動物用医薬品:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Veterinary Medicine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1689812

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

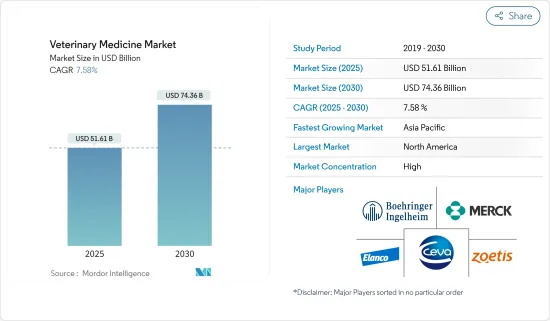

動物用医薬品の市場規模は2025年に516億1,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは7.58%で、2030年には743億6,000万米ドルに達すると予測されます。

メガ動向とマクロ成長促進要因:動物用医薬品市場は、いくつかの重要なメガ動向に後押しされ、大幅な拡大を目の当たりにしています。その最たるものがペットの人間化であり、動物の健康に対する意識の高まりとともに、ペットヘルスケアの重要性が高まっています。農業と人間のヘルスケアの両方における動物由来製品に対する需要の高まりが、この市場をさらに牽引しています。これらの要因は、動物の慢性疾患負担の増加、ペットや養鶏場の所有者による医薬品介入へのシフト、食肉やその他の動物由来製品に対する需要の高まりといった追加的な成長促進要因によって支えられています。

動物における慢性疾患の負担の増大と動物の採用増加:コンパニオンアニマルの慢性疾患はますます蔓延しており、犬の4頭に1頭は生涯のうちにがんと診断されると予想されています。変形性関節症のような疾患は、1歳以上の犬の推定20%が罹患しています。このような慢性疾患の増加は、ペットの飼育率の増加と一致しています。米国では約70%の世帯がペットを飼っており、動物用医薬品、診断、治療薬の需要をさらに押し上げています。ペットの飼い主は、ペットの健康と長寿に関心を持ち、先進的な動物ヘルスケア製品を積極的に求めています。

ペットと養鶏場の所有者による医薬品選好の増加:ペットの飼い主や養鶏農家は、感染症や慢性疾患の治療に医薬品を利用するようになっています。非ステロイド性抗炎症薬(NSAIDs)は犬の変形性関節症の治療に広く使用されており、グルココルチコイドはコンパニオンアニマルの慢性呼吸器疾患の治療に一般的になってきています。養鶏業では、フルラナーのような全身性の外部寄生虫駆除薬が蔓延への対処に好まれています。このような動物疾患治療への医薬品介入へのシフトは、特に家畜の健康管理やペット薬に重点を置くセクターにおいて、動物用医薬品市場の成長に拍車をかけています。

農業と人間のヘルスケアにおける食肉と動物由来製品の需要増加:OECD-FAO Agricultural Outlook Reportによれば、世界の食肉需要は増加傾向にあり、牛肉と子牛肉の消費量は2031年までに76,386kt cweに達すると予測されています。同様に、豚肉の消費量も同期間に18,000 kt cwe以上増加すると予想されています。この成長は、より健康な家畜を要求し、ワクチンや栄養補助食品を含む動物用ヘルスケア製品の必要性を煽る。エノキサパリンや乳糖のような医薬品など、ヒトのヘルスケアにおける動物由来製品の増加も、業界のニーズを満たすために動物の健康を維持することの重要性を強調しています。

動物用医薬品の市場動向

医薬品:動物用医薬品を支配するセグメント概要:

医薬品セグメントは動物用医薬品市場の最前線にあり、市場全体の51%を占めています。このセグメントには、抗生物質、抗炎症薬、寄生虫駆除薬など、コンパニオンアニマルや家畜が直面する健康問題に対処するために不可欠な動物用医薬品が幅広く含まれています。病気の治療と予防のために動物用医薬品を重視することは、世界的に動物の健康を確保する上で重要なことです。

成長の原動力:がん、変形性関節症、呼吸器疾患などの慢性疾患が動物に蔓延するようになったことで、医薬品に対する需要が高まっています。ペットの飼い主も畜産業者も同様に、これらの症状を管理する解決策を求めており、動物用医薬品市場の拡大を後押ししています。畜産においては、食肉や動物由来製品の安全な生産を確保する必要性も、特に家畜の健康管理に重点を置く地域における動物用医薬品の需要を支えています。

