|

市場調査レポート

商品コード

1689936

米国のビデオ監視:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)US Video Surveillance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国のビデオ監視:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

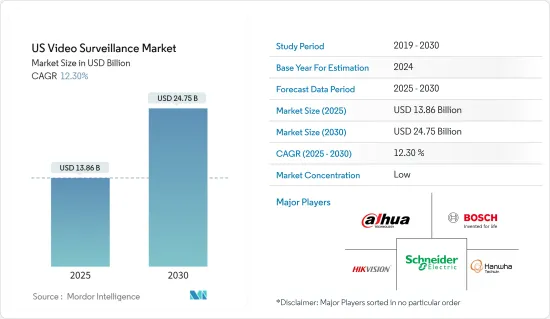

米国のビデオ監視市場規模は2025年に138億6,000万米ドルと推定され、市場推計・予測期間(2025~2030年)のCAGRは12.3%で、2030年には247億5,000万米ドルに達すると予測されます。

米国では、監視カメラはホテル、レストラン、オフィスビルなど民間の小売・商業施設で最も一般的です。

主なハイライト

- 同国では、スマートホームセキュリティカメラの普及も進んでおり、市場調査対象がさらに拡大する可能性があります。AIベースのビデオ解析は効率をさらに高め、特にスマートシティアプリケーションにおいて、ビジネスにセキュリティ関連以外の多くの洞察を提供します。最近の動向では、アマゾンがAWS Panorama技術を発表し、インテグレーターが開発者と協力して、メーカーに関係なく、ビデオ監視用にカスタマイズされたディープラーニングとビデオ分析アプリを簡単に作成できるようになりました。

- 米国では近年、ビデオ監視の利用が拡大しています。統合型ビデオ監視には、ユーザーが効率的かつ迅速に情報を送信できる技術が搭載されています。しかし、この機能は、ハッキングやキャプチャされたシナリオの機密性を危険にさらす可能性があります。悪意のある操作は、無許可のユーザーへのビデオ映像やクリップのスムーズなトランスミッションを通じて行われます。

- ここ数年、ビデオ監視システムはモノのインターネット(IoT)の一部となっています。IoTセンサーは多くの場合、空気中の汚染物質のレベル、騒音レベル、振動など、人間以上のものを検知することができます。このため、ユーザーは脅威のあるエリアを監視できるようになるため、多くのカメラベースの監視ソリューションに統合される態勢が整っています。

- しかし、他のIoTシステムと同様、内在するセキュリティ・リスクがユーザーのプライバシーを著しく侵害する可能性があります。主にディープラーニングに基づく高度な機械学習技術が研究され、武器検知、火災検知、店内ショッピング、顔認識センサー、異常検知など、複数のタスクを自動化するために最新のビデオ監視システムに統合されています。

- 主要な業界別では、従業員の行動を変化させ、より良い結果をもたらすためのより良いプラットフォームとして、監視が信頼されています。企業による監視戦術は従業員に大きな悪影響を及ぼし、プライバシーの問題の発生、ストレスの増大、アイデンティティの喪失をもたらしました。しかし、どのような侵入的な技術もそうであるように、公共のビデオカメラを導入する利点は、コストや危険性とのバランスを取る必要があります。

米国のビデオ監視市場動向

ビデオアナリティクスが市場を大きく成長させる

- 米国では多くの大企業がより高度なセキュリティ監視システムを必要としているため、ビデオアナリティクス分野の開発に最も貢献すると期待されています。この業界は主に、技術的知識へのアクセスのしやすさ、リアルタイムで実用的な情報に対する公開会社のニーズの高まり、技術的にアップグレードされた公共保護インフラに対する国のニーズの拡大によって後押しされています。

- 革新的な能力へのアクセスは、多数の重要なテクノロジー・ビジネスの存在によって促進されてきました。米国はビデオ監視の主要部門を掌握しており、業界を前進させています。さらに、テロ攻撃の可能性から、当局は多くの地域に高度な監視装置を設置せざるを得なくなっています。さらに、さまざまな業界でセキュリティ上の脅威を特定するために、ビデオ分析システムを導入しています。

