|

市場調査レポート

商品コード

1689696

インドの製造受託機関(CMO):市場シェア分析、産業動向、成長予測(2024年~2029年)India Contract Manufacturing Organization (CMO) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インドの製造受託機関(CMO):市場シェア分析、産業動向、成長予測(2024年~2029年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

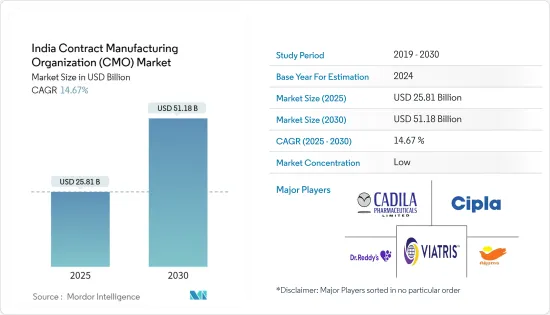

インドのCMO市場規模は2024年に225億1,000万米ドルと推定され、市場推定・予測期間(2024~2029年)のCAGRは14.67%で、2029年には446億3,000万米ドルに達すると予測されます。

製造受託機関(CMO)は、契約に基づいて医薬品開発・製造サービスを製薬産業に記載しています。特にがん研究において注射薬の需要が高まっていることから、製造受託市場は拡大するとみられます。注射剤は他の製剤よりも高い収益が期待でき、優れた治療効率を示します。

主要ハイライト

- CMOは厳しい規制を遵守し、熟練した労働力、最先端の製造施設、費用対効果の高いサービスポートフォリオを誇る。製薬産業では競争が激化しているため、製品の早期上市が急務であり、市場で先駆的な地位を築くことが求められています。その結果、製品上市の早期化、価格圧力の高まり、CMOが提供する利点(タイムラインの短縮、競合コストで高品質な製品)などが、主要市場促進要因となっています。

- インドの製薬産業は、ジェネリック医薬品、OTC医薬品、ワクチン、原薬、研究・製造受託、バイオシミラー、生物製剤などの重要なセグメントを包含しています。特筆すべきは、インドが安価なワクチンの主要供給国であることです。

- 世界のワクチン生産量の60%を占めるインドは、世界保健機関(WHO)のジフテリア・百日咳・破傷風(DPT)ワクチンとカルメット・ゲリン菌(BCG)ワクチンの需要の40~70%を満たし、麻疹ワクチンのシェアも90%と圧倒的です。このような広大な生産能力を持つインドは、調査対象市場の潜在的促進要因として位置づけられています。

- 2023年、インド政府は中央医薬品標準管理機構(Central Drugs Standard Control Organization)により、様々な遺伝性疾患を対象とする21の新薬を認可しました。この動きは、地元企業が新たな施設を設立し、急増する医薬品需要に対応する道を開くものです。さらに、インドは医薬品輸出国として極めて重要な役割を果たしており、米国は特にインドからの輸入に依存し、インドに工場を設立しています。

- しかし、課題も山積しています。政府の規制が厳しく、特定地域における低分子医薬品や生物製剤の承認が減少しているため、市場の成長が阻害される可能性があります。さらに、小規模のCDMOは、先進的技術がないため、エラーリスクの高まりに直面します。劣悪な品質や価格設定の課題に対する懸念が、市場拡大の取り組みをさらに複雑にしています。

インドのCMO市場の動向

大手製薬企業によるアウトソーシング量の増加

- インド製薬工業協会(IDMA)は、新興国市場におけるコスト上昇と規制強化の圧力により、世界製薬企業は研究開発・製造の社内能力を削減せざるを得なくなっていると指摘しました。その代わりに、これらの企業は、受託製造、研究サービス、発展途上国での研究や臨床検査のアウトソーシングにますます目を向けるようになっています。さらに、欧州の製造施設の老朽化により、企業は研究・製造業務をインドにシフトしています。

- 生物製剤原薬(API)の開発は技術的に難しく、資本集約的であるため、その製造コストは従来の医薬品よりも大幅に高くなります。注目すべきは、生物製剤のアウトソーシングによる収益の約75%がAPI生産に由来することです。生物製剤の高い価値と利幅を認識し、医薬品製造受託機関(CMO)は能力の拡大に多額の投資を行っています。しかし、製薬会社は製造への直接投資よりも供給の確保を優先しています。

- 製薬セクタにおけるアウトソーシングの増加動向は、製造受託がバリューチェーンの重要なコンポーネントとなることで、成功するパートナーシップへの道を開いています。同市場は、製品の国内アウトソーシングを目指すインドの大手製薬会社の増加により、大幅な成長を遂げています。

- インド連邦予算によると、2020年の製薬産業の予算配分は33億4,000万インドルピー(約4,000万米ドル)でした。この配分は、2024年までに409億インドルピー(約4億9,000万米ドル)に急増すると予測されています。世界市場が拡大しているのは、インドのような新興国が持つ費用対効果の高い資源によるところが大きいです。

