架橋剤:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Crosslinking Agents - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 160 Pages

- 納期

- 2~3営業日

- 商品コード

- 1689921

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

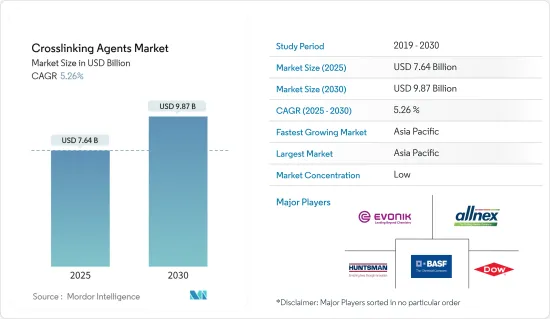

架橋剤の市場規模は2025年に76億4,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは5.26%で、2030年には98億7,000万米ドルに達すると予測されます。

COVID-19のパンデミックは市場にマイナスの影響を与えたが、建設と自動車セクターの世界の力強い成長により、予測期間中は堅調に成長すると予測されます。

主なハイライト

- 市場を牽引している主な要因は、各種コーティング剤に対する需要の高まりと、高性能架橋剤への注目の高まりです。

- 一方、自己架橋剤の存在が市場成長の妨げになる可能性もあります。

- 予測期間中、革新的なコーティングに対する需要の増加は、世界の架橋剤市場における大きなチャンスです。

- アジア太平洋地域が市場を独占しており、予測期間中に最も高いCAGRで成長すると予想されます。

架橋剤市場の動向

装飾用コーティングの需要増加

- 装飾用コーティング剤は、住宅、商業施設、施設、工業用建物の内外面に塗布されます。世界の建設セクターの増加が、装飾用コーティング剤における各種架橋剤の需要を押し上げています。

- アジア太平洋地域の建設セクターは世界最大です。人口の増加、中間所得層の増加、都市化により、健全なペースで増加しています。

- 中国はショッピングセンター建設における主要国のひとつです。中国は、ショッピングセンター建設における主要国のひとつです。中国には約4,000のショッピングセンターがあり、2025年までにさらに7,000がオープンすると推定されています。

- さらに、国家開発改革委員会によると、中国政府は2019年に推定投資額約1,420億米ドルの26のインフラ・プロジェクトを承認し、2023年までに完了すると推定され、現在も進行中です。住宅需要の高まりは、公共部門と民間部門の両方において、同国の住宅建設を促進すると思われます。

- 米国は世界最大の建設産業のひとつです。米国国勢調査局によると、米国で実施された新規建設の年間金額は、2020年の1兆4,995億7,000万米ドルに対し、2021年には1兆6,264億4,400万米ドルに達します。

- カナダでは、アフォーダブル・ハウジング・イニシアチブ(AHI)、ニュー・ビルディング・カナダ・プラン(NBCP)、メイド・イン・カナダなど、さまざまな政府プロジェクトがこの分野の拡大を支援しています。

- AIA(米国建築家協会)の建設コンセンサス予測パネルによると、非住宅建築建設支出は2022年に5.4%拡大し、2023年には6.1%の拡大へと強まる見通しです。2023年までには、主要な商業・工業・施設カテゴリーはすべて、少なくともそれなりに健全な伸びを示すと予測されています。

- このようなすべての要因が、予測期間中に装飾コーティングの需要を促進すると予測されます。

アジア太平洋地域が市場を独占する

- アジア太平洋地域は、中国の自動車部門が高度に発展していることに加え、建築や様々な産業部門を発展させるために長年にわたって継続的な投資が行われていることから、世界市場を独占すると予想されます。

- 中国政府は、2025年までに電気自動車の普及率が20%になると予測しています。2022年上半期には、中国本土で240万台以上のEVが顧客に納車され、これは中国における自動車販売台数の26%に相当します。同国での自動車生産台数の増加に伴い、自動車用コーティング剤の需要は増加するとみられ、架橋剤市場にも影響を与えると予想されます。

