|

市場調査レポート

商品コード

1689808

痙縮治療:市場シェア分析、産業動向、成長予測(2025年~2030年)Spasticity Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 痙縮治療:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 141 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

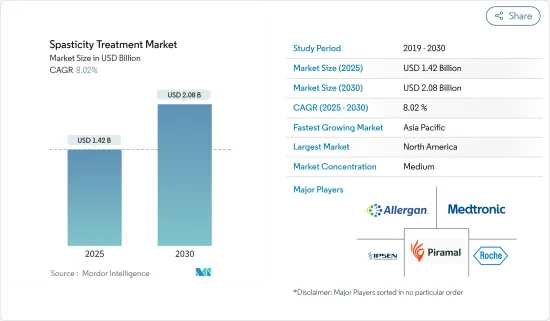

痙縮治療市場規模は2025年に14億2,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは8.02%で、2030年には20億8,000万米ドルに達すると予測されます。

市場成長の主要因は、世界の多発性硬化症、脳性麻痺、脳炎の有病率の増加、啓発プログラムの増加、新技術の採用です。

痙縮症例の増加と痙縮治療のための新技術の採用は、市場の主要促進要因です。例えば、Physicians Group LLCが2023年12月に発行したジャーナルによると、世界中で約1,200万人が痙縮に苦しんでいます。同供給源はまた、ロボット支援療法、電気刺激療法、仮想現実療法を含む現代の理学療法アプローチは、患者の運動機能を強化し痙縮を軽減する上で高い効率を示したと述べています。また、2023年2月に発表された研究によると、重度の痙縮を有する脳卒中患者に対して、ロボット支援による感覚運動療法エクササイズが適用され、大きな成果を示したといいます。この研究では、リハビリ機器による積極的な治療が痙縮治療に様々な効果をもたらすとも述べています。

痙縮を治療するための承認の増加と特殊製品の発売は、市場の成長を促進すると予想されます。例えば、2022年6月には、多発性硬化症やその他の脊髄障害に関連する痙縮の治療として米国FDAに承認されたバクロフェン経口顆粒(5、10、20mg)専門製品であるLYVISPAHが市販されました。Amneal Pharmaceuticalは、錠剤を飲み込むことが困難な痙縮患者に代替薬を提供するため、急速に溶ける風味の顆粒剤という形で同製品を開発しました。

また、痙縮治療のための先端治療の研究開発が活発化していることも、市場の成長をさらに促進すると予想されます。例えば、2023年3月、Saol Therapeuticsは、下肢筋痙縮に対するSL-1002の臨床開発のフェーズII結果を発表しました。下肢筋痙縮に対する第II相医薬品のPTSR(相転移成功率)適応基準は100%であることが判明しました。また、Sentynl Therapeuticsが臨床開発中のパイプライン医薬品であるSTI-103は、現在フェーズIにあり、筋痙縮に対するフェーズI医薬品は、フェーズIIに進むためのPTSR(相転移成功率)適応基準が74%です。したがって、痙縮治療の良好な結果は、市場での痙縮のための先進的な治療の発売が期待され、それによって予測期間中の市場成長を促進すると予想されます。

しかし、治療費の高さが痙縮治療の普及率を低下させることが予想され、予測期間中の市場成長の妨げになると考えられます。

痙縮治療市場動向

脳性麻痺セグメントが痙縮治療市場の主要シェアを占める見込み

脳性麻痺(CP)セグメントは痙縮治療市場で最大のシェアを占めると予想されます。脳性まひ症例の増加や、脳性まひの治療における痙縮治療の利点の増加といった要因が、予測期間中の同セグメントの成長を促進すると予想されます。

脳性麻痺は、世界中で確認される最も一般的な小児疾患の1つです。脳性小児麻痺の症例の増加や痙縮の再発は、痙縮治療市場の需要を促進し、予測期間中の同セグメントの成長に拍車をかけると予想されます。例えば、Cerebral Palsy Guidanceの2024年1月の更新によると、米国では約76万4,000人(幼児と成人を含む)が少なくとも1つの脳性麻痺の症状を持っています。また、毎年約1万人の赤ちゃんが脳性麻痺で生まれています。また、毎年1,200人から1,500人の学齢期の幼児が脳性麻痺と診断されています。

また、CPに関連する臨床検査の実施が承認されたことも、予測期間中の同セグメントの成長をさらに促進しています。例えば、2024年1月、ニューロテックインターナショナルは、脳性麻痺(CP)治療のためのNTI164の第I/II相臨床検査を開始するために、ヒト研究倫理委員会(HREC)から承認を受け、治療用品局(TGA)から許可を受けました。本検査は、脳性麻痺の中で最も有病率の高い痙直型CPの小児患者を対象に、NTI164の有効性と安全性を検討するものです。

したがって、CP症例の増加、CP臨床検査の増加、啓蒙プログラムの増加、CP患者における痙性治療の採用により、このセグメントは予測期間中に成長すると予測されます。

北米が予測期間中に市場を独占する見込み

北米は、多発性硬化症(MS)関連研究への資金提供の増加とドラッグデリバリーソリューションの開発により、痙縮治療市場を独占すると予測されます。したがって、痙縮治療の開発に対する以下のような要因や市場参入企業の取り組みが市場の成長を支え、予測期間中も同様の傾向を維持すると予測されます。

