世界の真菌性角膜炎治療- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Global Fungal Keratitis Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 119 Pages

- 納期

- 2~3営業日

- 商品コード

- 1689803

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

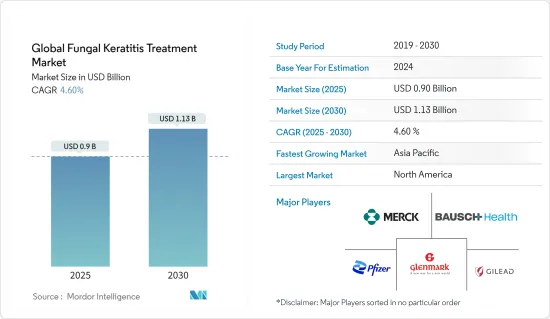

世界の真菌性角膜炎治療市場規模は、2025年に9億米ドルと推定され、予測期間(2025~2030年)のCAGRは4.6%で、2030年には11億3,000万米ドルに達すると予測されます。

COVID-19パンデミックは、真菌性角膜炎治療市場の成長に大きな影響を与えると予測されています。パンデミックの発生により、研究開発活動に携わる主要参入企業のほとんどが、医薬品開発に関連する臨床検査を中止しています。さらに、2020年3月、米国疾病予防管理センターと米国眼科学会は、眼科医を含む医師は、適切な個人防護具の使用を前提としながら、対面診療を緊急かつ緊急性の高い患者に限定すべきであると勧告しました。また、米国では眼科受診が当初80%近く減少し、6月中旬現在でも累積で40%減少していると推定されています。このことは、調査した市場にマイナスの影響を与えると考えられます。

真菌性角膜炎の負担増と市場開拓は、真菌性角膜炎治療市場の成長を促進すると予想されます。2021年1月に発表された紙製「Global Epidemiology of Fungal Keratitis and Its Outcomes(真菌性角膜炎の世界疫学とその転帰)」によると、研究者らは、真菌性角膜炎の世界年間発症率は約100万例で、患者の8%~11%が失明すると推定しています。真菌性角膜炎に関連する危険因子は、外傷、コンタクトレンズの使用、コルチコステロイド外用剤の使用、糖尿病、社会経済的地位の低さです。眼外傷が真菌性角膜炎の最も一般的な危険因子であることは間違いないです。さらに、真菌性角膜炎の新たな治療を開発・発見するための取り組みがいくつか行われています。例えば、2018年9月、インドのL.V. Prasad Eye Instituteは、真菌性角膜炎における5%ナタマイシンと1%ボリコナゾールの併用治療に関するフェーズ2/フェーズ3検査を、無作為化二重マスク臨床検査で完了しました。同ラボは2021年に第IV相検査を開始する予定です。したがって、このような臨床検査の良好な結果が新たな治療につながる可能性があり、次期市場の成長を後押しする可能性が高いです。

また、2021年現在、インドのAravind Eye Care Systemは、真菌性角膜炎におけるコラーゲン・クロスリンキングの視覚的・臨床的転帰を評価するため、局所抗真菌療法を用いたランダム化比較検査を調査中です。この研究は、非治癒性真菌性角膜炎における角膜クロスリンキングが、穿孔の予防と治癒プロセスの促進において果たす役割を明らかにすることを目的としています。このように、前述の要因により、研究対象市場は市場成長に貢献すると期待されているが、製品の特許切れや真菌性角膜炎治療の副作用が、今後数年間の市場成長の妨げになると考えられます。

