|

市場調査レポート

商品コード

1851142

IoTプロフェッショナルサービス:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)IoT Professional Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| IoTプロフェッショナルサービス:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月17日

発行: Mordor Intelligence

ページ情報: 英文 126 Pages

納期: 2~3営業日

|

概要

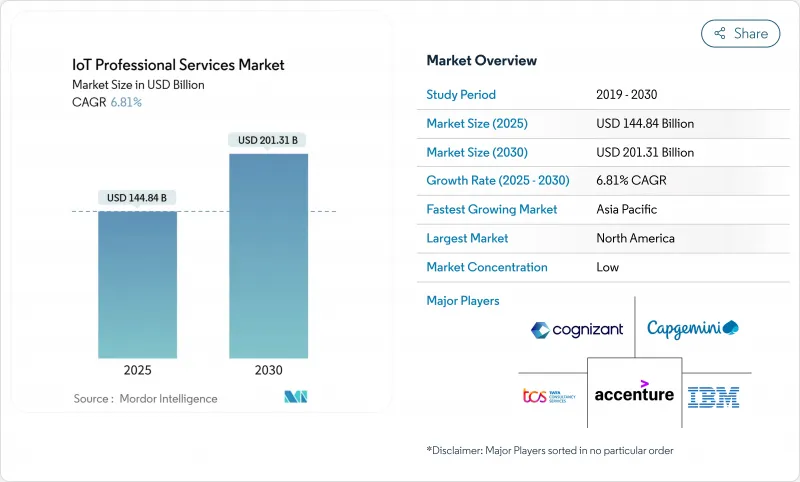

IoTプロフェッショナルサービス市場は、2025年に1,448億4,000万米ドルを創出し、2030年には2,013億1,000万米ドルに達すると予測され、CAGRは6.81%で進展します。

コネクテッドデバイスのエコシステムの拡大、5Gの展開、エッジコンピューティングへの投資により、企業は実験から本格的な展開へと移行しており、専門的なコンサルティング、システム統合、マネージドサービスの専門知識が必要となっています。成果ベースの価格設定、特定分野に特化したソリューション、インダストリー4.0をめぐる規制の義務化は、サプライヤーのパッケージングと価値の提供方法を再構築しています。デバイスの台数とデータ主導のビジネスモデルが融合する場所での需要は最も強いが、サイバーリスクの高まりと人材不足が当面の成長期待を弱めています。全体として、IoTプロフェッショナルサービス市場は、断片的なプロジェクト業務から、テクノロジー・パフォーマンスをビジネス成果に結びつける反復的なプラットフォーム対応業務へと移行しつつあります。

世界のIoTプロフェッショナルサービス市場の動向と洞察

コネクテッドデバイスの普及とセンサーコストの低下

世界のコネクテッドデバイスの台数は188億台に増加し、多様なハードウェア、ファームウェア、通信プロトコルを管理する企業のキャパシティが拡大しています。センサーの低価格化により、大規模な展開が経済的に実行可能になっていますが、デバイスの異種性がライフサイクル管理の複雑性を増大させています。そのため、プロフェッショナル・サービス・パートナーは、マルチベンダー・フリートに対応するプロビジョニング、コンフィギュレーション、モニタリングのフレームワークを設計するよう求められています。軽量M2M、ゼロタッチオンボーディング、セキュアエレメント認証は、ベストプラクティスの青写真として支持を集めています。エッジコンピューティングへの投資は、2028年までに総額3,780億米ドルに達すると予測されており、オンプレミス処理とクラウド分析のバランスをとる統合サービスへの需要がさらに高まっています。

企業のデジタル変革ロードマップ

取締役会は、IoTデータを戦略的資産として扱い、コネクテッドデバイス・プロジェクトをより広範なデジタルコア・プログラムに組み込む傾向が強まっています。IBMは、デジタル・トランスフォーメーションに関連するコンサルティング収益49億6,000万米ドルを報告し、孤立したパイロットから企業全体の近代化へのシフトを強調しています。サービス・プロバイダーは現在、測定可能なROIを提供するセンサー・アーキテクチャとアナリティクス・パイプラインに業務KPIをマッピングする能力で評価されています。バイヤーがアップタイム、コスト削減、収益アップの保証を要求するにつれ、成果ベースの価格設定が支持されるようになっています。デジタル・コアの成熟に伴い、デバイス、ネットワーク、アプリケーションのパフォーマンスを継続的に最適化するマネージド・サービス・ラップへの需要が高まっています。