- 米国FDA認可の製造施設が100以上あり、その数は増加の一途をたどっています。Zydus CadilaやLUPINのような大手製薬企業の存在も、インドの製薬産業をより強固なものにしています。

原薬(API)・中間体部門が成長を遂げる

- 原薬の製造はここ数年一貫して増加しています。今後も特許切れが予想され、世界のジェネリック医薬品生産能力の大幅な増加が見込まれるため、APIは着実に増加し続けると考えられます。産業の大半の企業は、生物製剤の創製と原薬生産の増強に重点を置いています。

- さらに、医療セグメントにおけるインド政府によるイニシアチブの増加、生物製剤の技術革新、がんや加齢関連疾患の増加は、原薬製造産業の拡大を後押しする重要な理由のほんの一部に過ぎないです。また、医薬品の研究開発の拡大、慢性疾患率の上昇、ジェネリック医薬品の関連性の高まり、バイオ医薬品の使用量の増加なども、拡大の背景にある可能性があります。

- インドの製薬産業は、製剤の基礎原料となる医薬品有効成分である様々な原薬を生産しています。製剤は産業の生産高の残り5分の4を占め、原薬で約5分の1を占めています。また、インドは500以上の原薬を製造し、60の治療カテゴリーで6万のジェネリック医薬品を製造していることから、医薬品原薬(API)の専門知識も有しています。

- インドはまた、製薬企業への投資を奨励し、完全所有または合弁の施設を設立することで、国内CMO市場の拡大から利益を得ています。2023年4月時点のインドからの医薬品輸出の分布に関するInvest Indiaのデータによると、製剤と生物製剤が73.31%でトップ、次いで原薬、中間体、その他の成分となっています。中国とインドのコスト構造も乖離しており、中国はより高価なアウトソーシング先となっています。また、米国や欧州の企業はサプライチェーンの多様化を目指しており、インドに利益をもたらしています。

- ジェネリック医薬品の生産と輸出において重要な役割を担うインドは、中国への依存に警戒感を強めています。国内生産を強化するため、インド政府はいくつかの施策を開始しました。インドが中国の輸入品に大きく依存していることを痛感した政府は、国内の原薬生産を強化するため、4億米ドルを拠出することを発表しました。この動きは、Lasa Supergenerics、Shilpa Medicare、Gujarat Themis、Solara Active Pharmaなど主要APIメーカーの株価を大きく上昇させました。

インドのCMO産業概要

製造受託機関(CMO)は製薬会社やバイオテクノロジー企業向けに製造サービスを提供しています。CMOはこれらの企業に代わって、医薬品や治療を製造します。CMOは、開発された医薬品の配合をもとに、クライアントの需要に応じて生産規模を調整します。CMOは、安全性、一貫性、規制基準の遵守を優先して製造プロセスを行っています。

インドの医薬品製造受託機関(CMO)市場はセグメント化されており、上位ベンダーが大きな市場シェアを占めています。こうした大手企業以外にも、市場シェアを拡大するために技術革新や提携に投資している企業が複数存在します。そのため、競争企業間の敵対関係は激しくなっています。主要参入企業は、Dr Reddy's Laboratories、Cadila Pharmaceuticals Limited、Cipla Ltd.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- エコシステム分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場力学

- 市場促進要因

- 比較的低コストでの熟練労働者の入手可能性

- 大手製薬企業によるアウトソーシング量の持続的増加

- アジア太平洋の大規模市場へのアクセスという地理的優位性

- 市場抑制要因

- 政府の厳しい規制の存在と、国内の特定地域における多数の低分子化合物と生物製剤の承認の減少

- 世界の医薬品CMO産業概要とインド市場で確認された主要手がかり

- アジア太平洋の主要市場概要

- マハラシュトラ州とテランガナ州におけるCMO施設の主要ホットスポット

- インドのCMO産業における最近のプライベートエクイティ投資

第6章 市場セグメンテーション

- サービスタイプ別

- 原薬・中間体

- 完成用量

- 固体

- 液体

- 半固形剤と注射剤

第7章 インドのCMO産業への戦略的提言

- インドは、特に注射剤セグメントでCMO施設の設立を計画する新規ベンダーにとって、主に国内需要とジェネリック医薬品の成長により、引き続き高い提案力を維持

- コスト優位性と人材プールへのアクセス

- 薬事承認パイプラインとベースケースシナリオ

- インドにおける潜在的M&A対象の分析

第8章 競合情勢

- 企業プロファイル

- Dr. Reddy's Laboratories

- Cadila Healthcare Limited

- MSN Laboratories Pvt Ltd

- Viatris Inc(Mylan Laboratories Ltd)

- Medipaams India Pvt Ltd

- Cipla Ltd.