真菌性角膜炎治療市場の動向

予測期間中、真菌性角膜炎治療市場は局所領域が大きな成長率を示す見込み

真菌性角膜炎の治療には、市販の抗真菌薬や全身用製剤を点眼薬に配合した局所用抗真菌薬が主に使用されています。ナタマイシンは真菌性角膜炎の治療として唯一承認されている外用抗真菌剤です。しかし、ナタマイシンは眼への浸透性が悪いため、主に角膜表層感染の症例に有用です。アンフォテルシンBは、全身投与は副作用と関連しているため、主に局所経路で使用されます。それは一般に非経口的な公式を再構成することによって準備される0.15%の解決として使用されます。カンジダ角膜炎の治療として選択されています。フルコナゾールの誘導体であるボリコナゾール(VCZ)は、外用剤と経口剤があります。しかし、経口ボリコナゾールは真菌感染症に認可されており、1%外用液は適応外使用です。また、外用抗真菌薬とともに、外用タクロリムスなどの免疫抑制剤が真菌性角膜炎を含む真菌感染症の補助療法として使用されています。さらに、技術の進歩や検査の増加に伴い、薬剤溶出コンタクトレンズのような新たな標的デリバリーが注目を集めています。外用薬は真菌性角膜炎に有効であるが、眼への浸透性が低いことが市場の主要抑制要因となっています。一方、新しい局所製剤の開発と真菌性角膜炎に対する唯一の承認薬であることから、局所投与経路は一定期間大きな成長を維持すると予想されます。

北米が市場で大きなシェアを占めると予想され、予測期間中も同様と予想される

北米は、真菌性角膜炎の症例の増加と真菌性角膜炎の治療における新たな動向により、真菌性角膜炎治療市場を独占すると予想されます。米国は、真菌性角膜炎患者の増加やその他の慢性眼疾患、研究開発費の増加により、予測期間を通じて北米地域の真菌性角膜炎治療市場全体を支配すると予想されます。米国では、真菌性角膜炎は湿度が高く温暖な地域でよく見られます。2020年10月に発表された「The global incidence and diagnosis of fungal keratitis」(真菌性角膜炎の世界的発生率と診断)と題された研究によると、米国南部は他の地域と比較して真菌性角膜炎の有病率が高いです。さらに、2019年の経済協力開発機構(OECD)によると、米国の総医療支出は3兆6,341億米ドルでした。研究開発費の増加や大手参入企業の存在が需要の伸びをもたらす可能性があります。真菌性角膜炎の病態生理を理解するためにいくつかの研究が実施されており、この地域での市場研究を支援すると期待されています。例えば、2020年6月にAmerican Journal of Ophthalmology誌に掲載された研究では、内皮角膜形成術の際にドナー縁組織の真菌培養が陽性であれば、患者に真菌性角膜炎を発症させる主要な危険因子となることが明らかになりました。このような研究により、適切な予防治療戦略の必要性が生じ、調査された市場にプラスの影響を与えると予想されます。現在、糸状菌による真菌性角膜炎の治療の第一選択薬としてFDAに承認されている唯一の抗真菌薬は、Novartisが開発したNatacyn(ナタマイシン点眼液5%)です。2019年10月、このナタシンはEyevance PharmaceuticalsがNovartisから買収しました。したがって、上記のすべての要因は、予測期間中に同地域の市場成長を促進すると予想されます。

真菌性角膜炎治療産業概要

真菌性角膜炎治療市場の競争は中程度です。市場シェアの面では、現在、少数の大手企業が市場を独占しています。現在市場を独占している企業には、Pfizer Inc.、Leadiant Biosciences、Gilead Biosciences, Inc.、Bausch Health、Novo Holdings A/S (Xellia Pharmaceuticals)、Alvogen、Merck & Co. Inc.です。各社は競争市場での地位を確保するため、研究開発活動への投資とともに、M&A、共同研究、提携などさまざまな戦略を通じて進化しています。例えば、2019年10月、Eyevance PharmaceuticalsはNovartisからTOBRADEX ST(トブラマイシン/デキサメタゾン点眼液)0.3%/0.05%とNATACYN(ナタマイシン点眼液)5%の買収を発表しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場の促進要因

- 真菌性角膜炎疾患の負担増

- 研究開発の活発化

- 市場抑制要因

- 真菌性角膜炎治療に関連する特許の喪失と副作用

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 投与経路別

- 経口

- 注射剤

- 局所

- 流通チャネル別

- 病院

- ドラッグストア

- その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Alvogen

- Bausch Health

- Gilead Biosciences, Inc.

