|

市場調査レポート

商品コード

1689739

東南アジアの電池:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Southeast Asia Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 東南アジアの電池:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

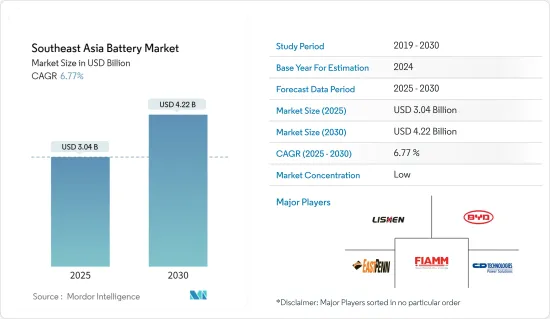

東南アジアの電池の市場規模は2025年に30億4,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは6.77%で、2030年には42億2,000万米ドルに達すると予測されています。

2020年にはCOVID-19が市場にマイナスの影響を与えたもの、流行前のレベルに達しています。

主なハイライト

- 中期的には、自動車セクターの需要拡大、リチウムイオン電池価格の下落、東南アジアをデータセンターのハブにする計画などの要因が、予測期間中の市場を牽引すると見込まれます。

- 自動車、データセンター、通信の各分野で電池の需要が伸びているにもかかわらず、ほとんどの国が他のエネルギー貯蔵手段に依存しているため、電池エネルギー貯蔵分野は伸び悩むと予想されます。このことは、予測期間中、エネルギー貯蔵分野におけるバッテリー市場の成長を抑制する可能性が高いです。

- さらに、再生可能エネルギーを各国の送電網に統合する計画は、予測期間中、リチウムイオン電池メーカーやサプライヤーに大きなビジネスチャンスをもたらすと予想されます。

- タイは、自動車、データセンター、その他のエンドユーザー部門からの需要増加により、予測期間中に市場を独占すると予想されます。

東南アジアの電池市場動向

自動車分野が市場を独占すると予測

- 以前は内燃機関車(ICE)だけが使用されていました。内燃機関車には鉛蓄電池が使用されており、大幅な代替品がないまま継続する可能性があります。

- しかし現在では、環境に対する懸念の高まりから、技術は電気自動車にシフトしています。EVでは、エネルギー密度が高く、自己放電が少なく、メンテナンスがほとんど不要なリチウムイオン電池が主に使用されています。

- リチウムイオン電池システムは、プラグイン・ハイブリッド車や電気自動車を推進します。高エネルギー密度、急速充電能力、高放電電力により、リチウムイオン・バッテリーは、自動車の走行距離と充電時間に関するOEM要件を満たす唯一の利用可能な技術です。鉛ベースのトラクション・バッテリーは、比エネルギーが低く重量が大きいため、フルハイブリッド電気自動車や電気自動車に使用するには競合しないです。

- さらに、リチウムイオン電池の価格が急激に下落したため、その価値は2013年の668米ドル/kWhから2021年には123米ドル/kWhへと81.5%減少しました。この動向は今後も続くとみられ、この地域の幅広い経済層がEVを手ごろな価格で購入できるようになります。

- ハイブリッド車では、いくつかのバッテリー技術がさまざまな組み合わせでこれらの機能を提供できるが、ニッケル水素とリチウムイオン・バッテリーは、高速充電能力、良好な放電性能、寿命の耐久性により、高電圧で好まれます。

- いくつかの地域政府が排出量削減計画を策定しており、予測期間中に電気自動車(EV)の地域シェアが高まると予想されます。

- したがって、上記の要因により、予測期間中、自動車セクターが東南アジアの電池市場を独占すると予想されます。

タイが市場を独占する見込み

- タイが市場の大半のシェアを占めています。自動車、データセンター、通信セクターからの需要増加により、この動向は予測期間中も続くと予想されます。

- タイは自動車セクターにとって大きな投資ポテンシャルを提供しています。同国は、東南アジア諸国連合の中でも有数の自動車生産拠点です。同国は、自動車部品の組み立て業者から50年以上かけて、自動車製造と輸出のトップ・ハブへと発展しました。

- さらに、同国はEVセグメント、特にプラグイン・ハイブリッド電気自動車(PHEV)とハイブリッド電気自動車(HEV)で高い成長が見込まれています。2022年9月、BYD社はバンコクのラヨーンに海外初の電気乗用車工場を建設する計画を発表しました。

