グリコール:市場シェア分析、産業動向・統計、成長予測(2025~2030年)

Glycol - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1689948

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

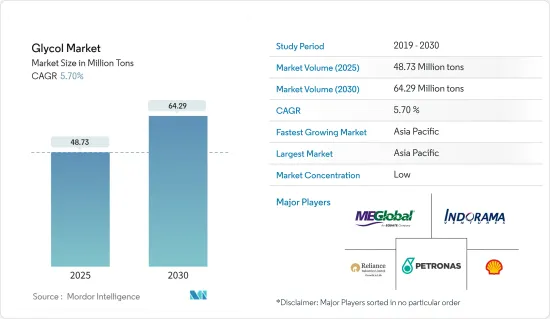

グリコールの市場規模は2025年に4,873万トンと推計され、2030年には6,429万トンに達すると予測され、市場推計・予測期間(2025~2030年)のCAGRは5.7%です。

2020年、COVID-19パンデミックは世界的なロックダウンとソーシャルディスタンス措置を引き起こし、サプライチェーンを混乱させ、多くの製造部門を閉鎖しました。これはグリコール市場に悪影響を与えました。しかし、市場は2021年には回復し、予測期間中は安定した成長が見込まれます。

主なハイライト

- 短期的には、繊維産業での使用量の増加と飲食品分野からの需要の増加が、市場の需要を牽引する主な要因です。

- 毒性と環境への懸念が市場成長の妨げになると予想されます。

- しかしながら、バイオベースのグリコールに対する需要の増加は、市場に新たな機会をもたらすと期待されています。

- アジア太平洋地域が世界市場を独占し、中国、インド、日本からの需要が大半を占めると予想されます。

グリコール市場の動向

繊維産業での使用の増加

- 主要原料であるプロピレングリコールとエチレングリコールは、様々な製品、特にポリエステル繊維を生産する上で極めて重要です。これらの繊維は衣料品、椅子張り、カーペット、枕などに使用されています。

- エチレングリコールの最も顕著な用途はポリエステル繊維で、繊維産業を支配しています。さらに、グリコールエーテルは繊維市場で染浴添加剤として重要な役割を果たし、色合いの正確さ、均染性、堅牢度などの特性を高め、染色温度とサイクル時間を短縮します。

- 世界の繊維分野が増加傾向にあるため、グリコール類の需要は増加する傾向にあります。World Trade Statistical Review 2023とUN Comtradeのデータによると、2022年には中国、EU、インドが繊維輸出のトップ3で、合わせて世界の繊維輸出の72.1%を占めています。

- 中国はスパンデックスの生産と消費の両方で世界をリードしています。中国化学繊維協会のスパンデックス部門は、2023年末までに中国のスパンデックス生産能力は123万9,500トン/年に達すると報告しました。調整後の生産能力は143トン/年の純増となり、2022年比で13%の伸びとなります。

- インド最古の産業のひとつであるインドの繊維部門は、GDPの2.3%、工業生産の13%、輸出の12%を占め、経済に大きな影響を与えています。インドブランドエクイティ財団のデータによると、2023年の繊維・アパレル輸出総額は367億米ドルに達しました。2024年には359億米ドルに達すると推定されています。また、既製服および付属品の輸出額は142億3,000万米ドルでした。2024年度には、インド最大の市場である米国への繊維製品・衣料品の輸出は、総輸出額の32.7%を占めます。このような輸出の急増は、インドにおけるグリコールの需要を高めると予想されます。

- National Council of Textile Organization(NCTO)のデータによると、米国は世界第3位の繊維輸出国です。米国の繊維産業は8,000以上の製品を軍に供給し、2023年には648億米ドルの出荷額を達成しました。同国は繊維研究開発の世界的リーダーとして際立っています。

- 一流のファッションブランドで有名なイタリアは、繊維分野の変革を目の当たりにしており、技術の進歩を取り入れながら近代化に努めています。ITMAによると、イタリアには約45,000社の繊維・ファッション企業があります。

- Comex Stat(ブラジル)のデータによると、2023年にはアルゼンチンがブラジルの繊維・アパレル輸出の主要輸出先となり、その額は2億3,000万米ドルを超えます。パラグアイとウルグアイがそれに続き、それぞれ1億3,300万米ドルと7,800万米ドルの輸出でした。

- アフリカでは、南アフリカが大陸の主要繊維輸出国に浮上し、2023年の輸出額は38億米ドルに達しました。Apparel and Textile Association of South Africa(南アフリカ・アパレルテキスタイル協会)のデータによると、これらの輸出の大部分は、主にテクニカルテキスタイルで、航空会社向けのものです。

