化粧品用顔料:市場シェア分析、産業動向・統計、成長予測(2025~2030年)

Cosmetic Pigments - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1689909

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

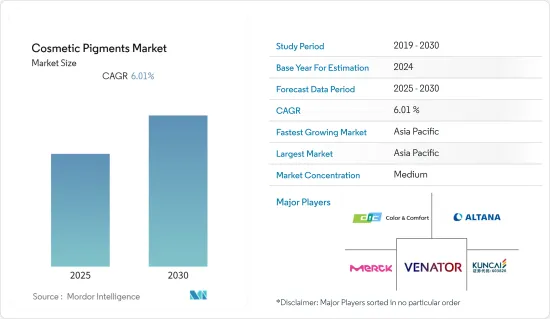

化粧品用顔料市場は予測期間中に6.01%のCAGRで推移する見込みです。

COVID-19のパンデミックは市場にマイナスの影響を与えました。これは、ロックダウンや制限により製造施設や工場が閉鎖されたためです。サプライチェーンと輸送の混乱はさらに市場に障害をもたらしました。しかし、2021年には業界は回復し、市場の需要は回復しました。

主なハイライト

- 短期的には、アジア太平洋地域における化粧品需要の増加と有機顔料需要の急拡大が市場成長を牽引する要因のひとつです。

- その反面、美容向上のための新しい医療技術が市場の成長を妨げると予想されます。

- しかし、有機的に生産された化粧品用顔料に対する需要の高まりは、予測期間中に数多くの機会を提供すると予想されます。

- アジア太平洋地域は最大の市場であり、中国、インド、日本、韓国などの国々からの消費の増加により、予測期間中に最も急成長する市場になると予想されます。

化粧品顔料の市場動向

市場を独占する無機顔料セグメント

- 無機顔料は炭素をベースとしない化学化合物であり、通常は溶液から沈殿した金属塩です。

- これらの顔料は、金属イオンを基礎とする不溶性化合物と定義することができます。無機顔料は一般的に光の影響に対して非常に耐性があります。なぜなら、結合の破壊を発生させるのに必要なエネルギーは、太陽光によって供給されるエネルギーよりも大きいからです。

- ほとんどの無機顔料は高温で製造され、一般的にプロセス温度の影響を受けないため、熱に強いです。

- 無機顔料は、天然物(陶土、炭素鉱床など)に由来する不溶性の金属化合物から構成されるか、合成されます。無機顔料は酸化鉄、酸化クロム、ウルトラマリン、マンガンバイオレット、白色顔料、真珠光沢効果で構成されています。

- 無機顔料の色の高い安定性と高い粒子分散性により、化粧品製品の製造において人気のある選択肢となっています。無機顔料の分散性の利点は、今後数年間、業界の成長率を高め、世界の無機顔料市場の発展が期待されます。

- 例えば、ドイツは欧州最大の化粧品市場であり、フランスと英国がそれに続きます。例えば、IKWによると、2022年のドイツの美容・パーソナルケア市場規模は143億3,300万ユーロ(151億411万米ドル)と推定され、2021年と比較して5.36%の増加を示しています。したがって、同国における美容・パーソナルケア製品の市場価値の増加は、同国における化粧品用顔料市場の需要増加をもたらすと予想されます。

- 男性用スキンケア市場は、可処分所得の増加、有名人の支持、個人の衛生や定期的な身だしなみを意識するようになった男性の間での製品発売の増加の結果として拡大しています。スキンケア製品に対する男性の嗜好は、伝統的な身だしなみを整えるためのものにとどまらない広がりを見せています。例えば、L'Orealによると、2022年にはスキンケア製品が世界の化粧品市場の41%を占めるといいます。

- さらに、広告や販促活動の増加により、米国の消費者は化粧品を購入しています。例えば、2022年の米国化粧品市場の売上は180億米ドルを超えます。2022年に最も好調なセグメントは顔用化粧品で、売上高は約65億米ドル、次いで目用化粧品セグメントです。これに対し、自然派化粧品市場の年間売上高は16億米ドルでした。

- したがって、上記の要因により、無機顔料セグメントは予測期間中に化粧品顔料市場を独占すると思われます。

市場を独占するアジア太平洋地域

- 現在、アジア太平洋地域が化粧品顔料の世界市場を独占しています。中国と日本は、この地域における化粧品顔料の主要な消費者です。

- 中国、インド、ASEAN諸国などの化粧品生産能力と消費の増加は、この地域の化粧品顔料の需要を増加させると予想されます。

- 中国国家統計局によると、2022年1月、中国の化粧品小売貿易収入は約91億8,000万米ドルに達し、2023年1月には約97億6,000万米ドルに達しました。中国の第二、第三の都市で化粧品の需要がさらに拡大するにつれて、化粧品顔料市場は近い将来に成長の勢いを維持すると予想されます。さらに、スキンケアに対する男性の意識の変化が、中国の男性用化粧品市場の活況を促進しています。

