ブレーキフルード:市場シェア分析、産業動向・統計、成長予測(2025~2030年)

Brake Fluids - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1689908

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

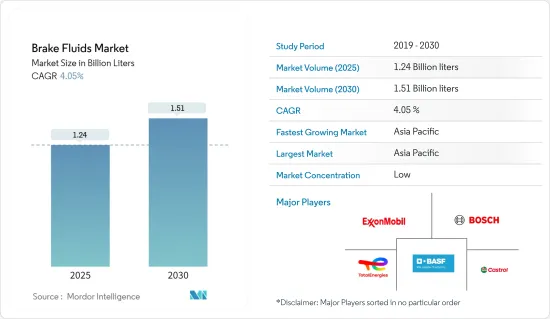

ブレーキフルードの市場規模は2025年に12億4,000万リットルと推定・予測され、2030年には15億1,000万リットルに達すると予測され、予測期間(2025~2030年)のCAGRは4.05%です。

ブレーキフルード市場は、COVID-19の流行により大きな課題に直面しました。世界のロックダウンと厳しい政府規制により、生産拠点が広範囲にわたって閉鎖されました。しかし、市場は2021年に回復し、今後数年間で大きく成長すると予測されます。

主なハイライト

- 短期的には、電気自動車やハイブリッド車の採用が増加し、自動車人口が急増していることが、市場の需要を牽引する主な要因となっています。

- しかし、ブレーキフルードの使用に関連する厳しい安全基準が市場の成長を妨げると予想されます。

- しかしながら、自動車システムの技術的進歩は市場に新たな機会をもたらすと期待されています。

- アジア太平洋地域が市場を独占し、中国とインドからの需要が大半を占めると予想されます。

ブレーキフルード市場の動向

市場を独占する小型商用車

- バン、トラック、バスなどの小型商用車(LCV)では、ブレーキフルードが安全で信頼性の高い制動力を確保します。これらの車両は、重い積載物を扱い、多様な走行条件に直面することが多いため、堅牢なブレーキシステムに依存しています。このシステムにおけるブレーキフルードの重要性は極めて高いです。

- ブレーキフルードに対する需要の高まりには、新興市場における軽量で高性能な自動車への嗜好の高まり、新たな自動車拠点の設立、可処分所得の増加などがあります。

- 2023年、世界の新車販売台数は2022年比11.9%増の9,270万台超と堅調な伸びを示したと、国際自動車製造者機構(OICA)が報告しています。特に、2023年の世界の商用車新車登録台数は2,750万台となり、2022年の2,420万台から13.3%増加しました。

- また、OICAのデータによれば、2023年の小型商用車生産台数は2,144万台と、前年比9%増となり、市場の成長をさらに後押ししました。

- アジア・オセアニア地域の国々は、世界市場における新興自動車ハブとして戦略的に位置づけられています。アジア・オセアニア地域の自動車登録台数は、他の地域と比較して最も多いです。この地域の登録台数は、主に中国、日本、韓国、インドによって占められています。2023年、この地域の商用車新車販売台数は2022年比で10.9%増加し、2022年の717万台に対し2023年には796万台が登録されました。

- しかし、インドでは、商用車(CV)販売台数は、24年度に2~5%の小幅な伸びを示した後、2024-25会計年度(25年度)には落ち込むと予測されています。ICRA(Investment Information and Credit Rating Agency of India Limited)のデータでは、25年度は4~7%減少すると予測されています。

- OICAによると、北米の2023年の自動車生産台数は1,914万台で、2022年の1,775万台から7.8%増加しました。小型商用車が大部分を占め、2022年の1,224万台から2023年には1,330万台に増加しました。

- 連邦自動車交通局のデータによると、ドイツの自動車台数は2022年の5,305万台から2023年には5,350万台に達しました。さらに、Kraftfahrt-Bundesamtは、ドイツの自動車登録台数が前年度の4,854万台に対し、2023年には4,876万台と、わずかに増加したことを強調しました。

- OICAによると、2023年のドイツの商用車登録台数は35万9,000台を超え、前年の31万2,000台から増加しました。

- OICAのデータによると、ブラジルの小型商用車生産台数は2023年に42万2,000台に達し、前年比20%増となりました。南アフリカも2023年の生産台数が前年比22%増の26万3,000台に達し、市場の成長を後押ししました。

- こうした動きを踏まえると、ブレーキフルードの需要は今後数年間で成長するものと思われます。

アジア太平洋地域が市場を独占

- アジア太平洋地域は、中国、インド、日本、韓国といった主要な自動車生産国の存在により、最大のブレーキフルード市場を占めると予想されます。これらの諸国は、自動車の製造基盤を強化し、効率的なサプライチェーンを構築して収益性の向上に努めています。

- 中国の自動車産業は、自動車保有台数の堅調な伸びと技術の進歩を反映し、潤滑油の主要消費国として際立っています。中国汽車工業協会(CAAM)のデータによると、2023年、中国の自動車販売台数と生産台数はそれぞれ3,000万台という節目を迎え、前年比2桁増となりました。