- このような力学を考慮すると、世界のグリコール市場は今後数年間で成長する態勢を整えています。

アジア太平洋が市場を独占

- アジア太平洋地域がグリコール消費をリードし、市場を独占し、予測期間中に最も急成長する地域に浮上します。この急成長は、特に中国、インド、韓国、日本、東南アジア諸国など、包装、飲食品、自動車、輸送、化粧品、繊維など、多様なエンドユーザー産業からの需要が高まっていることが背景にあります。

- アジア太平洋地域では、輸出や国内消費の増加に伴い、飲食品や消費財などの業界が包装材料を求める傾向が強まっています。この地域の包装市場は、特にeコマースの台頭により、包装食品や動きの速い消費財への意欲が高まっていることに支えられています。その利点から、エンジニアリングプラスチック製品、特にPET容器とボトルは、包装分野で大幅な上昇を目の当たりにしています。PETはエチレングリコール、テレフタル酸ジメチル(DMT)、テレフタル酸から派生します。

- 中国の包装産業は、世界の重要な包装産業のひとつです。中国の包装産業が一貫して成長しているのは、経済が拡大し、購買力を持つ中間層が急増しているためです。さらに、同国の包装産業は成長が見込まれています。中国政府の報告書によると、同産業の評価額は2025年までに2兆人民元(2,900億米ドル)に達すると推定されています。

- 食品加工産業の台頭により、インドでは食品包装の需要が高まると予想されています。食品加工省は、インド経済の主要企業である食品加工部門が食品市場全体の32%を占めていることを強調しています。市場推計・予測によると、同産業の生産高は2025年までに5,350億米ドルに達し、年率15.2%で成長し、市場の成長を支えています。

- 包装以外にも、エチレングリコールは自動車のラジエーターの凍結防止剤として重要な役割を果たしています。自動車業界は活気に満ちており、中国が世界をリードしています。国際自動車建設機構(OICA)のデータによると、2023年の中国の自動車生産台数は3,016万台で、2022年の2,702万台から12%増加しました。このような自動車生産の急増は、グリコール市場を強化する構えです。

- 韓国は、Hyundai、Samsung、Kiaといった有名ブランドを擁する成熟した自動車産業を誇っています。自動車工業協会と韓国自動車研究院の予測では、2024年の国内自動車生産台数は1.0%増加し、436万台に達すると予想されています。この成長は、市場の需要を促進すると予想されます。

- 中国の化粧品市場は過去10年間で急成長を遂げました。中国国家統計局のデータによると、2023年の化粧品小売売上高は約4,141億7,000万人民元(585億米ドル)に達しました。第2、第3の都市で需要が急増し、男性用スキンケアも顕著に増加していることから、グリコール市場は成長するとみられます。

- 韓国は世界の美容市場のトップ10にランクされ、その革新性、天然成分の使用、魅力的な包装で称賛されています。食品医薬品安全省(MFDS)のデータによると、韓国の化粧品輸出は2023年に85億米ドルに達し、世界第4位の地位を確保しました。

- 手ごろな価格で高品質の医薬品を提供することで知られるインドの医薬品部門は、急速な科学的進歩の軌道に乗っています。政府は、2030年までに500億米ドルから1,300億米ドル、2047年までに4,500億米ドルに急増すると予測しています。こうした成長は、予測期間中の医薬品製造におけるグリコール需要の高まりを示唆しています。

- このような力学を考えると、アジア太平洋地域は、様々な産業における需要の急増に牽引され、大きな成長を遂げることになります。

グリコール産業の概要

グリコール市場は細分化されています。主なプレーヤーは、Shell PLC、MEGlobal、Indorama Ventures Public Company Limited、Reliance Industries Limited、PETRONAS Chemicals Group Berhadなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 繊維産業における使用の増加

- 飲食品分野からの需要増加

- その他

- 抑制要因

- 毒性と環境への懸念

- その他

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- タイプ別

- エチレングリコール

- モノエチレングリコール(MEG)

- ジエチレングリコール(DEG)

- トリエチレングリコール(TEG)

- ポリエチレングリコール(PEG)

- プロピレングリコール

- その他

- エチレングリコール

- エンドユーザー産業別

- 自動車・輸送

- 包装

- 飲食品

- 化粧品

- 医薬品

- 繊維

- その他

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- カタール

- アラブ首長国連邦

- ナイジェリア

- エジプト

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- BASF SE

- China Petrochemical Corporation

- China Sanjiang Fine Chemical Co. Ltd

- Dow

- Huntsman International LLC

- India Glycols Limited

- Indian Oil Corporation Ltd

- Indorama Ventures Public Company Limited

- INEOS

- LOTTE Chemical Corporation

- LyondellBasell Industries Holdings B.V.