- Eisai Pharmaceuticals India Pvt Ltd

- Delwis Healthcare Pvt Ltd

- Maxheal Pharmaceuticals India Ltd

- Rhydburg Pharmaceuticals Ltd

- Theon Pharmaceuticals Limited

- BDR Pharmaceuticals International

- Akums Drugs and Pharmaceuticals Limited

- Wockhardt Limited

- Unichem Laboratories Ltd

- Ciron Drugs & Pharmaceuticals Pvt Ltd

第9章 市場の将来展望

The India CMO Market size is estimated at USD 22.51 billion in 2024, and is expected to reach USD 44.63 billion by 2029, at a CAGR of 14.67% during the forecast period (2024-2029).

Contract manufacturing organizations (CMOs) provide drug development and manufacturing services to the pharmaceutical industry under contractual agreements. With a rising demand for injectable drugs, especially in cancer research, the contract manufacturing market is set to expand. Injectable drugs promise higher returns than other formulations and demonstrate superior therapeutic efficiency.

Key Highlights

- CMOs adhere to stringent regulations and boast a skilled workforce, cutting-edge manufacturing facilities, and a cost-effective service portfolio. Heightened competition in the pharmaceutical sector underscores the urgency of swiftly launching products, aiming for a pioneering market position. Consequently, the push for earlier product launches, mounting pricing pressures, and the advantages offered by CMOs-like reduced timelines and high-quality products at competitive costs-serve as primary market drivers.

- The Indian pharmaceutical landscape encompasses significant segments, including generic drugs, OTC medicines, vaccines, bulk drugs, contract research and manufacturing, biosimilars, and biologics. Notably, India stands out as a leading supplier of affordable vaccines.

- Boasting 60% of the global vaccine production, India meets 40-70% of the World Health Organization's (WHO) demand for diphtheria, pertussis, and tetanus (DPT) and Bacillus Calmette-Guerin (BCG) vaccines, alongside a dominant 90% share for the measles vaccine. Such vast production capabilities position India as a potential growth driver for the studied market.

- In 2023, the Indian government, as per the Central Drugs Standard Control Organization, greenlit 21 new drugs targeting various genetic diseases. This move paves the way for local players to establish new facilities, addressing the surging medicine demand. Additionally, India plays a pivotal role as a pharmaceutical exporter, with the U.S. notably relying on Indian imports and establishing plants there.

- However, challenges loom on the horizon. Stringent government regulations and declining approvals for small molecules and biologics in specific regions could stifle market growth. Moreover, smaller CDMOs face heightened error risks due to a lack of advanced technology. Concerns over subpar quality and pricing challenges further complicate market expansion efforts.

India CMO Market Trends

Rise in Outsourcing Volume by Big Pharma Companies

- The Indian Drug Manufacturers Association (IDMA) highlighted that rising costs and regulatory pressures in developed markets are compelling global pharmaceutical companies to reduce their internal capacities in research, development, and manufacturing. Instead, these companies are increasingly turning to contract manufacturing, research services, and outsourcing of research and clinical trials in developing nations. Additionally, ageing manufacturing facilities in Europe have led companies to shift their research and manufacturing operations to India.

- Developing a biological Active Pharmaceutical Ingredient (API) is a technically challenging and capital-intensive, making its production cost significantly higher than conventional drugs. Notably, around 75% of the revenue from outsourcing biologics is derived from API production. Recognizing the high value and margins associated with biologic drugs, Contract Manufacturing Organizations (CMOs) heavily invest in expanding their capacities. However, pharmaceutical companies prioritize supply security over direct investments in manufacturing.

- The trend of rising outsourcing in the pharmaceutical sector is paving the way for successful partnerships, with contract manufacturing becoming a vital component of their value chains. The market is witnessing substantial growth, driven by an increasing number of large pharmaceutical companies in India seeking to outsource products domestically.

- As per the Union Budget of India, the pharmaceutical industry's budget allocation in 2020 was INR 3.34 billion (approximately USD 0.04 billion). This allocation was projected to surge to INR 40.9 billion (around USD 0.49 billion) by 2024. The global market is expanding, largely due to the cost-effective resources available in developing nations like India.

- India stands out as a favored destination for CMOs, boasting over 100 US FDA-approved manufacturing facilities, a number that's on the rise. The robust presence of major players like Zydus Cadila and LUPIN further strengthens the country's pharmaceutical landscape.

The Active Pharmaceutical Ingredient (API) and Intermediates Segment to Witness Growth

- The manufacturing of APIs has consistently increased over the past few years. This will continue to rise steadily, with further patent expiries expected in the future and a significant increase in global generic production capacities. Most businesses in the industry emphasize creating biological APIs and boosting API production.