- 米国では、監視カメラがアナログカメラに取って代わるケースが増えています。こうしたカメラには、強力な顔や被写体の識別技術が搭載されており、監視資料を継続的に収集し、膨大な公開データベースを作成しています。さらに、この国の民主主義の枠組みは、CCTVシステムの導入を強く支持しています。例えば、国土安全保障省は、ビデオ・セキュリティー・カメラを配備するために、地方自治体に対して何十億米ドルもの安全資金を支払っています。連邦政府の援助はビデオ分析の需要を高め、予測期間中のビデオ監視機器の開発を促進すると予想されます。

- 主要技術プレイヤーの地域開拓の増加は、予測期間中の市場成長に貢献すると見られています。最近では、Cisco MerakiがKloudspotと協業し、従業員や消費者により安全でスマートなワークスペースを提供できるよう企業を支援しています。

住宅が大きな市場ポテンシャルを持つ

- 住宅用ビデオ監視ソリューションは、1台以上の録画デバイスをネットワークに接続し、取得した映像や音声データを特定の場所に転送します。写真はリアルタイムで視聴されるか、中央ステーションに送信されて録画・保存されます。脅威の増加や犯罪行為によるセキュリティ監視グッズのニーズの高まりが、国内のビデオ監視システムの需要を牽引しています。

- スマートホームの出現により、ここ数年、住宅分野でのビデオ監視システムの注目度が高まっています。この分野で実装される監視システムは、監視やアクセス制御など、さまざまなアプリケーションを持っています。これらのシステムには、動体検知機能や暗視機能も搭載されています。

- 同国では空き巣の発生率が高いため、近年は監視カメラなどのセキュリティシステムの導入が増加しており、スピードの低下に役立っています。例えば、FBIによると、2022年10月、米国における2021年の空き巣発生率は人口10万人当たり271.1件でした。これは、強盗発生率が人口10万人あたり308件であった前年から低下したことを表しています。

- ビデオ解析は、住宅用セキュリティビデオ監視技術において重要な役割を果たし、アラームの誤作動を減らし、不審な状況を検知するシステムの能力を高めます。1万世帯のブロードバンド世帯を対象とした業界専門家による消費者調査によると、米国のブロードバンド世帯のうち、スマートビデオドアベルを購入する意向のある26%の世帯では、購入する特定のビデオドアベルを選択する際に、人工知能(AI)または高度な分析機能が不可欠であると評価する人がほとんどでした。

米国のビデオ監視業界の概要

米国のビデオ監視市場は競争が激しく、影響力のあるプレーヤーで構成されています。この市場は、内外の市場勢力による効果的な圧力により、成長率が高まっています。市場に参入している主要企業には、Dahua Technology、Hikvision Digital Technology、Hanwha Techwin、Schneider Electric SE、Robert Bosch GmbHなどがあります。

2022年9月、映像中心のインテリジェントIoTソリューションの世界的リーダーであるDahua Technology U.S.A.社は、消費者に夜間照明の選択肢を増やすLiteシリーズの斬新なカメラを発表しました。VU-MORE Colorカメラは、赤外線と白色光のツインアップライトを搭載しており、照度やシーンの活動に応じて自動的に展開されます。

2022年2月、ボッシュ・セキュリティ・システムズ社は、完全な状況情報を提供する革新的なM.I.C. I.P. Fusion 9000i 9mmカメラを発表しました。今回追加されたM.I.C. I.P. fusion 9000i 9mmカメラは、既存のM.I.C. I.P. fusion 9000iのラインアップを補完するもので、電力・ユーティリティ施設、データセンター、その他の保護レベルの高い施設の敷地境界沿いなど、境界検知アプリケーションに完全な状況情報を提供します。メタデータ・フュージョンと呼ばれる革新的な方法を使用して、カメラは熱と光学ストリーミング・ビデオからの物体識別情報を組み合わせ、1枚の画像に表示することができます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 市場促進要因

- IPカメラの価格低下と分析およびソフトウェアの技術進歩

- 有効な商業モデルとしてのビデオ監視サービス(VSaaS)の出現

- 市場の課題

- プライバシーとセキュリティの問題

- 高解像度画像のための大容量ストレージの必要性

- 米国で活動する中国企業に課される規制

- 市場機会

- COVID-19が業界に与える影響の評価

- 市街地監視の主なケーススタディと導入事例

- 主要セグメントの主要企業が採用しているベストプラクティス

第5章 市場セグメンテーション

- タイプ

- カメラ

- ビデオ管理システムとストレージ

- ビデオ解析

- エンドユーザー

- 商業

- 小売

- 国家インフラと都市監視

- 輸送機関

- 住宅

- その他のエンドユーザー

第6章 競合情勢

- 企業プロファイル

- Dahua Technology Co. Ltd

- Robert Bosch GmbH

- Hikvision Digital Technology Co. Ltd

- Hanwha Techwin

- Schneider Electric SE

- Honeywell Security Group

- Panasonic Corporation

- NEC Corporation

- Genetec Inc.

