アルファメチルスチレン:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Alpha Methylstyrene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1689954

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

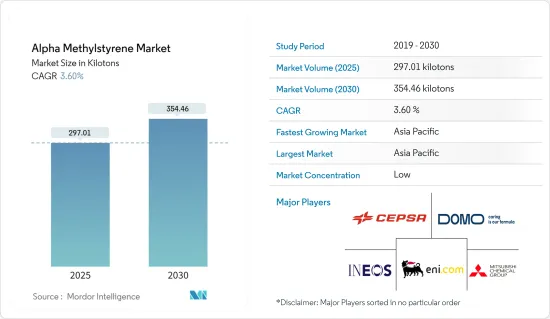

アルファメチルスチレンの市場規模は2025年に297.01キロトンと推計され、予測期間(2025-2030年)のCAGRは3.6%で、2030年には354.46キロトンに達すると予測されます。

COVID-19は、すべての産業が製造プロセスを停止したため、市場にマイナスの影響を与えました。ロックダウン、社会的距離、貿易制裁が世界のサプライ・チェーン・ネットワークに大規模な混乱を引き起こしました。しかし、この状況は2021年には回復しており、予測期間中は市場に利益をもたらすと予想されます。

主なハイライト

- 中期的には、ABS樹脂の製造需要の増加とエレクトロニクス分野におけるアルファメチルスチレンの需要増加が市場を牽引する主な要因です。

- その反面、アルファメチルスチレンの製造時に排出される有害廃棄物が市場の成長を抑制する可能性が高いです。

- 耐久性のあるワックスと耐熱性接着剤の需要の増加は、今後数年間、市場にとって好機となる可能性が高いです。

- アジア太平洋地域が最も高い市場シェアを占めており、予測期間中、この地域が市場を独占する可能性が高いです。

アルファメチルスチレン市場動向

自動車産業が市場を独占

- アルファメチルスチレンはABS樹脂製造の中間体です。さらに、ABS樹脂は自動車産業において金属の代替として使用されています。軽量化を追求する様々な自動車部品にABS樹脂が使用されています。ABSは一般的に、ダッシュボード部品、シートバック、シートベルト部品、ハンドル、ドアローナー、ピラートリム、インストルメントパネルなどの部品に使用されています。

- OICA(Organization Internationale des Constructeurs d'Automobiles)によると、世界の自動車生産台数は2022年に8,501万台に達し、2021年の8,020万台と比較して6%の成長率を示しました。

- さらに、電気自動車の生産台数の増加は、市場調査の市場需要を高める可能性が高いです。例えば、EV Volumesによると、2022年には合計1,050万台のBEVとPHEVが新たに納入され、2021年と比較して55%増加しました。

- アジア太平洋地域は、世界で最も価値のある自動車メーカーの本拠地です。中国、インド、日本、韓国などの新興諸国は、製造基盤を強化し、効率的なサプライチェーンを構築して収益性を高めるために努力してきました。

- 中国汽車工業協会(CAAM)によると、中国は世界最大の自動車生産拠点であり、2022年の自動車総生産台数は2,720万台と、昨年の2,610万台から3.4%増加します。

- 欧州では、ドイツは重要な自動車メーカーのひとつです。ドイツ自動車工業会(VDA)によると、ドイツの2022年7月の自動車生産台数は26万3,400台で、2021年同期比7%の伸びを記録しました。さらに、ドイツでは電気自動車の需要が増加しています。そのため、さまざまな企業が同国で電気自動車の生産台数を増やしています。例えば、2023年6月、フォードはドイツのハイテク生産施設であるケルン電気自動車センターの落成を発表しました。

- 北米では、OICAによると、2022年の自動車生産台数は1,770万台で、2021年の約1,610万台に比べて10%増加しました。

- このため、予測期間中、自動車生産の拡大とともにアルファメチルスチレンの需要も伸びると予想されます。

アジア太平洋がアルファメチルスチレン市場を独占する

- アジア太平洋地域は、アルファメチルスチレン市場において世界的に顕著なシェアを占めており、予測期間中も市場を独占すると予想されます。

- 国家統計局が発表したデータによると、中国のタイヤ産業は大幅な成長を遂げており、これは国内および国際市場におけるタイヤ需要の増加を反映しています。

- 中国国家統計局によると、2023年5月現在、中国のプラスチック製品の月間生産量はおよそ600万トンです。2020年1月以降、プラスチック製品の月間生産量が最も多かったのは2021年12月の795万トンでした。

