|

市場調査レポート

商品コード

1689827

航空気象レーダー- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Aviation Weather Radar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 航空気象レーダー- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

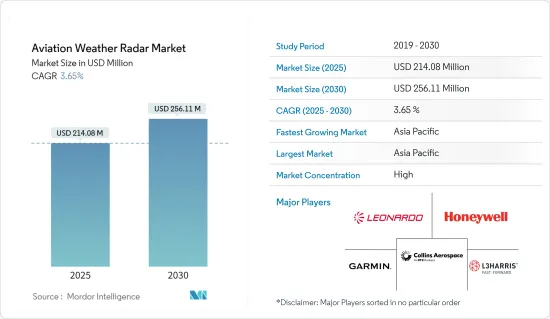

航空気象レーダー市場規模は2025年に2億1,408万米ドルと推定され、予測期間(2025~2030年)のCAGRは3.65%で、2030年には2億5,611万米ドルに達すると予測されています。

航空気象レーダー市場は、気象モニタリングの重要な必要性により、先進的レーダーシステムの需要が急増しています。悪天候から航空機を守ることが主要な市場の促進要因となっています。予期せぬ天候不順は航空機の混乱につながり、深刻な場合は損害につながるため、空港では気象レーダーの導入が急務となっています。

最先端のレーダー技術、特にパルスドップラーレーダーを採用することで、航空機は悪天候をより効率的かつ安全に航行できるようになります。さらに、産業では、より軽量でコンパクトなレーダーシステムへのシフトが顕著であり、燃料効率の向上とメンテナンスコストの低減を実現しています。

しかし、レーダーシステムの高コストと複雑さ、規制や環境上の障害など、市場は課題に直面しています。市場各社は、こうした課題を克服し競合を維持するために、研究開発、イノベーション、コラボレーションに注力する必要があります。こうしたハードルが市場成長の妨げになる可能性はあるもの、先進的レーダーシステムに対する民間航空、一般航空、軍用航空産業からの需要の高まりは、予測期間中、市場を積極的に牽引するものと考えられます。

航空気象レーダー市場の動向

予測期間中、軍用航空が最も高い成長率を示す

世界の軍事航空部門は、地政学的緊張の高まりと大規模な近代化プログラムによって急成長を遂げています。この急増は、先進的能力を備えた先進的な航空機の需要に拍車をかけています。世界の軍事費は増加傾向にあり、各国は防衛強化を優先しているため、先進航空機市場は拡大に向かっています。2023年の世界の軍事費のピークは2兆4,400億米ドルで、2022年から9%の大幅増となります。

世界の防衛支出の増加に伴い、各国は自国の安全保障を強化するために軍用機にますます注目するようになっています。このような需要の高まりは、ある出来事によって裏付けられています。例えば、2024年6月、トルコと米国は記念碑的な契約を締結し、トルコは230億米ドルで40機の新型F-16を取得しました。同様に2024年1月、Lockheed Martinはスロバキア初のF-16を2機納入しました。このF-16はノースロップ・グラマンの最新鋭APG-83 AESAレーダーを搭載しています。ブロック70/72のF-16に搭載されているこのレーダーは、F-22やF-35から先進的機能を受け継ぎ、状況認識能力の向上、全天候型照準、詳細なデジタル地図表示を記載しています。パイロットは、スルーやズームなどのカスタマイズ型機能から恩恵を受け、操作能力をさらに高めることができます。

これに続き、Honeywellはレーダー技術をさまざまな軍用機に拡大しました。HoneywellのRDR-7,000気象レーダーシステムは、防衛と軍事用途に比類のない気象に関する洞察と状況認識を提供するように設計された最先端のソリューションです。特に、輸送機、ヘリコプター、特殊任務機など、幅広い軍用機にシームレスに統合できるように設計されています。これらの進歩は、今後数年間における市場の大幅な成長を促進する原動力となっています。

予測期間中、アジア太平洋が最も高いCAGRを記録

アジア太平洋は、予測期間中に最も高いCAGRを記録し、世界の航空セクタをリードすることになります。特筆すべきは、中国が民間航空セグメントで米国を追い越す勢いであることで、インドは英国を追い抜き、最大・第3位の市場に位置づけられます。この急成長は、航空会社の堅実な機材調達戦略と空港インフラの大幅な拡大に支えられています。2022年、中国は航空インフラを強化し、新たに6つの貨物空港と29の汎用空港を導入し、年末の合計数はそれぞれ254と399となりました。今後、中国は旅客需要の増大に対応するため、2035年までにさらに215の空港を増設するという野心的な計画を立てています。