- Axis Communications AB(Canon)

- CP Plus International

- Avigilon Corporation

- Allied Telesis Inc.

- Infinova Corporation

- Palantir Technologies

- Cisco Systems Inc.

- Agent Video Intelligence Ltd

- Verint Systems Inc.

- FLIR Systems Inc.

- Qognify Inc.

第7章 投資分析

第8章 市場機会と今後の動向

The US Video Surveillance Market size is estimated at USD 13.86 billion in 2025, and is expected to reach USD 24.75 billion by 2030, at a CAGR of 12.3% during the forecast period (2025-2030).

In the United States, surveillance cameras are most common among private-sector retail and commercial establishments, such as hotels, restaurants, and office complexes.

Key Highlights

- The country is also witnessing the rising adoption of smart home security cameras, which may further expand the scope of the market studied. AI-based video analytics further enhance efficiencies, offering many non-security-related insights for businesses, especially in smart city applications. Recently, Amazon announced the AWS Panorama technology that enables integrators to work with a developer to easily create customized deep learning and video analytic apps for video surveillance cameras, regardless of manufacturer.

- The use of video security cameras has expanded in recent years in the United States. Integrated video security cameras include technology that enables users to send information efficiently and quickly. This capability, however, may jeopardize the confidentiality of the scenario that has been hacked or captured. Malicious operations are performed via the smooth transmission of video footage and clips to unauthorized users.

- Over the past several years, video surveillance systems have become a part of the Internet of Things (IoT). An IoT sensor can often detect even more than humans, such as levels of pollutants in the air, noise level, and vibrations. For this reason, they are poised to be integrated into many camera-based surveillance solutions as they allow users to monitor threatened areas.

- However, like other IoT systems, inherent security risks can lead to significant violations of a user's privacy. Advanced machine learning techniques, primarily based on deep learning, are being researched and integrated within modern video surveillance systems for automating multiple tasks, including weapon detection, fire detection, in-store shopping, sensors of face recognition, and anomaly detection.

- Major industry verticals are trusting surveillance as a better platform for altering the behavior of employees to yield better results. Corporate companies' surveillance tactics had highly adverse effects on employees, resulting in the emergence of privacy issues, increased stress, and the loss of identity. However, like any intrusive technology, the benefits of deploying public video cameras must be balanced against the costs and dangers.

US Video Surveillance Market Trends

Video Analytics to Witness Significant Market Growth

- The United States is expected to provide the most to the development video analytics sector since many significant enterprises there require higher security surveillance systems. The industry is primarily fueled by the accessibility of technological knowledge, companies' increasing need for actionable information in real-time, and the country's expanding need for technically upgraded public protection infrastructure.

- Accessibility to innovative capabilities has been facilitated by the existence of numerous important technology businesses. The United States controls the major sector for video surveillance, propelling the industry forward. Further, the potential of terrorist strikes has forced authorities to install advanced monitoring equipment in a number of areas. Moreover, they have implemented video analytics systems to identify security threats in various industries.

- In the United States, surveillance cameras are increasingly replacing analog cameras. Such cameras have powerful facial and subject identification technology that continuously harvests surveillance material and produces a massive public database. Furthermore, the nation's democratic framework strongly favors implementing CCTV systems. For example, the Homeland Security Department pays local authorities billions of dollars in safety funding to deploy video security cameras. Federal assistance is expected to increase the demand for video analytics, propelling the development of video surveillance equipment over the forecast period.

- Major technology players' increasing regional developments are expected to contribute to market growth over the forecast period. Recently, Cisco Meraki collaborated with Kloudspot to assist businesses in providing safer and smarter workspaces for their workers and consumers.

