|

|

市場調査レポート

商品コード

1689831

インドのホスピタリティ産業- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Hospitality Industry In India - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドのホスピタリティ産業- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

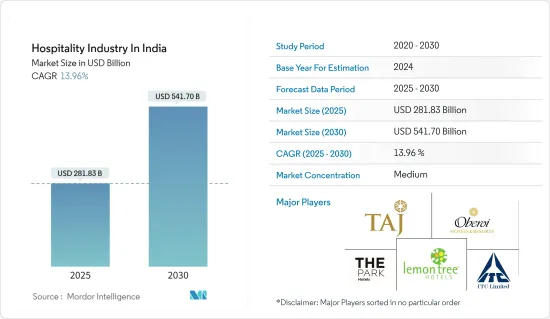

インドのホスピタリティ産業市場規模は2025年に2,818億3,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは13.96%で、2030年には5,417億米ドルに達すると予測されます。

インドは、レジャーやビジネスで訪れる旅行者の世界の主要目的地として成功を収めており、このことが同国のホスピタリティ部門にプラスの影響を与えていることは間違いないです。

世界の旅行先としてのインドの魅力は、その地政学的安定性、世界クラスのインフラ、国際的なイベント開催へのコミットメントによってさらに高まっています。したがって、これらの要因は観光産業の成長に寄与し、結果としてホスピタリティ産業の堅調さを維持しています。

インドの国内観光業は目覚ましい回復力と強さを見せており、インド住民の間で滞在型旅行への嗜好が高まっていることが注目されています。このような滞在志向は、利便性、安全性、インド国内の隠れた魅力を発見する機会など、いくつかの要因によってもたらされています。

ホスピタリティ・ツーリズム部門の成長率は顕著な伸びを示しています。インドは、ビジネス実施に有利な条件(EoDB)の上位100カ国一覧に含まれており、グリーンフィールドFDIランキングでは世界第1位を占めています。クルーズ観光産業を強化するため、インド政府(GoI)は、チェンナイ港、ゴア港、コチ港、マンガロール港、ムンバイ港をクルーズ観光の拠点として開発することを決定しました。これらの港には、ホスピタリティサービス、小売店、ショッピングセンター、レストランなど、さまざまな施設が設置される予定です。

インドのホスピタリティ市場動向

ホテルプロジェクト数の増加が市場を牽引

インドのホスピタリティセクタは、ホテルプロジェクトの急増により顕著な盛り上がりを見せています。産業の稼働率は前年比60~67%増となりました。にもかかわらず、平均料金(ARR)は完全に回復し、前年比37~39%の大幅な上昇を示しました。その結果、客室1室あたりの売上高(RevPAR)は前年比89~91%の著しい伸びを示しました。

需要の力強い回復に牽引され、ホテル企業は今年、拡大戦略を加速させ、キーによるブランド契約は前年比で35%以上増加しました。TopHotelProjectsの建設データベースによると、インドでは481件、5万7,879室のプロジェクトが予定されています。例えば、IHCLは8,700室、LTHは26年度までに2,600室の増築を計画しています。さらに、Marriott Internationalは、今年インドで12軒のホテルをオープンする予定で、同国のホテルチェーンの現在のポートフォリオに約1,200室が加わることになります。Radisson Hotel Grouも昨年、9つのブランドポートフォリオで21軒のホテルと契約し、インドでの足跡を広げています。Hoteliersは、レジャースポットやTier-3、Tier-4都市での存在感を高めており、これらの地域には未開拓の大きな可能性があると認識しています。

さらに、2023年11月までのインドのG20議長国期間中、200を超えるG20会合が全国55カ所で開催されました。このため、これらの会議が開催された都市のホテル需要が顕著に増加し、インドのホテルセクタに大きな恩恵をもたらしました。

観光客誘致のための政府の取り組みと観光客の増加が市場を牽引

インドのホスピタリティ産業は、旺盛な内需とインド政府が観光セクタの拡大に改めて注力したことが主要因となっています。政府は、観光産業が主要な雇用創出源となる可能性を認識し、官民パートナーシップやすべての利害関係者を巻き込んだミッション志向のアプローチを通じて、観光産業を積極的に推進しています。政府は、地域の空のつながりを強化するため、さらに50の空港、ヘリポート、水上飛行場を復活させる計画です。また、国内外からの観光客を対象とした包括的な包装として、50の観光地を開発することを目指しています。大規模な鉄道やラストワンマイル接続への投資を含む、政府のインフラ開発への継続的な重点は、このセクタに利益をもたらすと期待されています。