痙縮症状を引き起こす疾患の罹患者数の増加が、同国の市場成長を促進すると考えられます。MS Canadaの2024年2月の最新情報によると、カナダは多発性硬化症(MS)の罹患率が世界で最も高い国の一つであり、約9万人のカナダ人がこの症状を患っています。平均して、毎日12人のカナダ人がMSの診断を受けています。ほとんどの人が20歳から49歳の間にMSと診断され、予測不可能なこの病気の影響は生涯続きます。

痙縮管理における薬剤の有益性に関する調査は、ますます増加しています。調査は、科学的根拠に裏付けられた痙縮治療の利点を理解し、薬剤の使用法を向上させるのに役立っています。例えば、テキサス大学サウスウェスタン校が2023年3月に発表した研究では、経腸バクロフェンは脳性麻痺の痙縮治療に安全で効果的な薬剤であると結論付けています。この薬は投与が容易で副作用も少ないです。

多発性硬化症の罹患率の増加と治療へのアクセスのしやすさが、この国の市場成長を支えています。さらに、同国では費用対効果の高い治療が利用できるようになりつつあるため、予測期間中に市場の成長が急増すると予想されます。

痙縮治療産業概要

痙縮治療市場は適度な競争があり、複数の大手企業で構成されています。市場シェアの面では、現在市場を独占している主要参入企業のうち数社が、市場で満たされていない課題に対処するために新製品を開発しています。例えば、Medtronicは2023年10月、慢性疼痛、がん性疼痛、重度の痙縮患者向けの次世代髄腔内薬剤送達システム「SynchroMed III」の米国食品医薬品局(FDA)承認を取得しました。市場を独占している企業には、Medtronic PLC、Piramal Enterprises Ltd、Allergan PLC、Ipsen、F. Hoffmann-La Roche Ltd.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場の促進要因

- 啓発プログラムの増加と新技術の採用

- 先進治療の上市と手頃な価格の増加

- 市場抑制要因

- 治療費の高騰

- 厳しい規制枠組み

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 薬剤クラス別

- GABAアゴニスト

- α2アドレナリン作動薬

- ボツリヌス毒素

- 薬剤クラス別

- 適応症

- 多発性硬化症(MS)

- 脳性麻痺(CP)

- 外傷性脳損傷(TBI)

- その他

- 投与経路

- 経口

- 非経口

- エンドユーザー

- 小児

- 成人

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Medtronic PLC

- Sun Pharmaceuticals Industries Ltd

- Saol Therapeutics Inc.

- Piramal Enterprises Ltd

- Par Pharmaceuticals LLC

- Allergan PLC

- Ipsen

- F. Hoffmann-La Roche Ltd

- US WorldMeds LLC

- Taj Pharmaceuticals Limited

第7章 市場機会と今後の動向

The Spasticity Treatment Market size is estimated at USD 1.42 billion in 2025, and is expected to reach USD 2.08 billion by 2030, at a CAGR of 8.02% during the forecast period (2025-2030).

The major factors attributing to the market's growth are a growing prevalence of multiple sclerosis, cerebral palsy, and encephalitis around the globe, a rise in awareness programs, and the adoption of novel technologies.

The rising cases of spasticity and the adoption of new technologies for spasticity treatment are the key drivers for the market. For instance, according to the journal published by the Physicians Group LLC in December 2023, around 12.0 million people worldwide suffer from spasticity. The same source also stated that contemporary physical therapy approaches, including robotic-assisted therapy, electrical stimulation therapies, and virtual reality therapy, showcased high efficiency in enhancing motor function and reducing spasticity in patients. Also, according to the study published in February 2023, robotic-assisted sensorimotor therapy exercises were applied on stroke subjects with severe spasticity and have showcased significant achievement. The study also stated that active therapy with rehabilitation devices can lead to various benefits in spasticity treatment.

Rising approvals and the launching specialty products to treat spasticity are anticipated to drive market growth. For instance, in June 2022, LYVISPAH, a baclofen oral granules (5, 10, and 20 mg) specialty product approved by the United States FDA for the treatment of spasticity related to multiple sclerosis and other spinal cord disorders, was commercially launched. Amneal Pharmaceutical has developed the product in the form of rapidly dissolving flavored granules to provide an alternative for spasticity patients who have difficulty swallowing pills.

Also, the rising research and development on advanced therapeutics for treating spasticity is anticipated to drive market growth further. For instance, in March 2023, Saol Therapeutics shared its Phase II results of the clinical development of SL-1002 for lower limb muscle spasticity. The phase transition success rate (PTSR) indication standard for Phase II medicines for Lower Limb Muscle Spasticity was found to be 100%. In addition, a pipeline drug, STI-103, is under clinical development by Sentynl Therapeutics and is currently in Phase I. The Phase I drug for muscle spasticity has a 74% phase transition success rate (PTSR) indication benchmark for progressing into Phase II. Therefore, the positive results of spasticity drugs are expected to have the launch of advanced therapeutics for spasticity in the market, thereby anticipated to drive the market growth during the forecast period.

