導電性シリコーン:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Conductive Silicone - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1689938

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

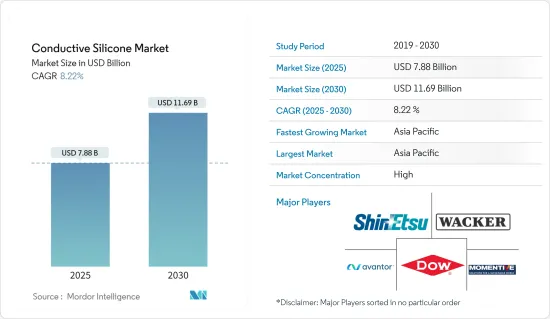

導電性シリコーンの市場規模は2025年に78億8,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは8.22%で、2030年には116億9,000万米ドルに達すると予測されています。

COVID-19の発生は当初、導電性シリコーンのサプライチェーンを混乱させました。その後、急速なデジタル化、遠隔学習やリモートワークの導入により、電子機器の需要が急増しました。そのため、導電性シリコーン市場は容易にパンデミック前の段階まで回復しました。

主なハイライト

- 電子機器における導電性シリコーンの需要の増加と、太陽電池産業における導電性シリコーンの使用量の増加が、導電性シリコーンの市場需要を高めると予想されます。

- 一方、EMIシールドにおける導電性シリコーンの代替品は、予測期間中の市場成長を抑制すると予想されます。

- マイクロ流体デバイスのような医療機器技術の進歩は、市場に新たな可能性をもたらしています。

- アジア太平洋地域は、自動車、エレクトロニクス、通信産業からの需要増加により、導電性シリコーン市場を独占しています。

導電性シリコーン市場動向

エレクトロニクス分野の成長による需要拡大

- 導電性シリコーンは、導電性、熱伝導性、柔軟性、耐腐食性などの優れた特性を持つため、電気・電子用途に広く使用されています。

- 導電性シリコーンの使用に伴う優れた導電性は、電気機器にとって理想的な材料となります。シリコーンの導電性粒子は電流の伝達を可能にし、信号、データおよび力の伝達を要求する適用のためにそれを有用にさせる。

- 中国は世界最大の電子機器生産基地です。スマートフォン、テレビ、その他の個人用電子機器などの電子製品は、エレクトロニクス分野で最も高い成長を記録しました。

- 同国は電子製品に対する需要が大きいです。この幅広い需要から利益を得るため、中国は「メイド・イン・チャイナ2025」計画のような戦略的イニシアティブに着手しました。この計画の下、中国政府は2030年までに生産高3,050億米ドルを達成し、国内需要の80%を満たすという目標を発表しました。さらに、中国はスマートフォンの生産拠点であり、導電性シリコーンの需要を大幅に押し上げています。

- 日本電子情報技術産業協会(JEITA)が発表したデータによると、2022年、日本のエレクトロニクス産業の総生産額は約11兆1,243億円(843億4,000万米ドル)に達し、前年から8%近く増加しました。

- ドイツは欧州最大の電子産業国です。ドイツ市場は欧州最大、世界第5位の電気・電子市場です。ドイツ電気電子協会によると、2022年には2,200億ユーロ(2,348億4,000万米ドル)以上を記録しました。

- ドイツの電気・電子関連企業は、国内外で160万人以上の従業員を雇用しています。また、国内の研究開発従業員の30%がエレクトロニクスとマイクロテクノロジーの分野で働いています。

- さらに、エレクトロニクスはドイツの輸出全体の13%を占めています。ドイツのエレクトロニクスおよびデジタル産業の名目輸出は、年率7.0%の成長を記録し、2023年4月には190億ユーロ(209億3,000万米ドル)に達します。今年1~4月の同部門の海外納入額は前年同期比10.7%増の842億ユーロ(927億5,000万米ドル)に達しました。

- フランス2030投資計画の一環として、フランス政府は2030年までに様々な電子技術開発のための学術研究エコシステムを支援するため、約8億ユーロ(8億8,000万米ドル)の投資を計画しています。

- したがって、前述の要因は近い将来、導電性シリコーンの需要を押し上げると予測されます。

アジア太平洋地域が市場を独占する

- アジア太平洋地域は導電性シリコーンの最大かつ急成長市場です。エレクトロニクス、自動車、発電産業での利用が増加していることなどが、アジア太平洋地域の導電性シリコーン需要を牽引しています。

- 中国、インド、日本、インドネシア、ベトナムなど、この地域の国々は発電プロジェクトへの投資が増加しており、導電性シリコーン市場の成長を後押ししています。

- また、帯電防止包装の重要性が高まっており、帯電時の埃対策や電気・電子機器の機能性・長寿命維持のために、電子機器における導電性シリコーンの利用が増加すると予想されます。アジアは電気・電子機器の最大の生産国で、中国、日本、インド、ASEAN諸国などが生産をリードしています。