Residential Addresses a Major Market Potential

- Residential video surveillance solutions connect one or more recording devices to a network and transfer the acquired video or audio data to a specific location. The photos are watched in real-time or sent to a central station for recording and retention. The growing need for security observation goods due to rising threats and criminal operations is driving the demand for video surveillance systems in the country.

- The emergence of smart homes increased the prominence of video surveillance systems in the residential segment in the past few years. The surveillance systems implemented in this sector have varied applications, such as monitoring and access control. These systems are also equipped with motion detection and night vision features.

- The high burglary rate in the country has increased the adoption of security systems such as video surveillance cameras over recent years, which has helped decrease the speed. For instance, according to the FBI, in October 2022, the national burglary rate in the United States was 271.1 incidences per 100,000 people in 2021. This represents a drop from the prior year when the burglary rate was 308 instances per 100,000 people

- Video analytics play a significant role in residential security video surveillance technology, reducing false alarm instances and enhancing the system's ability to detect suspicious situations. The industry expert consumer survey of 10,000 broadband households found that among the 26% of US broadband households that intend to buy a smart video doorbell, most rated artificial intelligence (AI) or advanced analytics capabilities as vital when selecting a specific video doorbell to purchase.

US Video Surveillance Industry Overview

The United States video surveillance market is highly competitive and consists of influential players. The market shows an augmented growth rate due to the effective pressure exerted by the market forces, both internally and externally. Some of the major players operating in the market include Dahua Technology Co. Ltd., Hikvision Digital Technology Co. Ltd, Hanwha Techwin, Schneider Electric SE, and Robert Bosch GmbH.

In September 2022, Dahua Technology U.S.A. Inc., a global leader in video-centric intelligent IoT solutions, introduced a novel camera in its Lite Series that provides consumers with more alternatives for nighttime lighting. The VU-MORE Color camera features twin infrared and white-light uplights that are automatically deployed depending on illumination and activity in the scene.

In February 2022, Bosch Security Systems Inc. introduced its innovative M.I.C. I.P. Fusion 9000i 9mm cameras, which provided complete situational information. The additional M.I.C. I.P. fusion 9000i 9mm camera complements the existing M.I.C. I.P. fusion 9000i line-up by providing complete contextual information to perimeter detecting applications, including along a site boundary at an electricity or utility facility, data center, or other high protective installations. Using an innovative method termed metadata fusion, the cameras can combine object identification information from heat and optical streaming video and show it in a single picture.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Market Drivers

- 4.4.1 Diminishing IP Camera Prices, Coupled with Technological Advancements in Analytics and Software

- 4.4.2 Emergence of Video Surveillance-as-a-Service (VSaaS) as a Viable Commercial Model

- 4.5 Market Challenges

- 4.5.1 Privacy and Security Issues

- 4.5.2 Need for High-capacity Storage for High-resolution Images

- 4.5.3 Restrictions Imposed on Chinese Companies Operating in the United States

- 4.6 Market Opportunities

- 4.7 Assessment of COVID-19 Impact on the Industry

- 4.8 Key Case Studies and Implementation Use-cases for City Surveillance

- 4.9 Best Practices Adopted by Key Players in Key Segments

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Cameras

- 5.1.2 Video Management Systems and Storage

- 5.1.3 Video Analytics

- 5.2 End User

- 5.2.1 Commercial

- 5.2.2 Retail

- 5.2.3 National Infrastructure and City Surveillance

- 5.2.4 Transportation

- 5.2.5 Residential

- 5.2.6 Other End Users

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Dahua Technology Co. Ltd

- 6.1.2 Robert Bosch GmbH

- 6.1.3 Hikvision Digital Technology Co. Ltd

- 6.1.4 Hanwha Techwin

- 6.1.5 Schneider Electric SE

- 6.1.6 Honeywell Security Group

- 6.1.7 Panasonic Corporation

- 6.1.8 NEC Corporation

- 6.1.9 Genetec Inc.

- 6.1.10 Axis Communications AB (Canon)

- 6.1.11 CP Plus International

- 6.1.12 Avigilon Corporation

- 6.1.13 Allied Telesis Inc.

- 6.1.14 Infinova Corporation

- 6.1.15 Palantir Technologies

- 6.1.16 Cisco Systems Inc.

- 6.1.17 Agent Video Intelligence Ltd

- 6.1.18 Verint Systems Inc.

- 6.1.19 FLIR Systems Inc.

- 6.1.20 Qognify Inc.