|

市場調査レポート

商品コード

1851911

ライナーレスラベル:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Linerless Labels - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ライナーレスラベル:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月10日

発行: Mordor Intelligence

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

概要

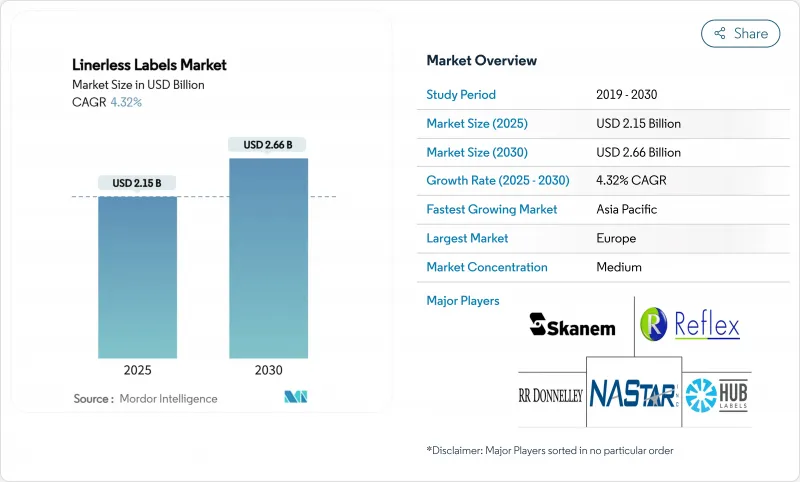

ライナーレスラベルの市場規模は2025年に21億5,000万米ドル、2030年には26億6,000万米ドルに達し、CAGR 4.32%で成長すると予測されています。

この規制は、2030年までにすべての包装をリサイクル可能にすることを義務付け、2040年までに一人当たりの包装廃棄物を15%削減することを目標としています。フレキソ印刷のシェアは引き続き40.32%を占めているが、eコマースが可変長オンデマンド印刷の需要を牽引しているため、インクジェットとサーマル技術に牽引されるデジタルシステムがCAGR7.43%で拡大しています。フィルム基材のシェアは48.23%で、特殊基材とリサイクル基材は、企業の循環型経済目標の中でCAGR 8.11%と最も高いです。水性アクリル系粘着剤のシェアは42.32%で優位を保っており、UV硬化型粘着剤がCAGR 7.84%で急成長し、コールドチェーンの性能ギャップを解決しています。欧州が34.62%のシェアでリードしているが、アジア太平洋は製造規模の拡大とeコマースの拡大を背景にCAGR 8.53%で上昇しています。

世界のライナーレスラベル市場の動向と洞察

持続可能な飲食品包装需要の急増

食品ブランドは、規制遵守と消費者の低負荷パッケージへの期待の両方を満たすためにライナーレスラベルを埋め込んでいます。Avery Dennison社は、2024年のIntelligent Labels部門の既存事業売上高成長率15%を報告し、その増加の大部分は、ライン入り製品と比較して材料使用量を30%削減し、二酸化炭素排出量を49%削減した食品アプリケーションによるものであるとしています。生鮮食品のサプライヤーは、埋立廃棄物を削減し、トレーサビリティを強化するためにライナーレス・ソリューションを指定することが増えており、自動パッケージング・ラインは動的ラベルサイジングを活用して材料使用量を最大40%削減します。これらの要因が組み合わさることで、チルド、冷凍、常温の各製品カテゴリーで市場導入が加速しています。大手の加工業者がサプライヤーへの義務付けを設定し、それが地域のバリューチェーンに連鎖することで、その効果はさらに大きくなります。リサイクル可能な面材と食品用紫外線硬化型接着剤への投資は、調理済み食品セクターでの採用をさらに推進します。

可変長出荷ラベルを必要とするeコマース・ロジスティクス・ブーム

小包の量が急増し、フルフィルメントセンターはラベルの在庫と無駄を最適化する必要に迫られています。東芝の産業用プリンターDL1024は、配送ラベルと荷造り伝票を1つの可変長フォーマットに統合することで、印刷コストを40%削減し、ライナーの無駄をなくします。米国郵政公社の小包ラベルガイド改訂版では、自動スキャンを高速化する合理的なデザインが強調されており、ライナーレス化を間接的にサポートしています。大容量の施設では、1ロールあたりのラベル枚数が50%増加し、ロール交換の回数が減り、スループットが向上したと報告されています。マイクロ・フルフィルメント・ハブでは、ライナーレスによるスペースの節約により、ピッキング能力が向上しています。小売業者の厳しいサステナビリティ・スコアカードは、過剰包装に関連するペナルティを避けるため、サプライヤーをライナーレスシステムに向かわせています。