競合情勢:医薬品分野が引き続き優位を占める中、市場各社は技術革新に注力しています。研究開発の努力は、より優れた効能と副作用の少ない新しい製剤を生み出すことに向けられています。さらに、企業は抗生物質の代替品を模索し、より持続可能で環境に優しい製品を開発しています。こうした努力は、買収による製品ポートフォリオの拡大への注力と相まって、市場競争力を維持するために不可欠です。

アジア太平洋地域:動物用医薬品成長の震源地、地域ダイナミクス:

アジア太平洋地域は動物用医薬品の急成長地域として浮上しており、2029年までのCAGRは8.5%と予測されています。この需要急増の背景には、中国、インド、日本などにおける急速な都市化、可処分所得の増加、ペット飼育に対する考え方の変化があります。また、人獣共通感染症の流行が拡大していることも、動物用ヘルスケア製品への関心を高め、病気の管理と予防を目的とした政府の取り組みを促しています。

マーケットカタリスト:この地域では畜産業が急成長しており、これが動物用ワクチンと医薬品の需要を牽引しています。中国やインドのような国々では肉製品の消費が増加しており、家畜の健康管理の改善が必要とされています。さらに、特に都市部ではペットの人間化が進み、コンパニオンアニマル・ケアへの支出が増加しており、動物病院・製品市場の成長に拍車をかけています。

戦略的課題:アジア太平洋地域で成功するために、市場プレーヤーは、特定の文化的嗜好や健康上の要件を満たすために製品をローカライズするようになってきています。現地の流通業者との提携や地域の製造施設への投資は、世界企業がより効果的に市場に浸透するのに役立っています。さらに、高度なヘルスケア・オプションについて獣医師や飼い主を教育することは、特に消費者がより包括的な獣医学的診断や手術のオプションを求めるにつれて、市場戦略の中核的要素になりつつあります。

動物用医薬品業界の概要

市場の特徴:世界プレーヤーが統合市場を独占世界の動物用医薬品市場は、高いレベルの統合が特徴であり、いくつかの主要企業が市場で大きなシェアを占めています。Zoetis、Merck &Co.Inc.、ベーリンガー・インゲルハイム、エランコなどの企業が、世界な展開と幅広い製品ラインアップを武器に、圧倒的なシェアを占めています。これらの企業は、強力なブランド認知度と強固な流通網の恩恵を受けており、動物用ヘルスケア製品市場での競争力を維持しています。

主要企業イノベーションと多様な製品提供ZoetisやMerck Animal Healthのような市場の主要企業は、新たな健康懸念に対応し、動物用医薬品を改善するための研究開発に継続的に投資しています。例えばZoetisは、呼吸器系ワクチンからConveniaのような特殊なペット用医薬品まで、製品ポートフォリオを多様化しています。また、戦略的買収も重要な役割を果たしており、ビルバック社などはコンパニオンアニマルケア製品を強化するためにiVet LLCのような企業を買収しています。このような努力は、競争の激しい市場でリーダーシップを維持するための革新と拡大の重要性を強調しています。

将来の成功のための戦略:調査と市場拡大成長を持続させるためには、大手企業は調査と市場拡大への投資を続けなければならないです。新興市場、特にペット飼育率が上昇している地域には、大きなビジネスチャンスがあります。地理的な多角化と獣医遠隔医療ソリューションの開発に注力することで、企業は身近な動物ヘルスケアに対する需要の高まりに応えることができます。さらに、製品開発において持続可能性と環境に優しい慣行を優先する企業は、動物用医薬品市場の予測成長でシェアを獲得する上で有利な立場になると思われます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 動物の慢性疾患に対する負担の増大と動物飼育の増加

- ペットや養鶏場のオーナーによる薬剤嗜好の増加

- 農業および人間のヘルスケアにおける肉および動物由来製品に対する需要の増加

- 市場抑制要因

- 動物ヘルスケアに関連する高コスト

- 新興国における動物医療に対する認識不足

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 製品タイプ別

- 医薬品

- 抗感染症薬

- 抗炎症薬

- 寄生虫駆除薬

- その他の医薬品

- ワクチン

- 不活性ワクチン

- 不活化ワクチン

- 組み換えワクチン

- その他のワクチン

- 薬用飼料添加物

- アミノ酸

- 抗生物質

- その他の薬用飼料添加物

- 医薬品

- 動物タイプ別

- コンパニオンアニマル

- 犬

- 猫

- その他のコンパニオンアニマル

- 畜産動物

- 家畜

- 家禽

- 豚

- 羊

- その他の畜産動物

- コンパニオンアニマル

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Boehringer Ingelheim

- Ceva Animal Health LLC

- China Animal Husbandry Co. Ltd

- Dechra Pharmaceuticals PLC

- Elanco

- Merck & Co. Inc.