- さらに、中国は化学加工のハブであり、世界の化学製品の大部分を占めています。世界最大の化学品市場である中国では、2023年には化学品生産の伸びがやや鈍化すると予想されます。ロシアとウクライナの戦争に続き、化学業界は2022年、エネルギーと原材料コストの上昇、パンデミック、経済の不確実性、政治的混乱によってすでに緊張している世界・サプライ・チェーンがさらにボトルネックになることを経験しました。BASFの化学産業アウトルックによれば、2023年の中国の化学生産は5.9%の微減となる見込みです。しかし、新しい化学プラントの建設への投資が増加しており、中期的にはAMSの需要を下支えします。

- インドは、アジア太平洋地域で中国に次ぐゴムの最大生産国・消費国のひとつです。インドでは、生産されるゴムの65%以上が自動車用タイヤ(50%)と自転車用タイヤ・チューブ(15%)の製造に使用されています。さらに、同国には66近いタイヤ生産工場と約41のタイヤ生産企業があります。

- IBEFによると、2022年4月~9月のプラスチック輸出総額は63億8,000万米ドルでした。この間、プラスチック原材料、医療品、パイプ・継手の輸出は、前年同期比で32.3%、24.8%、17.9%増加しました。

- このように、様々な産業からの需要の増加は、予測期間中にこの地域で調査された市場を促進すると予想されます。

アルファメチルスチレン産業の概要

アルファメチルスチレン市場は細分化されています。市場の主要企業には、ENI S.p.A.、INEOS、Cepsa、三菱化学、Domo Chemicalsなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- ABS樹脂製造の需要増加

- エレクトロニクス分野におけるアルファメチルスチレン需要の増加

- 抑制要因

- アルファメチルスチレン製造時の有害廃棄物排出

- その他の阻害要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 用途

- ABS製造

- プラスチック添加剤と中間体

- 接着剤

- コーティング剤

- その他の用途

- エンドユーザー産業

- タイヤ

- 自動車

- エレクトロニクス

- プラスチック

- その他のエンドユーザー産業

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州

- 世界のその他の地域

- 南米

- 中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- AdvanSix

- Altivia

- Cepsa

- Chang Chun Group

- Deepak

- Domo Chemicals

- Eni S.P.A.

- INEOS

- Kraton Corporation

- Kumho P&B Chemicals.,inc.

- Mitsubishi Chemical Corporation

- Prasol Chemicals Limited

- Rosneft

- Seqens

- SI Group, Inc.

- Solvay

- Yangzhou Lida Chemical Co., Ltd.

第7章 市場機会と今後の動向

- 耐久性ワックスと耐熱性接着剤の需要増加

- その他の機会

目次

The Alpha Methylstyrene Market size is estimated at 297.01 kilotons in 2025, and is expected to reach 354.46 kilotons by 2030, at a CAGR of 3.6% during the forecast period (2025-2030).

COVID-19 negatively impacted the market as all the industries halted their manufacturing processes. Lockdowns, social distances, and trade sanctions triggered massive disruptions to global supply chain networks. However, the condition is recovered in 2021, which is expected to benefit the market during the forecast period.

Key Highlights

- In the medium term, the major factors driving the market studied are the increasing demand for the manufacturing of ABS resins and increasing demand for alpha-methyl styrene in the electronics segment.

- On the flip side, hazardous waste release during the production of alpha methyl styrene is likely to restrain the market growth.

- Increase in demand for durable waxes and heat-resistant adhesives is likely to act as an opportunity for the market in coming years.

- Asia-Pacific accounted for the highest market share, and the region is likely to dominate the market during the forecast period.

Alpha Methylstyrene Market Trends

Automotive Industry to Dominate the Market

- Alpha methyl styrene is an intermediate for the production of ABS resin. Further, ABS resin is used as a replacement for metal in the automotive industry. Various automotive parts that look for weight reduction factors use ABS thermoplastic. ABS is commonly used for parts that include dashboard components, seat backs, seat belt components, handles, door loners, pillar trim, and instrument panels.

- According to the Organization Internationale des Constructeurs d'Automobiles (OICA), global automotive vehicle production reached 85.01 million in 2022, with a growth rate of 6% as compared to 80.20 million vehicles manufactured in 2021, thereby indicating an increased demand for alpha methyl styrene from the automotive industry.

- Furthermore, the rising production of electric vehicles is likely to enhance the market demand for the market-studied. For instance, according to the EV Volumes, a total of 10.5 million new BEVs and PHEVs were delivered during 2022, an increase of 55 % compared to 2021.

- Asia-Pacific region is home to some of the world's most valuable vehicle manufacturers. Developing countries such as China, India, Japan, and South Korea have been working hard to strengthen the manufacturing base and develop efficient supply chains for greater profitability.