- OICAのデータによると、2023年の小型商用車生産台数は中国が首位で約230万台、タイは126万台でこれに続きました。

- インドでは、インド自動車工業会(SIAM)のデータによると、2024年1月から3月までの乗用車、商用車、三輪車、二輪車、四輪車の生産台数は739万台に達しました。特に乗用車と商用車の販売台数は、それぞれ114万台と26万8,000台でした。

- 韓国は、Hyundai、Renault、Samsung、Kiaといった有名ブランドを擁する成熟した自動車産業を誇っています。自動車工業会と韓国自動車研究院の予測によると、2024年の国内自動車生産台数は1.0%増の436万台に達すると予想されています。この成長は、市場の需要を促進すると予想されます。

- OICAのデータによると、2023年の国内自動車販売台数は174万台に達し、2022年から3%以上増加しました。乗用車の販売台数は4.8%増の140万台となりましたが、商用車の販売台数は前年比1.1%減の26万台とわずかながら落ち込みました。

- さらにOICAによれば、2023年の日本の自動車販売台数は470万台に達し、2022年から13%増加しました。その内訳は、乗用車が15%以上増加して390万台、商用車は4%増の78万台でした。

- こうした動きを踏まえると、アジア太平洋地域におけるブレーキフルードの需要は増加するとみられます。

ブレーキフルード業界の概要

世界のブレーキフルード市場は、部分的に断片化されています。主なプレーヤー(順不同)には、TotalEnergies SE、Robert Bosch LLC、CASTROL LIMITED、Exxon Mobil Corporation、BASF SEが含まれます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 電気自動車とハイブリッド車の普及拡大

- 自動車人口の急増がブレーキフルード需要を牽引

- その他

- 抑制要因

- ブレーキフルードの使用に伴う厳しい安全基準

- その他

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- フルードタイプ別

- 石油系

- 非石油系

- 製品タイプ別

- DOT 3

- DOT 4

- DOT 5

- DOT 5.1

- 用途別

- 小型商用車

- 乗用車

- その他

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- カタール

- アラブ首長国連邦

- ナイジェリア

- エジプト

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア分析(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- BASF SE

- CASTROL LIMITED

- Chevron Corporation

- China Petrochemical Corporation(SINOPEC)

- Dow

- Exxon Mobil Corporation

- FUCHS

- Hi-Tec Oils Pty Ltd

- Morris Lubricants

- Motul

- Repsol

- Robert Bosch LLC

- TotalEnergies SE

- Valvoline

第7章 市場機会と今後の動向

- 自動車システムの技術進歩

- その他の機会

目次

The Brake Fluids Market size is estimated at 1.24 billion liters in 2025, and is expected to reach 1.51 billion liters by 2030, at a CAGR of 4.05% during the forecast period (2025-2030).

The brake fluids market faced significant challenges due to the COVID-19 pandemic. Global lockdowns and stringent government regulations led to widespread shutdowns of production hubs. However, the market rebounded in 2021 and is projected to grow substantially in the years ahead.

Key Highlights

- Over the short term, increasing adoption of electric and hybrid vehicles and surging vehicle population are the major factors driving the demand for the market studied.

- However, stringent safety standards associated with using brake fluids are expected to hinder the market's growth.

- Nevertheless, technological advancements in the automobile systems are expected to create new opportunities for the market studied.

- Asia-Pacific is expected to dominate the market, with most of demand coming from China and India.

Brake Fluids Market Trends

Light Commercial Vehicles to Dominate the Market

- In Light Commercial Vehicles (LCVs) like vans, trucks, and buses, brake fluid ensures safe and reliable stopping power. These vehicles, often handling heavy payloads and facing diverse driving conditions, depend on a robust braking system. The significance of brake fluid in this system is paramount.

- Rising demand for brake fluids includes a growing appetite for lightweight, high-performance cars in emerging markets, the establishment of new automotive hubs, and an uptick in disposable income.

- In 2023, global new vehicle sales saw a robust growth of 11.9% over 2022, totaling over 92.7 million units, as reported by the Organisation Internationale des Constructeurs d'Automobiles (OICA). Specifically, new commercial vehicle registrations worldwide rose to 27.5 million units in 2023, marking a notable 13.3% increase from the 24.2 million units recorded in 2022.

- Additionally, light commercial vehicle production climbed to 21.44 million units in 2023, marking a 9% rise from the previous year, according to OICA data, further fueling the market's growth.

- The countries in the Asia-Oceania region are strategically positioning themselves as the emerging automotive hub in the global market. The Asia-Oceania region registered the largest number of vehicles compared to other regions. Registration in this region is dominated mainly by China, Japan, South Korea, and India. In 2023, the region witnessed a 10.9% increase in new commercial vehicle sales compared to 2022, with 7.96 million units registered in 2023, compared to 7.17 million units in 2022.