同様の動きとして、インド民間航空省は2023年6月、今後2~3年以内に同国の空港数をヘリポートを含めて200~220に増やす計画を発表しました。インドは、この拡大を支える空港投資に、公的資金と民間資金の両方から120億米ドルという多額の予算を割り当てています。これらの空港がますます多様な気象レーダー技術を採用するにつれて、市場の需要はさらに拡大します。例えば、2024年2月、Termaはインド空港公団と契約を締結し、その有名なSCANTER 5502表面移動レーダー(SMR)をインドの4つの主要空港(ベンガルール、ムンバイ、ナビ・ムンバイ、ハイデラバード)に配備しました。信頼性の高い全天候型探知能力で知られるSCANTER 5502は、これらインドの極めて重要な空港の運用効率を大幅に高める態勢を整えています。

さらに、いくつかの地域の軍事が気象レーダーの調達を大幅に強化しており、その結果、航空気象レーダーの需要が高まっています。2024年5月には、Bharat Electronicsがドップラー気象レーダーの受注を明らかにし、総額48億1,000万インドルピー(約5,760万米ドル)に達しました。同様に、2024年4月、在パキスタン日本大使館は、スククール気象モニタリングレーダープロジェクトに対して550万米ドルの追加助成を約束しました。当初2021年1月に発表された1,312万米ドルのプロジェクトは、国際協力機構によって支援され、スークルレーダーの設置後はパキスタンのほぼ90%をカバーすることになります。これらの進歩は、今後数年間、この地域市場の成長にとって極めて重要な促進要因になると考えられます。

航空気象レーダー産業概要

航空気象レーダー市場は、Honeywell International Inc.、Collins Aerospace(RTX Corporation)、L3Harris Technologies Inc.、Leonardo SpA、Garmin Ltd.などの主要企業によって統合され、支配されています。このような優位性は、航空用気象レーダーを生産する企業の数が限られているため、市場が集中していることによる。

これらの企業は、より広範な航空機メーカーに対応するため、製品提供を拡大しています。例えば、2022年にスパイア・世界は、米国を拠点とする情報・モニタリング・偵察(ISR)企業であるTCOMに気象予報を提供する5年間の重要な契約を獲得しました。この契約では、TCOMがエアロスタット(揚力ガスを利用して飛行する航空機)を運用する10カ所に天気予報サービスを提供することになっています。このような戦略的な動きは、市場関係者間の競合情勢を再構築する構えです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場の促進要因

- 市場抑制要因

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- エンドユーザー

- 空港

- 航空機

- 民間航空機

- 軍用機

- 一般航空

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- ロシア

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- その他のラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- エジプト

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Honeywell International Inc.

- Collins Aerospace(RTX Corporation)

- L3Harris Technologies Inc.

- Leonardo SpA

- Garmin Ltd

- EWR Radar Systems Inc.

- Selex ES GmbH

- Vaisala Oyj

- Telephonics Corporation

- THALES

第7章 市場機会と今後の動向

The Aviation Weather Radar Market size is estimated at USD 214.08 million in 2025, and is expected to reach USD 256.11 million by 2030, at a CAGR of 3.65% during the forecast period (2025-2030).

The aviation weather radar market is experiencing a surge in demand for advanced radar systems, driven by the critical need for weather monitoring. Safeguarding aircraft from adverse weather conditions emerges as a key market driver. Instances of unexpected weather disturbances lead to aircraft disruptions and, in severe cases, damage, underscoring the urgency for airports to adopt weather radars.

Adopting state-of-the-art radar technologies, notably pulse-doppler radar, enables aircraft to navigate adverse weather conditions more efficiently and safely. Additionally, the industry is witnessing a notable shift toward lighter, more compact radar systems, offering improved fuel efficiency and lower maintenance costs.

However, the market faces challenges, including the high costs and complexities of radar systems and regulatory and environmental obstacles. Market players need to focus on R&D, innovation, and collaboration to overcome these challenges and stay competitive. While these hurdles could potentially hinder market growth, the rising demand from the commercial, general, and military aviation industries for advanced radar systems is set to drive the market positively during the forecast period.

Aviation Weather Radar Market Trends

Military Aviation to Exhibit Highest Growth Rate During the Forecast Period

The global military aviation sector is experiencing a surge, driven by rising geopolitical tensions and extensive modernization programs. This surge is spurring the demand for advanced aircraft with heightened capabilities. With global military expenditures on the rise and nations prioritizing defense enhancements, the market for advanced aircraft is poised for expansion. In 2023, global military spending peaked at USD 2,440 billion, marking a significant 9% increase from 2022.