- According to the China Association of Automobile Manufacturers (CAAM), China has the largest automotive production base in the world, with a total vehicle production of 27.2 million units in 2022, registering an increase of 3.4 % compared to 26.1 million units produced last year.

- In Europe, Germany is among the vital manufacturer of vehicles. According to the German Association of the Automotive Industry (VDA), Germany produced 263,400 units of cars in July 2022, registering a growth rate of 7% compared to the same period in 2021. Additionally, the demand for electric cars is increasing in Germany. Thus, various companies are increasing the production volume of electric cars in the country. For instance, in June 2023, Ford announced the inauguration of the Cologne Electric Vehicle Center, a hi-tech production facility in Germany.

- In North America, according to the OICA, automotive production in 2022 accounted for 17.7 million units, an increase of 10% compared to that in 2021, which was around 16.1 million units.

- Therefore, the demand for alpha methyl styrene is expected to grow with the expanding automotive production during the forecast period.

Asia-Pacific to Dominate Alpha Methyl Styrene Market

- Asia-Pacific holds a prominent share in the alpha-methylstyrene market globally and is expected to dominate the market during the period of forecast.

- As per the data released by the National Bureau of Statistics, China's tire industry is experiencing substantial growth, reflecting the increasing demand for tires in the domestic as well as international markets.

- According to the National Bureau of Statistics of China, as of May 2023, China produces roughly 6 million metric tons of plastic products monthly. Since January 2020, the highest monthly output of plastic products was recorded in December 2021, at 7.95 million metric tons.

- Furthermore, China is a hub for chemical processing, accounting for a major chunk of global chemicals. In China, the world's largest chemicals market, a slight slowdown in chemical production growth is expected in 2023. Following Russia and Ukraine war, the chemical industry experienced a year marked by further bottlenecks in global supply chains already strained by rising energy and raw material costs, pandemic, economic uncertainty, and political turmoil in 2022. Continuing on the tumultuous grounds, China is expected to register a slightly weaker growth of 5.9% in chemical production in 2023, as per the BASF's chemical industry outlook. However, the increasing investments in the construction of new chemical plants support the demand for AMS in the mid-term.

- India is one of the largest producers and consumers of rubber after China in the Asia-Pacific region. In India, over 65% of the rubber produced is used for manufacturing automotive (50%) and bicycle tires and tubes (15%). Moreover, the country has almost 66 tire-producing plants and about 41 tire-producing companies.

- According to IBEF, total plastics exports between April-September 2022 stood at USD 6.38 billion. During this period, the exports of plastic raw materials, medical items, and pipes and fittings increased by 32.3%, 24.8%, and 17.9% over the same time last year.

- Thus, rising demand from various industries is expected to drive the market studied in the region during the forecast period.

Alpha Methylstyrene Industry Overview

The alpha methyl styrene market is fragmented in nature. Some of the major companies in the market include ENI S.p.A., INEOS, Cepsa, Mitsubishi Chemical Corporation, and Domo Chemicals, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand For the Manufacturing of ABS Resins

- 4.1.2 Increasing Demand For Alpha-methyl Styrene In the Electronics Segment

- 4.2 Restraints

- 4.2.1 Hazardous Waste Release During the Production of Alpha Methyl Styrene

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume and Value)

- 5.1 Application

- 5.1.1 ABS Manufacture

- 5.1.2 Plastic Additives and Intermediates

- 5.1.3 Adhesives

- 5.1.4 Coatings

- 5.1.5 Other Applications

- 5.2 End-user Industry

- 5.2.1 Tire

- 5.2.2 Automotive

- 5.2.3 Electronics

- 5.2.4 Plastics

- 5.2.5 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AdvanSix

- 6.4.2 Altivia

- 6.4.3 Cepsa

- 6.4.4 Chang Chun Group

- 6.4.5 Deepak

- 6.4.6 Domo Chemicals

- 6.4.7 Eni S.P.A.

- 6.4.8 INEOS

- 6.4.9 Kraton Corporation

- 6.4.10 Kumho P&B Chemicals.,inc.

- 6.4.11 Mitsubishi Chemical Corporation

- 6.4.12 Prasol Chemicals Limited

- 6.4.13 Rosneft

- 6.4.14 Seqens

- 6.4.15 SI Group, Inc.

- 6.4.16 Solvay

- 6.4.17 Yangzhou Lida Chemical Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increase in Demand for Durable Waxes and Heat-resistant Adhesives

- 7.2 Other Opportunities

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日