- Euromonitor Internationalの調査によると、インドの美容・パーソナルケア(BPC)市場は総額150億米ドルで世界第8位、成長率は~10%です。さらに、2030年までに市場は倍増し、スキンケアと化粧品がこの成長を牽引すると予想されています。インドには中国と同じ人口動態の利点があるにもかかわらず、市場規模は中国のBPC市場の1/5です。そのため、同国ではスキンケアや化粧品への需要が増加しており、化粧品用顔料市場の需要拡大が見込まれています。

- さらに、アジア太平洋地域は、2022年に世界の化粧品市場の42%以上を占め、化粧品顔料市場を後押しすることが期待されています。

- これらすべての要因は、アジア太平洋地域が世界市場を独占することが期待されています。

化粧品顔料産業の概要

化粧品顔料市場は、その性質上、部分的に統合されています。この市場の主要企業(順不同)には、DIC Corporation、ALTANA AG、Merck KGaA、Venator Materials PLC.、Fujian Kuncai Material Technologyなどが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- アジア太平洋地域における化粧品需要の増加

- 有機顔料の需要急増

- その他

- 抑制要因

- 美容強化のための新しい医療技術

- 特定の顔料の使用に関わる厳しい規制

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 用途別

- 化粧品

- リップ製品

- ヘアカラー製品

- アイメイク

- その他

- 組成別

- 無機

- 有機

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- ALTANA AG

- Croda International Plc

- DIC Corporation

- ECKART

- Fujian Kuncai Material Technology Co., Ltd.

- GEOTECH

- IFC Solutions

- Kobo

- Koel Colours Private Limited

- LANXESS

- Merck KGaA

- Neelikon Food Dyes And Chemicals Ltd.

- Ocres de France

- Sandream Specialties

- Sensient Cosmetic Technologies

- Sudarshan Chemical Industries Limted

- Venator Materials PLC.

第7章 市場機会と今後の動向

第8章 有機的に生産された化粧品用顔料の需要の高まり

第9章 持続可能で環境に安全な化粧品用顔料の増加

目次

The Cosmetic Pigments Market is expected to register a CAGR of 6.01% during the forecast period.

The COVID-19 pandemic negatively impacted the market. This was because of the shutdown of the manufacturing facilities and plants due to the lockdown and restrictions. Supply chain and transportation disruptions further created hindrances for the market. However, the industry witnessed a recovery in 2021, thus rebounding the demand for the market studied.

Key Highlights

- Over the short term, the increasing demand for cosmetics products in the Asia-Pacific region and the rapidly growing demand for organic pigments are some of the factors driving the growth of the market studied.

- On the flip side, new medical technologies for beauty enhancement are expected to hinder the growth of the market.

- However, the rising demand for organically produced cosmetic pigments is anticipated to provide numerous opportunities over the forecast period.

- The Asia-Pacific region represents the largest market and is also expected to be the fastest-growing market over the forecast period owing to the increasing consumption from countries such as China, India, Japan, and South Korea.

Cosmetics Pigment Market Trends

Inorganic Pigment Segment to Dominant the market

- Inorganic pigments are chemical compounds not based on carbon and are usually metallic salts precipitated from solutions.

- These pigments can be defined as insoluble compounds with a basis of metallic ions. Inorganic pigments are generally very resistant to the effects of light because the energy required to generate a breakdown of bonds is greater than that provided by sunlight.

- Most inorganic pigments are manufactured at high temperatures and are generally not affected by the process temperatures, making them resistant to heat.

- Inorganic colors (pigments) are composed of insoluble metallic compounds derived from natural sources (e.g., china clay, carbon deposits) or are synthesized. Inorganic pigments consist of iron oxides, chromium oxides, ultramarines, manganese violet, white pigments, and pearlescent effects.

- The high stability of inorganic pigment color and high particle dispersion make it a popular choice in the manufacture of cosmetics products. The dispersion benefits of inorganic pigment are expected to increase the industry's growth rate and the development of the worldwide inorganic pigment market in the coming years.

