フレキシブル断熱材:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Flexible Insulation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1689957

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

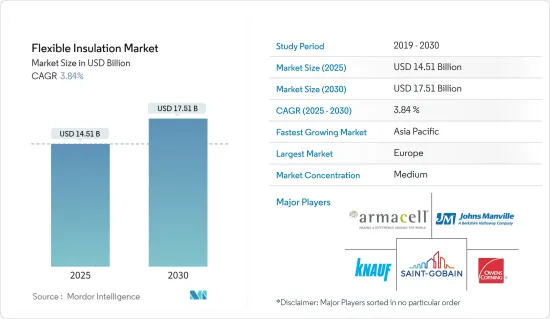

フレキシブル断熱材の市場規模は2025年に145億1,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは3.84%で、2030年には175億1,000万米ドルに達すると予測されます。

主なハイライト

- 建設業界からのエネルギー効率に対する要求の高まりと、フレキシブル配管断熱材の用途拡大が、今後数年間のフレキシブル断熱材市場を牽引すると予想されます。

- しかし、より優れた代替品が入手可能であることが市場成長の妨げになると予想されます。

- 電気自動車におけるエアロゲル断熱材の新たな機会が、予測期間中に市場にチャンスをもたらすと期待されています。

- 欧州が市場を独占すると予想されるが、アジア太平洋は中国、インド、日本などの国々からの消費の増加により、最も高いCAGRで推移すると予想されます。

フレキシブル断熱材の市場動向

ガラス繊維断熱材の需要増加

- ガラス繊維は、細いガラス繊維と高温バインダーとの極めて強力な結合で構成されています。これらの繊維(1本の直径はほぼ6~7ミクロン)は、数百万の小さな空気ポケットを閉じ込めるように分布しており、それによって優れた断熱性と遮音性を生み出しています。ファイバーグラスは化学的に不活性で、アイアンショット、硫黄、塩化物などの不純物は含まれていません。

- 腐食性がなく、カビの発生もありません。それは、再生可能な原料から製造され、製造のすべての段階で環境に優しいです。毛布(バットやロール)やルーズフィルのような様々な形の断熱材に使用され、硬質ボードやダクト断熱材としても利用できます。ガラス繊維断熱材は、砂、石灰石、ソーダ灰、再生ガラスカレットを混合して製造されます。

- 2種類のガラス繊維が、住宅、商業施設、インフラ建設に広く使用されています。ひとつは繊維状のもので、柔軟なブランケット、硬質ボード、パイプ断熱材、その他あらかじめ成形された形状のものがあります。不燃性で吸音性に優れています。もうひとつはセルラータイプで、ボード状やブロック状のものがあり、パイプ断熱材やさまざまな形状に加工できます。構造強度は高いが、耐衝撃性は低いです。この素材は不燃性、非吸収性で、多くの化学薬品に耐性があります。主に工業用オーブン、熱交換器、乾燥機、ボイラー、配管などの断熱に使われます。

- 米国のような国では建設活動が増加しており、これがガラス繊維製フレキシブル断熱材の需要を高めています。例えば、米国国勢調査局によると、2023年の米国の年間建設額は1兆9,787億米ドルで、2022年と比較して約7.03%増加しています。

- 繊維状ガラス断熱材は、板金ダクト、ハウジング、プレナムの外装に使用されます。半硬質から硬質のボードを形成し、冷凍機やその他の冷熱機器の断熱にも適しています。0°F(-18℃)~450°F(232℃)の温度範囲で使用できます。

- 最近では、ガラス繊維の製造にリサイクル窓ガラスや自動車ガラス、ボトルガラスを使用するケースが増えています。市場で入手可能なリサイクル原料の量は、リサイクル含有量に制限を設けています。リサイクル材料の使用は、断熱製品の製造に必要なエネルギーを着実に削減するのに役立っています。

- 上記の要因から、ガラス繊維断熱材の需要は予測期間中にさらに伸びると予想されます。

市場を独占する欧州

- 欧州は柔軟な断熱材の最大市場になると予測されています。建築物の効率を高めるためのEU指令に伴う厳しい建築物エネルギー規制が、この地域における柔軟な断熱材の需要を促進すると予想されます。