データプライバシーとサイバーセキュリティへの懸念

Ordr社は、ヘルスケアIoT環境の82%が少なくとも1つの深刻な脆弱性を抱えていることを発見し、ランサムウェア、安全性リスク、規制上の罰金に対する取締役会レベルの不安を煽っています。そのため企業は、セキュアブートチップから暗号化されたデータパイプライン、マイクロセグメント化されたネットワークに至るまで、多層的な防御を必要としています。必要なスキルは、組み込みセキュリティ、OTプロトコル、クラウドIAMにまたがるが、ほとんどのITチームは人員不足のままです。SOC-as-a-Service、レッドチーム・テスト、ゼロトラスト・リファレンス・アーキテクチャに投資するサービス・プロバイダーは、セキュリティの不安を複数年のリテイナー契約に変えるのに最も適した立場にあります。

セグメント分析

IoTコンサルティングは、ベンダーニュートラルな戦略、ROIモデリング、ビジネスケースの検証に対する持続的な需要を反映し、2024年の売上シェアは32.5%を維持した。しかし、複雑なミドルウェア、データレイク、アナリティクスのオーケストレーションを伴うロードマップを企業が本番展開に転換するにつれて、システム設計と統合はCAGR 7.2%で拡大しています。プロバイダーは、ドメインアクセラレーター、リファレンスアーキテクチャ、工場での稼働時間やエネルギー効率の向上に料金をリンクさせる成果ベースの契約によって差別化を図っています。設計と統合のIoTプロフェッショナルサービス市場規模は、5Gとエッジのプロジェクトがパイロットからスケールアップするにつれて急拡大すると予測されます。

また、デバイス監視、予知保全、リモート更新オーケストレーションを組み合わせたマネージド・サービス・ラップにも勢いがあります。サプライヤーは、プラットフォームのサブスクリプションをSLAに裏付けされたオペレーションセンターとバンドルすることで、年金収入を確保し、クライアントのロックインを深めています。統合の複雑さが増すにつれて、ファームウェアのCI/CD、デジタルツインシミュレーション、AI主導のテスト自動化といったツールへの投資が、市場競争力を維持するための重要な課題となっています。

大企業は、多様なポートフォリオ、グローバルサプライチェーン、大規模な近代化予算により、2024年の支出の63.7%を生み出しました。しかし、中小企業はCAGR 7.5%で最も急成長しているバイヤーグループであり、資本支出を削減し、導入期間を短縮する従量課金のクラウドプラットフォームによって実現されています。中小企業にとって、サービス・パートナーは、パッケージ化されたスターター・キット、モジュール化された価格設定、コストを短期的なキャッシュフローに合わせる融資ブリッジを提供する必要があります。ガバナンス・テンプレート、セキュリティ・ベースライン、ROIダッシュボードを、リソースに制約のあるチーム向けにカスタマイズするプロバイダーは、IoTプロフェッショナルサービス市場の拡大するサブセグメントにおいて決定的な優位性を獲得します。

大口顧客では、アドバイザリー、インテグレーション、マネージド・ラン・オペレーションにまたがるマルチタワー契約がボリューム・スケールとなっています。プロジェクトは、ハイブリッド・デリバリー・センターを通じて調整される段階的なグローバル展開を特徴とすることが多いです。これとは対照的に、中小企業向け案件では、迅速なTime to Value、ERPやCRMとの事前設定済み統合、コールドチェーンモニタリングやエネルギーサブメータリングなどの垂直テンプレートが重視されます。この二極化により、サプライヤーは、フォーチュン500のクライアントのために深さを保ちつつ、IoTプロフェッショナルサービス市場全体における高速の中小企業案件のためにデリバリーを工業化するという、二重の市場参入運動を行うことを余儀なくされます。