- Furthermore, increased initiatives by the Indian government in the healthcare field, biologics innovation, and an increase in cancer and age-related disorders are just a few of the vital reasons propelling the expansion of the API manufacturing industry. The expansion could also be due to expanding R&D on medication, rising chronic illness rates, growing generic relevance, and rising biopharmaceutical usage.

- The Indian pharmaceutical industry produces a variety of bulk pharmaceuticals, which are active pharmaceutical ingredients that serve as the basic raw materials for formulations. Formulations comprise the remaining four-fifths of the industry's output, with bulk pharmaceuticals making up about one-fifth. The nation also possesses expertise in active pharmaceutical ingredients (APIs), as it is the manufacturer of more than 500 APIs and the source of 60,000 generic brands in 60 therapeutic categories.

- India also benefits from expanding the domestic CMO market by encouraging investments in pharmaceutical businesses to establish wholly-owned or joint venture facilities. According to the data by Invest India on the distribution of pharmaceutical exports from India as of April 2023, formulations and biologicals took the top position with 73.31%, followed by bulk drugs, intermediates, and other components. The cost structure in China and India has also diverged as China has become a more expensive outsourcing destination. Also, companies from the United States and Europe aim to diversify their supply chains, benefiting India.

- India, a significant player in the production and export of generic medications, has grown wary of its reliance on China. To bolster domestic production, the Indian government has initiated several measures. Responding to the stark realization of India's heavy dependence on Chinese imports, the government unveiled a substantial USD 400 million grant to bolster the country's API production. This move triggered a significant surge in the stock prices of key API players, including Lasa Supergenerics, Shilpa Medicare, Gujarat Themis, and Solara Active Pharma.

India CMO Industry Overview

Contract manufacturing organizations (CMOs) offer production services tailored for pharmaceutical and biotechnology firms. Acting on behalf of these entities, CMOs produce drugs, medicines, and therapies. They take a developed drug formula and scale production based on the client's demand. CMOs prioritize safety, consistency, and adherence to regulatory standards in their production processes.

The Indian contract manufacturing organization (CMO) market is fragmented, with the top vendors accounting for a significant market share. Apart from these major players, several players in the market are investing in innovations and partnerships to gain an increased market share. Therefore, the intensity of competitive rivalry is high. The key players are Dr Reddy's Laboratories, Cadila Pharmaceuticals Limited, and Cipla Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Ecosystem Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Availability of Skilled Labor at Relatively Lower Cost

- 5.1.2 Sustained Increase in Outsourcing Volumes by Big Pharma Companies

- 5.1.3 Geographical Advantage in the Form of Access to Large Markets in the APAC Region

- 5.2 Market Restraint

- 5.2.1 The Existence of Stringent Government Restrictions and a Decrease in the Approval of Numerous Small Molecules and Biologics in Specific Regions of the Nation

- 5.3 Overview of the Global Pharmaceutical CMO Industry and Major Cues Identified in the Indian Market

- 5.4 Overview of Major Markets in Asia-Pacific

- 5.5 Major Hotspots for CMO Facilities in Maharashtra and Telangana

- 5.6 Recent Private Equity Investments in the CMO Industry in India

6 MARKET SEGMENTATION

- 6.1 By Service Type

- 6.1.1 API and Intermediates

- 6.1.2 Finished Dose

- 6.1.2.1 Solids

- 6.1.2.2 Liquids

- 6.1.2.3 Semi-solids and Injectables

7 STRATEGIC RECOMMENDATIONS ON INDIA CMO INDUSTRY

- 7.1 India Remains a High Proposition for New Vendors Planning to Set Up Their CMO Facilities, Specifically in the Injectables Domain, Mainly Due to Growth in Domestic Demand and Generic Drugs

- 7.2 Cost Advantages and Access to Talent Pool

- 7.3 Regulatory Approval Pipeline and Base Case Scenarios

- 7.4 Analysis of Potential M&A Targets in India

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Dr. Reddy's Laboratories

- 8.1.2 Cadila Healthcare Limited

- 8.1.3 MSN Laboratories Pvt Ltd

- 8.1.4 Viatris Inc (Mylan Laboratories Ltd)

- 8.1.5 Medipaams India Pvt Ltd

- 8.1.6 Cipla Ltd.

- 8.1.7 Eisai Pharmaceuticals India Pvt Ltd

- 8.1.8 Delwis Healthcare Pvt Ltd

- 8.1.9 Maxheal Pharmaceuticals India Ltd

- 8.1.10 Rhydburg Pharmaceuticals Ltd

- 8.1.11 Theon Pharmaceuticals Limited

- 8.1.12 BDR Pharmaceuticals International

- 8.1.13 Akums Drugs and Pharmaceuticals Limited

- 8.1.14 Wockhardt Limited

- 8.1.15 Unichem Laboratories Ltd

- 8.1.16 Ciron Drugs & Pharmaceuticals Pvt Ltd