As global defense spending climbs, countries are increasingly looking to military aircraft to bolster their security. This heightened demand is underscored by certain events. For instance, in June 2024, Turkey and the United States sealed a monumental deal, with Turkey acquiring 40 new F-16 aircraft in a USD 23 billion agreement. Similarly, in January 2024, Lockheed Martin delivered Slovakia's first two F-16s, featuring Northrop Grumman's cutting-edge APG-83 AESA radar. This radar, found in the Block 70/72 F-16s, inherits advanced capabilities from its F-22 and F-35 counterparts, offering improved situational awareness, all-weather targeting, and detailed digital map displays. Pilots benefit from tailored features like slew and zoom, further enhancing their operational capabilities.

Following suit, Honeywell extended its radar technology to a range of military aircraft. The RDR-7000 weather radar system from Honeywell is a cutting-edge solution designed to provide unparalleled weather insights and situational awareness for defense and military applications. Notably, it is engineered for seamless integration across a broad spectrum of military aircraft, including transport, helicopters, and specialized mission planes. These advancements are primed to drive significant market growth in the years ahead.

Asia-Pacific to Register the Highest CAGR During the Forecast Period

Asia-Pacific is set to lead the global aviation sector, boasting the highest CAGR during the forecast period. Notably, China is on track to overtake the United States in commercial aviation, while India is poised to outstrip the United Kingdom, positioning itself as the largest and third-largest market. This growth surge is underpinned by airlines' robust fleet procurement strategies and substantial expansions in airport infrastructure. In 2022, China bolstered its aviation infrastructure, introducing six new freight airports and 29 general-purpose airports, bringing the year-end totals to 254 and 399, respectively. Looking forward, China has ambitious plans to add a further 215 airports by 2035 to cater to the escalating passenger demands.

In a similar vein, the Indian Ministry of Civil Aviation, in June 2023, unveiled plans to elevate the country's airport count to 200-220, including heliports, within the next 2-3 years. India has allocated a significant USD 12 billion for airport investments to support this expansion, drawing from both public and private funding. As these airports increasingly adopt diverse weather radar technologies, the market demand is further amplified. For instance, in February 2024, Terma clinched a contract with the India Airports Authority to deploy its renowned SCANTER 5502 surface movement radars (SMRs) in four major Indian airports, namely Bengaluru, Mumbai, Navi Mumbai, and Hyderabad. Renowned for its reliable all-weather detection capabilities, the SCANTER 5502 is poised to significantly enhance the operational efficiency of these pivotal Indian airports.

Furthermore, several regional militaries are significantly boosting their procurement of weather radars, consequently driving up the demand for aviation weather radars. On this note, in May 2024, Bharat Electronics revealed orders totaling INR 481 crore (approx. USD 57.6 million), with a notable Doppler weather radar order. Similarly, in April 2024, the Embassy of Japan in Pakistan pledged an additional USD 5.5 million grant for the Sukkur weather surveillance radar project. Initially announced in January 2021 at a cost of USD 13.12 million, the project, bolstered by the Japan International Cooperation Agency, is set to cover nearly 90% of Pakistan after the Sukkur radar's installation. These advancements are poised to be pivotal drivers for the regional market's growth in the years to come.

Aviation Weather Radar Industry Overview

The aviation weather radar market is consolidated and dominated by key players, including Honeywell International Inc., Collins Aerospace (RTX Corporation), L3Harris Technologies Inc., Leonardo SpA, and Garmin Ltd. This dominance is due to the limited number of companies producing weather radars for aviation, resulting in a concentrated market.

These companies are expanding their product offerings to cater to a broader range of aircraft manufacturers. For example, in 2022, Spire Global secured a significant five-year contract to provide weather forecasts for TCOM, a US-based intelligence, surveillance, and reconnaissance (ISR) firm. The agreement entails delivering weather forecast services to 10 sites where TCOM operates aerostats (aircraft that utilize lifting gas for flight). Such strategic moves are poised to reshape the competitive landscape among market players.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 End User

- 5.1.1 Airport

- 5.1.2 Aircraft

- 5.1.2.1 Commercial Aviation

- 5.1.2.2 Military Aviation

- 5.1.2.3 General Aviation

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 France

- 5.2.2.3 Germany

- 5.2.2.4 Russia

- 5.2.2.5 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 Latin America

- 5.2.4.1 Brazil

- 5.2.4.2 Rest of Latin America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 Egypt

- 5.2.5.4 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Honeywell International Inc.

- 6.2.2 Collins Aerospace (RTX Corporation)

- 6.2.3 L3Harris Technologies Inc.

- 6.2.4 Leonardo SpA

- 6.2.5 Garmin Ltd

- 6.2.6 EWR Radar Systems Inc.

- 6.2.7 Selex ES GmbH

- 6.2.8 Vaisala Oyj

- 6.2.9 Telephonics Corporation

- 6.2.10 THALES