- For instance, Germany is the largest cosmetic market in Europe, followed by France and the United Kingdom. For instance, according to IKW, in 2022, the market value of beauty and personal care in Germany is estimated to be EUR 14,333 Million (USD 15104.11 Million), which shows an increase of 5.36% compared to 2021. Therefore, an increase in the market value of beauty and personal care products in the country is expected to create an upside demand for the cosmetic pigments market in the country.

- The market for men's skincare is expanding as a result of rising disposable income, celebrity endorsements, and increased product launches among men who are becoming more conscious of their personal hygiene and regular grooming. Men's preferences for skincare products are expanding beyond those for traditional grooming. For instance, according to L'Oreal, in 2022, skincare products made up 41% of the global cosmetic market.

- Moreover, due to the increase in advertising and promotional activities, consumers in the United States are purchasing cosmetics. For instance, in 2022, the revenue of the United States cosmetics markets lay at over USD 18 billion . The strongest segment in 2022 was face cosmetics with a revenue of around USD 6.5 billion, followed by the eye cosmetics segment. The natural cosmetics market in comparison generated an annual revenue of USD 1.6 billion.

- Therefore, due to the above-mentioned factors, the inorganic pigments segment is likely to dominate the cosmetic pigments market during the forecast period.

Asia-Pacific Region to Dominate the Market

- Currently, the Asia-Pacific region dominates the global market for the cosmetic pigments market. China and Japan are the leading consumers of cosmetic pigments in the region.

- The increasing cosmetic production capacities and consumption in countries such as China, India, and ASEAN countries, are expected to increase the demand for cosmetic pigments in the region.

- According to the National Bureau of Statistics of China, in January 2022, the retail trade revenue of cosmetics in China amounted to about USD 9.18 billion and reached about USD 9.76 billion in January 2023. As the demand for cosmetic products expands further in second-and third-tier cities of China, the cosmetic pigments market is expected to maintain its growth momentum in the near future. In addition, the changing attitude among men toward skin care fosters the booming of the men's cosmetics market in China.

- According to Euromonitor International Study, the Indian beauty and personal care (BPC) market is the 8th largest in the world with a total value of USD 15 billion and is growing at ~10%. Furthermore, the market is expected to double by 2030 with skin care and cosmetics driving this growth. Despite having the same demographic advantage as China, the size of the Indian market is 1/5th the size of the Chinese BPC market, primarily due to lack of penetration outside metros and tier 1 cities. Therefore, increasing demand for skin care and cosmetics products in thge country is expected to cretae an upside demand for cosmetic pigments market.

- Moreover, the Asia Pacific accounts for over 42% of the global cosmetics market in the year 2022, which is expected to boost cosmetic pigments market.

- All these factors are expected to make the Asia-Pacific region dominate the global market.

Cosmetics Pigment Industry Overview

The Cosmetic Pigments Market is partially consolidated in nature. The major players in this market (not in a particular order) include DIC Corporation, ALTANA AG, Merck KGaA, Venator Materials PLC., and Fujian Kuncai Material Technology Co., Ltd., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Cosmetic Products in the Asia-Pacific Region

- 4.1.2 Rapidly Growing Demand for Organic Pigments

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 New Medical Technologies for Beauty Enhancement

- 4.2.2 Straight Regulations Pertaining to the Use of Certain Pigments

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Application

- 5.1.1 Facial Makeup

- 5.1.2 Lip Products

- 5.1.3 Hair Colour Products

- 5.1.4 Eye Makeup

- 5.1.5 Other Applications

- 5.2 Composition

- 5.2.1 Inorganic

- 5.2.2 Organic

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 ALTANA AG

- 6.4.2 Croda International Plc

- 6.4.3 DIC Corporation

- 6.4.4 ECKART

- 6.4.5 Fujian Kuncai Material Technology Co., Ltd.

- 6.4.6 GEOTECH

- 6.4.7 IFC Solutions

- 6.4.8 Kobo

- 6.4.9 Koel Colours Private Limited

- 6.4.10 LANXESS

- 6.4.11 Merck KGaA

- 6.4.12 Neelikon Food Dyes And Chemicals Ltd.

- 6.4.13 Ocres de France

- 6.4.14 Sandream Specialties

- 6.4.15 Sensient Cosmetic Technologies

- 6.4.16 Sudarshan Chemical Industries Limted

- 6.4.17 Venator Materials PLC.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

8 The Rising Demand for Organically Produced Cosmetic Pigments

9 Increasing Sustainable and Environmentally Safe Pigments for Cosmetics

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日