- However, in India, commercial vehicle (CV) sales are projected to dip in the financial year 2024-25 (FY25) after a modest 2-5% growth in FY24. The data from ICRA (Investment Information and Credit Rating Agency of India Limited) forecasts a 4-7% decline in FY25.

- North America's motor vehicle production in 2023 hit 19.14 million units, a 7.8% increase from 2022's 17.75 million units, according to OICA. Light commercial vehicles constituted a significant portion, rising from 12.24 million units in 2022 to 13.30 million units in 2023.

- Data from the Federal Motor Transport Authority indicates that Germany's motor vehicle count reached 53.50 million in 2023, up from 53.05 million in 2022. Furthermore, the Kraftfahrt-Bundesamt highlighted that car registrations in Germany saw a slight uptick, with 48.76 million in 2023 compared to 48.54 million the previous year.

- According to OICA, Germany registered over 359 thousand commercial vehicles in 2023, up from 312 thousand units the previous year.

- OICA data reveals that Brazil's light commercial vehicle production hit 422 thousand units in 2023, marking a 20% increase from the prior year. South Africa also saw a boost, with production reaching 263 thousand units in 2023, a 22% rise from the previous year, bolstering the market's growth.

- Given these dynamics, the demand for brake fluids is poised for growth in the coming years.

Asia-Pacific to Dominate the Market

- The Asia-Pacific region is expected to account for the largest brake fluid market due to the presence of leading automobile producers such as China, India, Japan, and South Korea. These countries are working hard to strengthen the manufacturing base for vehicles and develop efficient supply chains for greater profitability.

- China's automotive industry stands out as the leading consumer of lubricants, reflecting its robust vehicle fleet growth and technological advancements. In 2023, both automobile sales and production in China reached a milestone, hitting 30 million units each, marking a double-digit increase from the previous year, as per the data from the China Association of Automobile Manufacturers (CAAM).

- As per the data from OICA, China led in the production of light commercial vehicles in 2023, churning out approximately 2.30 million vehicles, with Thailand trailing at 1.26 million.

- In India, data from the Society of Indian Automobile Manufacturers (SIAM) indicates that from January to March 2024, the production of passenger vehicles, commercial vehicles, three-wheelers, two-wheelers, and quadricycle reached 7.39 million units. Specifically, sales for passenger and commercial vehicles were 1.14 million units and 268 thousand units, respectively.

- South Korea boasts a mature automotive industry with notable brands like Hyundai, Renault, Samsung, and Kia. Projections from the Automobile Manufacturers Association and The Korea Automobile Research Institute anticipate a 1.0% rise in domestic automobile production for 2024, reaching 4.36 million units. This growth is expected to drive demand in the studied market.

- OICA data shows that in 2023, vehicle sales in the country reached 1.74 million units, up over 3% from 2022. Passenger vehicle sales climbed 4.8% to 1.4 million units, but commercial vehicles saw a slight dip, selling 0.26 million units, down 1.1% from the previous year.

- Further, OICA reports that Japan's vehicle sales in 2023 touched 4.7 million units, marking a 13% uptick from 2022. Breaking it down, passenger vehicle sales rose over 15% to 3.9 million units, while commercial vehicles saw a modest 4% increase, totaling 0.78 million units.

- Given these dynamics, the demand for brake fluids in the Asia-Pacific is set to rise.

Brake Fluids Industry Overview

The global brake fluids market is partially fragmented in nature. The major players (not in any particular order) include TotalEnergies SE, Robert Bosch LLC, CASTROL LIMITED, Exxon Mobil Corporation, and BASF SE.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Adoption of Electric and Hybrid Vehicles

- 4.1.2 Surging Vehicle Population to Drive the Demand for Brake Fluids

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Safety Standard Associated With the Use of Braking Fluids

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 By Fluid Type

- 5.1.1 Petroleum

- 5.1.2 Non-petroleum

- 5.2 By Product Type

- 5.2.1 DOT 3

- 5.2.2 DOT 4

- 5.2.3 DOT 5

- 5.2.4 DOT 5.1

- 5.3 By Application

- 5.3.1 Light Commercial Vehicles

- 5.3.2 Passenger Cars

- 5.3.3 Other Applications

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Qatar

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 South Africa

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 CASTROL LIMITED

- 6.4.3 Chevron Corporation

- 6.4.4 China Petrochemical Corporation (SINOPEC)

- 6.4.5 Dow

- 6.4.6 Exxon Mobil Corporation

- 6.4.7 FUCHS

- 6.4.8 Hi-Tec Oils Pty Ltd

- 6.4.9 Morris Lubricants

- 6.4.10 Motul

- 6.4.11 Repsol

- 6.4.12 Robert Bosch LLC

- 6.4.13 TotalEnergies SE

- 6.4.14 Valvoline

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements in the Automotive Systems

- 7.2 Other Opportunities

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日