- 国家電気自動車政策委員会(NEVPC)のロードマップでは、タイは2025年までに10万台から30万台、最終的には2026年までに40万台から75万台を追加すると予想されています。

- さらに2022年4月、タイ政府は電気自動車(EV)の動力源となる亜鉛イオン電池の製造に資金を提供することに合意しました。タイは、天然資源である亜鉛を利用する価値のあるEV用電池工場を現地開発します。

- さらに、タイはICTセクターの成長において大きな進歩を遂げ、テクノロジーの世界では二の次の存在であったのが、急速に地域のリーダーの1つに躍り出た。過去10年間で、タイのデジタル・シェアはますます加速しており、労働力教育とスキル構築で大きな成果を上げています。

- 政府はタイ4.0プログラムのもと、ビジネス・モジュールを計画しました。このプログラムは、クラウド・コンピューティング、インタラクティブ・メディア、ビッグデータ、モノのインターネットなどの新技術の利用を促進するものです。したがって、同国ではデータセンターの需要が高く、予測期間中にデータセンターの電池需要が増加すると予想されます。

- したがって、上記の要因により、タイは予測期間中に東南アジアのバッテリー市場を独占すると予想されます。

東南アジアの電池産業の概要

東南アジアの電池市場は、Tianjin Lishen Battery Joint-Stock、FIAMM Energy Technology SpA、BYD、C&D Technologies Inc.、East Penn Manufacturing Co.Inc.などの主要企業が存在するため、部分的に断片化しています(順不同)。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2028年までの市場規模および需要予測

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 抑制要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 電池タイプ別

- 鉛蓄電池

- リチウムイオン電池

- その他の電池タイプ

- エンドユーザー別

- 自動車

- データセンター

- 通信

- エネルギー貯蔵

- その他エンドユーザー

- 地域別

- インドネシア

- マレーシア

- フィリピン

- シンガポール

- タイ

- ベトナム

- ミャンマー

- その他の東南アジア地域

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- BYD Co. Ltd.

- C&D Technologies Inc.

- East Penn Manufacturing Co. Inc.

- Tianjin Lishen Battery Joint-Stock Co. Ltd.

- Exide Industries Ltd.

- FIAMM Energy Technology SpA

- GS Yuasa Corporation

- LG Chem Ltd.

- Panasonic Corporation

- Saft Groupe SA

- Samsung SDI Co. Ltd.

- Clarios

- Tesla Inc.

- Leoch International Technology Limited

第7章 市場機会と今後の動向

The Southeast Asia Battery Market size is estimated at USD 3.04 billion in 2025, and is expected to reach USD 4.22 billion by 2030, at a CAGR of 6.77% during the forecast period (2025-2030).

Though COVID-19 negatively impacted the market in 2020, it has reached pre-pandemic levels.

Key Highlights

- Over the medium term, factors such as growing demand from the automotive sector, declining lithium-ion battery prices, and plans to make Southeast Asia a data center hub are expected to drive the market during the forecast period.

- Despite the growing demand for batteries in the automotive, data centers, and telecommunications sectors, the battery energy storage segment is expected to witness stagnant growth, as most countries depend on other energy storage alternatives. This, in turn, is likely to restrain the growth of the battery market in the energy storage segment during the forecast period.

- Moreover, plans to integrate renewable energy with the national grids in respective countries are expected to create significant opportunities for lithium-ion battery manufacturers and suppliers during the forecast period.

- Thailand is expected to dominate the market during the forecast period due to the increasing demand from the automotive, data center, and other end-user sectors.

Southeast Asia Battery Market Trends

Automotive Sector is Expected to Dominate the Market

- Vehicles with internal combustion engines (ICE) were the only types used earlier. ICE vehicles have been using lead-acid batteries, which may continue with no significant replacement available.

- However, nowadays, technology has been shifting toward electric vehicles due to rising concerns about the environment. In EVs, mostly lithium-ion batteries are used, as they provide high energy density, have low self-discharge, and require little maintenance.

- Lithium-ion battery systems propel plug-in hybrid and electric vehicles. Due to their high energy density, fast recharge capability, and high discharge power, lithium-ion batteries are the only available technology that meets the OEM requirements for vehicles' driving range and charging time. Lead-based traction batteries are not competitive for use in full-hybrid electric cars or electric vehicles because of their lower specific energy and higher weight.