- Glenmark Pharmaceuticals

- Leadiant Biosciences

- Merck & Co. Inc.

- Aurolab

- Eyevance Pharmaceuticals LLC

- Novo Holdings A/S(Xellia Pharmaceuticals)

- Pfizer Inc.

第7章 市場機会と今後の動向

目次

The Global Fungal Keratitis Treatment Market size is estimated at USD 0.90 billion in 2025, and is expected to reach USD 1.13 billion by 2030, at a CAGR of 4.6% during the forecast period (2025-2030).

The COVID-19 pandemic is anticipated to impact the growth of the Fungal Keratitis Treatment market significantly. The outbreak of pandemic has led most of the major players involved in research and development activities to halt the clinical trials related to drug development. Additionally, in March 2020, the Centers for Disease Control and Prevention and the American Academy of Ophthalmology recommended that physicians, including ophthalmologists, should limit in-person care to urgent and emergent patients while assuming the use of appropriate personal protective equipment. Also, it is estimated that there was a nearly 80% initial decrease in ophthalmology visits and that as of mid-June there was still a cumulative decrease in ophthalmology visits of 40% in the United States. This is likely to have a negative impact on the market studied.

The growing burden of fungal keratitis and product development is expected to fuel the fungal keratitis treatment market growth. According to the article 'Global Epidemiology of Fungal Keratitis and Its Outcomes' published in January 2021, researchers estimated that the annual global incidence of fungal keratitis to be approximately 1 million cases, with 8% to 11% of patients losing an eye. The risk factors associated with fungal keratitis are trauma, contact lens use, topical corticosteroid use, Diabetes mellitus, and low socioeconomic status. Incidental ocular trauma is undoubtedly the most common risk factor for fungal keratitis. Additionally, several efforts are being made to develop and find new therapeutics for fungal keratitis. For instance, in September 2018, L.V. Prasad Eye Institute, India completed the Phase 2/Phase 3 study on Combination Treatment of 5% Natamycin and 1% Voriconazole in Fungal Keratitis with the randomized double-masked clinical trial. The research institute is likely to initiate the Phase IV trials in 2021. Thus, the positive outcomes of such trials may result in a new treatment that is likely to boost the market growth in the upcoming period.

Also, as of 2021, Aravind Eye Care System, India is investigating a randomized control trial with topical anti-fungal therapy to assess the visual and clinical outcomes of collagen cross-linking in fungal keratitis. The study is aimed at finding the role of corneal cross-linking in non-resolving fungal keratitis in the prevention of perforation and enhancement of the healing process Thus, owing to the aforementioned factors, the studied market is expected to contribute to the market growth, however, loss of patents of product and side effects of the fungal keratitis treatment is likely to hinder the growth of the market over upcoming years.

Fungal Keratitis Treatment Market Trends

Topical Segment is Expected to Show a Significant Growth Rate in the Fungal Keratitis Treatment Market Over the Forecast Period

The Topical antifungals, either commercially available or compounded from systemic preparation into eye-drops are the majorly used drugs for the management of fungal keratitis. Natamycin is the only approved topical antifungal preparation for the treatment of fungal keratitis. However, due to the poor ocular penetration, natamycin is primarily been useful in cases with superficial corneal infection. Amphotercin B is majorly used by the topical route as systemic administration is associated with adverse effects. It is commonly used as a 0.15% solution prepared by reconstituting the parenteral formulation. It is the drug of choice for Candida keratitis. Voriconazole (VCZ), a derivative of fluconazole, is available in topical and oral formulations. However, oral voriconazole is approved for fungal infections, 1% topical solution is an off-label use. Also, along with the topical antifungals, immunosuppressants such as topical tacrolimus are employed as adjuvant therapy in fungal infections including fungal keratitis. Moreover, with the growing technological advancements and trials, the new targeted deliveries such as drug-eluting contact lenses are growing attraction. Topical drugs are effective against fungal keratitis, however, poor ocular penetration is the primary restraint in the market. On the other hand, with the development of the new topical formulations and being the only approved medication for fungal keratitis, the topical route of administration is expected to hold significant growth over the period.

