網膜硝子体手術装置-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Vitreoretinal Surgery Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1689861

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

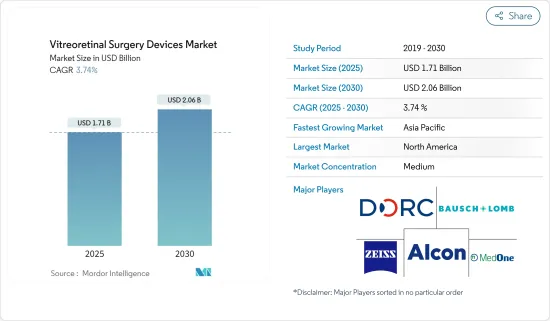

網膜硝子体手術装置市場規模は2025年に17億1,000万米ドルと推定・予測され、予測期間(2025年~2030年)のCAGRは3.74%で、2030年には20億6,000万米ドルに達すると予測されています。

COVID-19の大流行は前例のない健康上の懸念であり、さまざまな外科手術に悪影響を及ぼしました。緊急性のない手術は行わないようにという規制当局の厳しい指導により、パンデミック期間中、手術件数は激減しました。例えば、2021年9月にPubMed Centralが発表した調査によると、COVID-19の大流行は、初期段階における糖尿病性網膜症の臨床治療に大きな影響を与えました。したがって、COVID-19は調査市場に影響を与えました。しかし、COVID-19の症例数が減少し、広範なワクチン接種プログラムが実施されたことで、調査市場は今後数年間でCOVID-19以前のレベルの潜在力を取り戻すと予想されました。

糖尿病性網膜症や黄斑円孔などの眼疾患の発生率の増加や老年人口の増加が、予測期間中の調査市場の成長を促進するとされています。例えば、国立医学図書館が2021年5月に発表した調査研究によると、糖尿病網膜症は依然として糖尿病の一般的な合併症であり、成人就労人口における予防可能な失明の主な原因でした。糖尿病患者のうち、糖尿病網膜症の有病率は22.27%、視力を脅かす糖尿病(VTDR)は6.17%、臨床的に重要な黄斑浮腫(CSME)は4.07%でした。

眼疾患の多くは、黄斑変性症のように加齢に伴うものです。世界の老年人口の増加に伴い、眼疾患の負担は増加すると予想され、これは調査対象市場の成長を増大させる可能性が高いです。例えば、World Population Aging Highlights United Nations 2022報告書によると、2022年には世界全体で65歳以上の人口が7億7,100万人になることが判明しています。高齢者人口は2030年には9億9,400万人、2050年には16億人に達すると予測されています。高齢者は糖尿病性網膜症や黄斑円孔などの眼疾患を伴うことが多いため、高齢者人口の増加により、このような疾患を治療する網膜硝子体手術装置の採用が進むと予想されます。

各社は足跡を拡大するため、新製品の上市開発や提携に積極的に取り組んでいます。例えば、DORCは2021年1月、TissueBlue for Staining of the ILM During Vitreoretinal Surgery(網膜硝子体手術中のILM染色用TissueBlue)のカナダ保健省の承認を取得しました。TissueBlueは、内境界膜(ILM)を選択的に染色することで、眼科手術を支援するためにカナダ保健省によって承認された最初の染料です。このような開発は、予測期間中の市場の成長を促進すると期待されています。

したがって、黄斑変性症、糖尿病網膜症、黄斑円孔などの眼疾患の発生率の増加や老年人口の増加などの要因により、網膜硝子体手術装置市場は予測期間中に成長すると予想されます。しかし、手術による副作用が予測期間中の市場成長を抑制すると予想されます。