- Moreover, the exponential decline in lithium-ion batteries' prices reduced their value by 81.5% from USD 668/kWh in 2013 to USD 123/kWh in 2021. The trend is likely to continue in the future, making EVs affordable to a broader range of economic groups in the region.

- For hybrid vehicles, several battery technologies can provide these functions in different combinations, with nickel-metal hydride and lithium-ion batteries preferred at higher voltages due to their fast recharge capability, good discharge performance, and lifetime endurance.

- Several regional governments developed plans to reduce emissions, which are expected to increase the region's share of electric vehicles (EV) during the forecast period.

- Therefore, owing to the abovementioned factors, the automotive sector is expected to dominate the Southeast Asian battery market during the forecast period.

Thailand is Expected to Dominate the Market

- Thailand accounts for the majority share of the market. This trend is expected to continue during the forecast period, owing to the increasing demand from the automotive, data center, and telecom sectors.

- Thailand provides great investment potential for the automotive sector. The country has a leading automotive production base in the Association of Southeast Asian Nations. The country has developed from an assembler of auto components into a top automotive manufacturing and export hub in over 50 years.

- Moreover, the country is expected to witness high growth in the EV segment, particularly in plug-in hybrid electric vehicles (PHEVs) and hybrid electric vehicles (HEVs). In September 2022, BYD Co. announced plans to build its first overseas electric passenger car plant in Rayong, Bangkok.

- Under the National Electric Vehicle Policy Committee (NEVPC) roadmap, Thailand is expected to add between 100,000 and 300,000 vehicles by 2025 and finally between 400,000 and 750,000 vehicles by 2026.

- Further, in April 2022, the Thai government agreed to fund the manufacturing of zinc-ion batteries to power electric vehicles (EVs). Thailand will develop a local EV battery plant worth using zinc as a natural resource.

- Furthermore, Thailand has made great progress in growing its ICT sector, moving quickly from being a secondary player in the world of technology to one of the regional leaders. Over the past decade, the digital share in Thailand has been closing at an ever-increasing speed, with the country making significant gains in labor force education and skills building.

- The government planned its business module under Thailand's 4.0 Program. This program helps increase the use of new technologies such as cloud computing, interactive media, big data, and the internet of things. Hence, the country is expected to have a high demand for data centers, which is expected to increase the demand for batteries in its data centers during the forecast period.

- Therefore, owing to the abovementioned factors, Thailand is expected to dominate the Southeast Asian battery market during the forecast period.

Southeast Asia Battery Industry Overview

The Southeast Asian battery market is partially fragmented due to the presence of key players, including (in no particular order) Tianjin Lishen Battery Joint-Stock Co. Ltd., FIAMM Energy Technology SpA, BYD Co. Ltd., C&D Technologies Inc., and East Penn Manufacturing Co. Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Battery Type

- 5.1.1 Lead-acid Battery

- 5.1.2 Lithium-ion Battery

- 5.1.3 Other Battery Types

- 5.2 By End-User

- 5.2.1 Automotive

- 5.2.2 Data Centers

- 5.2.3 Telecommunication

- 5.2.4 Energy Storage

- 5.2.5 Other End-Users

- 5.3 By Geography

- 5.3.1 Indonesia

- 5.3.2 Malaysia

- 5.3.3 Philippines

- 5.3.4 Singapore

- 5.3.5 Thailand

- 5.3.6 Vietnam

- 5.3.7 Myanmar

- 5.3.8 Rest of Southeast Asia

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 BYD Co. Ltd.

- 6.3.2 C&D Technologies Inc.

- 6.3.3 East Penn Manufacturing Co. Inc.

- 6.3.4 Tianjin Lishen Battery Joint-Stock Co. Ltd.

- 6.3.5 Exide Industries Ltd.

- 6.3.6 FIAMM Energy Technology SpA

- 6.3.7 GS Yuasa Corporation

- 6.3.8 LG Chem Ltd.

- 6.3.9 Panasonic Corporation

- 6.3.10 Saft Groupe SA

- 6.3.11 Samsung SDI Co. Ltd.

- 6.3.12 Clarios

- 6.3.13 Tesla Inc.

- 6.3.14 Leoch International Technology Limited