infrastructure market will continue to evolve with the hardware and cloud segments developing synergistically. As AI applications proliferate, the demand for scalable, robust infrastructure will grow, spurring further specialization in AI hardware and cloud-native solutions.

AI Infrastructure Industry Overview

Tech Giants Lead the Market: The AI Infrastructure market is dominated by tech giants like Intel, Nvidia, IBM, Microsoft, and Samsung. These companies hold significant market share due to their extensive resources, comprehensive AI solutions, and global reach.

Nvidia's DGX Cloud Service: This AI supercomputing service enables businesses to train sophisticated generative AI models, showcasing the company's leadership in providing end-to-end AI infrastructure solutions.

IBM and Microsoft Hybrid Solutions: Both companies have developed hybrid cloud solutions that integrate AI capabilities, empowering enterprises to deploy AI across various environments efficiently.

Substantial R&D Investments: Leading players invest heavily in research and development to maintain their competitive edge, ensuring they stay at the forefront of AI technology advancements.

Innovation and Specialization Drive Market Success: Success in the AI Infrastructure market hinges on continuous innovation and industry-specific specialization.

Cisco's Generative AI Solutions: Cisco introduced new network, security, and observability offerings powered by generative AI, highlighting the importance of innovation in gaining a competitive edge.

Mphasis.ai's Industry Focus: Mphasis focuses on integrating AI capabilities into existing technological environments, optimizing operational efficiency in specific sectors.

Strategic Partnerships: Google Cloud's expansion of AI consulting services exemplifies how companies can leverage strategic collaborations to broaden their offerings and tap into new markets.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Consumers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for AI Hardware in High-performance Computing Data Centers

- 5.1.2 Increasing Applications of IIoT and Automation Technologies

- 5.1.3 Rising Application of Machine Leaning and Deep Learning Technologies

- 5.1.4 Huge Volume of Data Being Generated in Industries such as Automotive and Healthcare

- 5.2 Market Restraints

- 5.2.1 Lack of Skilled Professionals in the Industry

6 MARKET SEGMENTATION

- 6.1 By Offering

- 6.1.1 Hardware

- 6.1.1.1 Processor

- 6.1.1.2 Storage

- 6.1.1.3 Memory

- 6.1.2 Software

- 6.1.1 Hardware

- 6.2 By Deployment

- 6.2.1 On-premise

- 6.2.2 Cloud

- 6.2.3 Hybrid

- 6.3 By End User

- 6.3.1 Enterprises

- 6.3.2 Government

- 6.3.3 Cloud Service Providers

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.2.4 Italy

- 6.4.2.5 Spain

- 6.4.3 Asia

- 6.4.3.1 China

- 6.4.3.2 India

- 6.4.3.3 South Korea

- 6.4.3.4 Japan

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.5.1 Brazil

- 6.4.5.2 Mexico

- 6.4.6 Middle East and Africa

- 6.4.6.1 Saudi Arabia

- 6.4.6.2 United Arab Emirates

- 6.4.6.3 Qatar

- 6.4.6.4 Israel

- 6.4.6.5 South Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Intel Corporation

- 7.1.2 Nvidia Corporation

- 7.1.3 Samsung Electronics Co. Ltd

- 7.1.4 Micron Technology Inc.

- 7.1.5 Sensetime Group Inc.

- 7.1.6 IBM Corporation

- 7.1.7 Google LLC

- 7.1.8 Microsoft Corporation

- 7.1.9 Amazon Web Services Inc.

- 7.1.10 Cisco Systems Inc.

- 7.1.11 Arm Holdings

- 7.1.12 Dell Inc.

- 7.1.13 Hewlett Packard Enterprise Development LP

- 7.1.14 Advanced Micro Devices

- 7.1.15 Synopsys Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 200 Pages

- 納期

- 2~3営業日