However, the high cost of the treatment is expected to reduce the adoption rate of spasticity treatment, which is expected to hinder the market growth during the forecast period.

Spasticity Treatment Market Trends

The Cerebral Palsy Segment is Expected to Hold the Major Market Share in the Spasticity Treatment Market

The cerebral palsy (CP) segment is expected to account for the largest of the spasticity drugs market. Factors such as an increase in cerebral palsy cases and a rise in benefits offered by spasticity drugs in treating cerebral palsy are expected to drive the segment growth during the forecast period.

Cerebral palsy is one of the most common childhood disorders witnessed around the globe. An increase in cerebral palsy cases and recurring spasticity is expected to drive the demand for the spasticity treatment market, fueling the segment growth during the forecast period. For instance, as per the January 2024 update by Cerebral Palsy Guidance, around 764,000 people in the United States (including children and adults) have at least one symptom of cerebral palsy. Also, around 10,000 babies are born each year with cerebral palsy. Between 1,200 and 1,500 school-aged children are diagnosed with cerebral palsy each year.

Also, the approval to conduct clinical trials related to CP further facilitates the segment growth during the forecast period. For instance, in January 2024, Neurotech International received approval from the Human Research Ethics Committee (HREC) and clearance from the Therapeutic Goods Administration (TGA) to begin a Phase I/II clinical trial of NTI164 for the treatment of cerebral palsy (CP). The study will investigate the efficacy and safety of NTI164 in pediatric patients with spastic CP, the most prevalent form of CP.

Therefore, owing to the increase in CP cases, growing CP clinical trials, rise in awareness programs, and adoption of spasticity therapies among CP patients, the segment is predicted to grow during the forecast period.

North America is Expected to Dominate the Market During the Forecast Period

North America is expected to dominate the spasticity drugs market owing to the increasing funding for multiple sclerosis (MS) related research coupled with the development of drug delivery solutions in the country. Hence, the following factors and market players' initiatives to develop drugs to treat spasticity are projected to support the market growth and maintain a similar trend during the forecast period.

The increasing number of people affected by diseases causing spasticity symptoms is likely to drive market growth in the country. According to MS Canada's February 2024 update, Canada has one of the world's highest rates of multiple sclerosis (MS), with around 90,000 Canadians living with the condition. On average, 12 Canadians receive an MS diagnosis every day. Most people are diagnosed with MS between the ages of 20 and 49, and the effects of the disease, which can be unpredictable, persist throughout their lives.

Research on the benefits of drugs in spasticity management is increasing. The research assists in comprehending the advantages of spasticity drugs supported by scientific evidence and enhancing the usage of the drugs. For instance, a study published in March 2023 by the University of Texas Southwestern in the National Library of Medicine concluded that enteral baclofen is a safe and effective medication for treating spasticity in cerebral palsy. This medication is easy to administer and has minimal side effects.

The growing incidence rates of multiple sclerosis and the accessibility of the treatment have supported the country's growth in the market. Additionally, the increasing availability of cost-effective treatment in the country is anticipated to surge the market growth during the forecast period.

Spasticity Treatment Industry Overview

The spasticity treatment market is moderately competitive and consists of several major players. In terms of market share, a few of the major players currently dominating the market are developing new products to address unmet challenges in the market. For instance, in October 2023, Medtronic received US Food and Drug Administration (FDA) approval for its next-generation SynchroMed III intrathecal drug delivery system for patients with chronic pain, cancer pain, and severe spasticity. Some companies dominating the market are Medtronic PLC, Piramal Enterprises Ltd, Allergan PLC, Ipsen, and F. Hoffmann-La Roche Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in Awareness Programs and Adoption of Novel Technologies

- 4.2.2 Launch of Advanced Therapeutics and Increased Affordability

- 4.3 Market Restraints

- 4.3.1 High Cost of Treatment

- 4.3.2 Stringent Regulatory Framework

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Drug Class

- 5.1.1 GABA Agonist

- 5.1.2 Alpha2-adrenergic Agonists

- 5.1.3 Botulinum Toxins

- 5.1.4 Other Drug Class

- 5.2 Indication

- 5.2.1 Multiple Sclerosis (MS)

- 5.2.2 Cerebral Palsy (CP)

- 5.2.3 Traumatic Brain Injury (TBI)

- 5.2.4 Other Indications

- 5.3 Route of Administration

- 5.3.1 Oral

- 5.3.2 Parenteral

- 5.4 End User

- 5.4.1 Pediatrics

- 5.4.2 Adults

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Medtronic PLC

- 6.1.2 Sun Pharmaceuticals Industries Ltd

- 6.1.3 Saol Therapeutics Inc.

- 6.1.4 Piramal Enterprises Ltd

- 6.1.5 Par Pharmaceuticals LLC

- 6.1.6 Allergan PLC

- 6.1.7 Ipsen

- 6.1.8 F. Hoffmann-La Roche Ltd

- 6.1.9 US WorldMeds LLC

- 6.1.10 Taj Pharmaceuticals Limited