さらに、最近の個人所得税の引き下げは可処分所得を押し上げ、観光・ホスピタリティ部門の需要を促進します。観光省は、スワデシュ・ダルシャン・スキームをスワデシュ・ダルシャン2.0(SD2.0)として活性化し、ホスピタリティ・観光部門のデジタル化とビジネスのしやすさを促進するため、全国ホスピタリティ産業統合データベース(NIDHI)を導入しました。このイニシアチブは、現在NIDHI+としてアップグレードされ、宿泊施設だけでなく、旅行代理店、ツアーオペレーター、観光輸送オペレーター、飲食品ユニット、オンライン旅行アグリゲーター、コンベンションセンター、観光促進機関も含めることを目指しています。

インド国内訪問者数上位の州は、ウッタル・プラデシュ州、タミル・ナードゥ州、アンドラ・プラデシュ州、カルナータカ州、グジャラート州です。インドでは、各国からの外国人旅行者数(FTA)が顕著に増加しており、観光部門の回復が期待されています。

インドのホスピタリティ産業概要

インドのホスピタリティ産業に関する本レポートは、ホテルとホスピタリティ産業の主要な国際的参入企業と国内主要企業を網羅しています。インドのホスピタリティセクタはダイナミックで新興です。インド国内のホスピタリティ産業への参入に関心を持つ国内外の参入企業にとって、より大きな成長の可能性を秘めています。市場の主要企業には、Oberoi Hotels & Resorts、Park Hotel、ITC Hotels、Lemon Tree Hotels、Taj Hotelsなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 市場概要

- 市場の促進要因

- インドにおける旅行・観光産業の成長

- ホテルプロジェクトの増加

- 市場抑制要因

- 熟練労働者の不足が市場課題

- 持続可能性と競合が産業の成功を脅かす

- 市場機会

- 産業の裾野を広げる政府の取り組み

- オンラインマーケティングの活用による顧客基盤の拡大

- COVID-19のホスピタリティ産業への影響

- 宿泊施設と飲食品部門の収益フローに関する洞察

- インドの主要都市と観光客数

- ホスピタリティ産業への投資(不動産、FDI、その他)

- ホスピタリティ産業における技術革新

- 共同生活空間がホスピタリティ産業に与える影響

- ホスピタリティ産業へのその他の経済貢献に関する洞察

- 産業の魅力-ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- インドに存在する観光・旅行代理店のタイプに関する洞察

第5章 市場セグメンテーション

- タイプ別

- チェーンホテル

- 独立系ホテル

- セグメント別

- サービスアパートメント

- バジェット&エコノミーホテル

- 中上級ホテル

- 高級ホテル

第6章 競合情報

- 市場集中度

- 企業プロファイル

- Oberoi Hotels and Resorts

- ITC Hotels

- The Park Hotel

- The Leela Palaces, Hotels and Resorts

- Taj Hotels

- Lemon Tree Hotels

- Hyatt Hospitality company

- MarrIoTt International Inc.

- Radisson Hotel Group

- OYO Rooms

- Loyalty Programs Offered by Major Hotel Brands

第7章 市場機会と今後の動向

第8章 免責事項と出版社について

The Hospitality Industry In India Market size is estimated at USD 281.83 billion in 2025, and is expected to reach USD 541.70 billion by 2030, at a CAGR of 13.96% during the forecast period (2025-2030).

India has been successful as a leading global destination for leisure and business travelers, which has undoubtedly positively impacted the country's hospitality sector.

India's attractiveness as a global travel destination has been further enhanced by its geopolitical stability, world-class infrastructure, and commitment to hosting international events. Therefore, these factors contribute to the growth of the tourism industry and, as a result, keep the hospitality industry firm.

India's domestic tourism has shown remarkable resilience and strength, and an increasing preference for staycations among Indian residents has been noticed. This preference for staycation is driven by several factors, including convenience, safety, and the opportunity to discover hidden gems within India.

The growth rate of the hospitality and tourism sector has seen a notable increase. India is included in the list of the top 100 countries with favorable conditions for conducting business (EoDB) and holds the first globally regarding greenfield FDI ranking. To enhance the cruise tourism industry, the Government of India (GoI) has chosen to develop the Chennai, Goa, Kochi, Mangalore, and Mumbai ports as cruise tourism hubs. These ports will have various amenities such as hospitality services, retail outlets, shopping centers, and restaurants.

India Hospitality Market Trends

Increase in the Number of Hotel Projects is Driving the Market

India's hospitality sector has experienced a notable boost due to the surge in hotel projects. The industry saw an increase in occupancy rates ranging from 60-67% compared to the previous year. Despite this, average rates (ARR) have fully recovered, showing a significant rise of 37-39 % from the prior year. Consequently, Revenue per Available Room (RevPAR) has seen a remarkable growth of 89-91% in the current year compared to the previous year.

Driven by a robust rebound in demand, hotel companies have expedited their expansion strategies this year, leading to a more than 35% increase in brand signings by keys compared to the previous year. According to the TopHotelProjects construction database, India is set to welcome 481 projects with 57,879 rooms. For example, IHCL aims to incorporate 8,700 rooms, while LTH plans to add 2,600 rooms by FY26. Additionally, Marriott International anticipates opening 12 hotels in India this year, contributing around 1,200 rooms to the hotel chain's current portfolio in the country. Radisson Hotel Group has also extended its footprint in India by signing 21 hotels across nine brand portfolios last year. Hoteliers have been expanding their presence in leisure destinations and Tier-3 and -4 cities, acknowledging the vast untapped potential in these regions.