- 中国は世界で最も広範な電子機器生産の拠点です。スマートフォン、テレビ、その他のパーソナル・デバイスなどの電子製品が最も高い成長を記録しました。

- 公式データによると、2023年、Huahong Groupの無錫は、65/55-40nmをカバーするプロセスグレード、月産能力8万3,000個の12インチ特殊プロセス生産ラインの建設を計画しています。

- さらに、Nexchip Semiconductor Corporationは2023年、12インチウエハー製造プロジェクトに約29億米ドルを投資しました。

- 最近、中国ではエネルギー需要の高まりから、さまざまな再生可能エネルギー・プロジェクトに投資しています。2023年11月、中国政府は230GWの風力・太陽光発電容量の導入を計画しました。同国は2060年のカーボンニュートラル目標達成を目指し、2023年にさまざまな風力・太陽光発電プロジェクトに総額1,400億米ドルを投資しました。

- 2021年から2025年にかけての送電網への投資予算は4,550億米ドルで、過去10年間から60%増加しました。また、2020年から系統連系蓄電容量を倍増させ、2023年には67GWに達します。

- したがって、上記の要因は、予測期間中にこの地域における導電性シリコーンの需要を促進すると予想されます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 調査範囲

- 調査範囲

- 調査の前提条件と市場定義

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- エレクトロニクス産業からの需要拡大

- 太陽電池産業での用途拡大

- 抑制要因

- EMIシールドにおける導電性シリコーンの代替品

- バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 製品タイプ別

- エラストマー

- 樹脂

- ゲル

- その他の製品タイプ(ペースト、ギャップフィラー、接着剤、グリース)

- 用途別

- 接着剤およびシーラント

- 熱インターフェース材料

- 封止剤およびポッティングコンパウンド

- コンフォーマルコーティング

- その他の用途(バイオメディカル、光触媒)

- エンドユーザー産業別

- 自動車

- 建設

- 発電

- 電気・電子

- その他のエンドユーザー産業(産業機械、消費財、航空宇宙)

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- カタール

- アラブ首長国連邦

- ナイジェリア

- エジプト

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場ランキング分析

- 主要企業の戦略

- 企業プロファイル

- 3M

- Avantor Inc.

- CHT Germany GmbH

- Dongguan City Betterly New Materials Co. Ltd

- Dow

- Elkem ASA

- Euro Technologies

- Henkel AG & Co. Kgaa

- Momentive

- Parker Hannifin Corporation

- Polymax Ltd

- Shin-Etsu Chemical Co. Ltd

- Silicone Solutions

- Soliani Emc Srl

- Specialty Silicone Products Inc.

- Wacker Chemie AG

第7章 市場機会と今後の動向

- 医療機器における新たな技術開発

目次

The Conductive Silicone Market size is estimated at USD 7.88 billion in 2025, and is expected to reach USD 11.69 billion by 2030, at a CAGR of 8.22% during the forecast period (2025-2030).

The COVID-19 outbreak initially disrupted the conductive silicone supply chain. Later on, demand for electronics surged due to rapid digitization and the adoption of distance learning and remote work. Thus, the conductive silicone market readily recovered to its pre-pandemic stage.

Key Highlights

- The increasing demand for conductive silicone in electronic devices and its increasing usage in the solar industry are expected to raise the market demand for conductive silicone.

- On the other hand, the alternative to conductive silicone in EMI shielding is anticipated to restrain market growth during the forecast period.

- Advancements in medical device technology, such as microfluidic devices, are opening up new possibilities within the market.

- The Asia-Pacific region dominates the conductive silicone market, owing to rising demand from the automotive, electronics, and telecommunications industries.

Conductive Silicone Market Trends

Growth in the Electronics Segment to Augment the Demand

- Conductive silicone is extensively used in electrical and electronics applications because of its superior properties such as electrical conductivity, thermal conductivity, flexibility, and corrosion resistance.

- The superior electrical conductivity associated with the use of conductive silicone makes it the ideal material for electric devices. Silicone's conductive particles enable the transfer of electrical current, making it useful for applications that require the transmission of signals, data, and power.

- China is the largest base for electronics production in the world. Electronic products such as smartphones, TVs, and other personal electronic devices recorded the highest growth in the electronics segment.

- The country has a large demand for electronic products. To benefit from this extensive demand, China has embarked on strategic initiatives like the "Made in China 2025" plan. Under this plan, the Chinese government has announced its goal to reach an output of USD 305 billion by 2030 and, therefore, meet 80% of its domestic demand. Moreover, China is an industrial hub for smartphone production, significantly boosting the demand for conductive silicone.

- According to the data released by the Japan Electronics and Information Technology Industries Association (JEITA), in 2022, the total production value of the electronics industry in Japan amounted to around JPY 11,124.3 billion (USD 84.34 billion), showcasing a rise of nearly 8% from the previous year.