- 中国の自動車生産は、世界の自動車生産に大きく貢献しています。OICAによると、中国は世界最大の自動車生産拠点であり、2021年の自動車総生産台数は2,608万台で、昨年の2,523万台に比べて3%の増加を記録します。また、中国汽車工業協会(CAAM)によると、2022年1~7月の自動車生産台数は1,457万台で、前年比31.5%の伸びを記録しました。

- インドでは、Make in India改革のもと、多国籍企業がインドに拠点を設けるのに有利な規制が政府から提示されています。また、製造業におけるFDI比率の向上は、外国企業による投資をさらに誘致する可能性が高いです。これにより、今後数年間の工業生産が下支えされることが期待されます。

- 経済産業省の報告によると、日本の工業生産は2021年に3%以上増加しました。日本には電子機器やその他の部品の大規模な生産拠点があり、その大部分は北米、欧州、アジア太平洋の経済圏に輸出されています。電子情報技術産業協会(JEITA)が発表したデータによると、日本の電子・IT企業の世界生産は2022年末までに前年比2%のプラス成長を記録すると予想されています。

- 様々な用途における塗料・コーティング産業の継続的な成長が、今後数年間にわたり架橋剤市場を牽引していくと予想されます。

架橋剤産業の概要

架橋剤市場は、多くのプレーヤーが市場で競合しており、収益面では部分的に断片化されています。市場の主要企業としては、Evonik Industries AG、BASF SE、ダウ、Huntsman International LLC、Allnex GMBHなどが挙げられる(順不同)。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 数多くのコーティングに対する需要の増加

- 高性能架橋剤への注目の高まり

- 抑制要因

- 自己架橋剤の存在

- バリューチェーン分析

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- タイプ

- アミド

- アミン

- アミノ

- カルボジイミド

- イソシアネート

- その他のタイプ

- 用途

- 自動車コーティング

- 装飾用コーティング

- 工業用コーティング

- 包装用コーティング

- その他の用途

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場ランキング分析

- 主要企業の戦略

- 企業プロファイル

- BASF SE

- Aditya Birla Chemicals

- Allnex GMBH

- Covestro AG

- Evonik Industries AG

- Hexion

- Huntsman International LLC

- Dow

- Wanhua Chemical Group Co. Ltd

- Nisshinbo Chemical Inc.

- NIPPON SHOKUBAI CO. LTD

- Mitsubishi Chemical Corporation

- KUMHO P&B CHEMICALS INC.

第7章 市場機会と今後の動向

- 革新的なコーティング剤への需要

目次

The Crosslinking Agents Market size is estimated at USD 7.64 billion in 2025, and is expected to reach USD 9.87 billion by 2030, at a CAGR of 5.26% during the forecast period (2025-2030).

The COVID-19 pandemic negatively impacted the market but is projected to grow steadily in the forecast period owing to strong global growth in the construction and automotive sectors.

Key Highlights

- The major factors driving the market are rising demand for various coatings and an increased emphasis on high-performance crosslinking agents.

- On the other hand, the presence of self-crosslinking agents might hamper the market growth.

- During the forecast period, the increasing demand for innovative coatings is a major opportunity in the global crosslinking agent market.

- Asia-Pacific has dominated the market and is expected to grow with the highest CAGR during the forecast period.

Crosslinking Agents Market Trends

Increasing Demand for Decorative Coatings

- Decorative coatings are applied to the interior and exterior surfaces of residential, commercial, institutional, and industrial buildings. The increase in the construction sector worldwide is, in turn, boosting the demand for various crosslinking agents in decorative coatings.

- The construction sector in the Asia-Pacific region is the largest in the world. It is increasing at a healthy rate, owing to the rising population, increase in middle-class income, and urbanization.

- China is one of the leading countries concerning the construction of shopping centers. China is one of the leading countries in shopping-center construction. China has almost 4,000 shopping centers, while 7,000 more are estimated to be open by 2025.

- Moreover, according to National Development and Reform Commission, the Chinese government approved 26 infrastructure projects at an estimated investment of about USD 142 billion in 2019, which are estimated to be completed by 2023 and are ongoing. The growing demand for housing is likely to drive residential construction in the country, both in the public and private sectors.