網膜硝子体手術装置市場の動向

網膜後硝子体手術が予測期間中に大きな市場シェアを占める見込み

網膜後面硝子体手術(Pars plana vitrectomy:PPV)は、網膜剥離、硝子体出血、眼内炎、黄斑円孔などの病態を制御された閉鎖系で治療するために後眼部にアクセスすることができる、網膜硝子体手術で一般的に採用されている手技です。糖尿病網膜症や後部硝子体剥離など、眼球後部に関連する疾患/障害の有病率の高さが後部硝子体手術(網膜や硝子体に関連する疾患の治療に用いられる外科的処置)の需要を促進しており、これは網膜硝子体後方手術セグメントの成長に大きな影響を与えると予想されます。

例えば、2021年8月にPLOS ONEが発表した論文によると、糖尿病網膜症(DR)は糖尿病の最も一般的な重篤な合併症の一つと言われています。これは、高血糖レベルによって引き起こされる目の血管の損傷と定義されています。この情報源はまた、ドイツにおけるこの合併症のプールされた有病率は、ヘルスケア部門によって異なるが、約10%から30%であると述べています。したがって、糖尿病性網膜症の高い有病率は、セグメントの成長を促進すると予想されます。

さらに、WebMDが2021年7月に発表した記事によると、網膜剥離の年間発生率は約10,000人に1人、生涯では約300人に1人です。したがって、網膜後硝子体手術分野は網膜硝子体手術装置市場で大きなシェアを占めると予想されます。さらに、これらの疾患は高齢者に関連することが多いため、高齢者人口の増加も市場の成長を高めると予想されます。

したがって、糖尿病網膜症や後部硝子体剥離など、眼球後部に関連する疾患/障害の有病率の高さなどの要因により、網膜硝子体後方手術分野は予測期間中に大きな市場シェアを占めると予想されます。

予測期間中、北米が大きな市場シェアを占める見込み

北米は網膜硝子体手術装置市場で大きなシェアを占めると思われます。この地域は眼疾患の有病率や負担が高く、老年人口が増加しているため、予測期間中も同様の動向を示すと予想されます。例えば、2022年5月にBMC Ophthalmologyが発表した論文によると、糖尿病網膜症(DR)は糖尿病の失明の可能性のある合併症と考えられており、米国では毎年糖尿病患者のほぼ約28%が罹患しています。糖尿病性網膜症は通常、年1回の検診で発見できるが、糖尿病を患う多くのアメリカ人は、視覚障害や失明を防ぐための定期的な監視を受けていないです。糖尿病性網膜症が発見されないのは、特に病院環境においてであり、糖尿病入院患者の約44%の有病率があると推定され、そのうち半数以上がこれまで診断されていなかったといいます。

さらに、主に高齢者に発症する眼疾患の治療には網膜硝子体手術が推奨されることが多いため、国内の高齢者人口の増加も市場の成長を高めると予想されます。例えば、国連人口基金ダッシュボードが2022年に更新したデータによると、2022年にはカナダの総人口の19%が65歳以上になると推定されています。

各社は足跡を拡大するため、製品発売開発、技術革新、提携、協力に積極的に取り組んでいます。例えば、2022年3月、Carl Zeiss MeditecAG社は、白内障の乳化除去や前眼部硝子体手術に適応のあるQUATERA 700装置について、米国食品医薬品局(FDA)から510(k)の市販前承認を取得しました。このような開発は、予測期間における市場の成長を促進すると予想されます。

したがって、同地域における眼疾患の有病率の高さや負担の重さ、老人人口の増加といった要因が、予測期間中の市場成長を促進すると予想されます。

網膜硝子体手術装置産業の概要

網膜硝子体手術装置市場は、世界的および地域的に事業を展開する企業が存在するため中程度の規模となっています。競合情勢には、Dutch Ophthalmic Research Center International BV、Bausch &Lomb Inc.、OCULUS Optikgerate GmbH、MedOne Surgical Inc.など、市場シェアを持ち知名度の高い企業の製品発売、買収、提携、契約に基づく分析が含まれます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 眼疾患の発生率の増加

- 老年人口の増加

- 市場抑制要因

- 手技による副作用

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 製品タイプ別

- パーフルオロカーボン液体

- 内視鏡用器具

- 網膜硝子体用プレフィルドシリコーンオイルシリンジ

- 静脈切開システム

- その他の製品タイプ

- 手術タイプ別

- 網膜前部硝子体手術

- 網膜後硝子体手術

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Dutch Ophthalmic Research Center International BV

- Bausch & Lomb Inc.