レガシーラベリングラインの改造コスト

ライナーレスへの切り替えには、1ラインあたり5万~20万米ドルの資本アップグレードが必要となることが多く、小規模のコンバーターにとっては、投資回収期間がおよそ2年に延びるハードルとなります。FoxJetの全電動式ラベラーは現在、圧縮空気の必要性をなくすモジュール式の後付けキットを提供しており、運転コストを削減し、設置を容易にします。それでも、作業員のトレーニングやメンテナンスルーチンの見直しにより、間接的な出費は増えます。多くの生産者は、ハイブリッドワークフローを採用しています。新しいSKUにはライナーレスで対応し、レガシー機器は長期にわたる製品を処理します。ファイナンス・パッケージやサブスクリプション・モデルをバンドルしている機器ベンダーは、先行キャッシュ・プレッシャーを軽減することで、転換を加速することができます。

セグメント分析

2024年のライナーレスラベル市場では、フレキソグラフィーは40.32%のシェアを維持しているが、デジタルセグメントはCAGR 7.43%で拡大しています。eコマースブランドがバリアブルデータとリアルタイムのカスタマイズを要求しているため、小ロット・中ロットのデジタル印刷機のライナーレスラベル市場規模は急速に拡大します。フレキソ印刷の下塗りとインクジェット仕上げを融合させたハイブリッド印刷機は、無駄を削減し、切り替えを高速化します。サーマル・ダイレクト・システムは、ラベルがマテリアルハンドリングの磨耗に耐える必要があるにもかかわらず、コスト効率を維持できるため、ロジスティクスで威力を発揮します。デジタルワークフローは、水や溶剤の使用量も削減し、持続可能性のスコアカードに合致します。インライン仕上げとクラウドに接続されたカラーマネジメントへの投資により、出力の一貫性が向上し、デジタルフォーマットが中ロットで従来のフレキソと真っ向から競合できるようになります。

RFIDインレイ挿入との互換性は、デジタルの役割をさらに高め、スマートラベルのワンパス生産を可能にします。Web-to-ラベルのポータルを活用するコンバーターは、最小注文のハードルなしにパーソナライズされたデザインを必要とする小規模販売業者から新たな収益を獲得しています。基材メーカーがプライマーフリーフィルムをリリースすることで、インクの密着性が向上し、消耗品コストが削減されます。サマリーをまとめると、印刷技術ミックスは急速に変化しており、フレキソはコモディティ化したSKUに適している一方、デジタルはライナーレスラベル市場全体において、動きが速くデータが豊富なアプリケーションに適しています。

PPとPETを中心とするフィルムベースのファイスストックは、耐湿性と保存性の高さにより、ライナーレスラベル市場で48.23%のシェアを占めています。しかし、バイヤーのサーキュラーエコノミー(循環型経済)に対する誓約と、規制によるリサイクル含有量割当によって、特殊素材とリサイクル代替素材がCAGR 8.11%で上回っています。食品とパーソナルケアパッケージをカバーするリサイクルコンテントフィルムのライナーレスラベル市場規模は、2030年まで着実に上昇すると予測されています。UPMラフラタックのカーボン・アクション・ポートフォリオは、ISCC認証原料を使用し、ゆりかごからゲートまでの排出量を削減し、スコープ3の削減を目指すブランドにアピールしています。

紙のフェイスストックは、堆肥化性や触感の良さが耐久性よりも優先されるニッチを守る。薄いPPのオーバーセルと再生クラフトのベースを組み合わせたハイブリッド構造は、バージンプラスチックの含有量を減らしながら強度を最適化します。アルカリ浴で剥離するウォッシュオフフィルムは、PETのクローズドループリサイクルを可能にし、ボトルtoボトルシステムを求める飲料サプライヤーにとって極めて重要です。サプライヤーは、従来のラミネートラベルに匹敵する色と仕上げの幅を広げ、特殊ラベル採用の障壁を一つ取り除いた。バイアックスストレッチラインと解重合リサイクルプラントへの継続的な投資により、原料供給能力は需要の増加に対応できる規模に拡大します。