- The United States has one of the world's largest construction industries. According to the United States Census Bureau, the annual value for new construction put in place in the United States accounted for USD 1,626,444 million in 2021, compared to USD 1,499,570 million in 2020.

- In Canada, various government projects, including the Affordable Housing Initiative (AHI), New Building Canada Plan (NBCP), and Made in Canada, have been supporting the expansion of the sector.

- According to the AIA (American Institute of Architects) Construction Consensus Forecast Panel, nonresidential building construction spending is expected to expand by 5.4% in 2022 and strengthen to a 6.1% expansion in 2023. By 2023, all the major commercial, industrial, and institutional categories are projected to witness at least reasonably healthy gains.

- All such factors are anticipated to drive the demand for decorative coating during the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific is expected to dominate the global market, owing to the highly developed automotive sector in China, coupled with the continuous investments done in the region to advance the architectural and various industrial sectors through the years.

- The government of China estimates a 20% penetration rate of electric vehicles by 2025. China has the largest and fastest-growing EV market in the world, In H1 2022, over 2.4 million EVs were delivered to customers in mainland China equating to 26% of all car sales in China. With the increasing production of vehicles in the country, the demand for automotive coating is likely to ascend, which is anticipated to influence the market for crosslinking agents.

- Automobile manufacturing in China is a significant contributor to global automobile production. According to OICA, China has the largest automotive production base in the world, with a total vehicle production of 26.08 million units in 2021, registering an increase of 3% compared to 25.23 million units produced last year. Further, according to the China Association of Automobile Manufacturers (CAAM), in the first 7 months of 2022, the country has produced 14.57 million units of cars, registering a growth rate of 31.5% Year on Year.

- In India, under the Make in India reform, the government of the country has offered favorable regulations for multinationals to set up their bases in India. Moreover, an increase in FDI share in the manufacturing industry is further likely to attract investments by foreign players. Thereby, it is expected to support industrial production in the upcoming years.

- As per the reports by the Ministry of Economy Trade and Industry (METI), industrial production in Japan increased by over 3% in 2021. The country has a large production base for electronics and other components, the majority of which is exported to the economies in North America, Europe, and Asia-Pacific. According to the data published by the Japan Electronics and Information Technology (JEITA), Global production by Japanese electronics and IT companies is expected to record positive growth of 2% year on year by the end of 2022.

- Continuous growth in the paint and coatings industry for various applications is expected to drive the market for crosslinking agents through the years to come.

Crosslinking Agents Industry Overview

The crosslinking agents market is partially fragmented in nature in terms of revenue with many players competing in the market. Some of the major players in the market include (not in any particular order) Evonik Industries AG, BASF SE, Dow, Huntsman International LLC, and Allnex GMBH, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demad for Numerous Coatings

- 4.1.2 Increasing Focus on High-Performance Crosslinking Agents

- 4.2 Restraints

- 4.2.1 Presence of Self-Crosslinking Agents

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Amide

- 5.1.2 Amine

- 5.1.3 Amino

- 5.1.4 Carbodiimide

- 5.1.5 Isocyanate

- 5.1.6 Other Types

- 5.2 Application

- 5.2.1 Automotive Coatings

- 5.2.2 Decorative Coatings

- 5.2.3 Industrial Coatings

- 5.2.4 Packaging Coatings

- 5.2.5 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 Aditya Birla Chemicals

- 6.4.3 Allnex GMBH

- 6.4.4 Covestro AG

- 6.4.5 Evonik Industries AG

- 6.4.6 Hexion

- 6.4.7 Huntsman International LLC

- 6.4.8 Dow

- 6.4.9 Wanhua Chemical Group Co. Ltd

- 6.4.10 Nisshinbo Chemical Inc.

- 6.4.11 NIPPON SHOKUBAI CO. LTD

- 6.4.12 Mitsubishi Chemical Corporation

- 6.4.13 KUMHO P&B CHEMICALS INC.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Demand for Innovative Coatings

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 160 Pages

- 納期

- 2~3営業日