|

|

市場調査レポート

商品コード

1910673

空気圧機器:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Pneumatic Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 空気圧機器:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 137 Pages

納期: 2~3営業日

|

概要

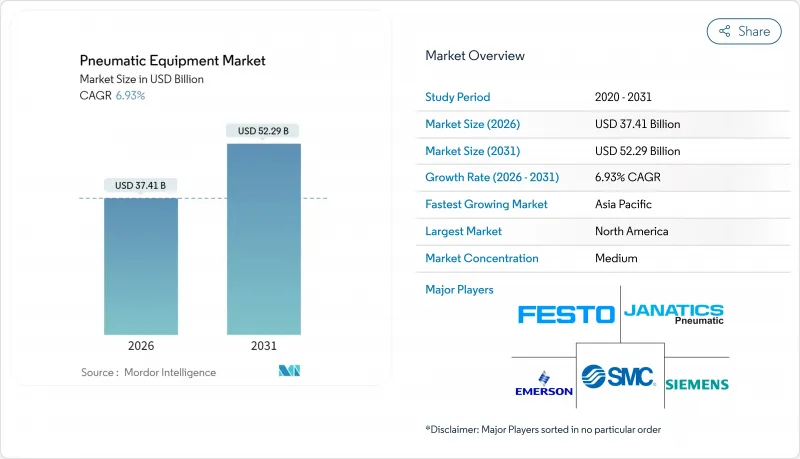

2026年の空気圧機器市場規模は374億1,000万米ドルと推定され、2025年の349億9,000万米ドルから成長し、2031年には522億9,000万米ドルに達すると予測されています。

2026年から2031年にかけてはCAGR6.93%で拡大する見込みです。

産業オートメーションの高度化、省エネルギー型圧縮空気システムの改修、および空気圧ハードウェアとIIoT診断技術の融合が、主要な成長要因となっております。半導体クリーンルーム、電気自動車用バッテリー生産ライン、衛生的な食品工場からの需要急増は、この分野の応用範囲の拡大を裏付けています。市場リーダー企業がダウンタイムとエネルギー損失を削減するため、従来型空気圧技術とデジタル監視を組み合わせることで、競合が激化しています。同時に、主要経済圏における効率性規制の強化が、ハイブリッド電気空気圧ソリューションへの移行を加速させており、サプライヤーに新たな差別化の道を開いています。

世界の空圧機器市場の動向と洞察

産業横断的な自動化の進展

大規模な工場のデジタル化は空気圧設計を再構築しており、サプライヤーは予測分析を可能にするセンサーや無線モジュールの組み込みを促しています。SMCのEXW1無線ノードはバルブマニホールドのサイズを86%削減し、主要な産業用イーサネットプロトコルをサポートしており、小型化と接続性が単一パッケージで融合する実例を示しています。プラント管理者にとって、シリンダーやバルブのリアルタイム健康データは、予期せぬ停止の減少と根本原因分析の迅速化につながります。特に電子機器、自動車、包装製品工場において、新規建設の「無人化」ライン構築に伴う導入勢いが顕著です。ISO 11011に基づく適合性監査では、圧縮空気のベースラインを定量化するソリューションの重要性が増しており、デジタル対応空気圧システムは魅力的な投資対象となっています。測定可能なOEE向上を実証できるサプライヤーは、従来型製品との競争入札で優位に立っています。

省エネルギー型圧縮空気システムへの需要

圧縮空気は産業用電力負荷の約10%を占めており、2025年1月施行の米国エネルギー省(DOE)新効率規制により、既存設備全体の更新が迫られています。アトラスコプコのハイブリッドコンプレッサー製品群は、固定速度モードと可変速駆動(VSD)モードを切り替え可能で、圧力安定性を±0.1バール以内に維持しながら、1台あたり年間9トンのCO2排出削減を実現します。欧州では、ASHRAE 90.1-2022規格に圧縮空気が追加されたことで、建築設計者の要求水準も高まっています。財務面では、漏洩率が30%を超えるケースが多く、工場ごとに年間数万米ドルの電力ロスが発生しているため、短期間で投資回収が可能な改修が促進されています。企業のサステナビリティ担当者は、漏洩検知プログラムを容易に実現可能な脱炭素化施策と位置付けており、高効率空気圧機器への需要をさらに加速させています。

高い生涯維持費とエネルギーコスト

総所有コスト監査によれば、エネルギーコストはコンプレッサーのライフサイクル費用の77%を占め、資本支出を大きく上回ります。漏洩対策プログラムは消費量を削減しますが、小規模プラントでは不足しがちな計測機器と人員を必要とします。オーストラリアの政府調査では平均漏洩率が30%と報告され、世界の非効率性のパターンが確認されています。IIoTセンサーは自動漏洩追跡を約束しますが、初期ハードウェアと分析サービスのサブスクリプション費用が価格に敏感な事業者を躊躇させています。欧州の一部地域で二桁の電力価格上昇が続いていることから、空気圧システムの費用に対する監視が強化され、稼働サイクルが許容する場合、購入者は代替駆動方式への移行を促されています。

セグメント分析

2025年、アップスイングバルブは空気圧機器市場シェアの33.02%を占め、自動化ライン内の圧力・流量制御における中核的役割を浮き彫りにしました。ピックアンドプレースロボットからバルクコンベヤに至るあらゆる回路が、動作シーケンスを調整するための方向制御弁・比例弁に依存しているため、その優位性は持続しています。成長は設置時間を短縮しスマートファクトリー構造に適合する、コンパクトでプロトコル非依存のマニホールドに傾いています。