North America is Expected to Hold a Significant Share in the Market and Expected to do Same in the Forecast Period

North America is expected to dominate the fungal keratitis treatment market owing to increasing cases of fungal keratitis and emerging trends in the treatment of fungal keratitis. The United States is expected to dominate the overall fungal keratitis treatment market in the North American region, throughout the forecast period, due to the increasing number of fungal keratitis patients, and other chronic eye conditions, along with rising research and development expenditure. In the United States, fungal keratitis is quite common in humid and warm regions. As per the study titled, '' The global incidence and diagnosis of fungal keratitis'', published in October 2020, the southern part of the United States have a higher prevalence of fungal keratitis as compared to other regions. Furthermore, according to the Organization for Economic Co-operation and Development (OECD) in 2019, total healthcare spending in the United States was USD 3,634.1 billion. The rising research and development expenditures and the presence of major players may result in the growth of demand. Several studies are being conducted to understand the pathophysiology for fungal keratitis which is expected to aid the market studied in this region. For instance, a study published in the American Journal of Ophthalmology, in June 2020, revealed that a positive fungal culture on the donor rim tissue during the time of endothelial keratoplasty can be a major risk factor for developing fungal keratitis in the patients. Such studies arise the need for proper preventative treatment strategies which is expected to positively impact the market studied. Currently, the only FDA-approved anti-fungal drug as the first line of treatment for fungal keratitis caused by filamentous fungi is Natacyn (natamycin ophthalmic suspension 5%) developed by Novartis. In October 2019, the Natacyn was acquired by Eyevance Pharmaceuticals from Novartis. Hence, all the above-mentioned factors are expected to boost the market growth in the region during the forecast period

Fungal Keratitis Treatment Industry Overview

The Fungal Keratitis Treatment Market is moderately competitive. In terms of market share, few of the major players are currently dominating the market. Some of the companies which are currently dominating the market are Pfizer Inc., Leadiant Biosciences, Gilead Biosciences, Inc., Bausch Health, Novo Holdings A/S (Xellia Pharmaceuticals), Alvogen, and Merck & Co. Inc. The companies are evolving through various strategies such as mergers and acquisitions, collaborations, and partnerships, along with investment in research and development activities to secure the position in the competitive market. For instance, in October 2019, Eyevance Pharmaceuticals announced the acquisition of TOBRADEX ST (tobramycin/dexamethasone ophthalmic suspension) 0.3%/0.05% and NATACYN (natamycin ophthalmic suspension) 5% from Novartis.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Burden of Fungal Keratitis Disease

- 4.2.2 Increasing Research and Development Activities

- 4.3 Market Restraints

- 4.3.1 Loss of Patents and Side Effects Associated with Fungal Keratitis Treatment Drugs

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Route of Administration

- 5.1.1 Oral

- 5.1.2 Injection

- 5.1.3 Topical

- 5.2 By Distribution Channel

- 5.2.1 Hospitals

- 5.2.2 Drug Stores

- 5.2.3 Others

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Alvogen

- 6.1.2 Bausch Health

- 6.1.3 Gilead Biosciences, Inc.

- 6.1.4 Glenmark Pharmaceuticals

- 6.1.5 Leadiant Biosciences

- 6.1.6 Merck & Co. Inc.

- 6.1.7 Aurolab

- 6.1.8 Eyevance Pharmaceuticals LLC

- 6.1.9 Novo Holdings A/S (Xellia Pharmaceuticals)

- 6.1.10 Pfizer Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 119 Pages

- 納期

- 2~3営業日