- MEGlobal

- Mitsubishi Chemical Group Corporation

- Nouryon

- PETRONAS Chemicals Group Berhad

- Petrorabigh

- Reliance Industries Limited

- SABIC

- Shell PLC

第7章 市場機会と今後の動向

- バイオベースのグリコール需要の増加

- その他の機会

目次

The Glycol Market size is estimated at 48.73 million tons in 2025, and is expected to reach 64.29 million tons by 2030, at a CAGR of 5.7% during the forecast period (2025-2030).

In 2020, the COVID-19 pandemic triggered nationwide lockdowns and social distancing measures, disrupting supply chains and shuttering numerous manufacturing sectors. This adversely affected the glycol market. However, the market recovered in 2021, and it is expected to grow steadily during the forecast period.

Key Highlights

- Over the short term, increasing usage in the textile industry and growing demand from the food and beverage sector are the major factors driving the demand for the market studied.

- However, toxicity and environmental concerns are expected to hinder the market's growth.

- Nevertheless, increasing demand for bio-based glycols is expected to create new opportunities for the market studied.

- Asia-Pacific is expected to dominate the global market, with the majority of demand coming from China, India, and Japan.

Glycol Market Trends

Increasing Usage in the Textile Industry

- Key raw materials propylene glycol and ethylene glycol are pivotal in producing various products, most notably polyester fibers. These fibers find applications in clothing, upholstery, carpets, and pillows.

- Ethylene glycol's most prominent application is in polyester fibers, which dominate the textile industry. Additionally, glycol ethers play a crucial role as dyebath additives in the textile market, enhancing properties like shade accuracy, level dyeing, colorfastness, and reducing dyeing temperatures and cycle times.

- With the global textile sector on the rise, the demand for glycols is set to increase. Data from the World Trade Statistical Review 2023 and UN Comtrade highlighted that in 2022, China, the European Union, and India were the top three textile exporters, collectively accounting for 72.1% of global textile exports.

- China leads the world in both spandex production and consumption. The Spandex Branch of China Chemical Fibers Association reported that by the end of 2023, China's spandex capacity reached 1.2395 million tons/year. After adjustments, this marked a net capacity increase of 143 kt/year, translating to a 13% growth from 2022.

- India's textile sector, one of the nation's oldest industries, impacts the economy significantly, accounting for 2.3% of the GDP, 13% of industrial production, and 12% of exports. Data from the Indian Brand Equity Foundation showed that the total textile and apparel exports reached USD 36.7 billion in 2023. It is estimated to reach USD 35.9 billion in 2024. Additionally, exports of readymade garments and accessories were valued at USD 14.23 billion. In FY 2024, exports of textiles and apparel to the United States, India's largest market, constituted 32.7% of the total export value. This surge in exports is expected to bolster the demand for glycols in India.

- According to data from the National Council of Textile Organization (NCTO), the United States ranks as the world's third-largest textile exporter. The US textile industry supplies over 8,000 products to the military and achieved shipments worth USD 64.8 billion in 2023. The country stands out as a global leader in textile research and development.

- Renowned for its prestigious fashion brands, Italy is witnessing a transformation in its textile sector, striving for modernization while embracing technological advancements. ITMA reports that Italy boasts around 45,000 textile and fashion companies.

- Data from Comex Stat (Brazil) revealed that in 2023, Argentina was the primary destination for Brazilian textile and apparel exports, valued at over USD 230 million. Paraguay and Uruguay followed, with exports worth USD 133 million and USD 78 million, respectively.

- In Africa, South Africa emerged as the continent's leading textile exporter, with exports reaching USD 3.8 billion in 2023. A significant portion of these exports, primarily technical textiles, catered to aeronautics companies, as reported by the data from the Apparel and Textile Association of South Africa.

- Given these dynamics, the global glycol market is poised for growth in the coming years.

Asia-Pacific to Dominate the Market

- Asia-Pacific is poised to lead glycol consumption, dominating the market and emerging as the fastest-growing region during the forecast period. This surge is fueled by escalating demands from diverse end-user industries, including packaging, food and beverage, automotive, transportation, cosmetics, and textiles, particularly in nations like China, India, South Korea, Japan, and various Southeast Asian countries.

- In Asia-Pacific, industries such as food and beverage and consumer goods are increasingly seeking packing materials, driven by rising exports and domestic consumption. The region's packaging market is buoyed by a growing appetite for packaged foods and fast-moving consumer goods, especially with the rise of e-commerce. Due to their advantages, engineering plastic products, notably PET containers and bottles, are witnessing a significant uptick in the packaging sector. PET is derived from ethylene glycol, dimethyl terephthalate (DMT), or terephthalic acid.