- Neogen Corporation

- Phibro Animal Health Corporation

- Sanofi SA

- Vetoquinol SA

- Virbac

- Zoetis

第7章 市場機会と今後の動向

目次

The Veterinary Medicine Market size is estimated at USD 51.61 billion in 2025, and is expected to reach USD 74.36 billion by 2030, at a CAGR of 7.58% during the forecast period (2025-2030).

Megatrends and Macro Growth Drivers: The Veterinary Medicine Market is witnessing substantial expansion, propelled by several critical megatrends. Chief among these is the increasing humanization of pets, which elevates the importance of pet healthcare, along with a growing awareness of animal health. Rising demand for animal-derived products-both in agriculture and human healthcare-further drives this market. These factors are supported by additional growth drivers such as the increasing burden of chronic diseases in animals, a shift toward pharmaceutical interventions by pet and poultry farm owners, and a heightened demand for meat and other animal-based products.

Growing Burden of Chronic Disease Conditions in Animals, Coupled with the Increasing Adoption of Animals: Chronic diseases in companion animals are becoming more prevalent, with one in four dogs now expected to be diagnosed with cancer during their lifetime. Conditions like osteoarthritis affect an estimated 20% of dogs older than one year. This increase in chronic conditions aligns with a growing rate of pet ownership. In the U.S., approximately 70% of households own a pet, further driving the demand for veterinary pharmaceuticals, diagnostics, and treatments. Pet owners, concerned with the health and longevity of their pets, are actively seeking advanced animal healthcare products.

Increase in Drug Preferences by Pet and Poultry Farm Owners: Pet owners and poultry farmers are increasingly turning to pharmaceutical solutions for treating both infectious and chronic diseases. Non-steroidal anti-inflammatory drugs (NSAIDs) are widely used to manage osteoarthritis in dogs, while glucocorticoids are becoming more common in treating chronic respiratory conditions in companion animals. In poultry farming, systemic ectoparasitic drugs like fluralaner are preferred for addressing infestations. This shift towards pharmaceutical interventions for animal disease treatment is spurring growth in the veterinary drug market, especially in sectors focusing on livestock health management and pet medication.

Increased Demand for Meat and Animal-based Products in Agriculture and Human Healthcare: The global demand for meat is on the rise, with beef and veal consumption projected to reach 76,386 kt cwe by 2031, according to the OECD-FAO Agricultural Outlook Report. Similarly, pig meat consumption is expected to grow by over 18,000 kt cwe in the same period. This growth demands healthier livestock, which fuels the need for veterinary healthcare products, including vaccines and nutritional supplements. The rise of animal-derived products in human healthcare, such as pharmaceuticals like enoxaparin and lactose, also underscores the importance of maintaining animal health to meet industry needs.

Veterinary Medicine Market Trends

Drugs: Dominating the Veterinary Medicine Landscape Segment Overview:

The Drugs segment is at the forefront of the Veterinary Medicine Market, representing 51% of the market's total size. This segment includes a broad spectrum of veterinary pharmaceuticals, such as antibiotics, anti-inflammatory medications, and parasiticides, all essential for addressing the health issues faced by both companion animals and livestock. This focus on veterinary drugs for disease treatment and prevention is key to ensuring the wellbeing of animals globally.

Growth Drivers: The increasing prevalence of chronic conditions in animals, such as cancer, osteoarthritis, and respiratory diseases, has created a growing demand for pharmaceutical interventions. Pet owners and livestock producers alike are seeking solutions to manage these conditions, pushing the veterinary pharmaceutical market to expand. In livestock farming, the need to ensure the safe production of meat and animal-based products also supports the demand for veterinary pharmaceuticals, especially in regions focused on livestock health management.

Competitive Landscape: As the Drugs segment continues to dominate, market players are focusing on innovation. Research and development efforts are being directed toward creating novel drug formulations with better efficacy and fewer side effects. Moreover, companies are exploring alternatives to antibiotics and developing more sustainable and eco-friendly products. These efforts, coupled with a focus on expanding product portfolios through acquisitions, are critical for maintaining market competitiveness.

Asia-Pacific: The Epicenter of Veterinary Medicine Growth Regional Dynamics:

Asia-Pacific is emerging as the fastest-growing region for veterinary medicine, with a projected CAGR of 8.5% through 2029. This surge in demand is driven by rapid urbanization, increased disposable incomes, and shifting attitudes toward pet ownership in countries like China, India, and Japan. The growing prevalence of zoonotic diseases has also heightened awareness of animal healthcare products, prompting government initiatives aimed at disease control and prevention.