- OCULUS Optikgerete GmbH

- BVI

- MedOne Surgical Inc.

- Alcon

- Carl Zeiss

- Topcon Corporation

- Hoya Corporation

- GEUDER AG

第7章 市場機会と今後の動向

目次

The Vitreoretinal Surgery Devices Market size is estimated at USD 1.71 billion in 2025, and is expected to reach USD 2.06 billion by 2030, at a CAGR of 3.74% during the forecast period (2025-2030).

The COVID-19 pandemic was an unprecedented health concern and adversely affected various surgical procedures. Due to regulatory authorities' strict guidance to prevent any non-emergent surgeries, the volume of surgeries drastically decreased throughout the pandemic. For instance, as per the research study published by PubMed Central in September 2021, the COVID-19 pandemic significantly impacted the clinical care for diabetic retinopathy during the early phase. Thus, COVID-19 had an impact on the studied market. However, with the decreasing number of COVID-19 cases and wide-scale vaccination programs, the studied market was expected to regain its pre-COVID-19 level potential over the coming years.

The increasing incidence of eye disorders such as diabetic retinopathy and macular holes and the increasing geriatric population is attributed to driving the growth of the studied market over the forecast period. For instance, according to the research study published in May 2021 by the National Library of Medicine, diabetic retinopathy remained a common complication of diabetes mellitus and a leading cause of preventable blindness in the adult working population. Among the people with diabetes mellitus, the prevalence of diabetic retinopathy was 22.27%, 6.17% for vision-threatening diabetes mellitus (VTDR), and 4.07% for clinically significant macular edema (CSME).

Many eye disorders are age-associated, like macular degeneration. With the growing global geriatric population, the burden of eye diseases is expected to increase, which is likely to augment the growth of the studied market. For instance, according to World Population Aging Highlights United Nations 2022 report, it was found that in 2022 there were 771 million people aged 65 years or over globally. The older population is projected to reach 994 million by 2030 and 1.6 billion by 2050. As older adults are often associated with eye disorders such as diabetic retinopathy and macular holes, the rising geriatric population is expected to enhance the adoption of vitreoretinal surgery devices to treat such diseases.

The companies are actively involved in new product launch developments and collaborations to expand their footprint. For instance, in January 2021, DORC received Health Canada approval of TissueBlue for Staining of the ILM During Vitreoretinal Surgery. TissueBlue is the first dye approved by Health Canada to aid in ophthalmic surgery by selectively staining the internal limiting membrane (ILM). Such development is expected to drive the market's growth over the forecast period.

Hence, owing to the factors such as the increasing incidence of eye disorders such as macular degeneration, diabetic retinopathy, and macular holes and the increasing geriatric population, the vitreoretinal surgery devices market is expected to grow over the forecast period. However, the side effects of the procedures are expected to restrain the market's growth during the forecast period.

Vitreoretinal Surgery Devices Market Trends

Posterior Vitreoretinal Surgery is Expected to Hold a Significant Market Share Over the Forecast Period

Pars plana vitrectomy (PPV) is a commonly employed technique in vitreoretinal surgery that enables access to the posterior segment for treating conditions such as retinal detachments, vitreous hemorrhage, endophthalmitis, and macular holes in a controlled, closed system. The high prevalence of diseases/disorders associated with the posterior segment of the eye, such as diabetic retinopathy and posterior vitreous detachment, is driving the demand for posterior vitrectomy (surgical procedures used to treat diseases associated with retina and vitreous), which is expected to have a significant impact on the growth of posterior vitreoretinal surgery segment.