- China's packaging industry is one of the significant global packaging industries. The consistent growth of China's packaging industry can be attributed to its expanding economy and a burgeoning middle class with increased purchasing power. Furthermore, the packaging industry in the country is expected to grow. A report by the Chinese government estimates the industry achieving a valuation of CNY 2 trillion (USD 290 billion) by 2025.

- With the rising food processing industry, India anticipates heightened demand for food packaging. The Ministry of Food Processing highlights that the food processing sector, a major player in India's economy, represents 32% of the overall food market. Projections estimate the industry's output to hit USD 535 billion by 2025, growing at an annual rate of 15.2%, supporting the market's growth.

- Beyond packaging, ethylene glycol plays a crucial role as an anti-freezing agent in car radiators. The automotive landscape is vibrant, with China leading globally. Data from the Organisation Internationale des Constructeurs d'Automobiles (OICA) revealed that in 2023, China produced 30.16 million vehicles, a 12% increase from 27.02 million in 2022. This surge in automobile production is poised to bolster the glycol market.

- South Korea boasts a mature automotive industry with notable brands like Hyundai, Renault, Samsung, and Kia. Projections from the Automobile Manufacturers Association and Korea Automobile Research Institute anticipate a 1.0% rise in domestic automobile production for 2024, reaching 4.36 million units. This growth is expected to drive demand in the market studied.

- China's cosmetics landscape has seen rapid growth over the past decade. Data from the National Bureau of Statistics of China indicated that in 2023, retail sales of cosmetics reached approximately CNY 414.17 billion (~USD 58.5 billion). With demand surging in second and third-tier cities and a notable rise in men's skincare, the glycol market is set to thrive.

- South Korea ranks among the top ten global beauty markets and is celebrated for its innovation, use of natural ingredients, and attractive packaging. According to the data from the Ministry of Food and Drug Safety (MFDS), Korea's cosmetics exports hit USD 8.5 billion in 2023, securing fourth position globally.

- India's pharmaceutical sector, known for its affordable and high-quality medicines, is on a trajectory of rapid scientific advancements. The government forecasts the industry's value to soar from USD 50 billion to USD 130 billion by 2030 and an ambitious USD 450 billion by 2047. Such growth signals a heightened demand for glycol in pharmaceutical drug production during the forecast period.

- Given these dynamics, Asia-Pacific is set for significant growth, driven by surging demands across various industries.

Glycol Industry Overview

The glycol market is fragmented in nature. The major players include Shell PLC, MEGlobal, Indorama Ventures Public Company Limited, Reliance Industries Limited, and PETRONAS Chemicals Group Berhad.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Drivers

- 4.1.1 Increasing Usage in the Textile Industry

- 4.1.2 Growing Demand from the Food and Beverage Sector

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Toxicity and Environmental Concerns

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 Market Segmentation (Market Size in Volume)

- 5.1 By Type

- 5.1.1 Ethylene Glycol

- 5.1.1.1 Monoethylene Glycol (MEG)

- 5.1.1.2 Diethylene Glycol (DEG)

- 5.1.1.3 Triethylene Glycol (TEG)

- 5.1.1.4 Polyethylene Glycol (PEG)

- 5.1.2 Propylene Glycol

- 5.1.3 Other Types

- 5.1.1 Ethylene Glycol

- 5.2 By End-user Industry

- 5.2.1 Automotive and Transportation

- 5.2.2 Packaging

- 5.2.3 Food and Beverage

- 5.2.4 Cosmetics

- 5.2.5 Pharmaceuticals

- 5.2.6 Textile

- 5.2.7 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Qatar

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 China Petrochemical Corporation

- 6.4.3 China Sanjiang Fine Chemical Co. Ltd

- 6.4.4 Dow

- 6.4.5 Huntsman International LLC

- 6.4.6 India Glycols Limited

- 6.4.7 Indian Oil Corporation Ltd

- 6.4.8 Indorama Ventures Public Company Limited

- 6.4.9 INEOS

- 6.4.10 LOTTE Chemical Corporation

- 6.4.11 LyondellBasell Industries Holdings B.V.

- 6.4.12 MEGlobal

- 6.4.13 Mitsubishi Chemical Group Corporation

- 6.4.14 Nouryon

- 6.4.15 PETRONAS Chemicals Group Berhad

- 6.4.16 Petrorabigh

- 6.4.17 Reliance Industries Limited

- 6.4.18 SABIC

- 6.4.19 Shell PLC

7 Market Opportunities and Future Trends

- 7.1 Increasing Demand for Bio-based Glycols

- 7.2 Other Opportunities

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日