Market Catalysts: The region's rapidly growing livestock industry is a major driver of demand for veterinary vaccines and pharmaceuticals. Countries like China and India are seeing increased consumption of meat products, which necessitates better livestock health management practices. Furthermore, the rise in pet humanization, particularly in urban centers, has resulted in higher spending on companion animal care, spurring the growth of the veterinary clinics and products market.

Strategic Imperatives: To succeed in the Asia-Pacific region, market players are increasingly localizing products to meet specific cultural preferences and health requirements. Partnerships with local distributors and investments in regional manufacturing facilities are helping global companies penetrate the market more effectively. Additionally, educating veterinarians and pet owners about advanced healthcare options is becoming a core component of market strategy, especially as consumers demand more comprehensive veterinary diagnostics and surgery options.

Veterinary Medicine Industry Overview

Market Characteristics: Global Players Dominate Consolidated Market The global Veterinary Medicine Market is characterized by a high level of consolidation, with several key players commanding a significant share of the market. Companies such as Zoetis, Merck & Co. Inc., Boehringer Ingelheim, and Elanco dominate, leveraging their global reach and extensive product offerings. These companies benefit from strong brand recognition and robust distribution networks, allowing them to maintain a competitive edge in the animal healthcare products market.

Major Players: Innovation and Diverse Product Offerings Key market players like Zoetis and Merck Animal Health continuously invest in research and development to address emerging health concerns and improve veterinary pharmaceuticals. Zoetis, for example, has diversified its portfolio with products ranging from respiratory vaccines to specialized pet medication like Convenia. Strategic acquisitions also play a pivotal role, with companies such as Virbac acquiring firms like iVet LLC to strengthen their companion animal care offerings. These efforts underline the importance of innovation and expansion in maintaining leadership in a competitive market.

Strategies for Future Success: Research and Market Expansion To sustain growth, leading players must continue investing in research and market expansion. Emerging markets, particularly in regions with rising pet adoption rates, offer substantial opportunities. Geographic diversification and a focus on developing veterinary telemedicine solutions will help companies meet the growing demand for accessible animal healthcare. Additionally, companies that prioritize sustainability and environmentally friendly practices in product development will be better positioned to capture a share of the Veterinary Medicine Market's projected growth.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Burden of Chronic Disease Conditions in Animals, Coupled with the Increasing Adoption of Animals

- 4.2.2 Increase in Drug Preferences by Pet and Poultry Farm Owners

- 4.2.3 Increased Demand for Meat and Animal-based Products in Agriculture and Human Healthcare

- 4.3 Market Restraints

- 4.3.1 High Costs Associated with Animal Healthcare

- 4.3.2 Lack of Awareness about Animal Health in the Emerging Nations

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Product Type

- 5.1.1 Drugs

- 5.1.1.1 Anti-infectives

- 5.1.1.2 Anti-inflammatory

- 5.1.1.3 Parasiticides

- 5.1.1.4 Other Drugs

- 5.1.2 Vaccines

- 5.1.2.1 Inactive Vaccines

- 5.1.2.2 Attenuated Vaccines

- 5.1.2.3 Recombinant Vaccines

- 5.1.2.4 Other Vaccines

- 5.1.3 Medicated Feed Additives

- 5.1.3.1 Aminoacids

- 5.1.3.2 Antibiotics

- 5.1.3.3 Other Medicated Feed Additives

- 5.1.1 Drugs

- 5.2 By Animal Type

- 5.2.1 Companion Animals

- 5.2.1.1 Dogs

- 5.2.1.2 Cats

- 5.2.1.3 Other Companion Animals

- 5.2.2 Livestock Animals

- 5.2.2.1 Cattle

- 5.2.2.2 Poultry

- 5.2.2.3 Swine

- 5.2.2.4 Sheep

- 5.2.2.5 Other Livestock Animals

- 5.2.1 Companion Animals

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Boehringer Ingelheim

- 6.1.2 Ceva Animal Health LLC

- 6.1.3 China Animal Husbandry Co. Ltd

- 6.1.4 Dechra Pharmaceuticals PLC

- 6.1.5 Elanco

- 6.1.6 Merck & Co. Inc.

- 6.1.7 Neogen Corporation

- 6.1.8 Phibro Animal Health Corporation

- 6.1.9 Sanofi SA

- 6.1.10 Vetoquinol SA

- 6.1.11 Virbac

- 6.1.12 Zoetis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日