アクチュエータはCAGR7.46%で加速しており、これはメーカーがより高い積載精度と高速サイクルレートを必要としていることを反映しています。エマーソンのXVシリーズはスリムな設置面積で毎分350NLの流量を実現し、設計者がスループットを犠牲にすることなくキャビネットを小型化することを可能にします。クリーンエア規制の強化に伴い、エアプレパレーションユニットと精密継手がコンポーネント構成を補完し、予知保全の導入によりセンサーアクセサリーが盛んになっています。こうした結果、空圧機器市場は単体部品から、完全に統合されたデータ豊富なアセンブリへと移行を続けております。

2025年の空気圧機器市場における需要の40.02%をモーションコントロールが占め、リニアスライド、回転テーブル、プレスステーションなどでの普及度の高さを反映しています。この分野は、空気圧の優れた出力重量比とミリ秒単位の応答性という、高速組立ラインで重視される特性を活かしています。現在は、トレーサビリティのためにストロークデータをMESプラットフォームに送信するフィードバック対応シリンダーが重視されています。

マテリアルハンドリングは、電子商取引物流が自動仕分けセンターを牽引する中、7.95%という最速のCAGRを記録しています。協働ロボットとの連携認証を取得したSMCのRMHグリッパーは、ソフトタッチ把持が新たなSKU処理能力を開拓する好例です。流体制御はプロセス産業でニッチ市場を維持する一方、真空発生装置は半導体ウエハー搬送分野で拡大しています。融合の傾向が顕著で、先進的なマニホールドは位置決め・把持・真空制御を単一ノードに統合し、空圧機器市場におけるサプライヤーの顧客定着率を強化しています。

地域別分析

北米は、高仕様ソリューションを必要とする航空宇宙、製薬、自動車産業の成熟により、2025年の世界収益の34.21%を占めました。シーメンスがテキサス州とカリフォルニア州の新工場に100億米ドルを投資したことは、同地域における継続的なリショアリング動向を示しており、モーション、バルブ、コンプレッサーパッケージの部品受注を押し上げています。米国エネルギー省(DOE)のコンプレッサー規制が迫る中、設備更新サイクルを安定させる改修の波が起きています。

アジア太平洋地域は7.66%という最も高いCAGRを示しており、中国、インド、ASEAN諸国における新ファブやバッテリー工場の建設により、2031年までにその差を縮める見込みです。アトラスコプコによる韓国・キョンウォン機械の4,650万米ドルでの買収は、供給の現地化と急増する地域需要への対応という戦略的動きを示しています。インドとベトナムにおける半導体自給自足に向けた政府の優遇措置は、超クリーンな空圧機器への新たな需要を喚起しています。

欧州は厳格なエネルギー・持続可能性指令に支えられ、堅調なシェアを維持しています。ボッシュ・レックスロスのメキシコにおける1億6,000万ユーロの工場建設は、欧州OEMメーカーの二極化戦略を浮き彫りにしています。すなわち、研究開発は本国に維持しつつ、米国顧客基盤に近い地域にコスト効率の高い生産能力を構築する戦略です。南米および中東における小規模ながら成長中の機会は、頑丈な高圧空気圧アレイを必要とする石油化学多角化プロジェクトに依存しており、空気圧機器市場に漸増的な需要量をもたらしています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 産業全体における自動化の進展

- 省エネルギー型圧縮空気システムへの需要

- 衛生的な食品・飲料加工ラインの急速な成長

- 電気自動車製造施設の拡大

- マイクロアクチュエータに対するマイクロ流体アセンブリの需要

- IIoTを活用した予知保全の改修

- 市場抑制要因

- 高いライフサイクル維持費およびエネルギーコスト

- 精密作業における電動アクチュエータへの代替

- 圧縮空気漏れに対するESG基準に基づく罰則

- 半導体製造工場向け超清浄圧縮空気の不足

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- マクロ経済の影響分析

第5章 市場規模と成長予測

- コンポーネント別

- アクチュエータ

- バルブ

- エアプレパレーションユニット(FRL)

- 継手およびチューブ

- エアコンプレッサー

- 真空発生装置

- アクセサリー

- 機能別

- モーションコントロール

- 流体制御

- マテリアルハンドリング

- 真空の創造

- 発電/空気供給

- エンドユーザー業界別

- 自動車

- 食品・飲料の加工および包装

- 航空宇宙・防衛

- ライフサイエンス(製薬・医療機器)

- 電子機器および半導体

- 化学・石油化学

- 包装機械

- その他のエンドユーザー産業

- 圧力範囲別

- 低気圧(7バール未満)

- 中圧(7~15バール)

- 高圧(15バール以上)

- 地域別

- 北米

- 米国

- カナダ

- 南米

- ブラジル

- アルゼンチン

- チリ

- その他南米

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- ASEAN-5

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- エジプト

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Festo SE and Co. KG

- Emerson Electric Co.

- SMC Corporation

- Parker-Hannifin Corporation

- Siemens AG

- Ingersoll Rand Inc.

- Atlas Copco AB

- Bosch Rexroth AG

- Norgren Ltd.(IMI plc)

- Airtac International Group

- CKD Corporation

- Camozzi Automation S.p.A.

- Danfoss A/S

- Honeywell International Inc.

- Eaton Corporation plc

- ROSS Operating Valve Co.

- Bimba Manufacturing LLC(IMI)

- Janatics India Pvt Ltd

- Chicago Pneumatic Tool Co. LLC

- Koki Holdings Co., Ltd.

- Yamaha Motor Co., Ltd.(Robotics)