地域分析

欧州は2024年の売上高の34.62%を占め、規制の早期導入、小売網の緻密さ、コンバーター基盤の確立が強みとなっています。UPM RaflatacやHERMAといった地域大手がウォッシュオフやリサイクル・コンテント・フォーマットを開拓し、プライベートブランドに波及需要を生み出しました。リサイクル可能な包装を指定する政府調達基準は、欧州のリードをさらに強固なものにしています。北米は、eコマースの加速と、包装サプライヤーの廃棄コストを内部化する州全体の拡大生産者責任法案に後押しされ、これに続いています。この地域のコンバーターは、チルド食品や小包のハブに対応するために高速UVラインに投資し、CCLインダストリーズは戦略的買収によって生産能力を拡大しています。

アジア太平洋のCAGRは8.53%と最も速く、中国の製造規模とインドのeコマース普及の速さが牽引しています。同地域のライナーレスラベル市場シェアは、現地のコンバーターがデジタル印刷機を増設し、海外ブランドが調和のとれた持続可能なパッケージングを要求していることから、上昇する見込みです。日本のリンテック株式会社は、耐寒性接着剤の生産能力増強と研究開発に投資し、地域の技術リーダーシップを強化します。ベトナムやインドネシアなどの新興市場は、欧米の小売業者が設定する輸出認証基準を満たすためにライナーレスを採用します。南米では、ブラジルの大手飲料メーカーがPETボトルのリサイクルプロジェクトでウォッシュオフフィルムを試用しており、選択的な成長が見られます。中東・アフリカでは、多国籍FMCG工場がグローバル仕様を導入しているアラブ首長国連邦と南アフリカが導入の中心となっています。

規制の調和、国境を越えたeコマース、生産能力への投資などを総合すると、この地域の需要の持続的な回転が示唆されます。アジア太平洋地域の生産能力に資本が流入するにつれて、原材料のサプライチェーンが順応し、単価がさらに引き下げられ、ライン在庫からの代替が加速します。欧州は依然として規制の旗手であり、その政策革新は世界中でますます反映され、輸出志向のメーカーにとってライナーレス能力が基本要件として定着しつつあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 持続可能な食品・飲料包装需要の急増

- 可変長配送ラベルを必要とする電子商取引物流ブーム

- 欧州と北米における廃棄物削減の規制義務化

- オンデマンド・ライナーレス印刷によるQSR厨房自動化の普及

- RFID対応コネクテッド・パッケージングとマイクロ・フルフィルメントの採用

- 市場抑制要因

- レガシー・ラベリングラインの改修コスト

- 原材料価格の変動(接着剤と剥離コーティング剤)

- コールドチェーン環境における接着剤の蓄積問題

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 印刷技術別

- デジタル(インクジェットおよびサーマル)

- フレキソ印刷

- グラビア

- オフセットおよび凸版印刷

- ファセストック素材別

- 紙

- フィルム(PP、PET、PE)

- 特殊およびリサイクル基材

- 接着剤タイプ別

- 水性アクリル

- ホットメルト

- UV硬化型

- 溶剤ベース

- エンドユーザー業界別

- 食品

- 飲料

- ヘルスケアと医薬品

- 化粧品とパーソナルケア

- 家庭用化学品

- ロジスティクスとEコマース

- その他のエンドユーザー産業

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア、ニュージーランド

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- アラブ首長国連邦

- サウジアラビア

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- エジプト

- その他アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Avery Dennison Corporation

- CCL Industries(Inc. & Innovia Films)

- 3M Company

- Beontag

- UPM Raflatac

- Coveris

- Hub Labels Inc.

- Reflex Labels Ltd

- Skanem AS

- NAStar Inc.

- Optimum Group

- SATO Europe GmbH

- ProPrint Group

- Lexit Group AS

- R.R. Donnelley & Sons Co.

- Gipako UAB

- Lintec Corporation

- HERMA GmbH

- Zebra Technologies

- Multi-Color Corporation