- ドイツのような国の建設部門からのフレキシブル断熱材に対する旺盛な需要は、フレキシブル断熱材市場の成長のもう一つの理由です。ドイツにおけるホテルの建設も、予測期間中に急増する見込みです。2022年には89の新しいホテルと15,780の客室が立ち上げられ、2023年にはさらに78のプロジェクトと13,073のキーが計画されています。ホテルのパイプラインは2024年以降も堅調に推移すると予想され、すでに153プロジェクト、22,769室が進行中です。

- さらに、英国ではさまざまな建設プロジェクトが活発に行われており、柔軟な断熱材に対する将来の需要が高まると予想されています。例えば、ニュー・ロンドン・アーキテクチャーによると、ロンドンでは高層ビルが540棟近く計画・建設中で、既存の高層ビル数は360棟です。高層ビルの建設が増加していることが、調査された市場を牽引すると推定されます。

- フランスでは、建設業界の売上高指数はここ数年緩やかな成長を続けています。同国の建設業界は、8年間にわたる落ち込みの後、最近になって勢いを取り戻しました。エコロジー・連帯移行省は、フランスの建築許可総数が2023年12月の33,765戸から2024年1月には26,585戸に増加したことを明らかにしました。

- 欧州は、急速な工業化と大手断熱材メーカーの存在により、新興素材をいち早く採用し、高い製品売上高を記録しました。

- そのため、欧州地域におけるフレキシブル断熱材の需要拡大が、予測期間中の市場調査を促進すると予想されます。

フレキシブル断熱材産業の概要

フレキシブル断熱材市場は細分化されています。同市場の主要企業には、Armacell、Knauf Group、Johns Manville、Owens Corning、Saint-Gobainなどがあります(順不同)。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 建設業界からのエネルギー効率化要求の高まり

- フレキシブル配管用断熱材の用途拡大

- その他の促進要因

- 市場抑制要因

- 代替品の入手可能性

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 素材別

- エアロゲル

- 架橋ポリエチレン

- エラストマー

- ガラス繊維

- その他の素材

- 断熱タイプ別

- 音響絶縁

- 電気絶縁

- 断熱材

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- 市場ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Altana AG

- Armacell

- Cabot Corporation

- Etex Group

- Fletcher Insulation

- Johns Manville

- Kingspan Group

- Knauf Insulation

- Owens Corning

- Saint-Gobain

- Superlon Holdings Berhad

- Thermaxx Jackets

第7章 市場機会と今後の動向

- 電気自動車におけるエアロゲル断熱材の新たな機会

- その他の機会

目次

Product Code: 69527

The Flexible Insulation Market size is estimated at USD 14.51 billion in 2025, and is expected to reach USD 17.51 billion by 2030, at a CAGR of 3.84% during the forecast period (2025-2030).

Key Highlights

- The increasing demand for energy efficiency from the construction industry and the increasing application of flexible piping insulation are expected to drive the flexible insulation market in the coming years.

- However, the availability of better alternatives is expected to hinder the growth of the market.

- Emerging opportunities for aerogel insulation in electric vehicles are expected to create opportunities for the market during the forecast period.

- Europe is expected to dominate the market, while Asia-Pacific is expected to register the highest CAGR owing to the increasing consumption from countries such as China, India, and Japan.

Flexible Insulation Market Trends

Rising Demand for Fiberglass Insulation

- Fiberglass consists of extremely strong bonds between thin glass fibers and a high-temperature binder. These fibers (each of nearly 6-7 microns in diameter) are distributed to trap millions of tiny pockets of air in them, thereby creating excellent thermal and acoustic insulation. Fiberglass is chemically inert and has no impurities, such as iron shots, sulfur, or chloride.

- The product is non-corrosive and does not support mold growth. It is manufactured from renewable raw materials and is eco-friendly in every stage of manufacturing. It is used in different forms of insulation, such as blankets (batts and rolls) and loose-fill, and is also available as rigid boards and duct insulation. Fiberglass insulation is manufactured with a blend of sand, limestone, soda ash, and recycled glass cullet.