IoTプロフェッショナルサービス市場は、サービスタイプ別(IoTコンサルティング、IoTインフラサービス、その他)、組織規模別(中小企業、大企業)、展開形態別(クラウドベース、オンプレミス、ハイブリッド)、エンドユーザー産業別(製造業、小売業、その他)、地域別に分類されています。市場予測は金額(米ドル)で提供されます。

地域別分析

北米は2024年の売上高の37.5%を占め、高度な5Gカバレッジ、旺盛なベンチャー資金、NISTの国家IoT戦略などの連邦政府のイニシアティブに支えられています。米国の企業は、ゼロトラスト・セキュリティとAI対応アナリティクスを優先し、エンドツーエンドのポートフォリオを持つプロバイダーに有利な複雑なマルチタワー契約を推進しています。カナダはニアショアリングの動向と産業用IoTの近代化から恩恵を受け、メキシコはリアルタイムのサプライチェーン可視性に依存する国境を越えた製造回廊を活用しています。

アジア太平洋はCAGR 8.1%で最も急成長している地域です。中国は、製造業のデジタル化のために、多額のスマートシティ予算を割り当て、インダストリアル・インターネット・プラットフォームを推進しています。日本のSociety 5.0プログラムとシンガポールのSmart Nation構想は、コンプライアンス対応で拡張可能なソリューションに対する地域の需要を強化しています。インドの半導体およびAI政策は、対応可能な基盤をさらに拡大します。プロバイダーは、IoTプロフェッショナルサービス市場でこの勢いを生かすために、コスト競争力のあるデリバリーと文化的な深い連携、現地語サポートのバランスを取る必要があります。

欧州では、GDPR、EUサイバーセキュリティ法、各国のインダストリー4.0フレームワークなどに支えられ、コンサルティングや認証サポートに対するガバナンス主導の需要が創出され、着実な成長を維持しています。ドイツ、フランス、英国はデジタルツインプログラムに多額の投資を行い、東欧経済はEUの資金を活用してインフラの近代化を進めています。中東とアフリカはまだ始まったばかりだが、湾岸諸国がビジョン2030のスマートシティ・ポートフォリオを加速させており、ターンキーのプロフェッショナル・サービス・エンゲージメントを必要としていることから、将来性が期待されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- コネクテッドデバイスの普及とセンサーコストの低下

- 企業のデジタル変革ロードマップ

- 5Gとエッジコンピューティングの展開

- インダストリー4.0とスマートインフラに対する規制の後押し

- IoTサービスの成果ベースの価格モデル

- 統合需要を生み出すAI主導のAIOpsプラットフォーム

- 市場抑制要因

- データプライバシーとサイバーセキュリティへの懸念

- 相互運用性と規格の断片化

- 熟練したIoT人材の不足

- ハイパースケールクラウドワークロードのカーボンフットプリント精査

- サプライチェーン分析

- 規制情勢

- IoTエコシステム分析

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- マクロ経済要因が市場に与える影響

第5章 市場規模と成長予測

- サービスタイプ別

- IoTコンサルティング

- IoTインフラ・サービス

- システム設計と統合

- その他

- 組織規模別

- 中小企業

- 大企業

- 展開形態別

- クラウドベース

- オンプレミス

- ハイブリッド

- エンドユーザー業界別

- 製造業

- 小売り

- ヘルスケア

- エネルギーおよび公益事業

- 輸送と物流

- その他の業界

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- GCC

- トルコ

- イスラエル

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- IBM Corporation

- Accenture PLC

- ATandT Inc.

- Oracle Corporation

- Cognizant Technology Solutions

- Capgemini SE

- General Electric Company

- DXC Technology Company

- Tata Consultancy Services

- Wipro Ltd.

- Virtusa Corp.

- Infosys Ltd.

- Huawei Technologies

- Siemens AG

- Bosch.IO GmbH

- Tech Mahindra Ltd.

- PwC

- HCLTech Ltd.

- KPMG International

- Deloitte