Moreover, during India's G20 presidency until November 2023, over 200 G20 meetings were held in 55 different locations nationwide. This significantly benefited the Indian hotel sector, as there was a notable increase in demand for hotels in the cities hosting these meetings.

Government Initiatives to Attract More Tourism and Rise in Tourism is Driving the Market

The Indian hospitality industry is primarily fueled by strong domestic demand and the Indian government's renewed focus on expanding the tourism sector. Recognizing the sector's potential as a major employment generator, the government actively promotes it through public-private partnerships and a mission-oriented approach involving all stakeholders. The government plans to revive 50 additional airports, heliports, and water aerodromes to enhance regional air connectivity. It also aims to develop fifty tourism destinations as comprehensive packages for domestic and international tourists. The government's continued emphasis on infrastructure development, including significant railways and last-mile connectivity investments, is expected to benefit the sector.

Moreover, the recent reduction in personal income tax will boost disposable income, thereby driving demand in the tourism and hospitality sectors. The Ministry of Tourism has undertaken a revitalization of its Swadesh Darshan Scheme as Swadesh Darshan 2.0 (SD2.0) and introduced the National Integrated Database of Hospitality Industry (NIDHI) to facilitate digitalization and ease of doing business in the hospitality and tourism sector. This initiative, now upgraded as NIDHI+, aims to include not only Accommodation Units but also Travel Agents, Tour Operators, Tourist Transport Operators, Food & Beverage Units, Online Travel Aggregators, Convention Centres, and Tourist Facilitators.

The top states in terms of domestic visits in India are Uttar Pradesh, Tamil Nadu, Andhra Pradesh, Karnataka, and Gujarat. India witnessed a promising recovery in the tourism sector, with a notable rise in Foreign Tourist Arrivals (FTAs) from various countries.

India Hospitality Industry Overview

The report on the Indian hospitality industry covers major international players and the leading domestic players in the hotel and hospitality industry. The Indian hospitality sector is dynamic and emerging. It holds greater potential to grow for national and international players interested in entering the nation's hospitality industry. Some of the major players in the market include Oberoi Hotels & Resorts, the Park Hotel, ITC Hotels, Lemon Tree Hotels, and Taj Hotels.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in Travel and Tourism in India

- 4.2.2 Increase in the Number of Hotel Projects

- 4.3 Market Restraints

- 4.3.1 Lack of Skilled Labor is a Challenge for the Market

- 4.3.2 Sustainability and Competition Threaten Industry Success

- 4.4 Market Opportunities

- 4.4.1 Government Initiatives to Expand the Horizons of the Industry

- 4.4.2 Online Marketing can be Leveraged to Expand the Customer Base

- 4.5 Impact of COVID-19 on the Hospitality Industry

- 4.6 Insights Into Revenue Flows from Accommodation and Food and Beverage Sectors

- 4.7 Leading Cities in India with Respect to Number of Visitors

- 4.8 Investments (Real Estate, FDI and Others) in Hospitality Industry

- 4.9 Technological Innovations in the Hospitality Industry

- 4.10 Shared Living Spaces Impact on the Hospitality Industry

- 4.11 Insights Into other Economic Contributors to the Hospitality Industry

- 4.12 Industry Attractiveness - Porter's Five Forces Analysis

- 4.12.1 Bargaining Power of Buyers

- 4.12.2 Bargaining Power of Suppliers

- 4.12.3 Threat of New Entrants

- 4.12.4 Threat of Substitutes

- 4.12.5 Intensity of Competitive Rivalry

- 4.13 Insights Into Types of Tourism and Travel Agencies Present in India

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Chain Hotels

- 5.1.2 Independent Hotels

- 5.2 By Segment

- 5.2.1 Service Apartments

- 5.2.2 Budget and Economy Hotels

- 5.2.3 Mid and Upper Mid-Scale Hotels

- 5.2.4 Luxury Hotels

6 COMPETITIVE INTELLIGENCE

- 6.1 Market Concentration

- 6.2 Company Profiles

- 6.2.1 Oberoi Hotels and Resorts

- 6.2.2 ITC Hotels

- 6.2.3 The Park Hotel

- 6.2.4 The Leela Palaces, Hotels and Resorts

- 6.2.5 Taj Hotels

- 6.2.6 Lemon Tree Hotels

- 6.2.7 Hyatt Hospitality company

- 6.2.8 Marriott International Inc.

- 6.2.9 Radisson Hotel Group

- 6.2.10 OYO Rooms

- 6.3 Loyalty Programs Offered by Major Hotel Brands