- Two types of fiberglass are extensively used in residential, commercial, and infrastructural construction. One is the fibrous one, which is available in flexible blankets, rigid boards, pipe insulation, and other pre-molded shapes. It is non-combustible and has good sound absorption qualities. The second one is the cellular type, which is available in board and block forms and capable of being fabricated into pipe insulation and various shapes. It has good structural strength but poor impact resistance. The material is non-combustible, non-absorptive, and resistant to many chemicals. It is mainly used to insulate industrial ovens, heat exchangers, driers, boilers, and pipe work.

- Construction activities are increasing in countries like the United States, which is increasing the demand for fiberglass flexible insulation. For instance, according to the US Census Bureau, the annual value for construction in the United States accounted for USD 1,978.7 billion in 2023, which is an increase of about 7.03% compared to that of 2022.

- Fibrous glass insulation is applied to the exterior of sheet metal ducts, housings, and plenums. It forms semi-rigid to rigid boards that are also suitable for insulating chillers and other cold or hot equipment. It can be used in applications within the temperature range of 0°F (-18°C) to 450°F (232°C).

- In recent times, recycled windows and automotive or bottle glass have been increasingly used in the manufacture of glass fiber. The amount of usable recycled material available in the market limits the recycled content. The use of recycled material has helped to reduce the energy required to produce insulation products steadily.

- Owing to the above-mentioned factors, the demand for fiberglass insulation is expected to grow further over the forecast period.

Europe to Dominate the Market

- Europe is projected to be the largest market for flexible insulation. Stringent building energy codes accompanied by EU Directives to enhance efficiency in buildings are expected to drive the demand for flexible insulation in the region.

- Robust demand for flexible insulation from the construction sector in countries like Germany is another reason for the growth of the flexible insulation market. The construction of hotels in Germany is also expected to witness a sharp rise during the forecast period. The year 2022 witnessed the launch of 89 new hotels and 15,780 rooms, and 78 more projects with 13,073 keys were mooted for 2023. The pipeline of hotels is anticipated to stay strong for 2024 and beyond, with 153 projects and 22,769 rooms already in the works.

- Moreover, various construction projects are active in the United Kingdom, which is expected to enhance the future demand for flexible insulation. For instance, according to New London Architecture, there are nearly 540 planned and under construction high-rise buildings in London, with an existing number of 360 tall buildings. The growing construction of high-rise buildings is estimated to drive the market studied.

- In France, the construction index has been witnessing slow growth, with a gradual increase in the industry turnover index over the past few years. The construction industry in the country recently gained momentum after eight long years of decline. The Ministere de la Transition ecologique et solidaire revealed an increase in total building permits in France to 26,585 Units in January 2024 from 33,765 Units in December 2023.

- Europe was an early adopter of emerging materials on account of rapid industrialization and the presence of major insulation product manufacturers, thus leading to high product sales.

- Thus, the growing demand for flexible insulation in the Europe region is expected to drive the market studied during the forecast period.

Flexible Insulation Industry Overview

The flexible insulation market is fragmented in nature. Some of the major players in the market include (not in any particular order) Armacell, Knauf Group, Johns Manville, Owens Corning, and Saint-Gobain, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Increasing Demand for Energy Efficiency from the Construction Industry

- 4.1.2 Increasing Application of Flexible Piping Insulation

- 4.1.3 Other Drivers

- 4.2 Market Restraints

- 4.2.1 Availability of Alternatives

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By Material

- 5.1.1 Aerogel

- 5.1.2 Cross-Linked Polyethylene

- 5.1.3 Elastomer

- 5.1.4 Fiberglass

- 5.1.5 Other Materials

- 5.2 By Insulation Type

- 5.2.1 Acoustic Insulation

- 5.2.2 Electrical Insulation

- 5.2.3 Thermal Insulation

- 5.3 By Geography

- 5.3.1 Asia - Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia - Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Ranking Analysis

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Altana AG

- 6.3.2 Armacell

- 6.3.3 Cabot Corporation

- 6.3.4 Etex Group

- 6.3.5 Fletcher Insulation

- 6.3.6 Johns Manville

- 6.3.7 Kingspan Group

- 6.3.8 Knauf Insulation

- 6.3.9 Owens Corning

- 6.3.10 Saint-Gobain

- 6.3.11 Superlon Holdings Berhad

- 6.3.12 Thermaxx Jackets

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emerging Opportunity for Aerogel Insulation in Electric Vehicles

- 7.2 Other Opportunities

フレキシブル断熱材:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日