- Germany has the largest electronic industry in Europe. The German market is Europe's largest and the world's fifth-largest electrical and electronics market. It had registered more than EUR 220 billion (USD 234.84 billion) in 2022, according to the Germany Electrical and Electronics Association.

- Electrical and electronic companies in Germany employ a workforce of more than 1.6 million at home and abroad. Also, 30% of all R&D employees in the country are working in the field of electronics and microtechnology.

- Additionally, electronics constitute up to 13% of the country's overall exports. The nominal exports of the German electro and digital industry witnessed an annual growth of 7.0% to reach EUR 19.0 billion (USD 20.93 billion) in April 2023. In the first four months of this year, the sector's aggregated deliveries abroad experienced a Y-o-Y growth of 10.7%, reaching a value of EUR 84.2 billion (USD 92.75 billion).

- As part of the France 2030 investment plan, the French government plans to invest nearly EUR 800 million (USD 880 million) to support the academic research ecosystem for the development of various electronic technologies by 2030.

- Therefore, the aforementioned factors are projected to boost the demand for conductive silicone in the near future.

Asia-Pacific to Dominate the Market

- The Asia-Pacific region stands to be the largest and fastest-growing market for conductive silicone. Factors such as the increasing utilization in the electronics, automotive, and power generation industries have been driving the demand for conductive silicone in Asia-Pacific.

- Countries in the region, such as China, India, Japan, Indonesia, and Vietnam, are witnessing increasing investments in power generation projects, boosting the growth of the conductive silicone market.

- The heightened significance of anti-static packaging for dust control during electric charge and sustaining functionality and longevity of electrical and electronic devices is anticipated to increase the utilization of conductive silicone in electronics. Asia is the largest producer of electrical and electronic devices, with countries like China, Japan, India, and ASEAN countries leading production.

- China is the most extensive base for electronics production in the world. Electronic products such as smartphones, TVs, and other personal devices recorded the highest growth.

- According to official data, in 2023, Huahong Group's Wuxi planned to build a 12-inch specialty process production line with a process grade covering 65/55-40 nm and a monthly production capacity of 83,000 pieces.

- Furthermore, Nexchip Semiconductor Corporation invested around USD 2.9 billion in 2023 in the 12-inch wafer manufacturing project.

- Recently, China has been investing in various renewable energy projects due to the growing demand for energy in the country. In November 2023, the Government of China planned to install 230 GW of wind and solar capacity. The country invested a total of USD 140 billion in 2023 in various wind and solar projects with the aim of achieving its 2060 carbon-neutral target.

- The country has budgeted USD 455 billion in grid investments from 2021-2025, an increase of 60% from the previous decade. It also doubled its grid-connected energy storage capacity from 2020 to reach 67 GW in 2023.

- Hence, the factors mentioned above are expected to drive the demand for conductive silicone in the region during the forecast period.

Conductive Silicone Industry Overview

The conductive silicone market is consolidated in nature. The major players operating in the market (not in any particular order) include Wacker Chemie AG, DOW, Shin-Etsu Chemical Co. Ltd, Momentive, and Avantor Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 SCOPE OF THE REPORT

- 1.1 Scope of the Study

- 1.2 Study Assumptions and Market Definition

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from the Electronics Industry

- 4.1.2 Increasing Usage in the Solar Industry

- 4.2 Restraints

- 4.2.1 Alternative to Conductive Silicone in EMI Shielding

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size In Value)

- 5.1 By Product Type

- 5.1.1 Elastomers

- 5.1.2 Resins

- 5.1.3 Gels

- 5.1.4 Other Product Types (Pastes, Gap Fillers, Adhesives, and Greases)

- 5.2 By Application

- 5.2.1 Adhesives and Sealants

- 5.2.2 Thermal Interface Materials

- 5.2.3 Encapsulant and Potting Compounds

- 5.2.4 Conformal Coatings

- 5.2.5 Other Applications (Biomedical and Photocatalysis)

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Construction

- 5.3.3 Power Generation

- 5.3.4 Electrical and Electronics

- 5.3.5 Other End-user Industries (Industrial Machinery, Consumer Goods, and Aerospace)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Nordic Countries

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Qatar

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 South Africa

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Avantor Inc.

- 6.4.3 CHT Germany GmbH

- 6.4.4 Dongguan City Betterly New Materials Co. Ltd

- 6.4.5 Dow

- 6.4.6 Elkem ASA

- 6.4.7 Euro Technologies

- 6.4.8 Henkel AG & Co. Kgaa

- 6.4.9 Momentive

- 6.4.10 Parker Hannifin Corporation

- 6.4.11 Polymax Ltd

- 6.4.12 Shin-Etsu Chemical Co. Ltd

- 6.4.13 Silicone Solutions

- 6.4.14 Soliani Emc Srl

- 6.4.15 Specialty Silicone Products Inc.

- 6.4.16 Wacker Chemie AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 New Technological Developments in Medical Devices

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日