For instance, according to an article published by PLOS ONE in August 2021, diabetic retinopathy (DR) is said to be one of the most common serious complications of diabetes mellitus. It is defined as damage to the blood vessels of the eyes caused by high blood glucose levels. The source also stated that the pooled prevalence of this complication in Germany ranges from about 10% to 30%, depending on the healthcare sector. Thus, the high prevalence of diabetic retinopathy is expected to drive segmental growth.

Additionally, according to an article published by WebMD in July 2021, the annual incidence of retinal detachment is approximately one in 10,000 or about 1 in 300 over a lifetime. Hence, the posterior vitreoretinal surgery segment is expected to have a major share of the vitreoretinal surgery devices market. Moreover, as these diseases are often associated with older adults, the rising geriatric population is also expected to enhance market growth.

Therefore, due to the factors such as the high prevalence of diseases/disorders associated with the posterior segment of the eye, such as diabetic retinopathy and posterior vitreous detachment, the posterior vitreoretinal surgery segment is expected to have a significant market share over the forecast period.

North America is Expected to Hold a Significant Market Share Over the Forecast Period

North America will hold a significant share of the vitreoretinal surgery devices market. It is expected to show a similar trend over the forecast period, owing to the region's high prevalence and burden of eye diseases and the increasing geriatric population. For instance, according to the article published by BMC Ophthalmology in May 2022, diabetic retinopathy (DR) is considered a potentially blinding complication of diabetes mellitus that affects almost about 28% of diabetics in the United States every year. Diabetic retinopathy can typically be detected with annual screening, but many Americans with diabetes mellitus do not receive routine surveillance to prevent visual impairment or blindness. The source also stated that undetected diabetic retinopathy might be particularly prevalent in hospital settings, where it is estimated to have a prevalence of around 44% among diabetic inpatients, out of which over half were previously undiagnosed.

Moreover, The rising geriatric population in the country is also expected to enhance the market growth as vitreoretinal surgeries are often recommended to treat eye disorders that mainly occur in older people. For instance, according to the data updated by the United Nations Population Fund dashboard in 2022, an estimated 19% of Canada's total population was 65 years or older in 2022.

The companies are actively involved in product launch developments, innovation, partnerships, and collaborations to expand their footprint. For instance, in March 2022, Carl Zeiss MeditecAG received 510(k) premarket approval from the United States Food and Drug Administration (FDA) for their QUATERA 700 device, which is indicated for the emulsification and removal of cataracts and anterior segment vitrectomy. Such development is expected to drive the market's growth over the forecast period.

Therefore, the factors such as the high prevalence and burden of eye diseases in the region and the increasing geriatric population are expected to drive market growth during the forecast period.

Vitreoretinal Surgery Devices Industry Overview

The Vitreoretinal Surgery Devices Market is moderate due to the presence of companies operating globally and regionally. The competitive landscape includes analysis of companies based on product launches, acquisitions, collaboration, and agreements that hold the market shares and are well known, including Dutch Ophthalmic Research Center International BV, Bausch & Lomb Inc., OCULUS Optikgerate GmbH, and MedOne Surgical Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Incidence of Eye Disorders

- 4.2.2 Increasing Geriatric Population

- 4.3 Market Restraints

- 4.3.1 Side Effects of the Procedures

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Product Type

- 5.1.1 Perfluoro Carbon Liquids

- 5.1.2 Endoillumination Instruments

- 5.1.3 Vitreoretinal Prefilled Silicone Oil Syringes

- 5.1.4 Virectomy System

- 5.1.5 Other Product Types

- 5.2 By Surgery Type

- 5.2.1 Anterior Vitreoretinal Surgery

- 5.2.2 Posterior Vitreoretinal Surgery

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Dutch Ophthalmic Research Center International BV

- 6.1.2 Bausch & Lomb Inc.

- 6.1.3 OCULUS Optikgerete GmbH

- 6.1.4 BVI

- 6.1.5 MedOne Surgical Inc.

- 6.1.6 Alcon

- 6.1.7 Carl Zeiss

- 6.1.8 Topcon Corporation

- 6.1.9 Hoya Corporation

- 6.1.10 GEUDER AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日